Synopsis

Why are media outlets globally about to post a new attention-catching headline? Because the pole position as world's largest EV manufacturer is about to shift from Tesla (TSLA) to BYD (OTCPK:BYDDY). EV sales figures for the fourth quarter from China are about to be released, a quarter that will inaugurate a new global EV leader, adjudged by pure EV sales in the final quarter of 2023. This is bound to shift investors' eyes to BYD – hence the recommendation proffered in this article. Read on for a major opportunity to buy BYD before most investors do.

The article will cover:

- the financial history and current metrics of BYD. Note: These metrics represent BYDDY in US$, the ADR of Hong Kong-listed BYD Company, and conform to ADR security rules, included the stated GAAP figures.

- Recent EV sales trends for BYD and Tesla in China, and the basis of my conviction that BYD is about to displace Tesla as the new global EV leader.

- The merits of having an EV variant, the PHEV or Plug-in Hybrid Electric Vehicle that is gaining traction in many geographies (primarily due to range anxiety and inadequate charging networks), a variant conspicuously absent from Tesla's portfolio.

- The success of BYD's newly launched models, both in China and the recent headway made in Europe.

- a detailed comparison of BYD's financial history and valuation metrics with Tesla, showing how absurd the valuation discrepancy has become, especially with regard to future revenue and profit trajectories.

A Summary of BYD's incredible success

Rather than repeat BYD's history I refer the reader to two excellent recent articles by SA authors, ‘BYD: The King Of Electric Vehicles' and Invest In BYD For Its Vertically-Integrated International Offerings; also there's mine, Buy BYD: Largely Ignored Vs. Tesla's Meteoric Ascent that delves into the company's history from a financial perspective.

(NB. It's only proper that I mention my recommendation in article above was horribly wrong, with BYD falling 19% since publication (January '21), while the market returned 23%. Yet therein lies the opportunity.)

The graph below captures BYD's operating and valuation history since 2020. It shows a company whose market capitalisation has stayed roughly constant over the last 3 years, even though revenue and EBITDA have moved gradually higher, via an impressive improvement in operating margins. It's very evident that the static market valuation is the result of a collapse in the valuation rating (EV/EBITDA ratio) accorded by investors. A key point of this article is that this valuation contraction is unjustified, both from the actual operating history and, more importantly, the prospects.

ycharts.com

Sales up to 3Q 2023

BYD registered remarkable growth in 2023; in the September quarter BYD sold 431,603 BEVs (Battery Electric Vehicles), but it also sold 390,491 PHEVs (or Plug-in Hybrid Vehicles) leading to a sum of 822,094 passenger NEVs (New Energy Vehicles) in the third quarter of 2023, a YOY growth of 43.3% in deliveries, whereas YOY revenue growth was 31.1%

In comparison, Tesla (whose models are all BEVs) delivered 435,059 units worldwide in the third quarter, a YOY increase of 26.5%. That may seem almost as impressive as BYD, but due to Tesla's aggressive price cuts (to sustain EV volume growth in the face of new entrants), Tesla's YOY revenue growth for the September quarter was a modest 8.8%.

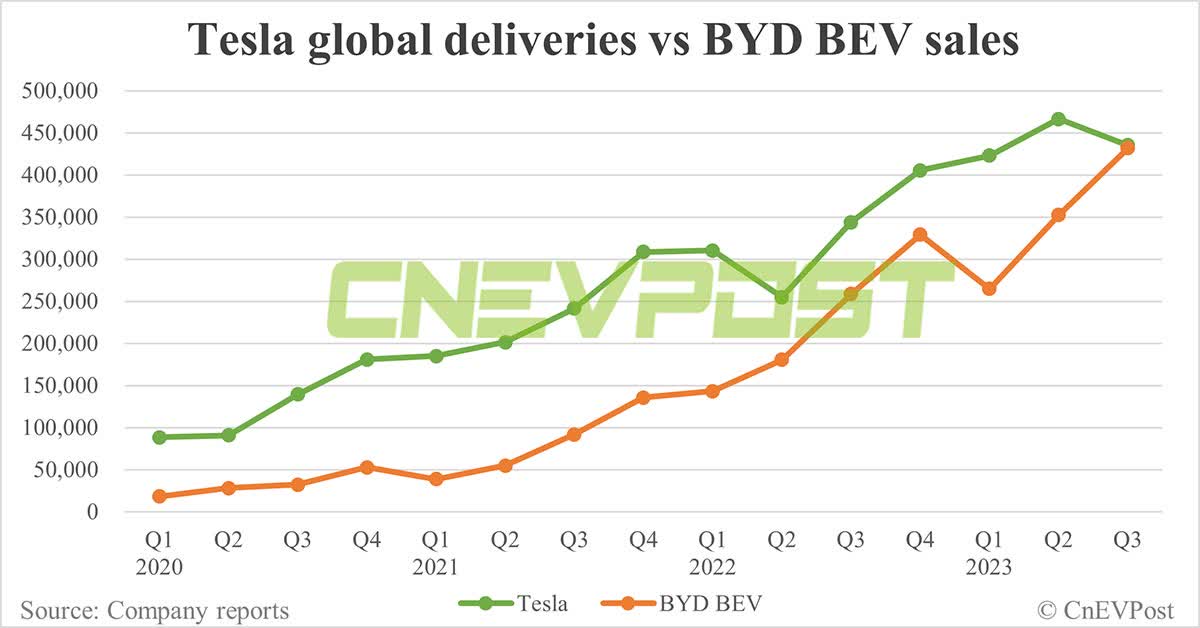

The neck-to-neck race of sales in 2023 up to Q3 '23 for the two companies is portrayed in the graph below. (Note the BYD figures below represent solely BEVs, not PHEVs – more on this later).

cnevpost.com

Sales in China in 4Q 2023

Although the final delivery numbers for December are not out, the trend below for November, showing deliveries in China (which is the main market for BYD and the second largest market for Tesla) shows how the pole position, as world's largest EV seller is about to move from Tesla to BYD.

cnevpost.com

In November, BYD sold 263,066 units in China, (made up of 168.776 BEVs, rest PHEVs) while Tesla sold 65.404 BEVs. Granted, Tesla has a larger presence in the US, but China's sales are the major growth variable.

It's almost a given that the world has a new EV leader, at least according to Bloomberg:

Chinese Carmaker Overtakes Tesla as World's Most Popular EV Maker

Elon Musk once scoffed at the notion that BYD could compete with his company. Now, the automaker run by billionaire Wang Chuanfu is poised to be the new No. 1 in electric vehicles.

The news headline, that BYD toppled Tesla as the world's leading BEV player in 4Q 2023 sales, once published this week, will be the catalyst that shifts investor attention from Tesla to BYD, and the glaring valuation differential, the focus of this article, will be redressed.

The importance of PHEVs

PHEVs or Plug-in Hybrids appear to be gaining popularity globally, partly because they receive the same tax incentives of pure BEVs (Battery Electric Vehicles) in many countries. But it's also due to range anxiety for BEVs, the consequence of inadequate electric charging networks in many geographies, including members of the European Union.

30% Of New Cars In France Now Plugin Electric Cars! Thanks to upcoming subsidy changes, plugin vehicles continue to rise in France, with last month's plugin vehicle registrations ending at 45,281 units. That total was divided between 30,769 BEVs (or 20% share of the overall auto market) and 14,512 PHEVs (10% share of the auto market).

The PHEV is a domain where BYD has strong offerings, but where Tesla is conspicuously absent. In China, BYD's home turf, hybrid vehicle have surged, posing a fresh threat to foreign automakers:

As EV makers in China wage an intense price war to prop up slowing demand, Chinese brands with strong hybrid lineups are emerging as winners, attracting consumers with vehicles with long range that can cost less than gasoline cars.

The BEV and PHEV combination offered by BYD is proving to be a powerful growth strategy. As seen from the table below (BYD global sales), even though BEV sales demonstrate superior growth rates, PHEVs are also in great demand, displaying robust growth rates too.

| BYD Global Sales 3Q 2023 vs 3Q 2022 | |||

| BEV | PHEV | Total NEV | |

| Jul-22 | 80 991 | 81 223 | 162 214 |

| Aug-22 | 82 678 | 91 299 | 173 977 |

| Sep-22 | 94 941 | 106 032 | 200 973 |

| Total 3Q '22 | 258 610 | 278 554 | 537 164 |

| Jul-23 | 134 783 | 126 322 | 261 105 |

| Aug-23 | 145 627 | 128 459 | 274 086 |

| Sep-23 | 151 193 | 135 710 | 286 903 |

| Total 3Q '23 | 431 603 | 390 491 | 822 094 |

| Quarter YOY Growth % | 66.9% | 40.2% | 53.0% |

Source: author's work

Next, some detail on new models that BYD has launched in Europe in 2023, that critics reviewed with high acclaim.

BYD models make waves in Europe

Despite incurring a 10% import duty imposed on Chinese EVs in Europe, newly launched BYD models have received excellent reviews in Europe:

BYD Seal: A Potential Tesla Model 3 Killer! The BYD Seal is set to make a significant impact in the electric vehicle market with its impressive looks, power and performance, advanced features, build quality and safety, E-Platform 3.0 technology, efficiency and climate adaptability, and its ability to compete with luxury sedans. With its upcoming launch in the global market, the BYD Seal proves to be a strong contender. Whether it's the impressive range, advanced blade battery technology, or the sleek and luxurious design, the BYD Seal 2023 has something to excite every electric vehicle enthusiast.

BYD Yangwang U8: A 1,100-Hp EV Off-Roader From China That Breaks The Game. An EV that puts every American off-roader to shame. Even more surprising is that despite the high-powered, fully-electric drivetrain, the SUV is underpinned by a ladder-frame chassis. This means that the Yangwang U8 features a body-on-frame construction similar to the increasingly rare, rugged SUVs like the Toyota Land Cruiser.

Valuation

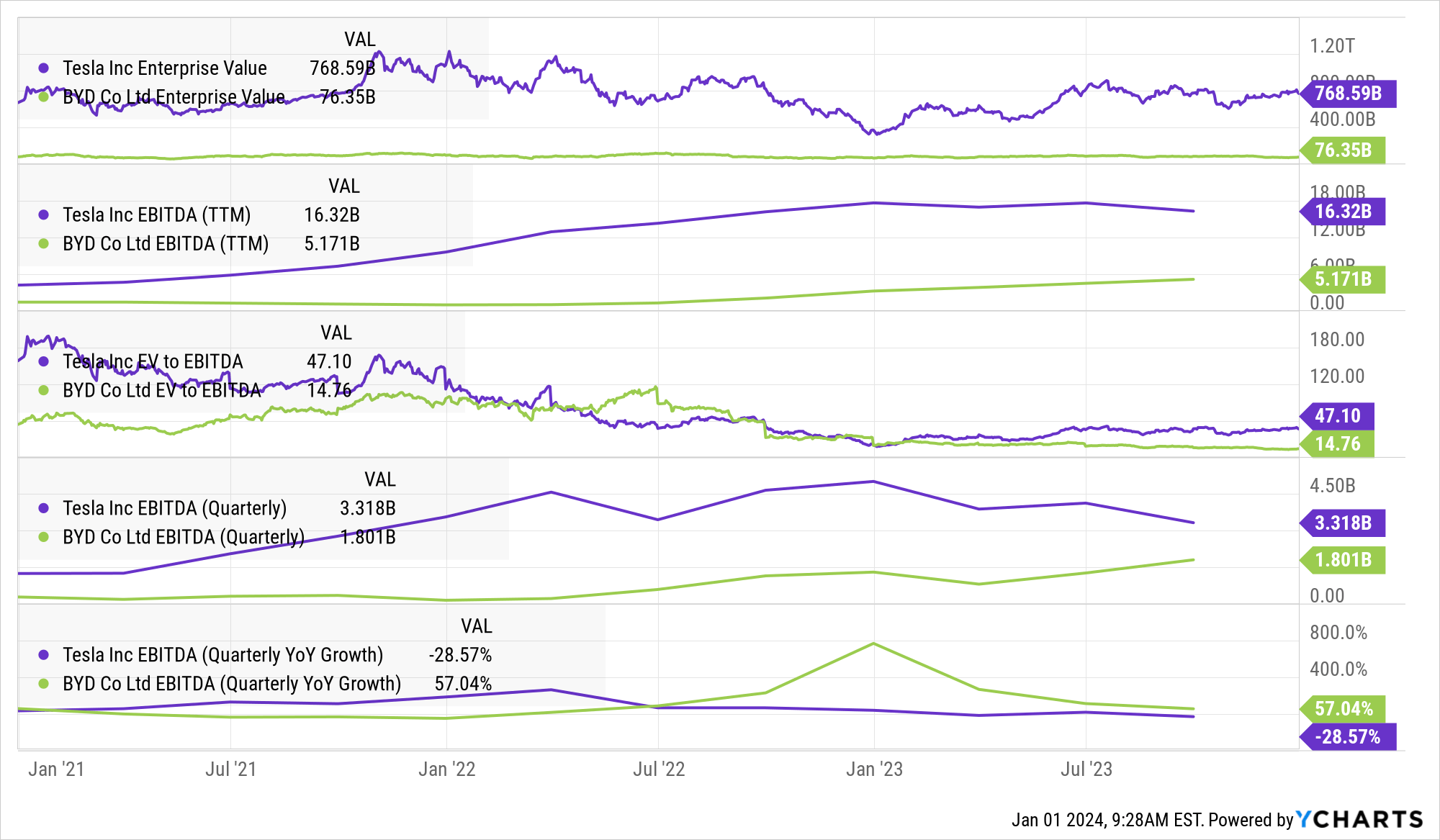

BYD vs Tesla Valuation Metrics (ycharts.com)

In the graph above, the first panel shows the enormous difference in the Enterprise Values of the two companies, $769Bn for Tesla and $76Bn for BYD, or a 10X difference. Yet the second panel shows that over the last 12-months, Tesla's profit (EBITDA) was higher only by a 3.2X multiple. It's clear that the valuation gap is explained by the valuation multiple accorded by investors – Tesla sports an EV/EBITDA multiple of 47.1X whereas BYD is valued at a 14.8 EV/EBITDA ratio. The irrationality of the market is further demonstrated by the growth in EBITDA for the latest September quarter (final panel in graph above): BYD posted a YOY growth of 57%, while Tesla's EBITDA actually contracted by 28% from the previous year.

The valuation gap between the two companies is bound to narrow, with BYD rising as investors discover this relatively unknown entity, and Tesla falling after a meteoric rise in 2023 as investors digest the declining profit trend.

BYD vs Tesla: Sales and Margins

Sales and Margin Trende (ycharts)

Salient points from graph above:

- Tesla is valued multiples higher on an EV/Sales basis;

- Tesla has greater sales in the latest twelve-month period, but only slightly so. ($96Bn for Tesla vs $82bn for BYD).

- The more relevant point for the investor is BYD's most recent sales growth (latest September quarter on YOY basis) is substantially higher than Tesla's – 31% vs 9%.

- Historically, Tesla garnered far higher operating margins than BYD, but the profitability for the two companies is now almost identical. Moreover, the trend for BYD is up while Tesla's is falling.

Summary

There seems little rational explanation for Tesla to trade at an EV/Sales ratio that is 8.5 multiples higher than BYD. The valuation chasm between BYD and Tesla has become so extreme, it defies rationality. Granted, Tesla holds unrealised potential in the form of Level 5 fully autonomous driving and Optimus robots, but there is insufficient evidence to date to incorporate their definitive success.

BYD is a Strong Buy here on a standalone basis – yet despite the Tesla's strong investor loyalty, I can't help taking a short position in Tesla – after the vertiginous rise in 2023 Tesla is highly likely to fall to bridge the valuation gap.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.