Covered call ETFs are becoming increasingly popular among retirement income investors.But as valuable as these vehicles are, they can be even better if you put some good players around them.I outline in detail how I supplement covered call ETFs with offense and defense ETF “tilts” to create and maintain a flexible, dynamic retirement portfolio for my family.

Exchange-traded funds, or ETFs, that write covered calls are emerging as a go-to core piece of retirement income portfolios, as well as for more risk-intolerant (e.g., conservative) investors. In my article back on August 30, I introduced an approach I take to managing around a core covered call ETF position. And the longer the stock and bond markets' recent rangebound trading continues, the more attractive covered call ETFs look. Returns will be more of a grind-it-out process in the future, as compared to the zero-interest-rate-policy (ZIRP) era we just had.

This “calls” for a modern approach (pun intended): covered call ETFs at the core

Thanks to many outstanding and well-meaning comments on that earlier article, I have a good idea what to focus on next. So, let's take that initial discussion a step further. Because it is now obvious to me that the Seeking Alpha audience is already highly-invested in this strategy, and there is strong interest in learning more, including ways to complement that covered call position, to make it a true anchor of a long-term portfolio.

This article focuses more on process and less on picks. In other words, my goal is to show how to apply the strategy I use around covered call ETFs. Know that it can be used with any covered call ETF. And with more than 200 ETFs now using options to protect and/or enhance their returns, I think this process is a timely one to share. It is based much more on a forward-looking view of markets that is lower-return/higher risk than what we have had the past 15 years, where the SPDR® S&P 500 ETF Trust (NYSEARCA:SPY) produced a superb annualized return of 11%.

But the past is the past. We can't own it. What we can do is to evaluate the market we have now, and contemplate and plan for future episodes of both harsh declines in the broad market, and periods of high return in bull markets. Because most, if not all covered call ETFs can be great core investments, but a little help around the edges can make them even more powerful core investments.

Grind it out!

In a “grind out returns” environment as opposed to what we've had for most of the period since the Global Financial Crisis in 2008, complicated by the mixed blessing of higher interest rates, yet higher inflation and exploding consumer and government debt, I see this as as potential modern “core and satellite” approach for investors. It certainly has been for me, as I honed it during the three years since I sold my investment advisory practice after 27 years in that industry, to “retire” and focus on investment research and investor education, with a focus on making ETFs easier to analyze, understand, and create effective portfolios with.

So, let's quickly review where the stock market appears to be now, and then I'll show a somewhat generic example of how to take that next step, use the covered call ETF as the portfolio core, but add a couple of pieces around it that have made me more comfortable holding them for longer periods of time.

The “Stuck Market” and the opportunity it brings for income and risk-management

The stock market is more like a stuck market. The broad market indexes are caught in a trading range. The same goes for many individual stocks and sectors. The middle part of this year brought a furious rally, driven by the Artificial Intelligence craze, the Fed flooding the system with liquidity to help regional banks get off the mat, among other factors.

But as the S&P 500 and Nasdaq sped toward their all-time highs, the train slowed down. It is as if the market feels a true breakout is unwarranted, but a steep decline is not yet justified. Given the explosion of covered call ETF issuance, and the spike in interest in them on this platform and elsewhere, this market segment is evolving into a vital category for income investors.

A trendless market is a good time to own covered calls, since you essentially are getting paid to wait…for something, anything, to happen. If the market goes up, you likely make just a small additional sliver of return, since you exchanged most of the upside for that regular covered call option income received, in most cases monthly, from the ETFs.

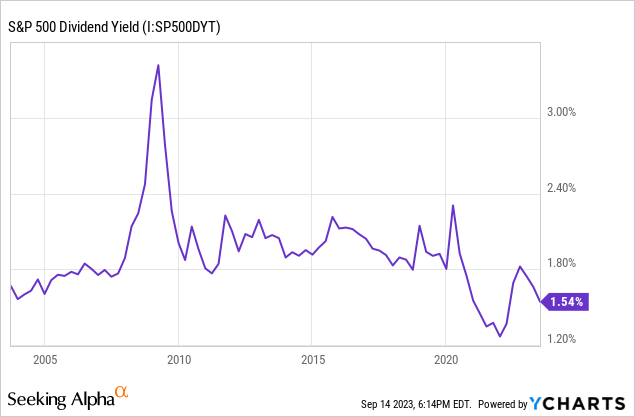

But there's another great reason to look closer at covered call ETFs. The stock market's dividend yield is near its lowest point in 30 years. A 1.5% yield on the S&P 500, shown in the above chart, and generally suppressed dividend yields across quality companies, reflects the dominance of growth stocks in that index after years of trouncing value stocks. But it also could be the result of companies favoring stock buybacks over distributing more dividends, for a long time now.

Take a close look at that graph above. 1.54% yield. That's the lowest S&P 500 yield at any point in the past 20 years, except for the aftermath of the pandemic, when a slew of companies, including some very large, prominent ones, temporarily suspended their dividends.

In other words, this is a tough time for traditional dividend investing for cash flow. About as tough as its been at any point in the past two decades.

Frankly, it doesn't matter how dividend yields on stocks got to this low point. They are there. So unless you are the type that prefers to hunt for high yielding stocks, and you have high confidence that the prices won't break down on an earnings miss or some other fundamental weak point (I don't!), having a core stock allocation in the form of a covered call ETF is a competitive approach, and one worth considering.

JEPI: still the one for many, but far from the only one for this approach

When it comes to covered call ETFs, the JPMorgan Equity Premium Income ETF (JEPI) has become the category asset leader by a large margin, sitting around $29 billion now. In the same way that today's markets are too focused on a small number of huge stocks, I think there are many ETFs in the covered call category that deserve a look. This is particularly the case when using them in the way I'm describing here. When you designate something as a “core” part of your portfolio, the more predictable it is, the easier it is to manage around it to reduce risk or enhance return.

So actively-managed covered call ETFs are certainly eligible in my book, but not the preferred choices. Bottom-line: I have not used JEPI for this approach, but that doesn't mean other investors can't.

XYLD: a strong fit for the core of this strategy

Investors can likely dream up many ways to use covered call ETFs. And with the proliferation of them in recent years, they will have the opportunity to try out even more approaches. But to me, the “active alpha” in the strategy I'm describing in this article comes more from what you do to manage around that covered call ETF position (with other ETFs) than from that covered call ETF itself.

Now, I do own multiple covered call ETFs at a time, essentially allocating my risk across multiple market segments (S&P 500, Nasdaq, Dow, small caps, bonds etc.) using a mix of covered call ETFs. But I tend to stick to index-tracking vehicles, because I don't want to invite the risk that I get the asset mix right, but an active manager drags my return.

That's why the Global X S&P 500® Covered Call ETF (NYSEARCA:XYLD) is on my short list for this approach, and why I own it now and rate it a Buy. The underlying assets in XYLD are extremely liquid, transparent, and predictable. The only thing I have to concern myself with is how much premium income it will throw off (which has more to do with market volatility than anything else) and whether I should be adding offense or defense around it at any point in time.

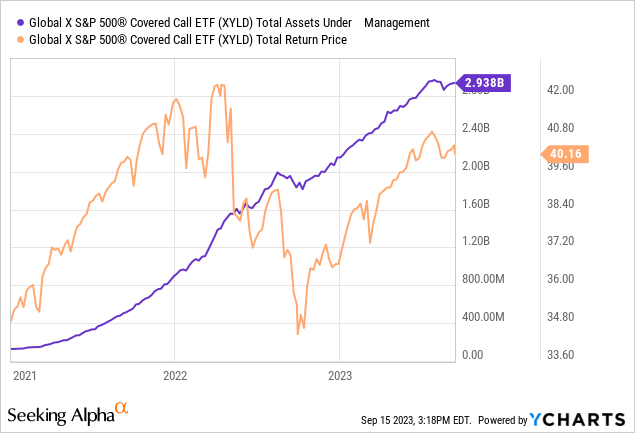

XYLD just passed its 10-year mark, but assets didn't really start to pile in until early 2021, as shown in the chart below. You can see how even though the total return of this ETF had its expected ups and downs with the stock market, assets have continued to come in at a steady rate (purple line). Assets are now just shy of $3 billion and it trades about $30 million a day in volume, so it is plenty liquid for many investors.

It is as transparent as they come in this industry, as the issuer, Global X, does a nice job of posting the exact options contract and amount being used as the covered call overlay on its S&P 500 index portfolio. I use it as the sample ETF position in my simplified model of my strategy below. We'll move on to that in a second, but right after I set the stage for why I think this strategy works for me, and why I am writing about it here in such detail, so that other investors can consider it for themselves.

There is just one problem with covered calls…and that's the point

Covered call ETFs are still equity exposure, at their core. Sure, the option premiums feel like an air conditioned home on a steaming hot day. But when winter hits, and the stock market gets chilly, that option income only offsets losses in the underlying stock portfolio to an extent. Investors find this out during many market dips of 10-15% or more.

That has led me to two related conclusions when it comes to using covered call ETFs as a key part of a portfolio:

1. They need some help in down markets

2. They need some help in up markets.

The first one is far more important to me. I prioritize risk-management. Always have, always will. So with the set of covered call ETFs I own as part of my income portfolio (alongside T-bills and short-term US Treasury ETFs), I am continuously thinking about how to cut the risk of a big loss.

Secondarily, but particularly in strong, broad-based stock market uptrends, I am looking for ways to augment that covered call ETF return, since I know it will only earn a fraction of what a fully-invested, unhedged equity ETF will.

Now, there is a very long list of ways to tackle either of the two missions above. But for the sake of simplicity here, I'm taking individual stocks and options off the table, and looking only at solutions involving ETFs. That's what I do 90% of the time myself.

The process in action: allocating around your covered call ETF core position

The strategy involves tactically allocating and rotating among three different types of ETFs.

1. One or more covered call ETFs

2. One or more “defense” ETFs

3. One or more “offense” ETFs.

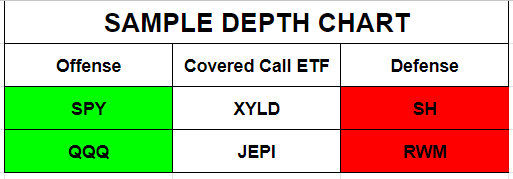

Here is a rudimentary sample of what I call a “Depth Chart.” It simply outlines the choices one has decided they will make in each category at any time. So, one or both of the two covered call ETFs would be held at all times. Depending on the mechanism used to determine if more “risk on” or “risk off” is preferred at any point in time, one or more of the offense positions or defense positions would be used.

There is not much reason to use both offense and defense positions simultaneously in a simplified portfolio setup like this one. Remember that the portfolio's anchor position, the covered call ETF, is a mix of offense and defense itself. The goal of the additional tactical positions is to add an offense or defense tilt at certain times. However, this is a very simple version of the framework.

For me, the covered call ETFs are generally held the longest, but I am constantly comparing the ones I follow to each other, in order to have what I feel is the best anchor to my portfolio at any time. Just think about the record gap between small caps and the Nasdaq 100 this year, and you probably know why I run it this way.

The other two, the offense and defense positions, are intended to be rotated based on whatever methodology one chooses to determine such decisions. I am a technician at heart, with 43 years of it in my background. So that and macro indicators I've developed, along with the experience of having been through, as they say, “a few rodeos,” all guides my ultimate buying and selling. But there's no reason one cannot automate this entire rotation process.

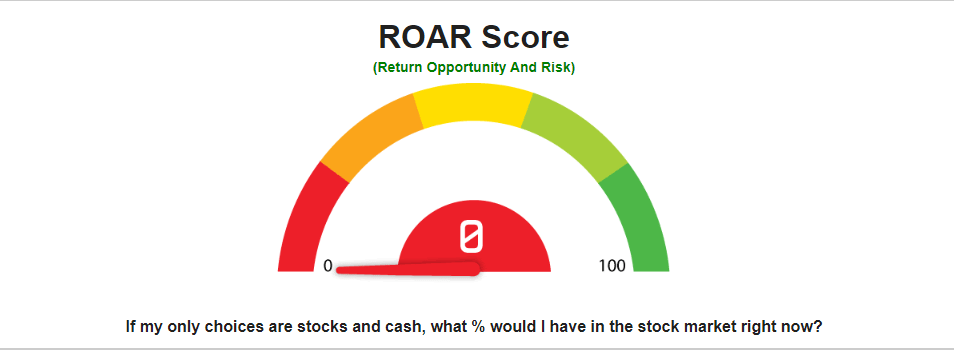

I first outline the market risk gauge I created and use for myself, which I call the ROAR Score, in this article earlier this year.

It is my bottom-line determinant of how much offense and defense I am willing to play in the portfolio at any point in time. I originally designed it to be used as an allocation between equity ETFs (the offense) and inverse equity ETFs (the defense). That was a long time ago.

So more recently, when cash yields returned to respectable levels, volatility and yield returned to the bond market, I started adding ETFs from those asset classes to my full depth chart, which now contains about 150 ETFs: sectors, themes, industries, ETFs that target segments of the yield curve, commodity-related ETFs (especially helpful lately with the run that oil and uranium have had – both have been strong contributors to my recent “offense).

Then, you came along

I never really thought about incorporating covered call ETFs into the ROAR Score and Depth Chart frameworks until last year. Primarily, because there were very few of them, and because I figured that I was already playing offense and defense, so covered call ETFs were more like an isolated position on the side, if anything.

Then, you came along. “You” the Seeking Alpha audience, with a great interest in my last article on covered call ETFs, and the extensive and thorough Q&A and debate that took place in the comments section. The lightbulb went on, and I even told a few of the commenters that the conversations in that virtual “room,” which continued to come at me for several days after it published, would prompt me to write in more detail about it. Promise kept! Keep the questions and debate coming.

Sample portfolio allocations in action

Since there is literally an infinite number of combinations of all three pieces of the strategy (covered call ETF, offense ETF, defense ETF), and I aim to keep this as simple as possible, I strongly encourage readers to focus on the concept here, not the particulars of this ETF or that ETF. The idea throughout this article has been to understand the mechanics, so you can decide how to apply it yourself as you see fit.

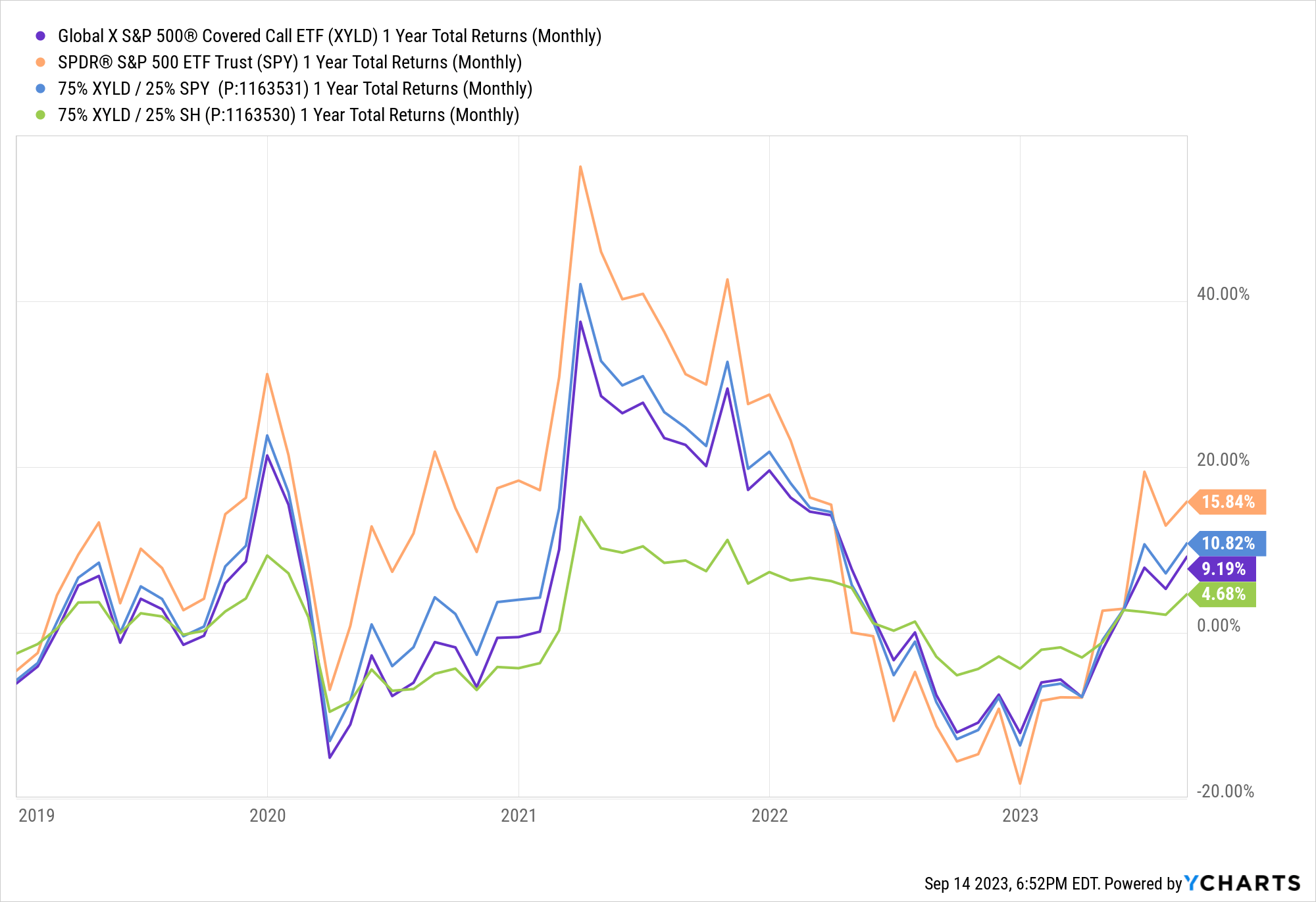

Below you see two charts. The first shows the SPY (as a benchmark), XYLD and a pair of hypothetical mini-mixes of ETFs. In one, I “tilt” the XYLD position to be more offensive, by taking 25% of it and allocating it to SPY. So, 75% of my S&P 500 investment is fully covered with call options (that's what XYLD does) and 25% is unhedged (SPY).

I did something similar, but in the other direction by taking 25% of the XYLD position and tilting it toward more defense by allocating it to ProShares Short S&P 500 ETF (SH).

Here is what a chart of “rolling” 1 year total returns looks like for SPY, XYLD and the two 75%/25% static mixes.

What should jump out at you right away is the green line during 2021 and 2022. In fact, its pretty flat throughout. None of these are intended to be precise allocations to be used, but to give you a flavor for what this strategy is capable of. And as the green line shows, if you simply swapped 1/4 of the covered call position for an inverse ETF, during the time you are positioned that way, the total portfolio is quite resistant to the market's downside. You'll also lag the whole way back up. That's where the rotation mechanism comes in. The goal is not to “market-time” this precisely, but rather to determine what level of risk in the core covered call ETF position is tolerable. And, what market conditions will prompt you to get somewhat more aggressive.

All the while, the majority of the covered call position (in this example, XYLD) is intact. That means you get 75% of the dividends and call premiums, plus any income that your other ETFs might spin out while you hold them. So in summary, this approach simply takes the idea of having 100% in a covered call ETF (or ETFs), then customizing your own method of managing around it. That involves taking some piece of the covered call ETF position (25% in my example, but it could be any percentage), and doing something different with it, with the aim of improving long-term results versus having 100% in the covered call ETF.

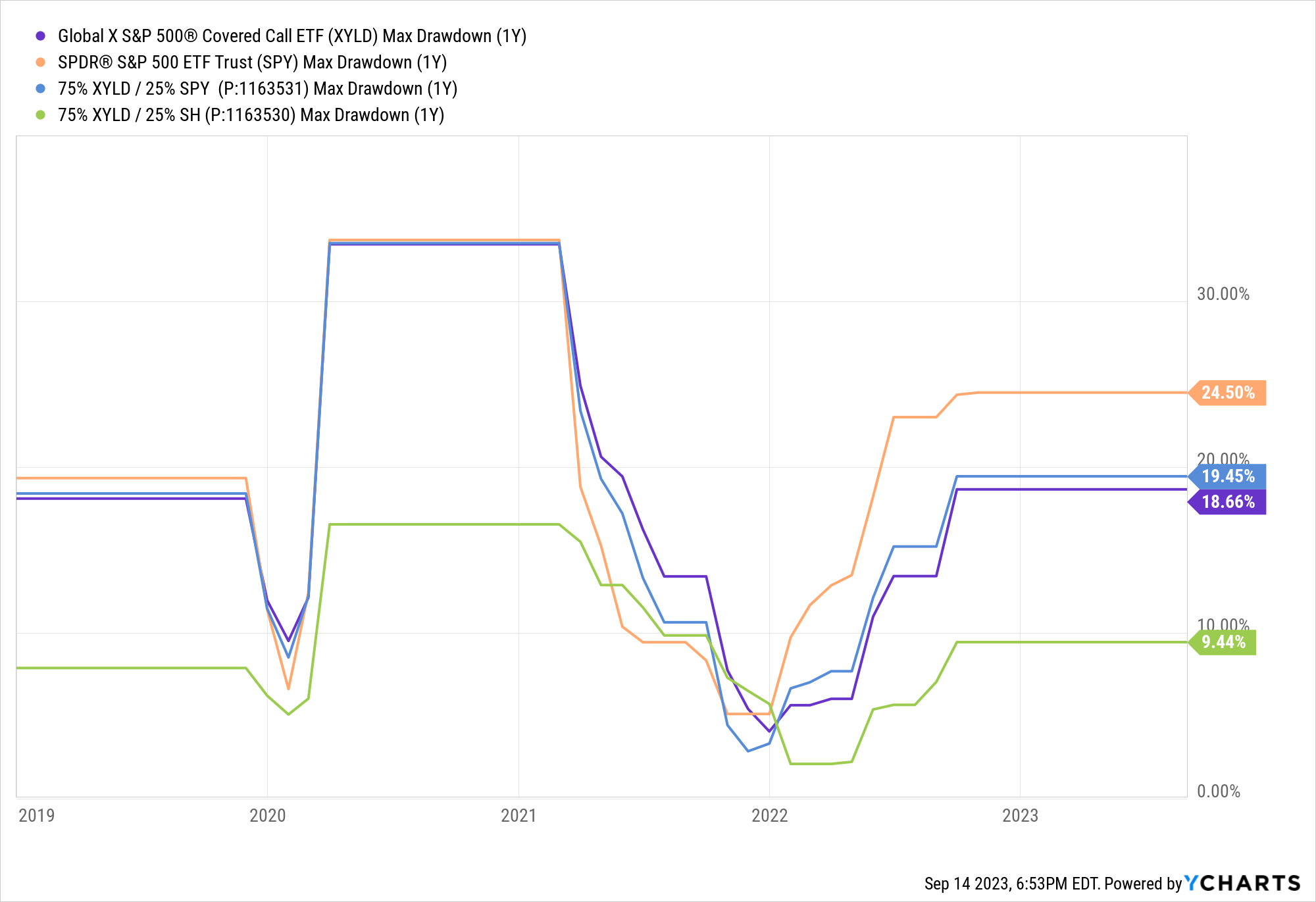

The last chart (below) shows how even that 1/4 defensive tilt can add value through reduced loss of capital. That green line, the one with the reduced risk since 25% was moved to an inverse ETF (SH), always has a lower “maximum drawdown” than the other allocations. This is pretty straightforward because I am using S&P 500-linked ETFs throughout this example. But imagine for just a moment that your inverse position was in, say, the small cap segment, and you used Nasdaq exposure whenever you added offense. Look back at how the latter has trounced the former and realize that the more you fill out that “depth chart” with alternative ETFs to plug in around the covered call ETF, the more “alpha” you add.

A quick note to JEPI owners

2023 is a good example of why I like this strategy, and use it for a big portion of my own retirement portfolio. in 2021, JEPI captured 75% of SPY's return (SPY was up about 28%, JEPI about 21%). But this year, as of this writing SPY is up 18% and JEPI is only up about 40% of that. That means there was probably an opportunity during part of 2023 to add some value, by infusing some offense during a stronger market trend. And as well as JEPI did in 2022, adding just a bit of defense during that year might have taken the outstanding -3.5% return of JEPI and turned it positive for the year.

Summary points

1. Covered call ETFs are getting very popular, very quickly, for good reason.

2. But they can potentially be even more valuable if viewed as a core or anchor position to build around, rather than as a full portfolio. XYLD is a solid choice to be part or all of that anchor position.

3. The construction of portfolios using the methodology I created, the market indicators and ETF research I've done to create an extensive roster of candidate for the “3 buckets” and the rotational method I use can be done as simply or as sophisticated as any investor wishes to. It takes some effort to get the hang of it, but I have found it provides a level of peace of mind that I didn't have before I started using it for my retirement portfolio.

Flexibility in the portfolio allocation process can be very valuable. It is a big part of what the process of seeking alpha in managing hard-earned wealth is all about!