Investment Thesis

I recommended Teck Resources Limited (NYSE:TECK) because of two catalysts that are in play.

- The company may still perhaps be acquired in whole or in part by Glencore (OTCPK:GLCNF).

- Demand for copper will increase with time, and there's not enough supply coming online to support copper demand in the next two years.

The news of Glencore's interest in Teck has died down. But I believe that Teck's actions in the past 6 months have demonstrated that they are intent on spinning out or restructuring their operations to shed their coal business and become a pure-play copper operation. Simply put, this is a classic Joel Greenblatt setup. The company has something extraordinary happening, but for now, we'll have to wait to see what ultimately takes place.

Teck Resources is my preferred copper company. If either copper prices firm up in the next two years or Teck Resources is bought out, either way, investors will see a premium to the current share price of approximately $44 per share. I'm looking to get 40% to 50% by the end of 2024.

Why Invest in Copper

Copper is needed for the electrification of the world. In the global pursuit of electrifying the energy transition and reducing carbon emissions, copper has emerged as a critical element. The transition to renewable energy sources, such as solar and wind power, necessitates a massive expansion of electrical infrastructure, from power generation facilities to transmission lines and energy storage solutions.

Copper, with its excellent electrical conductivity and reliability, plays a pivotal role in enabling the efficient and seamless flow of electricity across these systems.

One of the most significant applications of copper lies in renewable energy generation. Solar photovoltaic (PV) panels and wind turbines heavily rely on copper wiring.

Moreover, the electrification of transportation is another key aspect of the energy transition. The wider the adoption of EVs, the more need for copper in charging systems. The growth of EV adoption, along with the rise of energy storage systems like batteries, think lithium – think Albemarle (ALB) – underscores the importance of copper.

Copper's role in wiring infrastructure is nothing short of essential, especially in the transmission process.

One of the primary challenges in renewable energy generation is that many of the best locations for solar and wind farms are often situated far away from major cities and urban centers, where electricity demand is high.

As a result, the electricity generated needs to be transmitted over vast distances to reach its intended consumers.

As the world increasingly turns to renewable energy sources, and nuclear energy (think Cameco (CCJ), Uranium Energy Corp. (UEC)), the demand for copper in power transmission systems will continue to grow, playing a pivotal role in achieving a more sustainable and electrified future.

Why Teck Resources?

Teck Resources is in the midst of corporate action. The business wanted to spin off its coal business after it spun off the rest of its energy business in 2022.

Here's a quote from the shareholder letter echoing this action:

We continue to explore a range of options to realize the full potential of our world-class base metals business [copper business].

Meanwhile, the biggest takeaway from the quarter was that copper production guidance for 2023 was reduced by 16%, driven by further ramp-up delays at QB2 (one of the world's largest undeveloped copper mines). More specifically, Teck reduced 2023 copper production guidance to 330-375kt from 390-445kt.

However, Teck Resources reaffirms its previous 2024 production guidance from QB2. In other words, there are some minor ramp-up issues that Teck Resources expects to tackle soon and get back on track in the coming few months.

Q2'23 free cash flow was negative C$369 million on the back of higher capex use in the quarter, together with lower cash flows produced this quarter, relative to the same period a year ago.

How Should Investors Think About Teck?

There's a bit of a wait-and-see outcome for Teck Resources. I believe that the downside of this investment is muted if my two catalysts fail to work.

And I'm hoping to see the stock re-rating higher 40% to 50% by the end of 2024. Why?

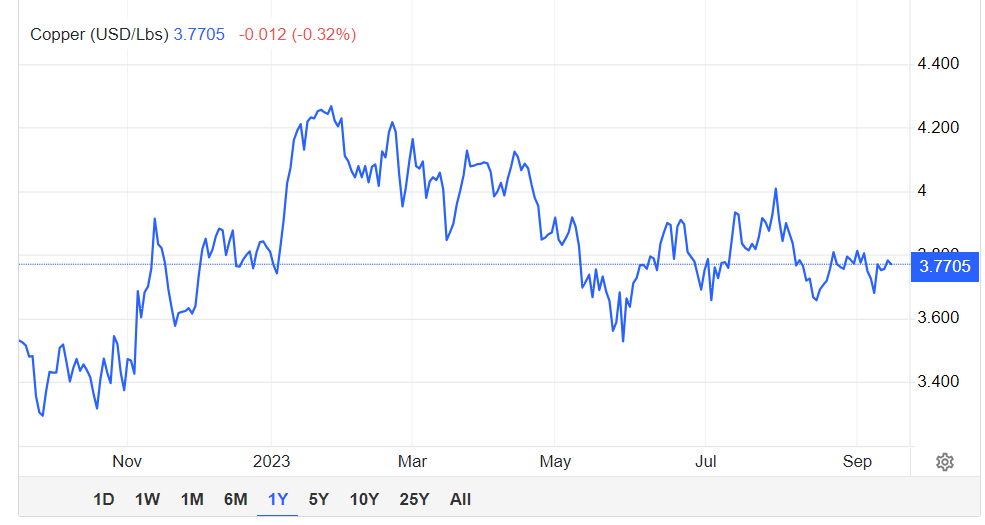

Trading Economics

Copper prices are firming up. That is, despite demand for copper from China being widely reported as being subdued. In other words, notwithstanding the subdued growth from China, copper demand from other countries is clearly strong enough. And what about when China's growth returns? That will further increase the demand for copper.

The Bottom Line

I recommended Teck Resources due to two potential catalysts: The possibility of an acquisition by Glencore; and the increasing demand for copper with limited supply coming online in the next two years.

Teck's actions to restructure its operations and focus on becoming a pure-play copper company are a key catalyst here, worthwhile waiting for. While Glencore's interest has subsided, Teck reaffirms that it's seeking to pursue all options.

Teck's future remains promising as it plays a pivotal role in the electrification of the world.

Copper's excellent electrical conductivity is essential for renewable energy generation and transmission processes, supporting the global energy transition.

With Teck's ongoing corporate actions and a potentially muted downside, investors might see the stock appreciate significantly by the end of 2024.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.