I believe Cloudflare's (NYSE:NET) share price has front run the company's fundamentals in recent months after a solid fourth quarter and positive management commentary. While I don't expect the company's growth to deteriorate meaningfully, absent a recession, I think near-term expectations have become too optimistic.

Customers remain cautious in regard to technology investments, although conditions appeared to improve slightly in the second half of 2023. With a realization that rates will remain higher for longer, spending could come under pressure again. Given Cloudflare's current valuation, any weakness is likely to be severely punished.

I previously suggested that near-term expectations were too high and that Cloudflare was at risk due to its high valuation. The stock is up roughly 8% since then but has struggled in recent weeks as investors grapple with higher interest rates and elevated geopolitical risk.

Market Conditions

Cloudflare's fourth quarter results were strong across the board. In addition to solid revenue and ACV growth, pipeline growth rates, sales productivity, average deal size and linearity all improved compared with the previous quarter. Cloudflare’s federal business was strong, including one particularly large Zero Trust deal with the Department of Commerce

While the macro environment has stabilized, conditions are still challenging. Cloudflare hasn't seen any signs of spending fatigue in security, stating that the threat landscape continues to drive demand. I believe that companies who pointed out spending fatigue in Q4 are facing idiosyncratic issues.

The number of job openings mentioning Cloudflare in the job requirements and the number of Cloudflare job openings have ticked up in recent months, which possibly supports the notion of improved conditions.

Figure 1: Job Openings Mentioning Cloudflare in the Job Requirements (source: Revealera.com)

Figure 2: Cloudflare Job Openings (source: Revealera.com)

I am extremely bullish about Cloudflare's long-term prospects and believe there is a large amount of latent demand that will be unleashed in a stable macro environment with lower interest rates. With expectations of rate cuts rapidly falling away, I would not be surprised to see further weakness going forward though.

Figure 3: “Cloudflare Pricing” Search Interest (source: Created by author using data from Cloudflare and Google Trends)

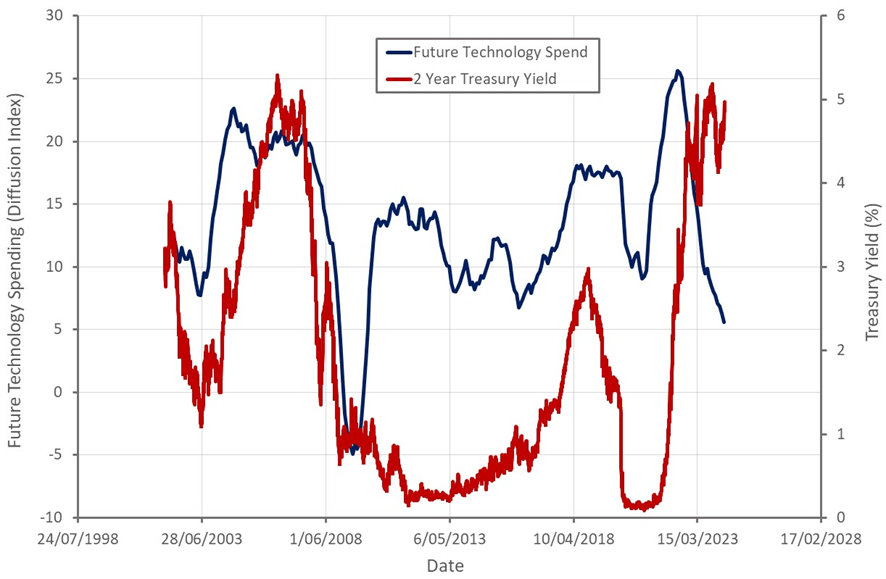

Figure 4: Future Technology Spending Plans and US 2-Year Treasury Yield (source: Created by author using data from The Federal Reserve)

Cloudflare Business Updates

Cloudflare’s product portfolio has expanded dramatically in recent years, with the company now having more than 50 revenue generating products. Cloudflare’s platform delivers integrated security, performance and a programmable edge that augments existing applications and allows the creation of new applications without configuring or maintaining infrastructure. The company is positioning itself as a connectivity cloud rather than a fourth hyperscaler though.

Cloudflare is building on this vision with the recently announced launch of its Magic Cloud Networking product. Magic Cloud Networking allows customers to easily connect and protect public and private cloud environments and avoid public cloud lock-in. This product is built on Cloudflare's acquisition of Nefeli, a multi-cloud networking startup. Nefeli provides a unified network management layer for cloud infrastructure deployments. Magic Cloud Networking integrates Nefeli's technology with Cloudflare's connectivity cloud.

Zero Trust

Cloudflare's Zero Trust solution now has feature parity with competitors, and as a result, it is gaining momentum. Cloudflare incurs minimal incremental cost from deploying Zero Trust, providing it with a large advantage. The company has suggested its Zero Trust gross profit margins are around 90%. Zero Trust also provides a source of revenue that requires limited incremental CapEx.

SASE is an expensive product that is often sold at the executive level, and this appears to have caused some issues with Cloudflare's go-to-market motion. Cloudflare continues to overhaul its sales organization, bringing on more senior leadership. This includes Mark Anderson, who was recently made President of Revenue. Mark was CEO of Alteryx (AYX) and previously led Palo Alto's (PANW) sales organization. Cloudflare is reportedly seeing greater productivity out of its sales organization on the back of improvement initiatives.

The growing success of Cloudflare's SASE solution could also be a driver of channel sales as larger deals attract partners. Channel-enabled revenue increased 70% YoY in Q4. Cloudflare is also now reportedly having more success penetrating larger organizations, and some of the company's largest wins in Q4 were SASE deals. As companies like Cloudflare introduce more feature complete SASE solutions, I expect that pressure will mount on early leaders, like Palo Alto Networks and Zscaler (ZS).

Figure 5: Cloudflare Relative Share Price Performance (source: Seeking Alpha)

AI

Cloudflare continues to see demand from companies using its infrastructure to move data to available and affordable GPUs in order to train AI models. This helps customers to avoid exorbitant egress charges for moving data. This business probably won't be sustainable long-term though. As the supply of GPUs catches up with demand, there will be less need for this type of service. There is also the risk of the cloud hyperscalers reducing or even removing egress fees.

Cloudflare wants to have GPUs for inference in every location by the end of the year. The company is currently utilizing GPUs from NVIDIA (NVDA), Intel (INTC) and AMD (AMD), as well as ASICs. Cloudflare also wants to abstract the hardware so that customers can deploy models without worrying about infrastructure.

Cloudflare's is seeing strong interest in its vector database and believes that it is a large opportunity. Vectorize is designed to allow customers to build AI applications on Cloudflare’s network. This is unlikely to be a near-term revenue driver though, as Cloudflare is currently focused on adoption rather than monetization.

Cloudflare recently announced Firewall for AI, a Web Application Firewall that it is developing specifically for applications using LLMs. This is a natural fit for Cloudflare as some of the vulnerabilities facing LLMs are similar to traditional web applications and APIs, like injections and data exfiltration. LLMs also introduce new issues though, in large part due to their non-deterministic behavior and because data is incorporated into the model through training. Cloudflare is working on functionality that would analyze prompts to try and identify malicious behavior.

Financial Analysis

Cloudflare’s fourth quarter revenue was 362.5 million USD, up 32% YoY. New ACV was up nearly 40% YoY and current RPO increased 35%. Results were driven by larger customers, with Cloudflare adding a record number of net new customers, spending more than both 0.5 million USD a year and 1 million USD a year. Cloudflare One also contributed to the strong Q4 performance, and EMEA revenue increased 38% YoY.

Cloudflare expects 372.5-373.5 million USD revenue in the first quarter, representing a 28-29% increase YoY. Full year revenue growth is currently expected to be 27%. While Cloudflare’s guidance is conservative, I think there is an elevated risk that growth doesn’t accelerate to the extent that investors expect. Performance in 2024 could be dominated by the path of interest rates and how customers respond to this.

Figure 6: Cloudflare Revenue Growth (source: Created by author using data from Cloudflare)

Cloudflare continues to see fairly strong growth in its customer base, particularly amongst customers who are spending more. Large customers are now responsible for 66% of Cloudflare’s revenue.

Table 1: Cloudflare Customers (source: Created by author using data from Cloudflare)

Cloudflare's dollar-based net retention rate was 115% in Q4 and has been relatively stable over the past few quarters. While this amount of expansion is solid in the current environment, Cloudflare has been targeting a higher net retention rate as its product portfolio has evolved.

Figure 7: Cloudflare Net Retention Rate (source: Created by author using data from Cloudflare)

Cloudflare is still not profitable on a GAAP basis, although margins have improved in recent quarters. This isn't a particularly important consideration, as Cloudflare is choosing to invest in future growth rather than realize current profitability. Cloudflare's growth is efficient, supporting this tactic.

Figure 8: Cloudflare Operating Profit Margin (source: Created by author using data from Cloudflare)

Conclusion

First quarter revenue should be strong and there will likely be a slight growth acceleration from the fourth quarter. While this is positive, it is already more than priced into the stock. In addition, the recent shift in interest rate expectations will likely weigh on customer spending going forward, potentially causing guidance to be soft. Cloudflare's valuation leaves little room for error, particularly given the current interest rate environment.

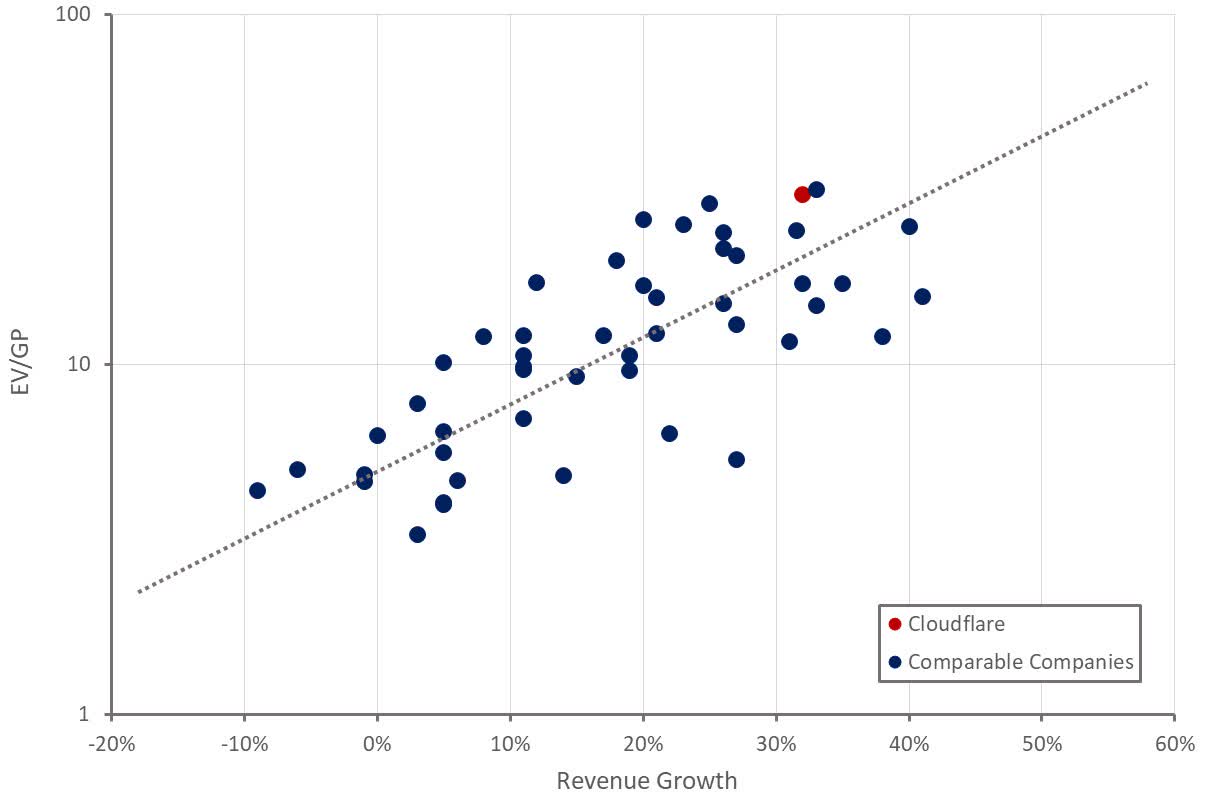

Figure 9: Cloudflare Relative Valuation (source: Created by author using data from Seeking Alpha)