TransMedics Group, Inc. (NASDAQ:TMDX), a company you probably never heard of, is transforming the organ transplant landscape.

This is a rare opportunity to invest in a company that's going to save thousands of lives (and already has), at a very early stage, but with already proven capabilities and FDA approvals.

Let's dive in.

Introduction To TransMedics

TransMedics Group was founded in 1998 by Dr. Waleed H. Hassanein. It is a medical technology company focused on transforming organ transplant therapy for end-stage organ failure patients.

When it comes to organ transplants, there are essentially two primary goals. One is to maximize the utilization of potential donors, meaning that no healthy organs of donors go to waste. The second is to reduce post-transplant complications.

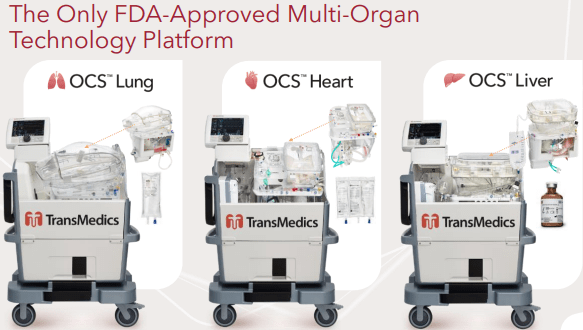

TransMedics developed a platform that's currently by far the leader on both these fronts in lung, heart, and liver transplants.

TransMedics Group Q4'23 Investor Presentation

The Organ Care System (OCS) allows donor organs to be maintained for longer periods of time, essentially mimicking a human environment, while keeping the organ in optimal condition to prolong its vitality and minimize post-transplant complications.

Today, the most commonly used method for organ preservation is cold storage, which is inferior to the OCS on both fronts.

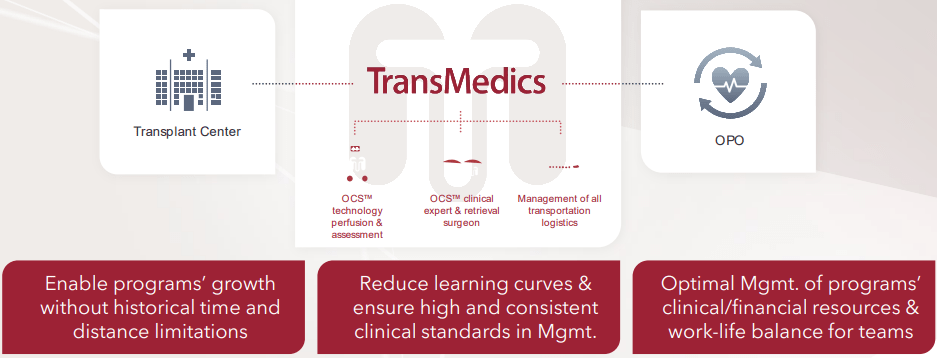

TransMedics also provides logistic solutions, and clinical experts which are specialized in organ transplants and the use of its technology, ensuring the success of the process.

The Transplant Chain & TransMedics Logistics

The organ transplant chain is a complex system with multiple parties. There are 250 transplant centers in the United States. These are specialty hospitals that are staffed and equipped specifically for complex transplant procedures.

In a typical transplant, the donor is in a different hospital, which is usually several hours away from the relevant center. When a donor suffers from brain death or circulatory death, their hospital is ready to preserve the relevant organs, either with the legacy cold storage method or the new OCS. When the organ is ready for transportation, it's usually delivered via flight to the relevant transplant center, where the procedure takes place.

In a typical transplant process, the receiver's insurance coverage pays the center for the procedure, and the center pays for the delivery of the organ, which means the center incurs the cost of transportation and storage.

After two years of general availability, TransMedics came to realize one of the biggest bottlenecks in the chain was in the transportation stage. Legacy players used to rely on charter flights, which weren't ideal.

Charter flights are more expensive, planes are old and not safe, and their routes aren't optimized for the geographic locations of the transplant centers which comes with higher costs and a low probability of getting there in time.

This has led TransMedics to acquire Summit Aviation, a full-service aviation company, in August 2023. Initially, the market didn't understand the acquisition, which makes sense considering it seems like a classic task to outsource.

However, as time went by and management explained its reasoning, the value of an air logistics capability that's exclusively dedicated to organ transplantation became increasingly clear and is viewed as a huge competitive advantage.

TransMedics Group Q4'23 Investor Presentation

With the acquisition, TransMedics launched the National OCS Program (NOP), which provides a one-stop-shop for transplant centers. The program provides the technology, staff, and logistics needed to maximize utilization and patient outcomes.

The Market

Today, TransMedics provides solutions in three organ programs – liver, lung, and heart.

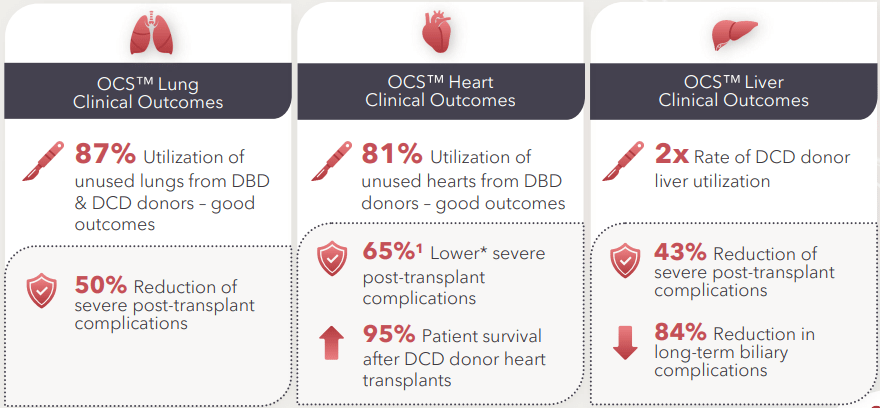

The company's proprietary technology and innovative logistic model, which came into use in 2023, resulted in a double-digit increase in the number of transplants in each of those organs, the first double-digit annual increase since 2016, and only the second since 2000.

TransMedics Group Q4'23 Investor Presentation

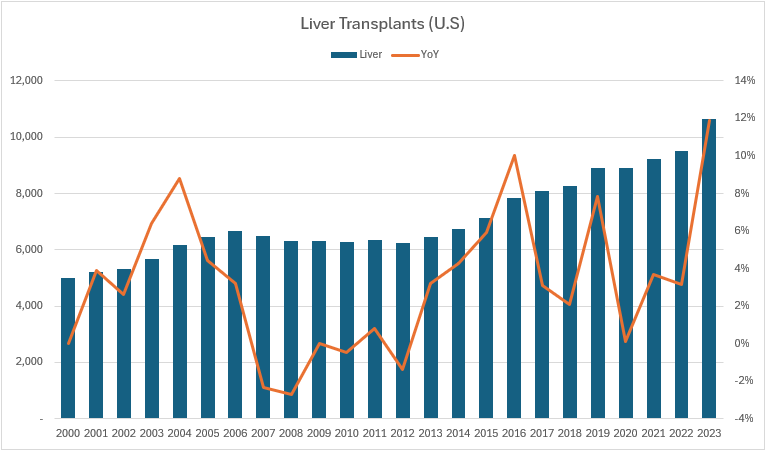

Liver

Liver is currently the largest business for TransMedics, responsible for 68% of revenues in the U.S. with $151.7 million, and 64% of revenues worldwide, with $151.8 million.

According to the Organ Procurement and Transplantation Network (OPTN), 10,660 liver transplants took place in the U.S. in 2023, up 11.9% Y/Y.

Created and calculated by the author based on data from OPTN.

As we can see, liver transplants reached a record annual growth in 2023, with TransMedics deserving much of the credit. According to management, they held a 17% share of U.S. liver transplants in 2023.

Based on that, we can estimate the current liver TAM at $900 million. While it could be argued this shows a somewhat small market, it's important to note that the market grew at a double-digit pace last year and should continue to grow at an elevated pace, driven by increased utilization enabled by TransMedics as thousands of people needed a transplant and didn't receive one.

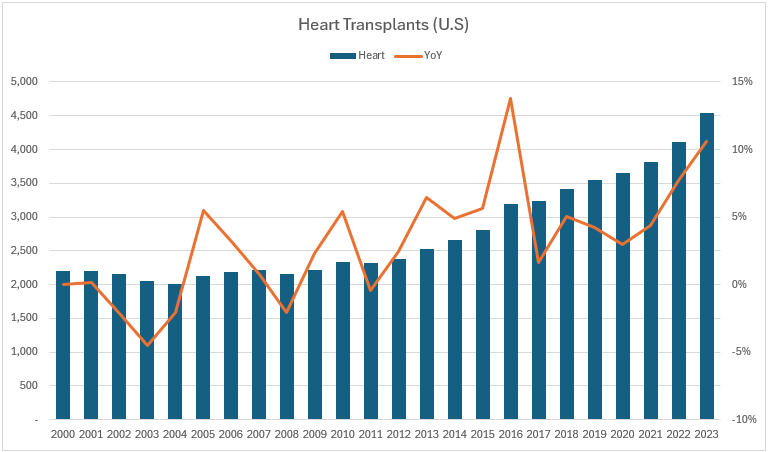

Heart

On the Heart, the second-largest business for the company, which is responsible for 27% of revenues in the U.S. with $59 million, and 31% of revenues worldwide, with $73 million.

According to the OPTN, 4,545 heart transplants took place in the U.S. in 2023, up 10.6% Y/Y.

Created and calculated by the author based on data from OPTN.

Heart also reached a record, and the second-largest annual growth rate since 2000. According to management, they held a 16% share of U.S. heart transplants in 2023, reflecting a $370 million TAM.

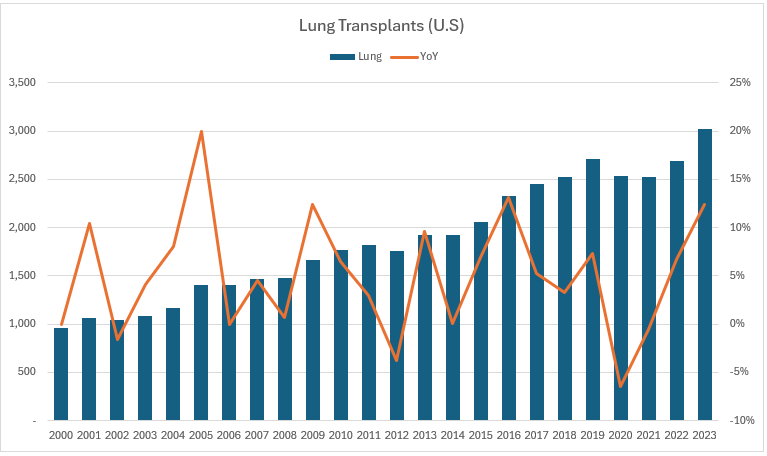

Lung

Lungs are currently the smallest part of the business, with approximately 5% of U.S. and worldwide revenues, totaling $10.5 million and $10.8 million, respectively.

According to the OPTN, 3,026 lung transplants took place in the U.S. in 2023, up 12.4% Y/Y.

Created and calculated by the author based on data from OPTN.

Lung transplants in 2023 were the highest ever, with the highest annual growth rate since 2016. According to management, they held a 4% share of U.S. heart transplants in 2023, reflecting a $263 million TAM.

Valuation & Opportunities

Adding up the TAMs we discussed above, we can estimate the U.S. market size at over $1.5 billion in 2023, growing at a 12% pace. The worldwide market is of course much bigger, but it's more of a long-term opportunity.

So, there's huge room for growth and market share gains in the near term, with management targeting revenues of $370 million in 2024 (53% growth), and 10,000 transplants in 2028 (more than 4x from 2023).

In terms of profitability, they expect gross margins in the 64% range, and operating expense growth of 35% at the mid-point, equaling a $23 million operating profit target for 2024.

Considering this is the same management that guided for $145 million in revenues in 2023 and ended up achieving almost double that, I'd say we can trust they will, at the very least, achieve their targets.

With a market cap of $2.7 billion and a net cash position of $335 million, TransMedics trades at a $2.4 billion EV, reflecting a seemingly high EV/EBIT multiple of 104x on 2024 guidance.

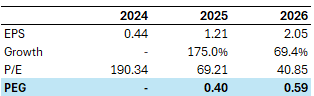

Looking at consensus estimates, TMDX is expected to generate EPS of $0.44 in 2024, also reflecting a high multiple at a 191x P/E.

However, there are several caveats. First, consensus estimates are currently aligned with the mid-point of management's guidance, which we saw is quite conservative. Two, and more importantly, this is a hyper-growth company. This means we should adjust its valuation to its expected growth rates.

Based on EPS estimates of $1.21 in 2025, and $2.05 in 2026, TMDX trades at the following PEG ratios:

Created and calculated by the author using data from Seeking Alpha

I estimate there's a much higher probability that TMDX beats those estimates over missing them, which means the real PEGs are even lower.

Being a relatively small company, TMDX is also a prime acquisition target for large med-tech companies. At these growth rates and with its strong balance sheet, we should expect at least a 30% premium over the average 5.0x-6.5x EV/Sales multiple in industry takeovers, reflecting more than 50% upside if we apply 2025 estimates.

Risks

When investing in a company like TransMedics, there are several risks to take into account.

First, the valuation is based on significant future growth and margin expansion, both are uncertain. Additionally, the market appetite for this type of risky investment can be volatile and fluctuate materially based on macro expectations. Another thing to consider is there's no obvious “floor” here in the form of a P/E multiple that's unquestionably low.

Second, there's the risk of competition. With gross margins north of 60% (and a potential to surpass 70% over time), there's always the risk of larger competitors wanting to take a piece of the pie. In addition, there are two other players with perfusion systems, called OrganOx and XVIVO. OrganOx is only in the liver, and XVIVO is only in the lung. Both are much smaller than TMDX and have much lower shares in their respective organs.

In that regard, TransMedics' technology is protected by patents, it has relationships with 98 transplant centers, and it built a unique logistics and services arm that's hard to duplicate. To me, those are strong entry barriers.

Lastly, there's execution risk. We're talking about a very young company, that's only getting started. It only reached GAAP profitability in Q4'23, and there's essentially no track record to rely on.

Conclusion

TransMedics is revolutionizing the organ transplant landscape. The company reached a tipping point in terms of profitability and market share and is now driving a nationwide acceleration in transplant growth.

The existing TAMs are already big enough for the company to more than 4x its revenues by 2028, with continued margin expansion and gross margins that approach 70%.

On top of that, there are several long-term opportunities outside the U.S., and adding additional organs.

Being a young company with a low market cap, there are several risks, but the current valuation, based on the company's future growth prospects, provides an extremely attractive risk/reward opportunity.

Therefore, I rate TransMedics as a Strong Buy.