RPV holds 85 S&P 500 stocks with “pure value” characteristics. The heaviest sector is financials, with 22% of asset value. It has recently outperformed the S&P 500, but return since inception is underwhelming. Volatility and drawdowns point to high risk. Two shortcomings of value indexes.

Invesco S&P 500 Pure Value ETF: A Very Volatile Value ETF (RPV)

This ETF article series aims at evaluating products regarding the relative past performance of their strategies and quality metrics of their current portfolios. As holdings and weights change over time, updated reviews are posted when necessary.

RPV strategy and portfolio

The Invesco S&P 500 Pure Value ETF (NYSEARCA:RPV) has been tracking the S&P 500 Pure Value Index since March 2006. It has 87 holdings, an expense ratio of 0.35% and a 12-month distribution yield of 2.03%.

As described in the prospectus by Invesco, S&P 500 stocks are assigned two scores for value and growth. The value score is based on three ratios: book-value-to-price, earnings-to-price, and sales-to-price. The growth score is based on the three-year sales per share growth, the three-year earnings yield change, and the 12-month share price return. The S&P 500 Pure Value Index selects stocks with the best value score, excluding those demonstrating both value and growth characteristics. Constituents with higher value scores receive greater weights.

In this article, RPV will be compared to the iShares S&P 500 Value ETF (IVE) and the SPDR S&P 500 ETF (Original Post>

Regarding the usual valuation ratios, RPV is much cheaper than IVE, which is cheaper than SPY:

| RPV | IVE | SPY | |

| Price/Earnings TTM | 8.84 | 18.75 | 19.02 |

| Price/Book | 1.1 | 2.63 | 3.59 |

| Price/Sales | 0.54 | 1.86 | 2.26 |

| Price/Cash Flow | 4.99 | 13.85 | 14.19 |

Source: Fidelity

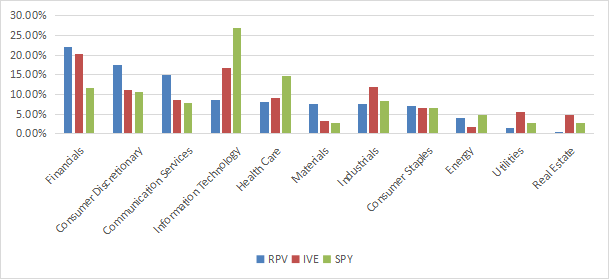

The heaviest sector is financials, with 22% of asset value. Compared to IVE and SPY, RPV overweights financials, consumer discretionary, communication and materials. It underweights technology, industrials, healthcare, utilities and real estate.

RPV holds 85 stocks. The top 10 holdings, listed in the next table, represent 24.3% of asset value. The heaviest one weighs 3.7%, so risks related to individual stocks are moderate.

| Ticker | Name | Weight% | EPS growth% | P/E TTM | P/E fwd | Yield% |

| PARA | Paramount Global | 3.68 | -8.44 | 5.21 | 12.81 | 3.93 |

| LUMN | Lumen Technologies, Inc. | 3.03 | 380.64 | 2.68 | 3.67 | 0 |

| DISH | DISH Network Corp. | 2.60 | -27.56 | 4.95 | 5.63 | 0 |

| GM | General Motors Co. | 2.36 | -8.59 | 6.41 | 6.53 | 0.92 |

| MHK | Mohawk Industries, Inc. | 2.31 | -83.55 | 48.11 | 9.59 | 0 |

| WBD | Warner Bros. Discovery, Inc. | 2.27 | -190.10 | N/A | N/A | 0 |

| KMX | CarMax, Inc. | 2.03 | -50.94 | 21.32 | 26.48 | 0 |

| WRK | WestRock Co. | 2.03 | -3.06 | 10.92 | 9.31 | 3.21 |

| C | Citigroup, Inc. | 2.02 | -30.69 | 7.46 | 8.69 | 3.91 |

| F | Ford Motor Co. | 1.97 | 205.19 | 6.24 | 7.04 | 4.35 |

Since inception (03/01/2006), RPV has lagged SPY by 49 bps in annualized return, and it beats IVE by 111 bps. It shows a much higher risk than the two other funds in drawdown and volatility (standard deviation of monthly returns).

| Total Return | Annual Return | Drawdown | Sharpe ratio | Volatility | |

| RPV | 313.28% | 8.76% | -75.32% | 0.43 | 23.27% |

| IVE | 247.55% | 7.65% | -61.32% | 0.46 | 16.47% |

| SPY | 346.08% | 9.25% | -55.19% | 0.57 | 15.71% |

Data calculated with Portfolio123

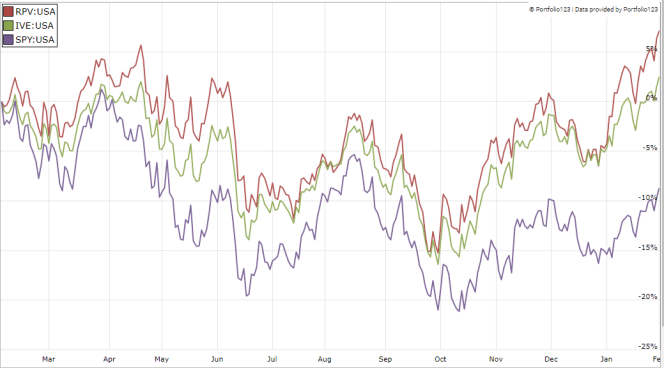

However, RPV has outperformed in the last 12 months:

Comparing RPV with my Dashboard List model

The Dashboard List is a list of 80 stocks in the S&P 1500 index, updated every month based on a simple quantitative methodology. All stocks in the Dashboard List are cheaper than their respective industry median in Price/Earnings, Price/Sales and Price/Free Cash Flow. After this filter, the 10 companies with the highest Return on Equity in every sector are kept in the list. Some sectors are grouped together: energy with materials, communication with technology. Real estate is excluded because these valuation metrics don't work well in this sector. I have been updating the Dashboard List every month on Seeking Alpha since December 2015, first in free-access articles, then in Quantitative Risk & Value.

The next table compares RPV performance since inception with the Dashboard List model, with a tweak: the list is reconstituted quarterly to make it comparable to a passive index.

| Total Return | Annual Return | Drawdown | Sharpe ratio | Volatility | |

| RPV | 313.28% | 8.76% | -75.32% | 0.43 | 23.27% |

| Dashboard List | 462.15% | 10.75% | -55.38% | 0.55 | 19.71% |

Past performance is not a guarantee of future returns

The Dashboard List outperforms RPV by 2 percentage points in annualized return, and it looks much safer regarding drawdowns and volatility. A note of caution: ETF performance is real, whereas the list is simulated.

Fundamental shortcomings

Most value indexes have two shortcomings in my opinion, and RPV is no exception. The first one is to rank stocks in the whole universe. It means valuation ratios are considered comparable across all sectors. Obviously they are not: you can read my monthly dashboard here to go deeper into this topic. It results in overweighting financials, whose valuation ratios are naturally cheaper. Some other sectors are disadvantaged, especially technology.

The second issue comes from the price/book ratio (P/B), which adds some risk in the strategy. Historical data show that a large group of companies with low P/B has a higher probability to hold value traps than a same-size group with low price/earnings, price/sales or price/free cash flow. Statistically, such a group will also have a higher volatility and deeper drawdowns in price. The next table shows the return and risk metrics of the cheapest quarter of the S&P 500 (i.e.125 stocks) measured in price/book, price/earnings, price/sales and price/free cash flow. The sets are reconstituted annually between 1/1/2000 and 1/1/2023 with elements in equal weight.

| Annual Return | Drawdown | Sharpe ratio | Volatility | |

| Cheapest quarter in P/B | 8.54% | -81.55% | 0.35 | 37.06% |

| Cheapest quarter in P/E | 10.71% | -73.62% | 0.48 | 25.01% |

| Cheapest quarter in P/S | 12.82% | -76.16% | 0.47 | 34.83% |

| Cheapest quarter in P/FCF | 15.32% | -74.77% | 0.61 | 27.03% |

Data calculated with Portfolio123

This explains why I use P/FCF and not P/B in the Dashboard List model.

Takeaway

RPV tracks a large cap value index based on three valuation metrics, including the book value to price. It has lagged the parent index S&P 500 since 2006, and it shows a much higher risk regarding volatility and drawdowns. It is also significantly more volatile than the S&P 500 Value Index. The “pure value” strategy overweights financials, with 22% of asset value. I think there are two shortcomings in its strategy: it ranks stocks regardless of their sectors, and the price/book ratio has a bad track record. An efficient value model should compare stocks in comparable sets, like my Dashboard List. This model prefers price/free cash flow to price/book, and a simple profitability rule helps filter out some value traps.