HYEM offers investors a 6.5% yield and prospective dividend growth from higher rates. Total returns have been quite good for the past year, and dividend growth is mediocre. An overview of VanEck Emerging Markets High Yield Bond ETF follows.

I last wrote about the VanEck Emerging Markets High Yield Bond ETF (NYSEARCA:HYEM) in late 2022. In that article, I argued that HYEM's strong dividend yield and prospective dividend growth made the fund a buy. Since then, returns have been mediocre, as market interest rates have risen. On the other hand, the fund has slightly outperformed most of its peers, due to its strong, above-average dividends. Performance seems reasonable enough and should improve as interest rates continue to stabilize. Dividends should see positive growth too, as the fund replaces its current portfolio with newer, higher-yielding bonds. HYEM's above-average 6.4% yield and prospective dividend growth make the fund a buy.

HYEM – Basics

- Investment Manager: VanEck

- Underlying Index: ICE BofA Diversified High Yield US Emerging Markets Corporate Plus Index

- Expense Ratio: 0.40%

- Dividend Yield: 6.37%

HYEM – Overview and Analysis

Index and Portfolio

HYEM is an index ETF investing in dollar-denominated high-yield emerging market corporate bonds. Emerging market issuers are defined as those with significant exposure to emerging markets, so issuers headquartered in developed countries are (potentially) included. Applicable securities must also meet a basic set of inclusion criteria. It is a market-capitalization-weighted index, with country and issuer caps to ensure diversification.

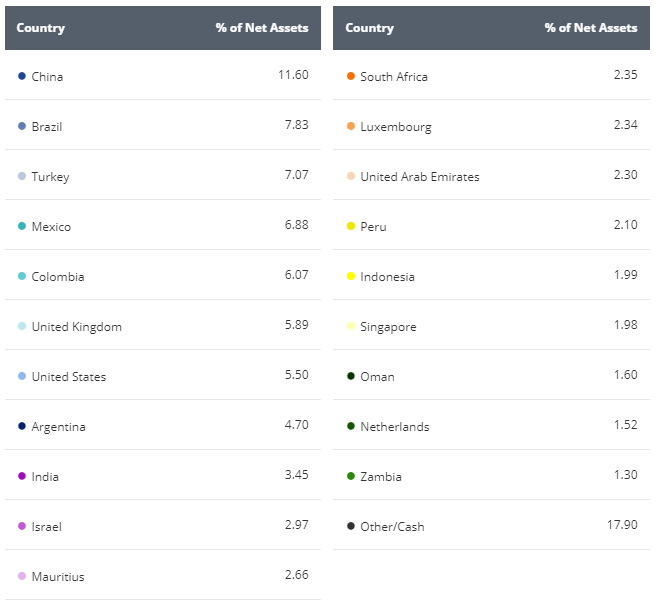

HYEM provides diversified exposure to its industry niche, with investments in over 500 different securities from dozens of countries and all relevant industry segments. Country weights are as follows:

Country weights seem reasonably well-diversified, and without significant overweight positions in China, common for some emerging market funds.

Industry exposures are as follows.

As can be seen above, HYEM is significantly overweight financials and materials, as these industries tend to be particularly large in many emerging market economies/public equity markets. Being overweight in these two industries does somewhat increase risk, but the fund seems diversified enough for a bond fund.

Credit Risk

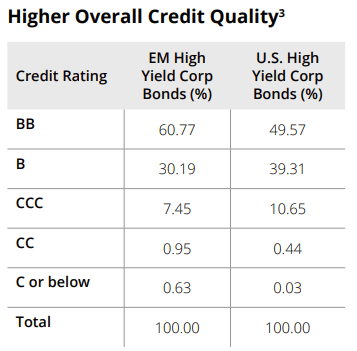

HYEM exclusively invests in non-investment grade corporate bonds, with an average credit rating of BB. Credit quality seems slightly higher than average for a high-yield corporate bond fund, quite a bit worse than the average broad-based bond fund.

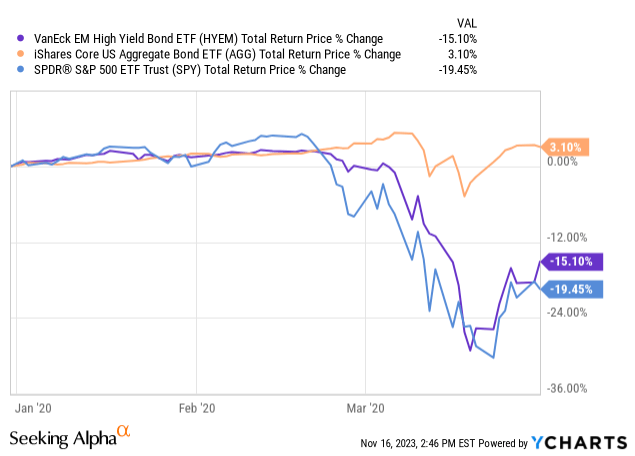

HYEM's credit ratings are indicative of issuers with somewhat weak financials and balance sheets. Securities rated BB and B, which encompass most of the fund, are almost always at no risk of short-term default, but risks increase during downturns and recessions. Focusing on emerging market bonds boosts risks and potential losses further. Expect above-average losses during downturns, as was the case in 1Q2020, the onset of the coronavirus pandemic. As the fund invests in bonds, it saw lower losses than the S&P 500 and most other equity indexes.

HYEM's low-quality, risky holdings are a significant negative for the fund and its shareholders, and its key drawbacks. Risks do not seem excessive to me, but more risk-averse investors might disagree.

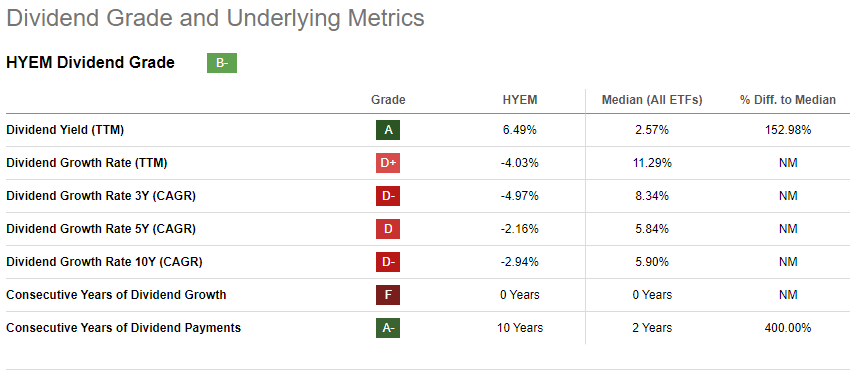

Dividend Analysis

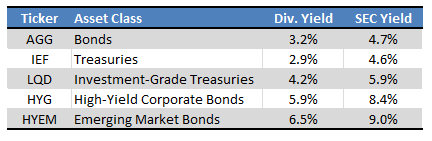

Risky bonds tend to sport comparatively high yields, and HYEM's dollar-denominated emerging market corporate bonds are no exception. As per JPMorgan (JPM), these securities currently yield around 9.0%, higher than most other fixed-income sub-asset classes, with the exception of senior loans.

HYEM itself yields 6.5%, quite a bit lower than the above. It generally takes a few years for higher interest rates to be reflected in a bond fund's dividend yield, as the fund must wait for its portfolio to mature to buy newer bonds at current market yields.

HYEM sports a 9.0% SEC yield, a more forward-looking, standardized yield metric. Said figure is in line with current market yields, and much more indicative of the dividends that investors should expect moving forward, in my opinion at least. HYEM's yield seems higher than average, on both traditional and SEC metrics.

HYEM's dividends should see strong, positive growth moving forward, as older, lower-yielding portfolio holdings mature and are replaced by newer, higher-yielding alternatives. Although this has been the case for almost all bond ETFs that I am aware of, it has not been the case for HYEM.

I am honestly not sure why dividends have not grown, as both market and fund conditions/fundamentals pointed toward significant growth in the past. A possible issue is that funds focusing on long-term bonds with very high maturities tend to see very slow dividend growth when rates rise. HYEM's maturities seem slightly higher than average, at 9.7 years on average, but even longer-term funds like the iShares 20+ Year Treasury Bond ETF (TLT) have seen positive dividend growth. HYEM holds many short-term bonds too, some of these should have matured by now, leading to higher yields and positive dividend growth.

Conditions continue to point towards future growth, and so I believe that growth is likely, although this has obviously not panned out in the past.

Performance Analysis

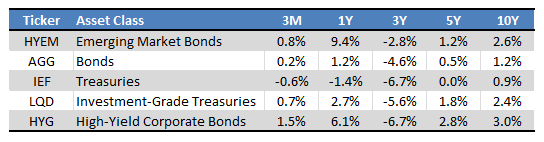

HYEM's performance track record is reasonably good, with the fund generally outperforming most bonds and bond sub-asset classes.

From the above, several things stand out.

HYEM's long-term returns are quite low, as interest rates were much lower in the past. Returns have significantly increased these past twelve months, as rates have (mostly) stabilized at a higher level. Returns will likely be strong moving forward, for the same reason. Much will depend on future interest rate policy, however.

HYEM has slightly underperformed relative to U.S. high-yield corporate bonds long term but has outperformed these past three years. From market data, emerging market bonds traded at slightly lower yields than comparable U.S. bonds for most of the past decade, but the opposite is true now, hence the differences in performance. HYEM continues to trade at a (small) spread to U.S. high-yield bonds, so I believe that it will continue to outperform moving forward.

Conclusion

HYEM's above-average 6.4% yield and prospective dividend growth make the fund a buy.