The iShares S&P 500 Growth ETF ( IVW ) is trading at its highest P/E ratio since the dot com bubble burst while the outlook for sales and earnings growth is far weaker than it was than as a direct result of the growth the constituent companies have already seen.

Source: IVW: Growth Stocks Risk Being Victims Of Their Own Success

The index has benefitted due to the extrapolation of the strong earnings growth seen over recent years, particularly in the Tech sector. It is our view that many of IVW's main components are in bubble territory, relying on unrealistic growth trajectories to justify their valuations. As revenue and earnings growth slows, investors are likely to require significantly higher risk premiums on IVW than we currently see, regardless of the interest rate environment.

iShares S&P 500 Growth ETF

Source: Bloomberg

Investors Are Extrapolating Rapid Earnings Growth

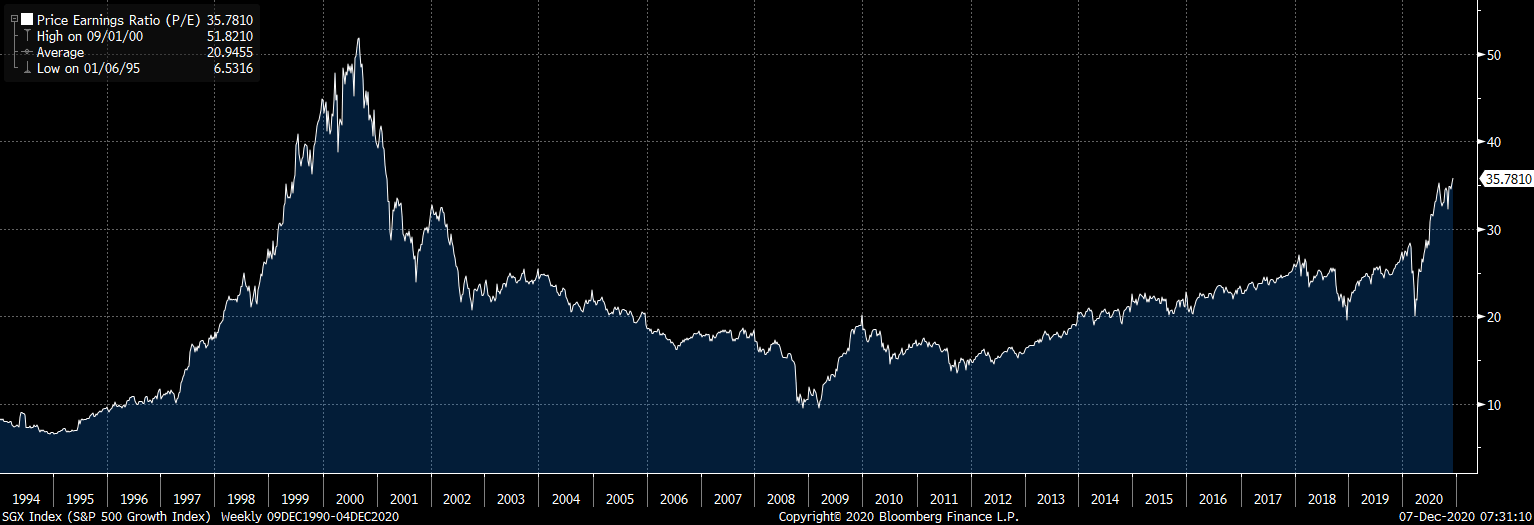

The underlying S&P 500 Growth Index (SGX) which the IVW tracks trades at a P/E ratio of 36x and offers a dividend yield of 1%, making it far more expensive than the overall SPX. Investors are implicitly anticipating much faster earnings expansion in these growth stocks compared to the overall market. However, earnings have already grown to such a high share of the overall market and economy that we think it will be difficult for them to continue doing so.

S&P 500 Growth Index

Source: S&P Global

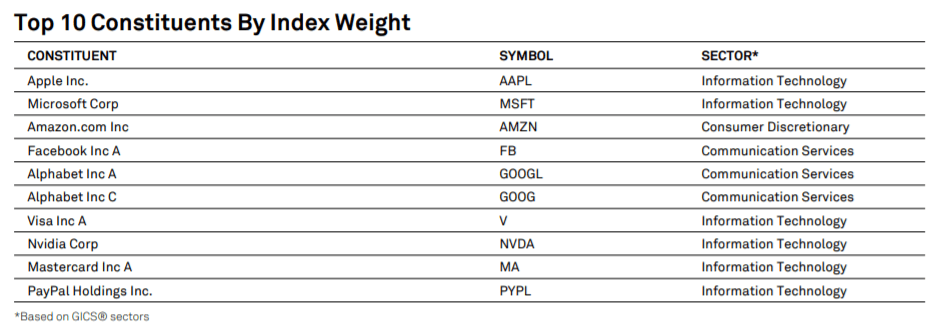

Total earnings of the SGX now account for 60% of the entire SPX. Furthermore, the 10 largest stocks in the index now represent over 40% of the index's entire value. These 10 stocks trade at a combined P/E ratio of 42x in anticipation of rapid future growth despite the fact that earnings already account for 22% of the SPX's entire earnings, up from just 8% 10 years ago.

These 10 growth stocks have seen earnings growth outstrip the SPX by almost 11% per year over the past decade, experiencing 15% nominal profit growth over this period. If this growth differential were to continue over the next decade then the profits of these 10 stocks would represent almost 60% of the SPX's total earnings. Extrapolating growth outperformance at such high levels of market share tends to result in unreasonably high assumptions, particularly considering that many of these companies compete with each other to some degree. Even if the growth advantage of these 10 stocks was cut in half it would still mean that profits would rise to almost 40% of the entire SPX by 2030.

Revenue Slowdown Highly Likely

We often here how these growth stocks are good investments because of the monopoly they have over their industries and the entrenchment of their services in our daily lives. The other side of the coin however is that the opportunity for revenue growth declines sharply once a large number of people have already bought your product. As we explained previously (see ‘NDX: A 75% Crash Should Surprise No One’) there is a wealth of evidence showing that revenues are a sharply declining function of market size. Apple (NASDAQ:AAPL) is a good example of this, with sales growth collapsing as its share of the industry has risen.

Three Headwinds For Profit Margins

In order for growth stocks to continue to expand earnings at a faster pace than the overall economy, we would likely need to see profit margins rise from already-high levels of 14%. However, there are a number of headwinds forming in terms of profit margins:

Potential for higher taxes: Declining tax payments have provided significant support to the bottom lines of the U.S.'s largest companies over recent years but there is now a threat of increased corporate taxes under a Biden presidency. While the proposed 28% corporate tax proposal may struggle to pass, the risks are certainly to the upside, while foreign governments are increasingly looking to get their share of tax revenues from the large Tech companies. On November 1 the U.K. implemented a 2% Digital Services Tax which will tax Google (NASDAQ:GOOG) (NASDAQ:GOOGL), Facebook (NASDAQ:FB), and Amazon (NASDAQ:AMZN) on the bulk of their U.K. revenues. France also looks set to go ahead with its 3% DST after failing to reach an agreement with the U.S. to avoid a potential beggar-thy-neighbour trade escalation.

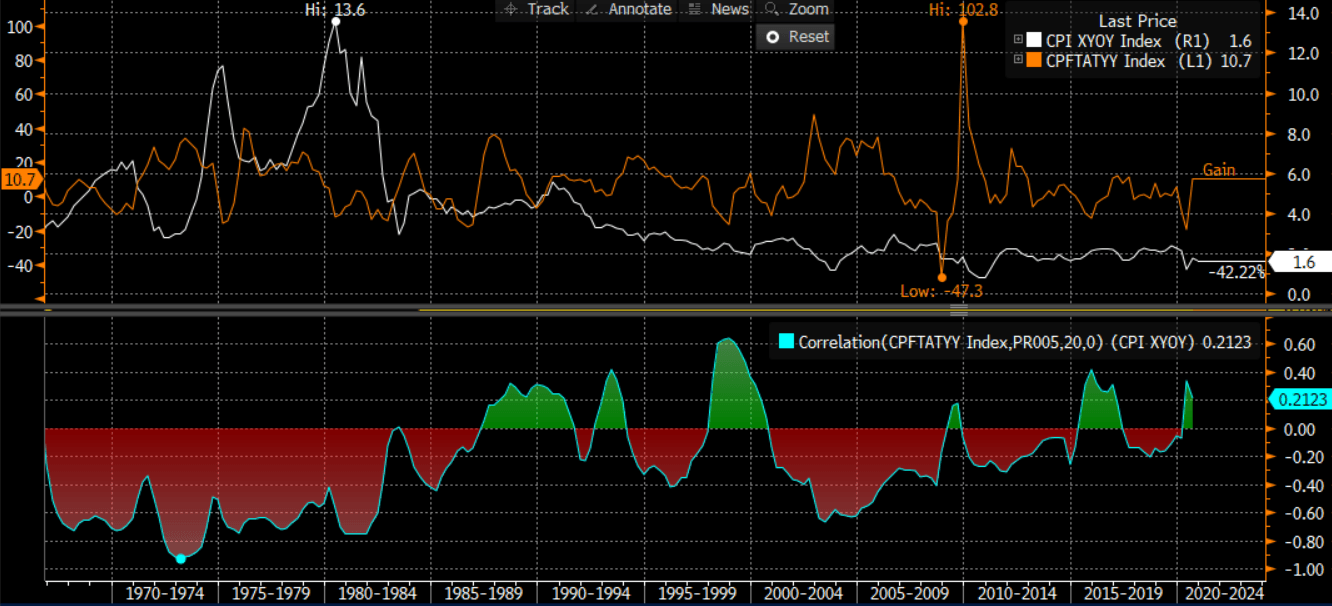

Rising inflation tax: Many analysts seem optimistic that high deficits under Biden will support economic growth over the coming years, but it is far more likely that nominal GDP grows at the expense of real GDP. When government spending is increasingly funded by money printing rather than taxes, the risk of inflation rises. As we can see from the chart below, rising inflation tends to be associated with falling profits even though it supports nominal GDP growth.

U.S. Corporate Profits Inversely Correlated With Inflation

Source: Bloomberg

Antitrust risks: One of the few areas of policy garnering bipartisan support in Congress is taking a tougher stance on regulating big Tech firms. The Wall Street journal noted last week that federal and state authorities, probing whether the tech giants abused their power in the internet economy, are preparing as many as four cases against Facebook and Google. According to the article, the authorities are preparing as many as four more cases targeting the two companies for abusing their power in the internet economy.

Realistic Growth Rates And Fair Valuations

When we consider that U.S. large cap stocks have consistently returned 7% real total returns over the past 100+ years from peak to peak and trough to trough, we believe that for the IVW to return historically-average returns with a 1% dividend yield we would need to see 6% real long-term earnings growth (assuming no change in the dividend payout ratio).

Regular readers will be aware of our negative outlook for U.S. long-term real GDP growth, which we expect to average no more than 1% over the next decade when measured from pre-Covid levels owing to a combination of declining working-age population growth and a continued decline in trend productivity owing to increased government and central bank interference in the economy. This means that in order for the IVW to deliver normal long-term returns we would likely need to see the country's largest Tech companies almost double their share of total profits over the next decade.

More likely in our view is that we see profit growth in the 10 companies mentioned above, and the IVW overall, post earnings growth rates just 1-2pp higher than the SPX and overall economy. In this case, fair value for the IVW works out to be around 75% below current levels, or a P/E ratio of below 10x, similar to those that prevailed at the 2009 low.

S&P 500 Growth Index

Source: Bloomberg

Low Rates Will Not Matter Once Risk Appetite Shifts

It is tempting to dismiss the above conclusion purely because of the fact that interest rates are low. We have shown however that there is no evidence at all that low interest rates prevent stocks from falling to fair value levels (see ‘Faith In The Fed's Ability To Support Stocks Is Unfounded’). As we saw as recently as March, as well as countless times throughout history, when the focus shifts from maximizing capital gains to minimizing capital losses, the level of interest rates is irrelevant to the marginal investor.

It is conceivable that real GDP growth comes in closer to 2% per year over the next decade compared to our 1% baseline case, while growth stocks may manage to grow earnings 3% faster than the entire economy rather than just 2%. However, even with these more optimistic growth assumptions, future returns would still be almost certain to come in lower then long-term averages owing to the extreme valuations we currently see.

Disclosure: I am/we are short IVW. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.