2023 Rally

The drumbeat about disconnect between fundamentals and year-to-date asset price moves is getting a bit louder. Investment Grade bonds is one area where this question has been raised on numerous occasions (especially against the backdrop of potential shifts in inflows due to personnel/policy changes in the Bank of Japan). The issue was also mentioned in discussions about China, where the surprising re-opening timeline and the policy U-turn in the real estate sector spurred a huge rally 3.5 months ago. Even though many investors stayed on the sidelines (after being hit in 2022), there is a view that actual economic releases – domestic activity, and especially the housing sector recovery – should start “delivering” (rather than just “promising”) for the rally to continue. So, the next batch of China’s activity gauges (out next week), will invite extra scrutiny.

Central Banks Policy Message

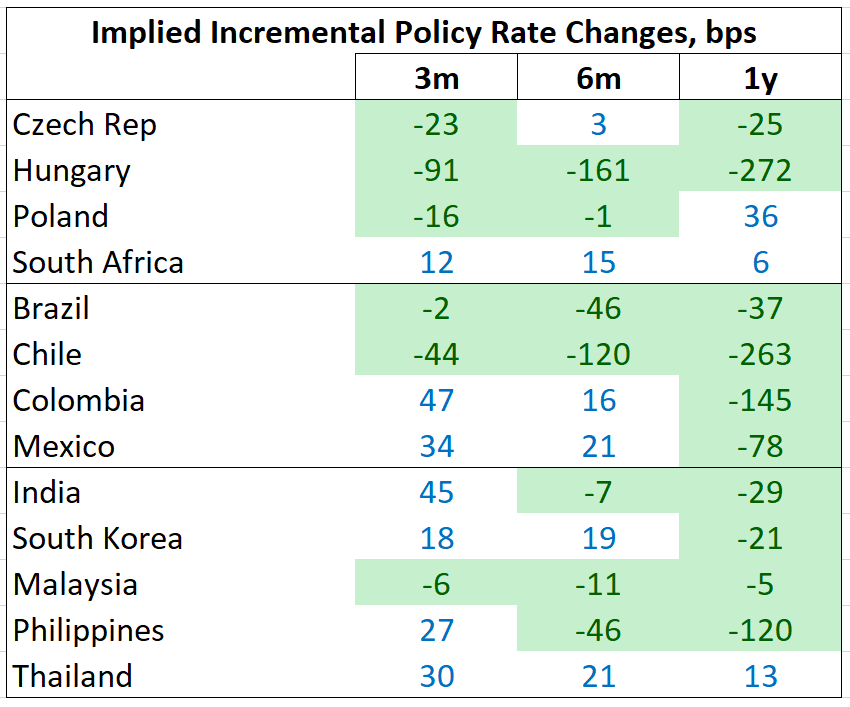

An important aspect of this story is whether central banks’ messaging/guidance is in alignment with the market expectations for policy rates. The gap between the two in the U.S. started to narrow lately – Fed Funds Futures now price in additional 25bps hikes in March and May (and a 54% probability of another hike in June), with implied H2 rate cuts reduced to 20bps. The market expectations for emerging markets (EM) do not look overly aggressive (maybe with a couple of exceptions, like Hungary or Chile, where local swap curves continue to price in north of 400bps of rate cuts in 2023 – see chart below). Is it because the post-pandemic policy response in EM was – largely – timely and credible, and EMs did not have to chase the Fed this time around?

EM Rate Cuts And Disinflation

The current policy signal in EM is clear and simple – the tightening cycle might be ending, but the bar for rate cuts is very high. Uruguay’s central bank stayed on hold yesterday, but noted that the policy rate path will depend on the normalization of inflation expectations. Indonesia’s central bank also kept the policy rate unchanged, expecting that inflation will return to the target range in H2-2023. In the meantime, the central bank decided to employ several instruments to support the currency and make sure local yields remain attractive. The Philippine central bank followed in Mexico’s footsteps, delivering a larger than expected overnight deposit facility rate hike (+50bps) after January’s huge upside inflation surprise. A meaningful upward shift in the central bank’s 2023 inflation forecast opens the door for further tightening in the coming months. As you can see, individual EM circumstances might vary, but a cautious policy bias should provide a cushion against the more hawkish Fed in the months to come. Stay tuned!

Chart at a Glance: EM Rate Cut Expectations – Not Too Outrageous

Source: Bloomberg LP.