Diy13/iStock via Getty Images

The iShares MSCI Saudi Arabia ETF (NYSEARCA:KSA) is an ETF that follows the Saudi Arabian IMI index, its listed market with an overwhelming exposure to financials and then, of course, a little to oil exposures and oil adjacent industries. Financials in Saudi Arabia economically aren't materially different from how they'd function in other countries, so ultimately they have been benefiting from the mirrored monetary policy to the US due to their fixed exchange rate regime, and they are benefiting from substantial prospects to generate loan growth due to large megaprojects, and slight liberalizations that have probably met or are meeting thresholds for expatriate workers to be able to live there relatively comfortably for more extended periods of time. Additionally, Saudi Arabia has major tourism goals to grow the representation of tourism in GDP fourfold, and is serious about diversifying its economy away from oil, which all benefits financials. On the oil side, which is the other exposure, the oil economy in Saudi is suffering despite higher prices because they're the ones that had to cut to get prices high. We don't see emerging US capacity as too much of a threat, with low-hanging fruit already harvested, and still like long-term oil prospects, although we are concerned about recessions in key global economies. We do not like the 0.74% expense ratio, and PEs are already quite high as stalling financials income is combined with strong expectations that rate cutting will come soon, which will decrease cost of funds. It's still probably at fair value considering its prospects, but not especially compelling.

KSA Breakdown

The PE is 18.8x, and the expense ratio is 0.74%. The latter is high as this isn't the most accessible market. The PE reflects that people definitely are somewhat aware of the untapped potential of the non-oil economy.

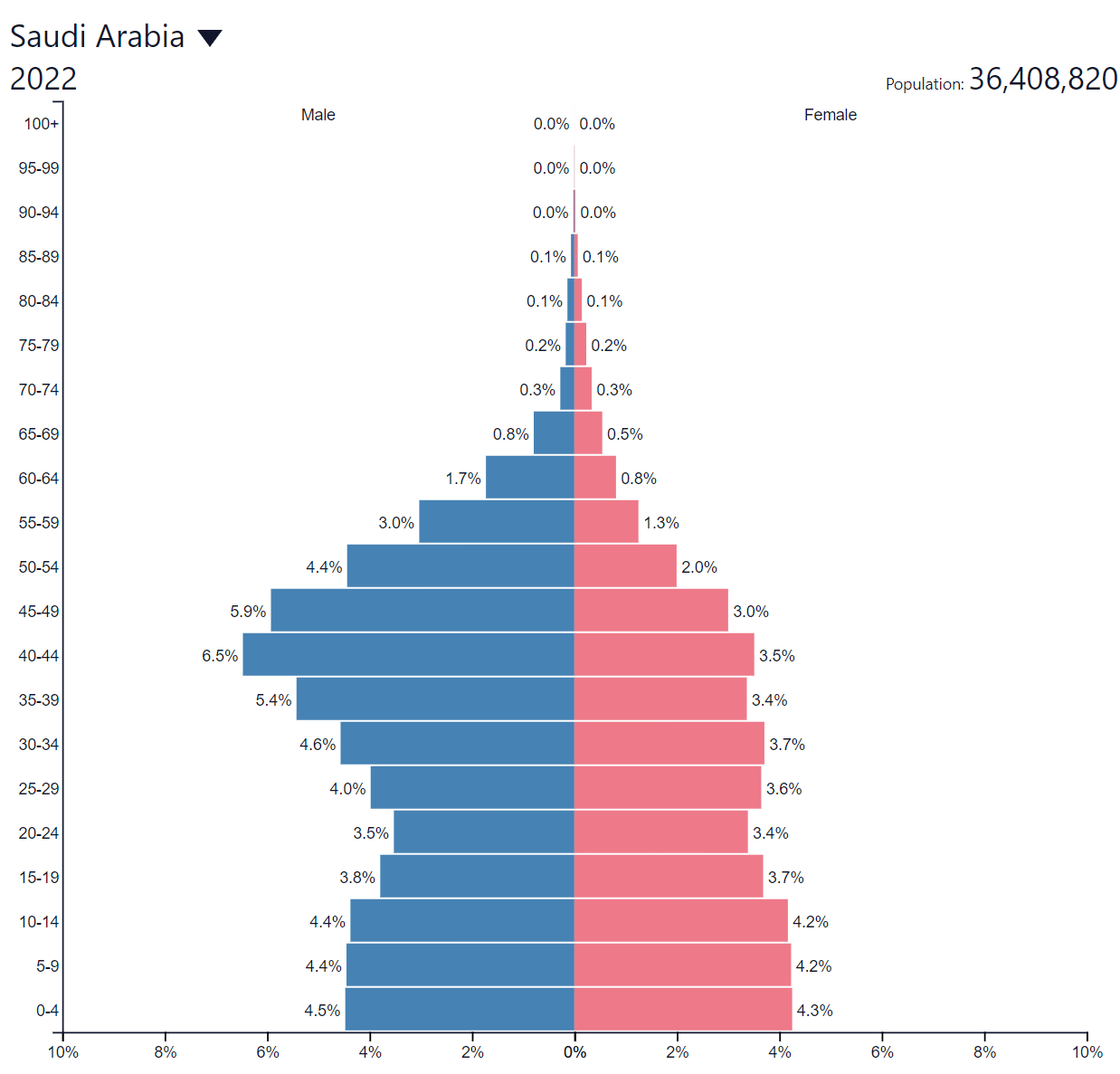

The Saudi demographic situation looks like this.

Saudi Population Pyramid (populationpyramid.net)

This bulge to the left is quite common for Gulf States, and we believe it comes down to the fact that they're in dire need of Western, middle-aged, professional men who are happy to come to a very traditional and Islamic country with low taxes and extraordinarily high expatriate pay. They are liberalizing slightly in other ways too that makes it easier for expatriates to live there, and likely these are the first overtures to making the sort of segmented expatriate society that exists in places like Dubai, where the much-needed professionals can socialize amongst themselves.

In general, Saudi is focused on trying to grow its non-oil economy, part of its core national plan the Vision 2030 program. They are going to make a push for tourism, and they will continue to expand investments into megaprojects, which has an important bearing on the financial exposures in the country. Corporate loans are growing to finance the companies that in turn are involved in the megaprojects, as well as other initiatives to increase homeownership, which has grown the mortgage books. Servicing larger numbers of expatriates and their money flows helps too. Balance sheets are growing healthily across Saudi financials. The issue is that there is some pressure on the cost of funding. Net income has actually stalled at some of the largest KSA allocations within the financial sector due to deposit beta ticking up. Therefore, while mirroring a Fed policy and having high-interest rates has afforded benefits for a while, the benefits are at the stage where they are peaking, and what would be best for the financials now is that the loans that are high rates on the asset side, which have grown nicely, are able to drive the benefits of the duration gap as the Fed finally brings down rates.

We've recently been saying that the key to that will be US maturity walls, which may transmit current policy more forcefully and create evidence that it's time to turn things down. The financial exposures in Saudi at this point are ready to benefit from that. The issue is that Al Rahji as an example, already trades at 22x PE in anticipation of all this, so these prospects are already rather priced in.

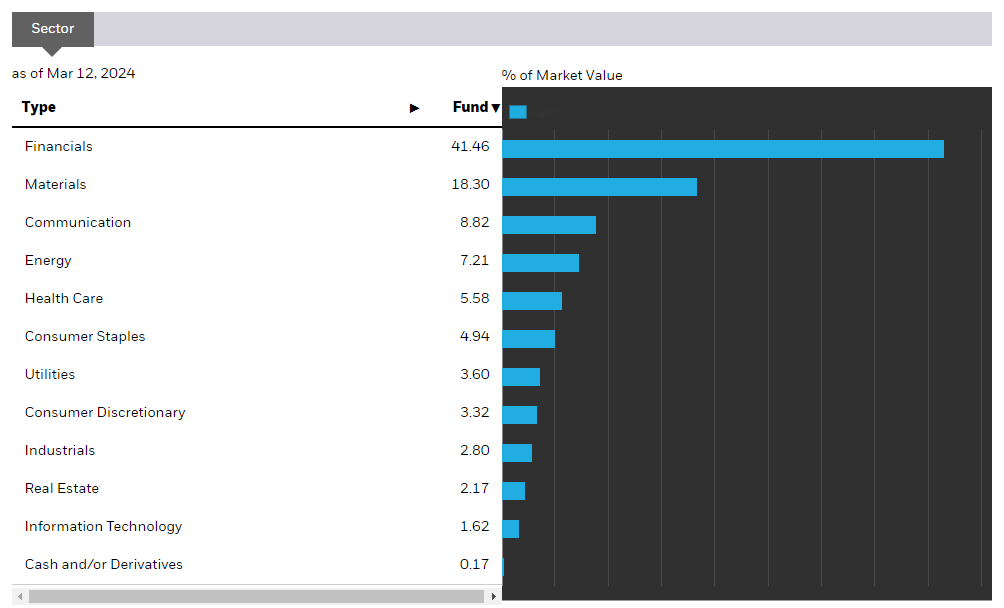

Sectors (iShares.com)

After Financials are the materials and energy businesses, which have some overlap. Materials includes major petrochem and other commodity chemical manufacturers, but also mining, where it has quite a lot of value in rare earths as well as gold. They have phosphate too, and some agricultural material exposures as well. The commodities that they mine are mostly performing well and are strategic, so no major concerns.

On oil, we note that the low-hanging fruit to increase capacity in the US have already been harvested. There isn't too much benefit left there, despite drill baby drill slogans from the Trump campaign. Incremental capacity will take some years to build up in the US, which means that the Saudi position is still very intact. Impact from the maturity wall would not be a good thing for the demand of oil in volumes. We'd be a bit concerned about that, and as the Saudis influence the price, it will come out of their volumes and continue to put pressure on their own oil-based GDP. Nonetheless, it is a strategic resource and the reduced stranded asset risk these days, since renewables got a bit trounced by the Ukraine war, means that these resources and the leverage they provide should keep Saudi Arabia comfortable in being able to exploit them optimally in our view.

Bottom Line

Financials are the core of the discussion and valuation, and our thinking is that the expectations and the thesis around rate cuts are already documented, and that those expectations are already priced in to the financial exposures in KSA. We are still concerned about a recession in other parts of the world, and that could come out of Saudi pockets, as they will likely want to keep oil prices high. Even if they lowered them for other strategic reasons, it would be volume into a weaker market, which isn't optimal. Other exposures are relatively resilient, or are at least strategic.

An 18.8x PE already implies substantial growth in earnings of the financials, which while possible, is not going to be so easy, and is dependent on the actions of other economies. Saudi Arabia is a reactive economy. The only leverage they might have now is indirectly on the outcome of the US election, where outcomes are usually decided by wallets, and no wallet likes a high oil price. It's difficult to guess how Fed policy transmission will change once corporates start running into maturity walls in the US. If this transmission doesn't improve meaningfully, we are still in the camp that inflation will be very sticky and that a real slowdown is needed in growth.