The year 2023 presented a huge shock to the banking industry, as it confronted three of the four largest bank failures in American history.

The collapses of Silicon Valley Bank, Signature Bank and First Republic Bank were due to a loss of value in their asset portfolios as the Fed raised interest rates by tightening monetary policy, which led to the flight of large uninsured deposits seeking safety and better returns elsewhere. The concern was that this would cause a contagion in other segments of the banking industry.

To date, this hasn’t happened.

As the asset quality and liquidity crises at these banks emerged, the Fed stepped in to make available support for the problem institutions. They encouraged use of their Discount Window to provide short term loans to meet some of the banks’ liquidity needs, and they created a new lending facility, the Bank Term Funding Program (BTFP), to extend credit for a longer period of time, with more lenient collateral requirements.

The Fed also supplied credit to the FDIC as they stepped in to take over the failed institutions.

As a move to prevent the further flight of deposits, the Fed and the FDIC took an extraordinary step and announced that all depositors at the failed institutions would be made whole, including uninsured depositors.

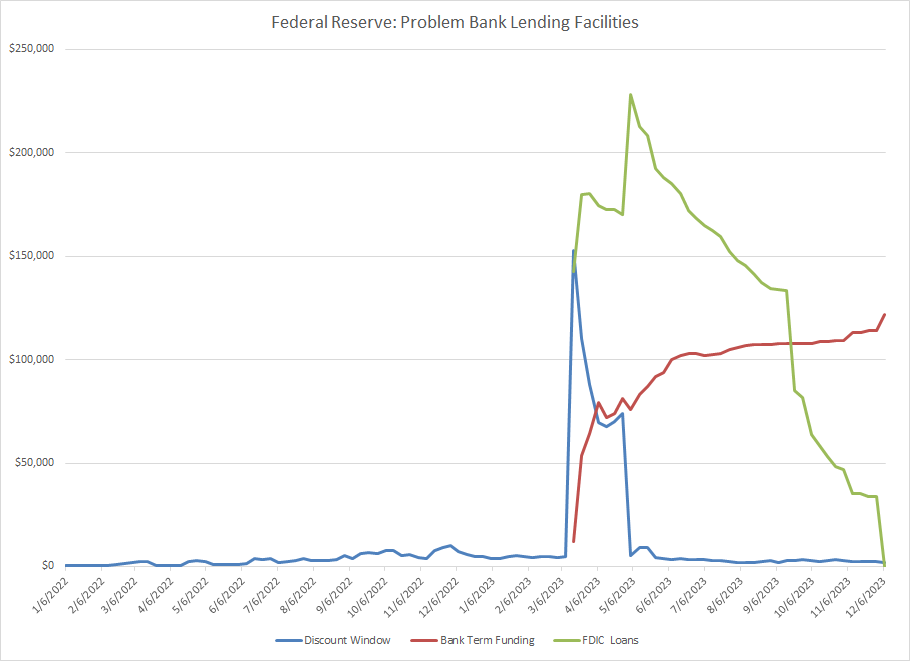

Problem Bank Loans At the Fed

The Fed fulfilled their role as the lender of last resort, as the troubled banks took advantage of the Fed’s lending facilities.

Discount Window borrowings spiked from $4 billion to $152 billion in the first week, and credit extensions to the FDIC rose from zero to $228 billion.

Federal Reserve

The Discount Window loans are the most expensive, and as the banking crisis progressed, borrowers switched from the Discount Window to the less costly BTFP. Discount Window borrowings within the first two months dropped back down to $4 billion, as the BTFP loans continuously climbed to $122 billion.

Over time, the FDIC loans also declined, and just this past week, almost nine months to the day of the first bank collapse, the FDIC loans dropped to zero.

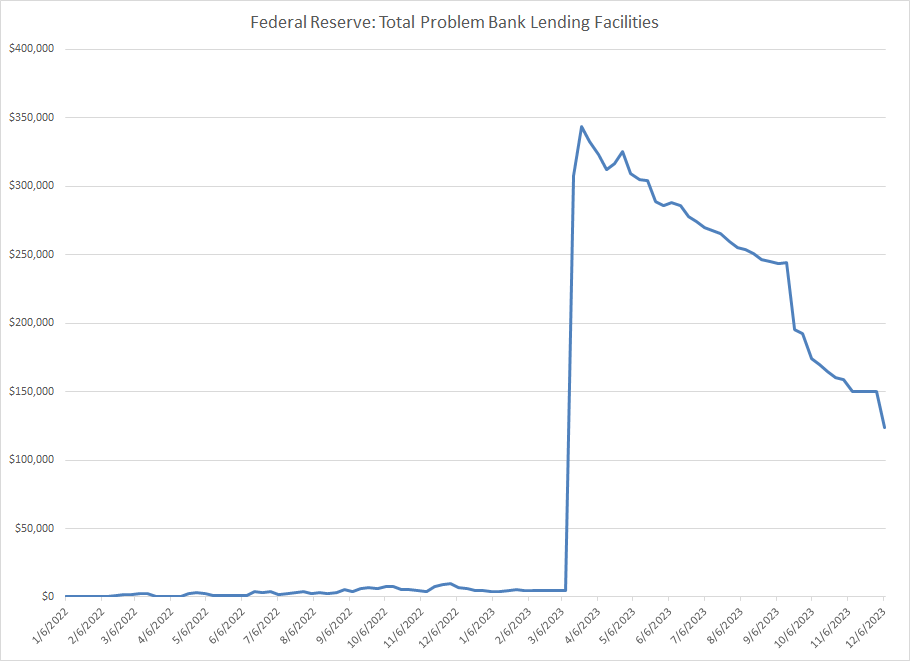

Cumulatively, the three Fed Problem Bank Lending Facilities peaked at $342 billion, but have gradually declined to $124 billion.

Federal Reserve

At first glance, the 64% drop in problem bank loans suggests that the situation has improved significantly in the banking industry.

This view is further supported by the performance of bank stocks. Both the KBW Bank Index (BKX) and the KBW Regional Bank Index (KRX) fell -37% from their highs during the banking crisis. However, the recent decline in problem loans, and the anticipation of a Fed pivot to cutting rates, have led to a 23% bounce back in the KBW Bank Index and a 32% gain in the KBW Regional Bank Index, from the lows.

Bloomberg

Even the Fed supports this view.

In fact, in each of the past six statements released by the Fed following an FOMC meeting, the second paragraph begins “The U.S. banking system is sound and resilient.” The pronouncement first appeared on March 22, 2023, a mere ten days after the failures of Silicon Valley Bank and Signature Bank. We expect it will be repeated for the seventh time this week, when the Fed releases their statement on Wednesday at the conclusion of the December 11/12 FOMC meeting.

A skeptic might, with poetic license, take the Shakespearean view “the Fed doth protest too much.”

Looming Trouble In The Banking Industry

When looking beneath the surface, a different picture of the banking industry emerges.

Although Problem Bank Loans at the Fed have been declining, this has not been the only source of emergency funding for banks. During the banking crisis, and beyond, commercial banks have been accessing loans from the Federal Home Loan Bank (FHLB.)

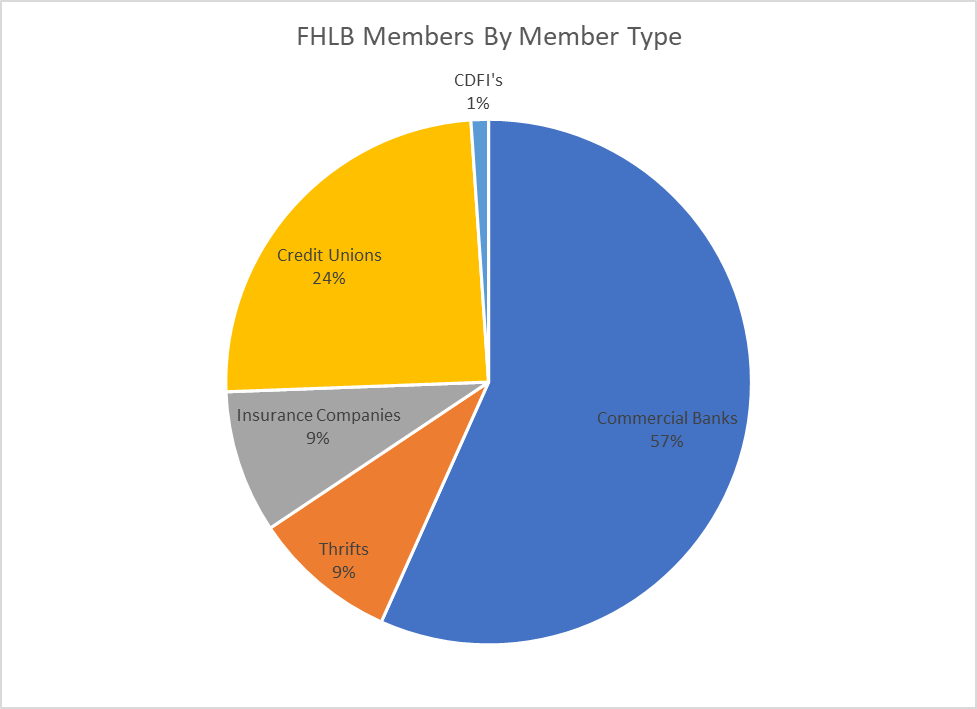

The FHLB was chartered in 1932 to provide liquidity to S&Ls, or Thrifts, to facilitate their ability to make mortgages, which would bolster the housing industry. As the Thrift industry dissipated in 1970’s-1980’s with the advent of the S&L Crisis (for a full discussion see my Seeking Alpha article “The Largest S&L In The World – Lessons Not Learned), the FHLB expanded their mandate to include commercial banks and credit unions.

Whereas in the 1980s 100% of FHLB members were Thrifts, by 2Q23 that figure had dropped to 9%, as the largest group of Member Banks in the FHLB system became the Commercial Banks, which comprised 57% of the total.

Federal Housing Finance Agency

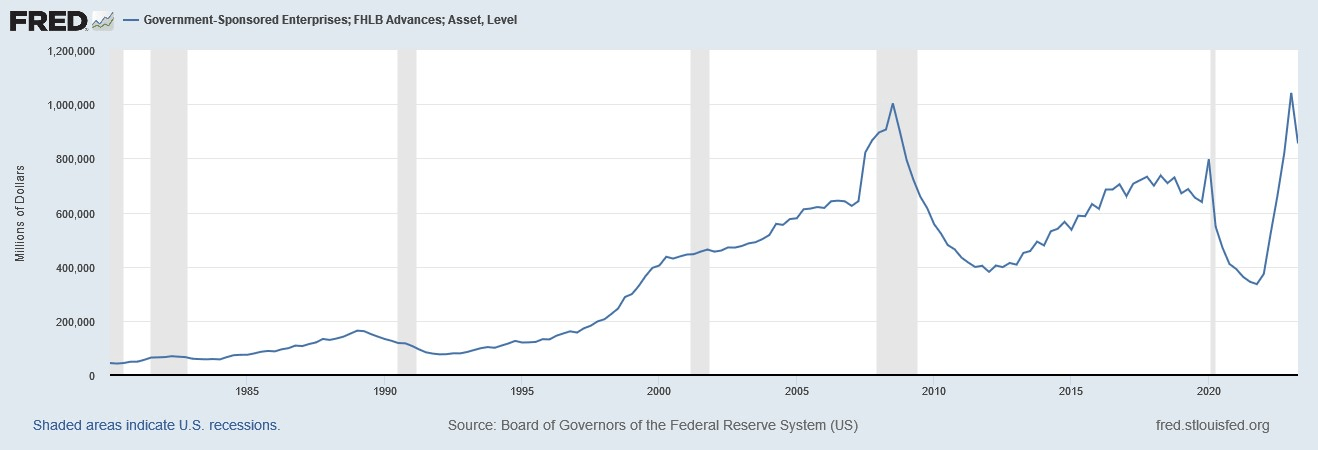

The FHLB’s primary business is to make fully secured, low-cost loans, known as advances, to their member banks. These advances are mainly used to fund low- cost mortgages. However, during this year’s banking crisis, member commercial banks tapped the FHLB for a different purpose; they used FHLB advances as a liquidity source, to offset the deposit outflows due to rising short term rates.

FHLB advances rose to an all-time high of $1.1 trillion during the banking crisis, from a 20-year low of $335 billion only 12 months earlier.

FRED

During the week of March 13, 2023, when the FDIC took over Silicon Valley Bank and Signature Bank, the FHLB funded $676 billion in advances. This represented the largest one-week volume of advances in FHLB history.

In effect, many banks were tapping the FHLB instead of the Fed, for emergency loans. First, FHLB advances were cheaper than going to the discount window at the Fed. Second, operationally it was easier for many banks to borrow from the FHLB, because they did not have all of the mechanical and administrative procedures in place to access Discount Window borrowings.

As of 3Q23, FHLB advances, although off the crisis high, remain elevated.

In their year end review, released on November 7, 2023, the Federal Housing Finance Agency (FHFA,) which regulates the FHLB, acknowledged they have to come up with better procedures to differentiate the FHLB from the Fed. It is not the FHLB’s role to be the lender of last resort.

Banking Crisis Revisited

One of the primary reasons for the failure of Silicon Valley Bank was a big loss in their holdings of US Treasury bonds. Many people became aware of the distinction between Available-For-Sale versus Held-To-Maturity accounting designations on commercial bank balance sheets.

The unrealized loss position of commercial banks has actually deteriorated since the banking crisis. As of 3Q23, U.S. banks were sitting on -$684 billion in unrealized losses, up from -$516 billion at 1Q23.

FDIC

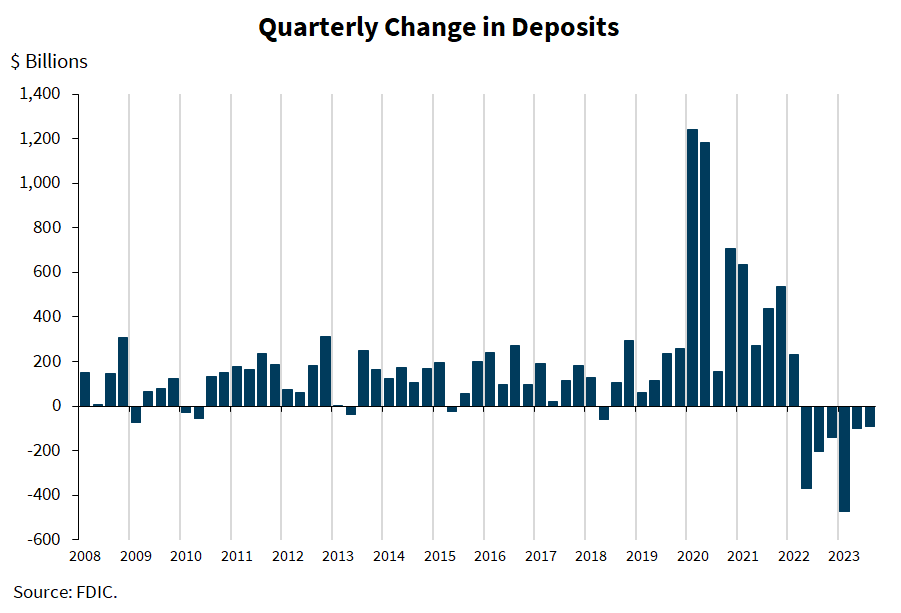

The other major reason for the failure of the banks was because large depositors chose to move their cash out of the banks. This trend has only continued. As of September 30, 2023, commercial banks had experienced a deposit outflow for the sixth consecutive quarter. While the trend has improved, as only $90 billion flowed out of banks in 3Q23 versus a decline of $473 billion in 1Q23, banks are still hemorrhaging deposits.

FDIC

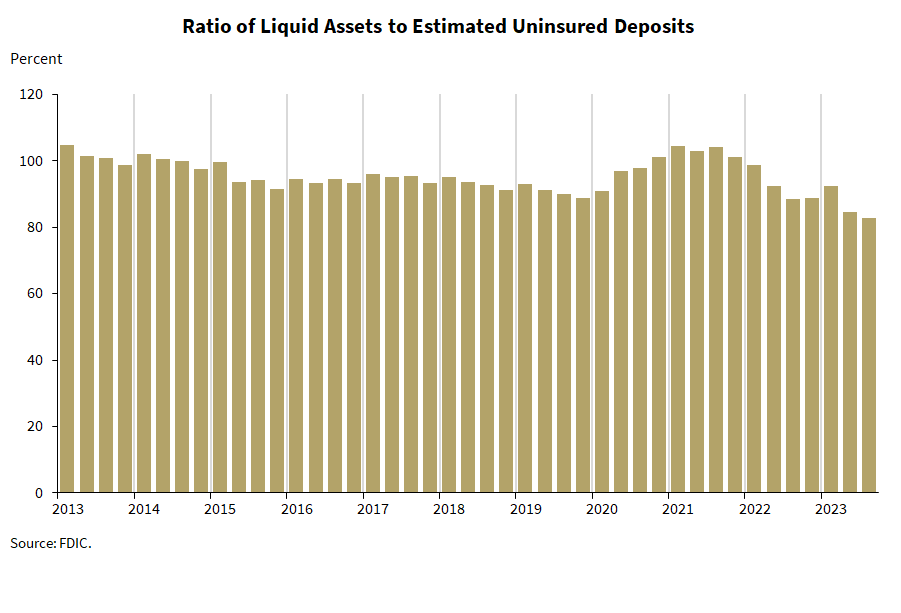

Not only are deposit levels declining, but the banking industry is experiencing further deterioration in another measure of their liquidity. The ratio of liquid assets to uninsured deposits has fallen to the lowest level in more than ten years. Liquid assets are defined as cash, Fed Funds sold, and repurchase agreements. A high ratio provides coverage if uninsured deposits flee. But the ratio has dropped to 82.8% coverage from 92.4% in 1Q23, and a recent high of 102.4% in 3Q21. The low ratio weakens the banking industry’s liquidity position.

FDIC

Problems With Asset Quality

In addition to the banking industry suffering from unrealized losses in their Treasury Bond portfolios, they are also suffering from deterioration in their loan portfolios.

The largest component of assets in the banking industry, aside from Government bonds (17.6%) and Cash (15.1%), is Commercial Real Estate (CRE,) at 12.8%.

CRE is the biggest segment of the banking industry’s loan portfolio. The smaller, more regional banks, have a larger CRE exposure than the large banks. Large banks, defined as the top 25 banks by assets, have 7% of their portfolios in CRE, while the smaller banks, defined as the non-top 25 banks, have 22% of their portfolios in CRE market.

Bloomberg and Federal Reserve

It is well known that the post-pandemic work environment has changed the dynamics of the CRE market. Work-From-Home has become more prevalent, hence the need for office space has declined. This is reflected in a sharp increase in vacancy rates. Nationally, the office vacancy rate was 17.8% in October, an increase from 16.3 % one year ago.

CBRE

The increase in vacancy rates has put downward pressure on rents. Lower rents, combined with rising vacancy rates and higher costs of borrowing due to the Fed tightening, has been reflected in the deterioration of loan quality. This can be seen in rising delinquency rates in the CRE space.

Past-Due and Noncurrent Loans are they highest they have been since 2013 and are rising. For many, this is a major concern. Additionally, as loans come due in the current higher rate environment, larger debt service costs will exacerbate the current asset quality problem

FDIC

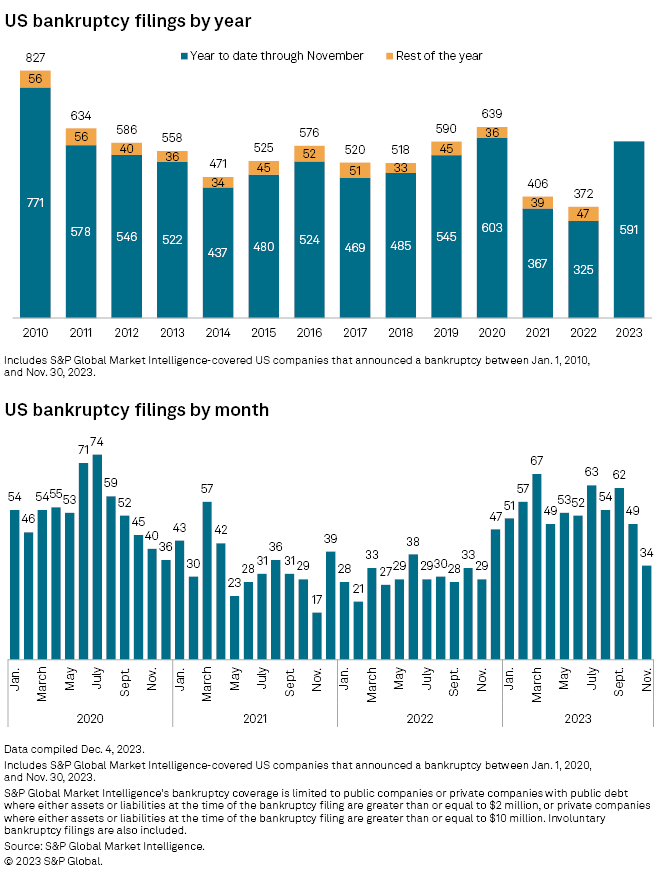

Despite the rosy outlook as evidenced by recent performance in the stock market, there are financial problems lurking around the corner. Corporate bankruptcies through the first eleven months of the year, are at their second highest level since 2010.

S&P Global

The most recent and most prominent filing came when WeWork (OTC:WEWKQ) declared bankruptcy on November 6, 2023. The once high-flying office-sharing company epitomizes the collapse of the office market. Valued at $47 billion as recently as 2019, the stock has plummeted by 98% this year.

In its wake will be further increases in office vacancy rates and additional pressure on rents. These factors, combined with higher mortgage rates, will lead to pressure on the underlying value of the commercial real estate.

Bank Regulatory Problems

One of the findings, in the aftermath of the recent banking crisis, was that more regulatory supervision was needed to prevent another round of bank failures.

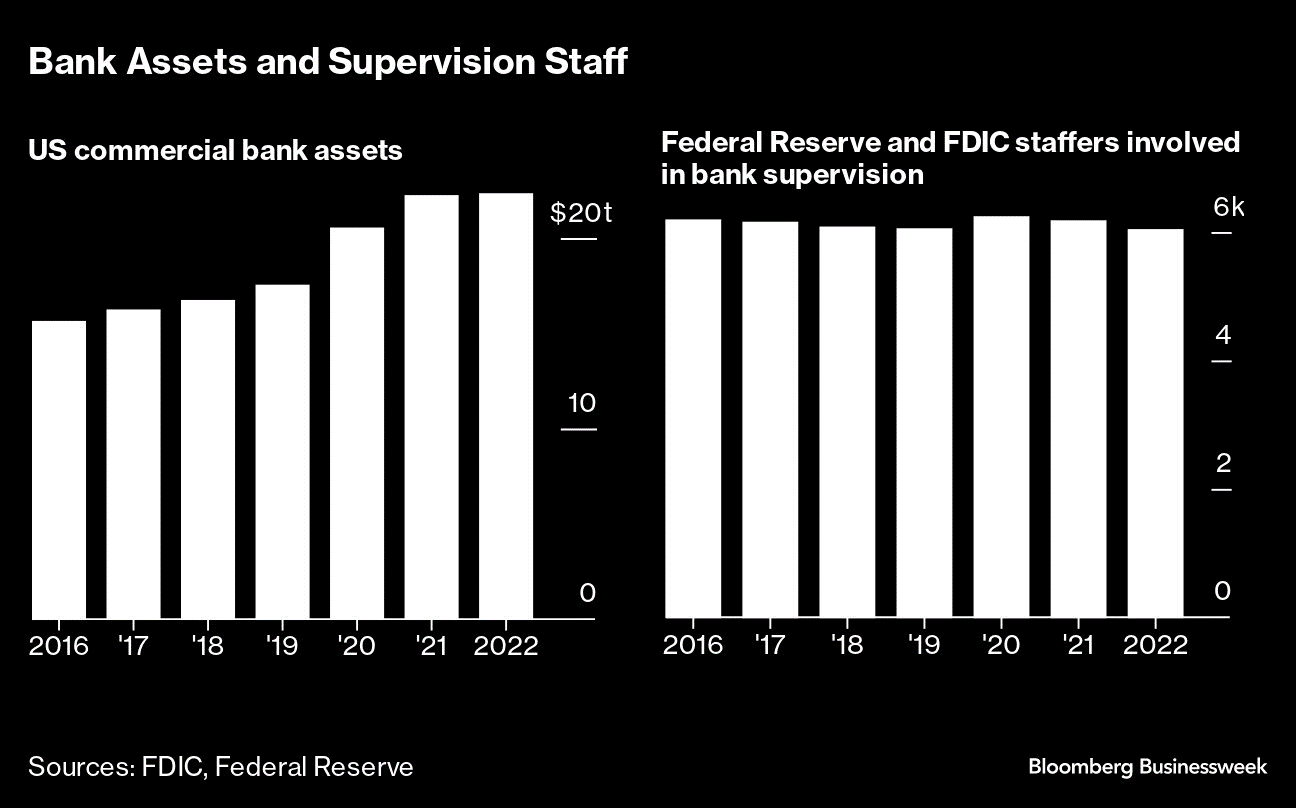

While sound in theory, the Fed and the FDIC have had difficulty implementing their plan in practice, because they have been struggling to hire new bank examiners and to keep experienced personnel. The problems include inadequate compensation and a demanding work environment.

The problem was exacerbated by recent reports of a toxic work environment at the FDIC. There have been allegations of sexual harassment and misogynist behavior among the staff. Turnover remains high.

Since 2016, commercial bank assets have surged by 40% to $22 trillion, yet during that time bank supervision staff at the Fed and FDIC has declined by 3%.

Bloomberg, FDIC and Federal Reserve

The FDIC has set up a special committee to address the root cause of the workplace problems, but it will take some time to implement corrective measures.

An additional regulatory hurdle the banking industry is facing are the proposed Basel III reforms, which came about as a means to mitigate risk following the Great Financial Crisis of 2008. The lessons learned were that banks were undercapitalized and overleveraged.

For the past fourteen years, bank regulators, on a global basis, have been working on a plan to improve capital ratios and liquidity ratios to maintain a financially stable banking industry, that can survive losses during an economic downturn.

The proposed regulations will apply to banks larger than $100 billion in total assets. The main requirement is to increase capital by 16%-20%.

Just this past week the CEOs of eight of the nations largest banks appeared before the Senate Banking committee to push back on the proposed regulatory changes. They felt that the increased capital requirements were not necessary, and would negatively impact consumers who would ultimately have to pay higher rates for things like credit cards, mortgages and other loan products.

While Basel III would only affect the 34 largest banks and is to be phased in over three years starting in 2025, it is taking up space among bank industry leaders.

Conclusion

The banking industry is still confronted with some of the challenges that led to the banking crisis earlier this year. Higher interest rates have negatively impacted the asset value of the bank’s securities portfolios and loan portfolios. Asset quality continues to deteriorate, and deposit levels continue to fall.

While regulators want to keep a firm eye on the banks operations, they have their own struggles to maintain adequate employment levels.

Though the U.S. economy has remained strong in 2023, the banking industry still faces significant downside risks from high interest rates and inflation. These issues will cause credit quality, liquidity and earnings problems for the industry.