Taiwan Semiconductor reported a weak quarter as the semiconductor sector remains under pressure.The chip company continues to aggressively invest on signs of a chip bottom and signals from customers of strong future demand.Warren Buffett sold shares on geopolitical fears, yet signs suggest Berkshire should've loaded up on cheap shares.The stock is cheap at 13x '24 EPS targets.

Taiwan Semiconductor Stock: Buffett Should've Bought More (NYSE:TSM)

Even despite the massive ongoing pressure on semiconductor demand, Taiwan Semiconductor Manufacturing Company Limited (NYSE:TSM) reported a magnificent March quarter. The company guided towards a bottom in the current quarter as the stock rallied on weak guidance, suggesting Buffett and Berkshire Hathaway (BRK.B, BRK.A) were wise to start loading up on the stock in the $80s. My investment thesis remains ultra Bullish on the stock heading into another up cycle in the semiconductor space in the 2H'23.

Strong Business Model

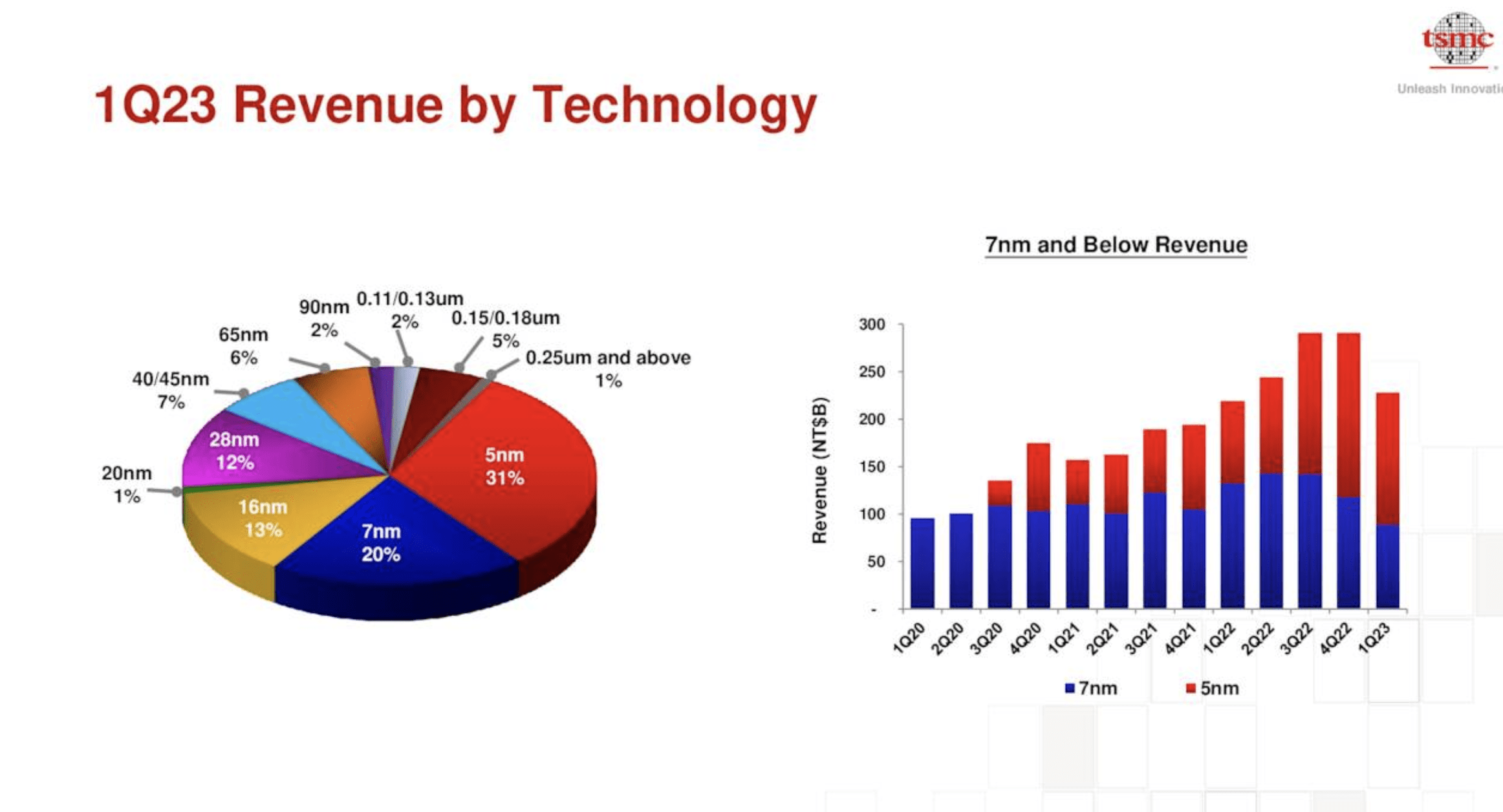

The Q1'23 results highlight why Buffett originally picked TSMC for an investment. The semiconductor company reported operating margins approaching 50% with half of the business focused on advanced chip production in the 5nm and 7nm process technology levels.

TSMC reported Q1 revenues fell 4.8% from $16.9 billion level reported last year. The business is struggling as customers pull back from high inventory levels with lower demand. The PC market fell 29% in Q1 in a sign of how weak end-user demand has been following Covid pull forwards back in 2020 and 2021.

Despite the business being under pressure, TSMC reported impressive 45.5% operating margins, though down 6.5 percentage points from the Q4 levels. The company has a massive profit machine and TSMC generally is seen with a strong moat over top competitor Intel (Original Post>

TSMC still forecasts spending an impressive $32 to $36 billion on capex this year after spending ~$10 billion in Q1. The quarterly spending rates will naturally dip to only around $8 billion for the last 3 quarters of the year.

The chip company guided to Q2'23 revenues of between $15.2 to $16.0 billion, down another 6.7% sequentially. The sequential revenue hit will push operating margins lower with a goal of still topping a massive 40% margin in the quarter despite the weakness.

The key here is the big moat and why Warren Buffett was originally attracted to this investment before quickly dumping the stock. Even under the worse case scenario, TSMC forecasts a 40% operating margin while Intel only guided to 39% gross margins for Q1 while free cash flows will turn negative.

The US chip giant even cut capex spending to around $20 billion with capital offsets of up to 30% from government assistance programs including the CHIPS Act. TSMC is forecasting spending $12+ billion in extra capex in 2023 placing the Taiwanese company in a far bigger lead in the chip manufacturing sector.

On the Q1'23 earnings call, the CEO was clear the spending is warranted based on long-term capacity demand of customers:

With this level of CapEx spending in 2023, we reiterate that TSMC remains committed to a sustainable and steadily increasing cash dividend on both an annual and quarterly basis. We will continue to work closely with our customers to plan our long-term capacity and invest in leading edge, and specialty technologies to support their growth while delivering profitable growth to our shareholders.

TSMC actually faces supply shortages for modern N3 chips due to high demand in AI, 5G and other technology areas. While some areas face high inventories, customers such as Nvidia (NVDA), Apple (AAPL) and Qualcomm (QCOM) demanding more modern chips in short supply.

Geopolitical Fears

Per a CNBC interview, Buffett appears to have sold TSMC after rethinking the political risks of owning a business headquartered in Taiwan. China has definitely ramped up rhetoric towards taking over the small island, but the risks still appear small in this case.

The latest Chinese news suggests Chinese leader Xi Jinping wants to be a global peacemaker. He has worked to broker peace deals in both Ukraine and with Middle East rivals Iran and Saudi Arabia. A military conflict in Taiwan would set back the economic ambitions of China by decades leaving the country without access to modern chips likely leaving the reunification of the island without benefit.

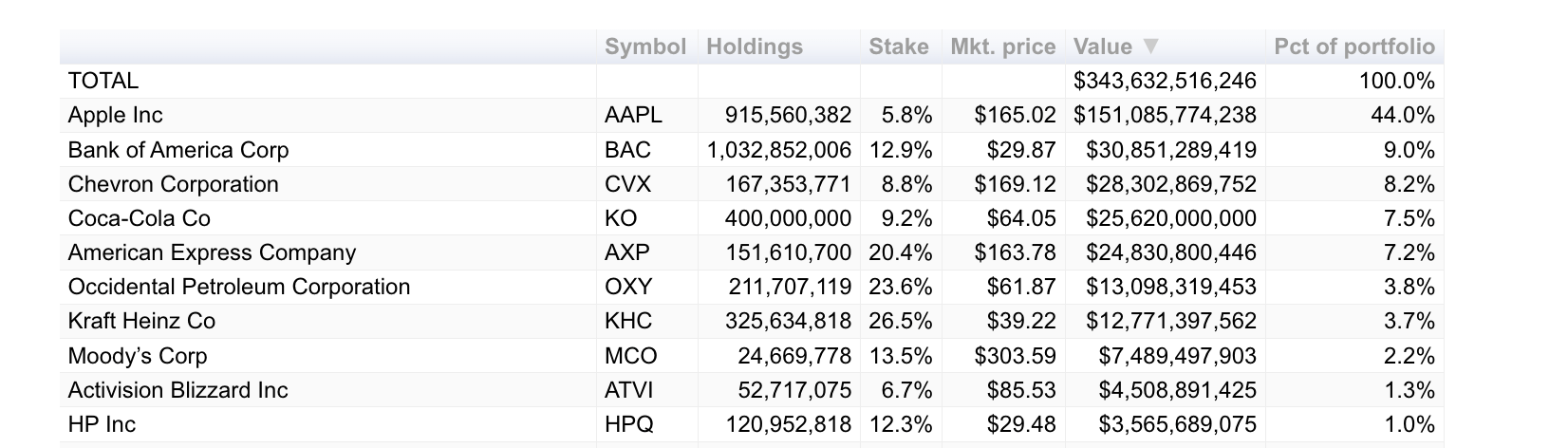

The odd part of the Buffett call to sell TSMC is that Apple (AAPL) is by far the largest position in the Berkshire portfolio now. The investment firm has an incredible 44% of their $345 billion portfolio in Apple with an ownership position of over 915 million shares.

The tech giant is moving away from China with an aggressive push into retail stores and manufacturing facilities in India to reduce the risk of a focus on the Communist country. If anything, Apple possibly has a higher concentration risk to China than TSMC does to Taiwan and China.

According to recent reports, Apple still has up to 95% of iPhone production in China focused around iPhone City. The tech giant was hit hard by Chinese covid shutdowns at the end of 2022, but Reuters has reported that Apple has reduced the supplier reliance on China to only 36%. Though, Apple still appears to have the vast majority of products built within in China based on JPMorgan estimating a goal for 25% of Macs, iPads, Apple Watches and AirPods, will be manufactured outside China by 2025 versus only 5% now.

Any move by China to militarily invade Taiwan will impact the ability of Apple to have goods manufactured in China. TSMC is building new fabs in the U.S., Japan and potentially the EU in order to reduce the risk of the business focus on just Taiwan similar to how Apple is moving manufacturing away from Foxconn in China.

TSMC even suggests the political uncertainty should allow the chip giant to sell those chips produced outside Taiwan at a premium valuation to match the perceived value of having such production outside of the influence of China:

The overseas fab is indeed the cost is higher, at least in the first several years. And we stated last time that some of the components like the construction costs may be as high as 5x. Now the way to mitigate that, first of all, it's — it represents our global expansion represent a value to the customers, then we will be selling that value as well.

Whatever TSMC earns this year is relatively irrelevant. The inventory correction will bottom in Q2 and bleed over into Q3 numbers, but the chip company will ultimately rebound to exit 2023 back in growth mode.

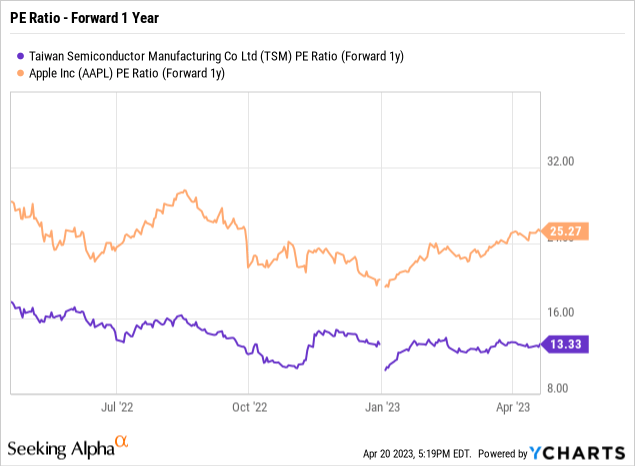

The management team has discussed a long-term growth target of 15% to 20% setting up a path to the $6.60 EPS target of analysts for 2024. The stock is very cheap at 13x the 2024 EPS target, especially with an AI chip boom on the way.

If anything, TSMC trades at a 50% discount to Apple despite having the same geopolitical risk. In addition, TSMC has vastly higher growth rates forecast in the years ahead while Apple is facing a slow growth scenario due to scale and the lack of new products.

Takeaway

The key investor takeaway continues to suggest China won't invade Taiwan when the country impacts the global economy to such an extent that China will face a severe economic backlash from such a move. The market shouldn't assign a risk premium to TSMC when Apple faces a similar risk of production disruptions in both Taiwan and China.

If anything, Buffett should've loaded up on TSMC and ditched Apple in the process due to the premium valuation multiple and reality that the tech giant faces similar geopolitical risks.