Introduction

The Global X Copper Miners ETF (COPX) is an ~$2bn valued ETF that covers a portfolio of 39 mining stocks that derive the majority of their revenue from copper mining or related activities. With copper futures currently trading at over $4.75 a pound, the highest level in years, there's some obvious excitement as to what producer margins could look like, particularly as mine capacity utilization rates are still below the ~85% levels seen during the pre-pandemic era of 2018 and 2019. Having said that, I believe it's also important not to disregard some of the recent political changes in the integral Latin American belt that could perhaps put a lid on some of the largesse these miners could likely accrue further down the line.

The Winds of Change in Latam Should Not be Ignored

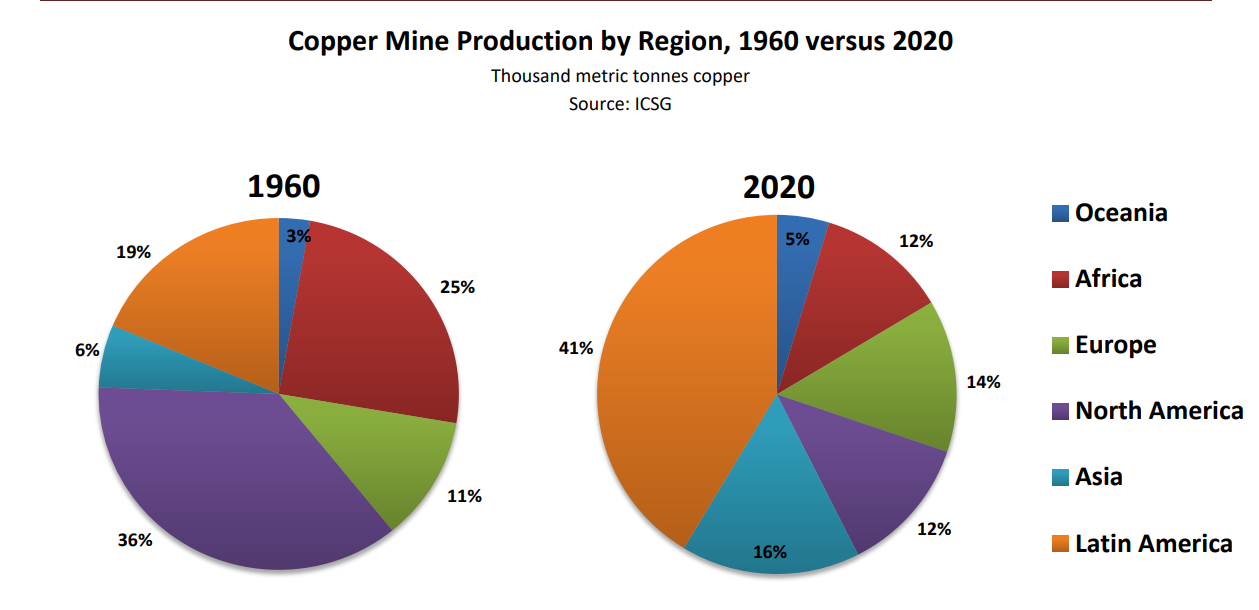

Over the years, the Latin American region has taken on a more prominent role in the mining of copper; over 60 years back, copper mine production from this region was only around 750,000 tonnes, accounting for 19% of total global production; in recent years, production has been closer to 8.5m tonnes, representing a whopping 41% of global production, and comfortably ahead of other geographic regions.

ICSG

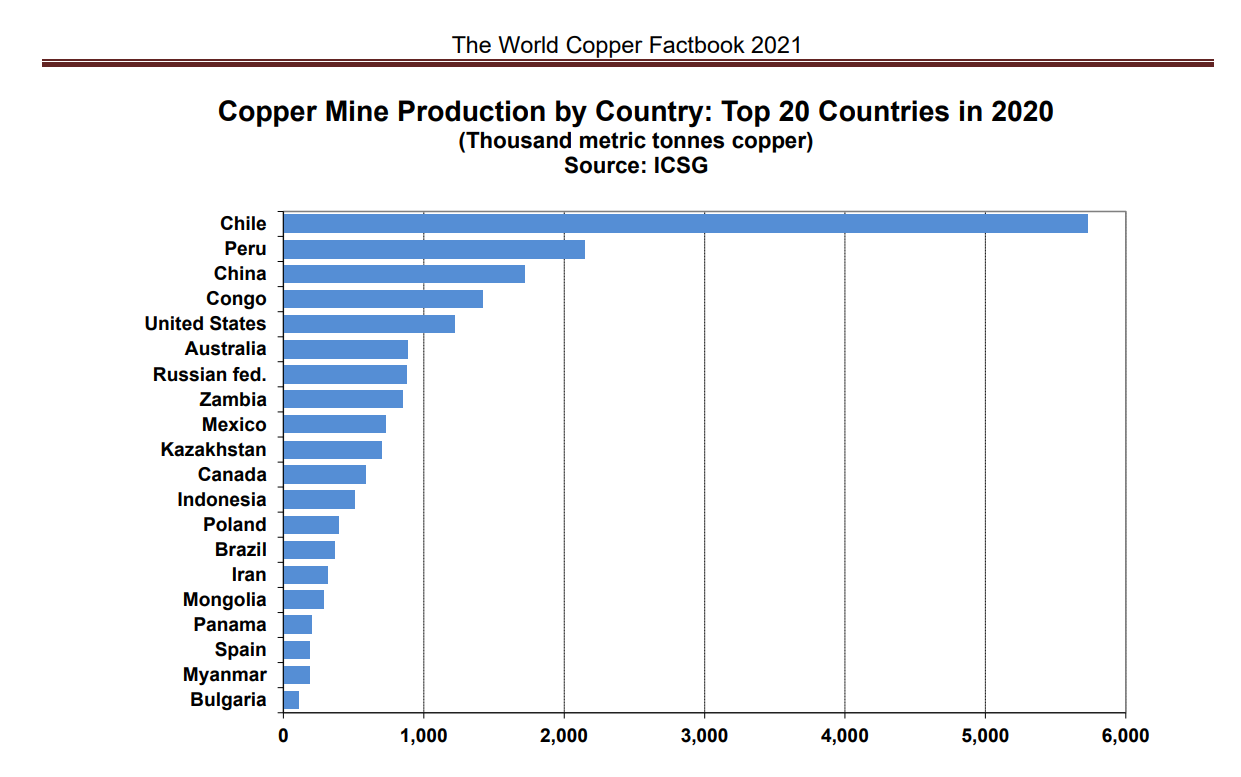

Within Latam, two regions, in particular, stand out; Chile which accounts for a third of global copper mine production, and Peru which accounts for 10%.

ICSG

Unsurprisingly, the bulk of COPX's top 10 holdings have significant mining operations within these two regions, so clearly, developments here (particularly in Chile), will likely weigh heavily on the fortunes of these stocks. Both countries have recently come through elections and we've seen the political landscape being dominated by more leftist hues; this does not bode well for the long-term prospect of mining companies.

In Chile, former student activist – Gabriel Boric came out on top, driven mainly by his rhetoric against Chile's market-oriented economic model that may have boosted the country's economic progress over the years but has also led to widescale social inequalities. Chile is currently in the midst of rewriting its constitution and also preparing a new bill to ramp up royalties on copper and link it to global copper prices. Basically, what you're likely to see are some fairly stringent measures that will attempt to transfer any excess wealth that mining firms generate towards various socialistic programs.

Some proposals that are being debated include levying a profitability tax on the operating profits of copper mining firms whilst also implying sales tax of around 3% on gross copper sales (note that even if these companies aren't in the black, they will still be expected to pay taxes). Needless to say, if some of these provisions eventually come through, Chilean-based copper miners are unlikely to get the full benefits of the secular demand-based tailwinds that are currently brewing in the copper industry.

The new Chilean constitution will also look to place more encumbrances on miners; for instance, water use may be restricted, or only temporary rights granted, in place of previously granted permanent water use rights. There are also intentions to annul previous mining concessions granted on indigenous land (even if these concessions are potentially reinstated, you would think that the mining community may be prompted to provide some pecuniary benefits to the indigenous communities). There are also strong suggestions that the Chilean government will look to nationalize mines in order to boost the fiscal position, providing only minimum or no compensation! This may well end up being just a one-off, but do also consider that Chilean-based miners struggled with production in January, which was incidentally the weakest reading in 11 years!

In Peru as well, the political landscape looks very uncertain (there have been four different cabinets over the last six months and the recently appointed mining minister is not perceived to have strong links with the private sector) even as the country is being run by the leftist based-Pedro Castillo. Admittedly, one of Castillo's initial proposals to increase mining taxes was rejected by the Peruvian Congress, but given his left-leaning intentions, don't expect this to be the end of it. It's also worth noting that mining firms in Peru have had a hard time placating indigenous communities and ongoing protests there have disrupted production.

All in all, there currently appears to be a lot of regulatory and political uncertainty in the Latam region; the questionable investment climate there means some of COPX's Latam-based constituents may need to reorient their investment and production plans. The likes of FCX and LUNMF are currently sitting on the fence and waiting for greater clarity to emerge.

Closing Thoughts

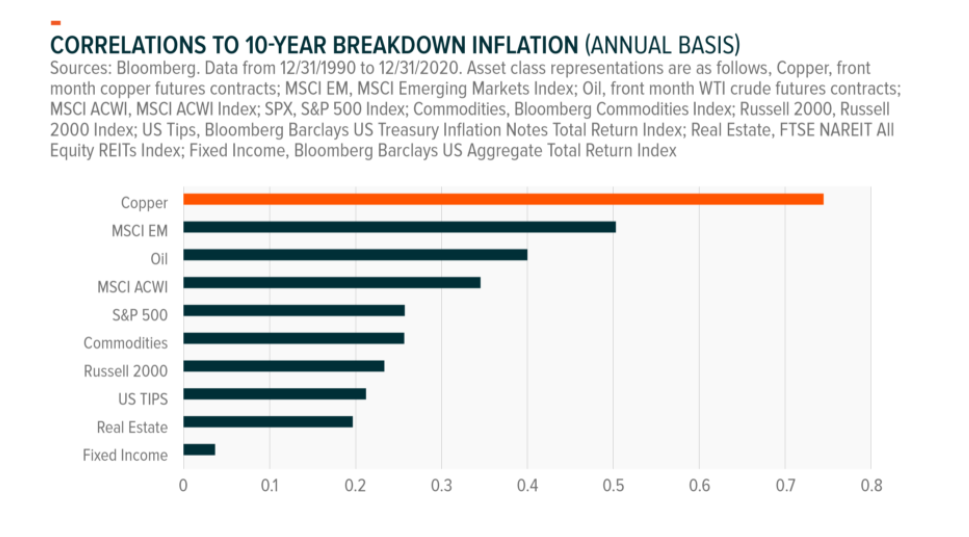

The slowdown of China over the last few months is no doubt a concern for the prospect of copper, but recent factory and construction activity reports there show some form of stabilization. There are also signs that reforms such as the “property tax” could be stalled for now whilst further stimulus measures will be implemented there. Ongoing geopolitical tensions and the associated sanctions on Russia (the 7th largest copper producer in the world) could disrupt the supply side dynamics even more. Note that copper inventory levels are currently at rather lowly levels of less than 73000 MT. Meanwhile, the metal also continues to benefit from rampant inflation expectations, as exemplified by the high correlation with the 10-year breakeven rate.

Global X

Then longer term, given the ongoing proliferation of EVs in the broad auto sales mix, a broad copper-focused decarbonization pivot, and a burgeoning “green energy” narrative across the world, you'd think this metal has the right ingredients to embark on a potential super-cycle.

Clearly, there's a lot to like about copper, but given some of the developments I've touched upon in the previous section, I'm not too sure, COPX is the most optimal way to generate alpha at this juncture, particularly as the relative strength ratios and the valuation picture implies unappealing risk-reward.

Since the 2020 lows, COPX's price has also expanded by nearly 5x, and if you compare COPX to an ETN that covers the Bloomberg Copper Subindex Total Return (JJC), things look rather elevated with limited value on offer.

StockCharts

Also, do note that currently, COPX does not appear to have much of an edge when you juxtapose it against a more diversified play such as the iShares MSCI Global Metals & Mining Producers ETF (PICK). PICK is an ETF that covers miners involved in not only copper but also diversified metals and mining, aluminum, steel, precious metals, etc.

StockCharts

COPX currently trades at a forward P/E multiple of 9x, whereas PICK trades at a ~22% discount of 7x. The income angle too is more compelling here with PICK offering a yield of over 5% almost 5x as much as COPX's corresponding figure of 1.25%.