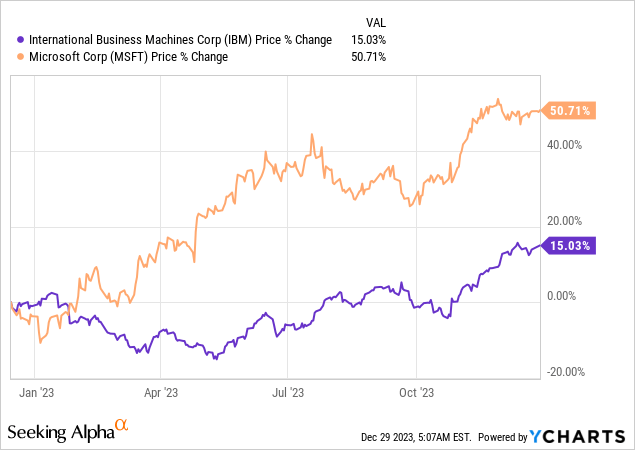

International Business Machines (NYSE:IBM) has gained around 15% since December 15, 2022, the date when my bullish thesis compared its incremental growth strategy with Microsoft (NASDAQ:MSFT) while also highlighting the strength of the consulting business. In the meantime, as charted below, the software giant's stock has delivered three times more gains thanks to the billions of dollars it invested in ChatGPT and its Azure OpenAI services used to generate content and build chatbots.

Data by YCharts

Now, after the ChatGPT eye opener in 2023, whereby people and organizations were initiated as to the opportunities made possible by Generative AI, it is the turn of IBM's stock to profit as enterprises start using the technology to make their corporate operations more productive in 2024.

For this purpose, I emphasize the synergies between Big Blue's consulting and software businesses as well as value the multiplier effect created by the Red Hat OpenShift and Watsonx platforms.

Synergistic Growth with Software and Consulting

First, despite the immense popularity of ChatGPT which is driven by Generative AI, it is estimated that only 5% of enterprises had deployed this flavor of artificial intelligence by October, implying that most of the opportunities are still for grabs. Second, looking beyond the attractiveness of new technology, it is also about balancing risks (or the amount of money and time spent on deployment) and the value obtained or gains in productivity. These risks are more easily taken by individuals or small companies who can afford to make mistakes but this is far from being the case with large enterprises where the business impact of making a wrong decision can result in millions of dollars of losses. This is the reason why after spending record amounts to acquire Nvidia's (NASDAQ:NVDA) GPUs to build their intelligent infrastructures, big corporations should opt for external consultants, like those from IBM, to double-check the impact of the technological change associated with AI and get it right on business transformation.

For this purpose, Big Blue has reoriented its platform-centric corporate strategy around hybrid cloud (with Red Hat Open Shift ) and AI (with Watsonx enterprise-ready generative AI), and separated from Kyndryl earlier. In this way, about 75% of IBM's growth vectors are now led by software and consulting which are also responsible for more recurring sales and are made up mostly (more than 50%) of Big Blue's technology. Noteworthily, IBM consulting also includes strategic partnerships with hyperscalers (or large public cloud providers) and other big SaaS players.

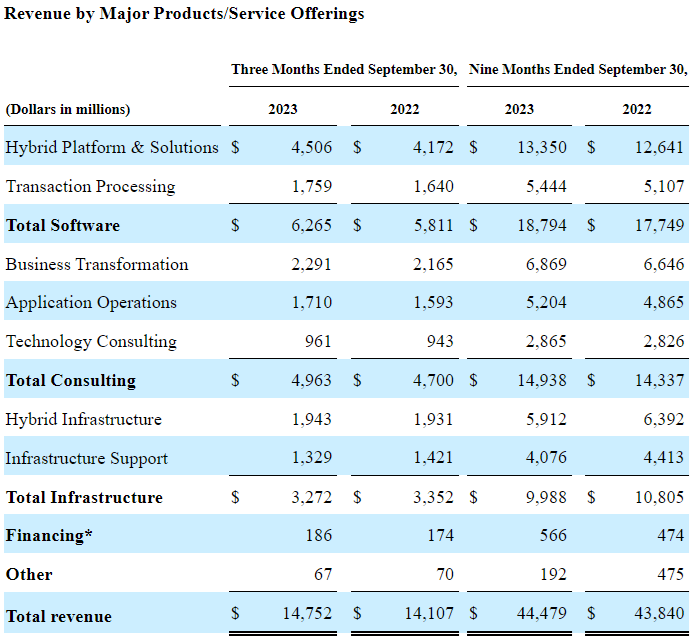

This strategy to partner instead of competing head-on with them has resulted in more sales, which make up about 40% of consulting revenues, or $5,975.2 billion (14,938 x 0.4 as per the table below) for the first nine months of 2023. This is explained by IBM consultants not only winning contracts for Watsonx to help corporations better leverage their data but also signing customers for Azure Open AI and Amazon Bracket platform.

SEC Filing (seekingalpha.com)

Thus, partnerships-related consulting revenue continues to grow rapidly as signings essentially doubled at the end of the third quarter of 2023 (Q3) on a year-to-year basis. Despite these positives, analysts are more enthusiastic about Microsoft's AI growth story and predict that it will add $25 billion to its topline by 2025. However, with the global AI software market expected to reach $850.6 billion by 2030, after growing by 35.97% CAGR from 2024 onwards, both companies should obtain a piece of the pie.

Valuing IBM using the Multiplier but exercising Moderation given the Risks

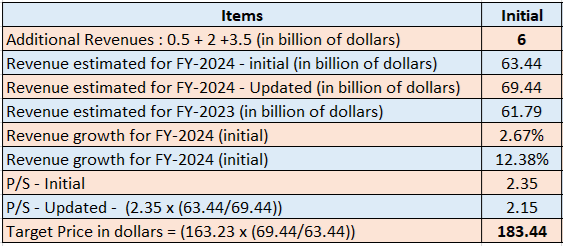

Looking at potential revenues from the Generative AI platform (Watsonx), according to Arvind Krishna, IBM's CEO during Q3's earnings call on October 25, the number of related bookings was equivalent to “low hundreds of millions of dollars. Later, according to the update provided by the CFO during the UBS Global Technology Conference on November 28, and, based on the adoption of the Red Hat OpenShift platform acquired in 2019, Watsonx-related sales were expected to reach $1 billion for the first 12 months.

Being conservative, I assume only half that amount, or $0.5 billion to add to FY-2024’s topline which ends in December next year. Additionally, considering synergistic growth as IBM’s platforms act as multipliers for IBM’s software and services businesses, for every dollar “landed” or spent by customers on the platform itself, $3-$5 and $6-$8 are obtained as software and services revenues respectively. Thus, assuming that the $0.5 billion for the Watsonx platform generates $2 billion and $3.5 billion in software and services sales respectively considering the midpoints, the total comes to $6 billion.

This, when added to the $63.44 billion expected for FY-2024 gives $69.44 billion as tabled below. This, in turn, translates to revenue growth of 12.38% instead of the 2.67% initially expected, and a lower P/S of 2.15x. Finally, I obtained a target of $183.44 based on the current share price of $163.23.

Table built using data from (seekingalpha.com)

Now, this is a high target but is for the long term, and in the meantime, the stock may be volatile namely due to interest rates.

As such, part of IBM's upside was triggered by the Federal Reserve confirming its more dovish stance on monetary policy at the beginning of November after keeping rates unchanged leading more people to expect cuts in 2024. Since then, IBM's stock has delivered a one-month performance of nearly 5% while Microsoft has faded by 2%. The explanation is Big Blue paying a forward dividend yield of over 4% which means that it competes with risk-free government bonds. Now, since lower rates are synonymous with lower treasury yields, IBM's higher dividends have become relatively more appealing, but, to be realistic, the U.S. Central Bank's actions will ultimately be guided by inflation figures, and, in case rates stay higher for longer, do expect stock volatility.

Still, looking at the price action, most of the stock's gains, or 10% were achieved in May after it unveiled Watsonx as per the introductory chart which means that the upside should continue as IBM delivers on its version of Generative AI driven by its army of over 20K data and AI consultants. In this respect, Watsonx includes customized foundational models, good at both language and computer coding. These two features when offered in tandem can potentially save companies 20% to 45% of what they spend annually on software engineering.

Still, its competitors have also innovated in the productivity aspect of AI.

Well-Positioned Vs Consultancies and Hyperscalers

IBM faces competition, both from conventional consulting companies like Accenture (ACN) or Infosys (INFY) as well as from the hyperscalers themselves like Alphabet (NASDAQ:GOOG). In this respect, Big Blue's advantage relative to consultancies is that both Red Hat OpenShift and Watsonx platforms are embedded in its software portfolio. This means that deals can be made faster as platform-based applications have already been integrated since Day One, thereby allowing clients to deliver faster on projects and save on costs.

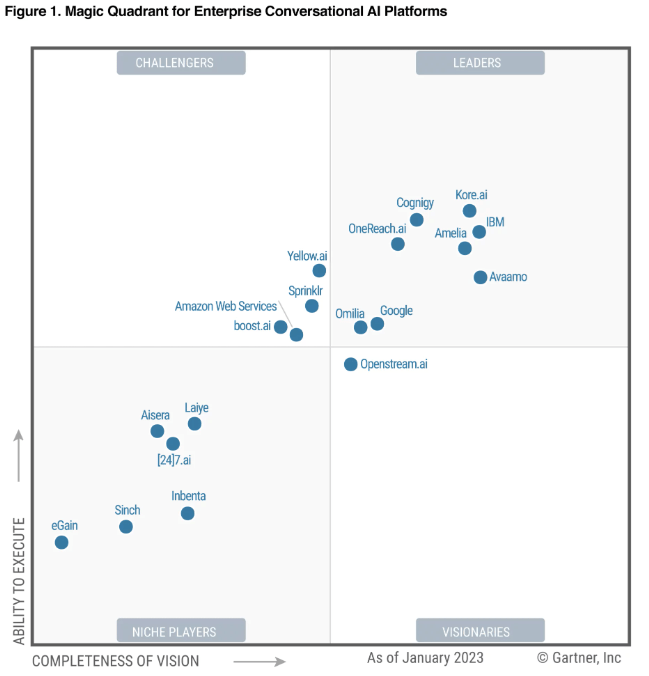

Next, coming to competition with hyperscalers, one key supporting factor for IBM is its recognition as a leader in the 2023 Gartner Magic Quadrant for Enterprise Conversational AI Platforms which should help Watsonx Assistant better compete with Google Workspace AI with tools integrated into the search giant's apps ecosystem or Amazon SageMaker Canvas for the development of AI-powered productivity tools.

Gartner's Magic Quadrant (www.ibm.com)

Furthermore, while Microsoft 365 Copilot is better known and came rapidly in the footsteps of ChatGPT, it must be mentioned that IBM’s Watsonx also incorporates NLP (natural language processing) for developing productivity tools to cater to complex tasks. In this connection, the company has been quietly forging partnerships with SAP SE (SAP), and Adobe (ADBE), just to name a few with more names to be announced in January during the fourth quarter earnings call.

Therefore, Big Blue faces competition but, remains well-positioned to sign in more customers as it also aggressively improves existing product strength through acquisitions, the latest one being the StreamSets and WebMethods platforms acquired from Software AG for 2.13 billion euros. The intention is to bolster both its AI and hybrid cloud offerings, as part of its synergistic growth strategy.

With Superior Profitability and Watsonx Governance, IBM is a Buy

Therefore, the company continues to invest both organically and inorganically, while at the same time building strategic partnerships to broaden its portfolio to include products made by competitors.

This strategy which should drive an additional $6 billion of AI-related sales in 2024 is less than one-quarter of what analysts expect for Microsoft and has been moderated to account for the competition, and revenue decline in IBM's infrastructure business (as per the revenue per major product table above), and the possibility of the Fed adopting a higher-for-longer posture.

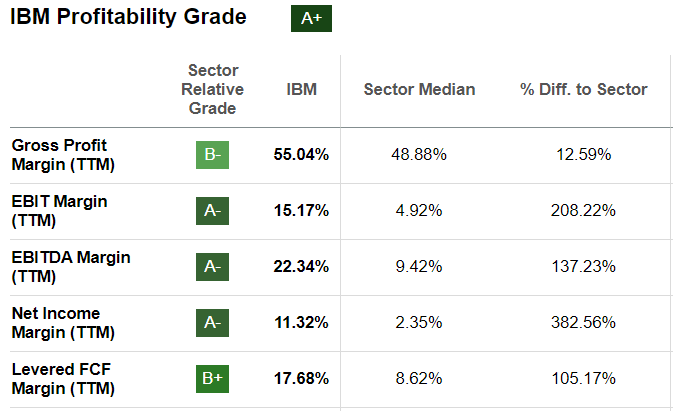

Therefore, the price target of $183 is a fair one and is further justified by the $6 billion is only a tiny fraction of the combined $2.6 trillion that organizations are expected to spend on software and IT services (including consulting) next year, according to Gartner. For this matter, despite bearing the impact of higher inflation and a slowing economy, worldwide IT spending should increase in 2024 (relative to 2023) driven partly by the need to evolve spending towards automation and efficiency-enabling technologies including artificial intelligence which require fewer employees. This in turn ushers better profitability, which, by the way, is already benefiting IBM as evidenced by the tens of thousands of man-hours saved through leveraging AI tools to improve efficiency. This increases the probability of maintaining its A+ profitability which is better than the median for the IT sector as illustrated below.

seekingalpha.com

Finally, widespread enterprise adoption of AI in 2024 should also give rise to legal issues especially when utilizing third-party content such as those produced by media outlets like News Corp (NASDAQ:NWS) to train OpenAI's language models. In this case, the launch of Watsonx Governance seems timely for ensuring transparency and compliance throughout the AI lifecycle.

Editor's Note: This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition, which runs through December 31. With cash prizes, this competition — open to all contributors — is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!