Depending on investors' tax brackets and risk tolerances, JEPI's stellar dividend yield can offer excellent income during this uncertain macroeconomic environment. The recent banking crisis, the Fed's continuous interest rate hikes, and OPEC+ cuts may further contribute to the volatile market sentiments, sustaining JEPI's returns through 2024, if not 2025.Combined with JPM's excellent backing, investors may want to add JEPI into their portfolio, to balance long-term dividend income and portfolio growth.

JEPI ETF: Stellar Dividends In Volatile Market Conditions

The Market Leading ETF Investment Thesis

The JPMorgan Equity Premium Income ETF's (NYSEARCA:JEPI) outperformance can be tracked through the inflow of funds thus far, which continues to outperform its peers.

JEPI Inflows Compared To Peers

By FQ1'23, JEPI recorded a total of $5.86B inflow of funds, expanding by +179% YoY. Notably, the ETF outperformed the Schwab U.S. Dividend Equity ETF (NYSEARCA:SCHD), which recorded only +85.5% growth in funds inflow YoY. Interestingly, the rest, such as SPDR S&P Dividend ETF (NYSEARCA:SDY), Invesco QQQ Trust ETF (NASDAQ:QQQ), and the S&P 500 (NYSEARCA:SPY), had reported YTD fund outflows instead.

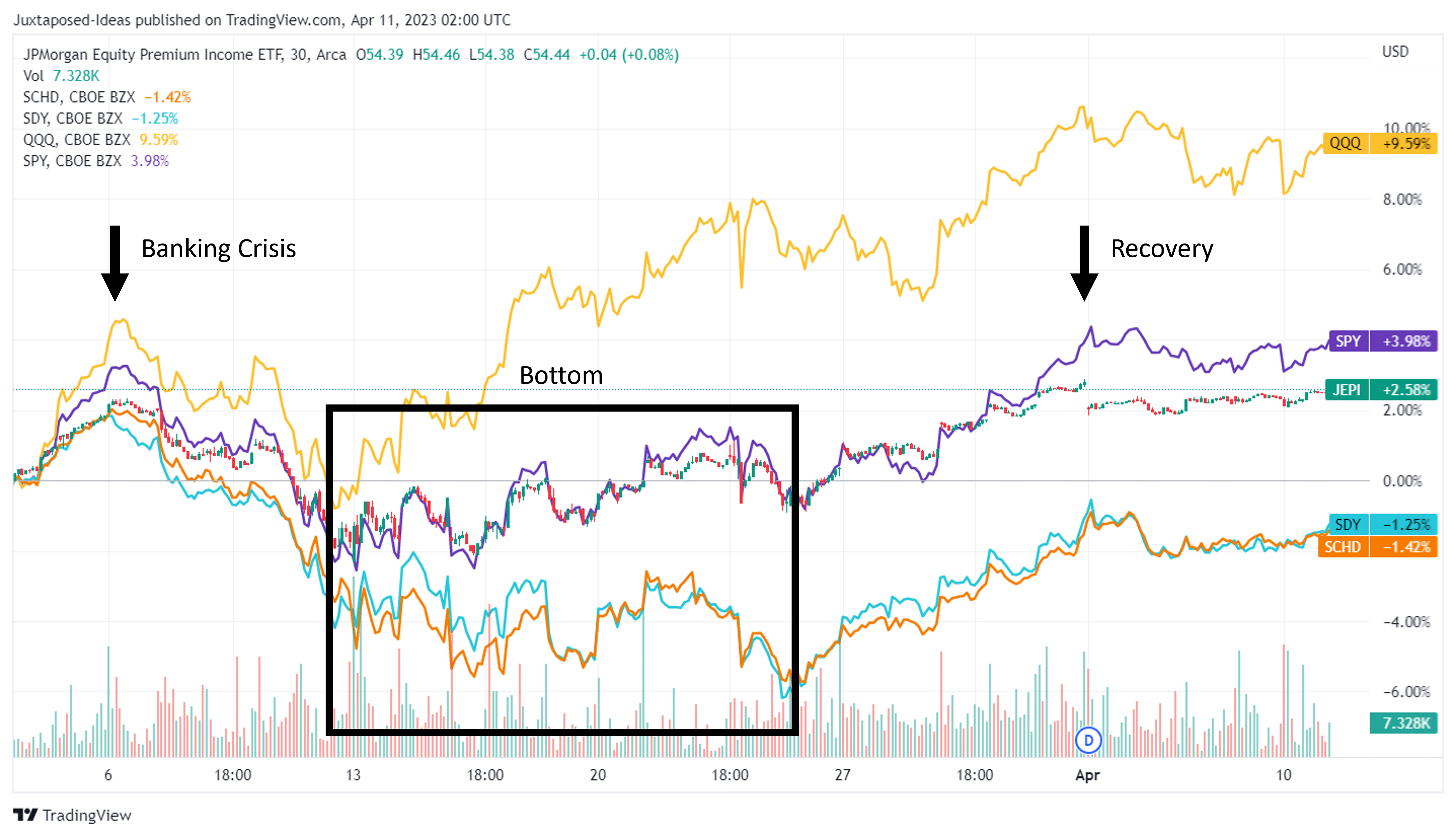

JEPI's Performance During Banking Crisis

The recent banking crisis had also triggered a deposit run, with -$235.5B outflowing from smaller US banks, $72.7B of deposits flowing to big US banks, and $273.3B to money market funds by the end of March 2023. Due to the extreme pessimism then, many ETFs had also drastically declined, including JEPI by mid March 2023.

However, the inflow of funds at $1.67B in March 2023 and JEPI's rapid recovery by early April 2023, compared to SCHD and SDY, demonstrated the investors' growing confidence in the ETF in our view.

This optimism might be partly attributed to its parent bank as well, JPMorgan Chase (NYSE:JPM), which supposedly “raked in billions in new deposits,” with Bank of America (NYSE:BAC) similarly adding $15B of deposits then. Combined with Jamie Dimon's role in leading the $30B of deposits to stabilize First Republic Bank (NYSE:FRC), a troubled mid-sized bank then, it was unsurprising that JEPI had performed relatively well.

JEPI Short Interest

Interestingly, JEPI came with an elevated Short Interest Volume of 595K shares with 0.18 Days to Cover based on NYSE, compared to SCHD at 380K/ 0.14 Days and SDY at 47K/ 0.13 Days to Cover, though naturally lower than Original Postsq">QQQ at 5.3M/ 0.19 Days and SPY at 163M/ 2.51 Days.

Given that short interest is often an indicator of pessimistic market sentiments, it is not overly bearish to surmise that we may see more market bottom retests ahead. The stock market sentiments are naturally worsened after the recent banking crisis and the Fed's sustained interest rate hikes, with the potential terminal rate of 5.25%.

Furthermore, the rising inflationary pressures were aggravated by the recent OPEC+ cuts, potentially upending the Fed's plan of reaching a 2% inflation target rate. Market analysts were already expecting higher Brent oil prices nearer to $100 by the end of 2024, compared to pre-pandemic levels of $60, suggesting further headwinds to the macroeconomic sentiments.

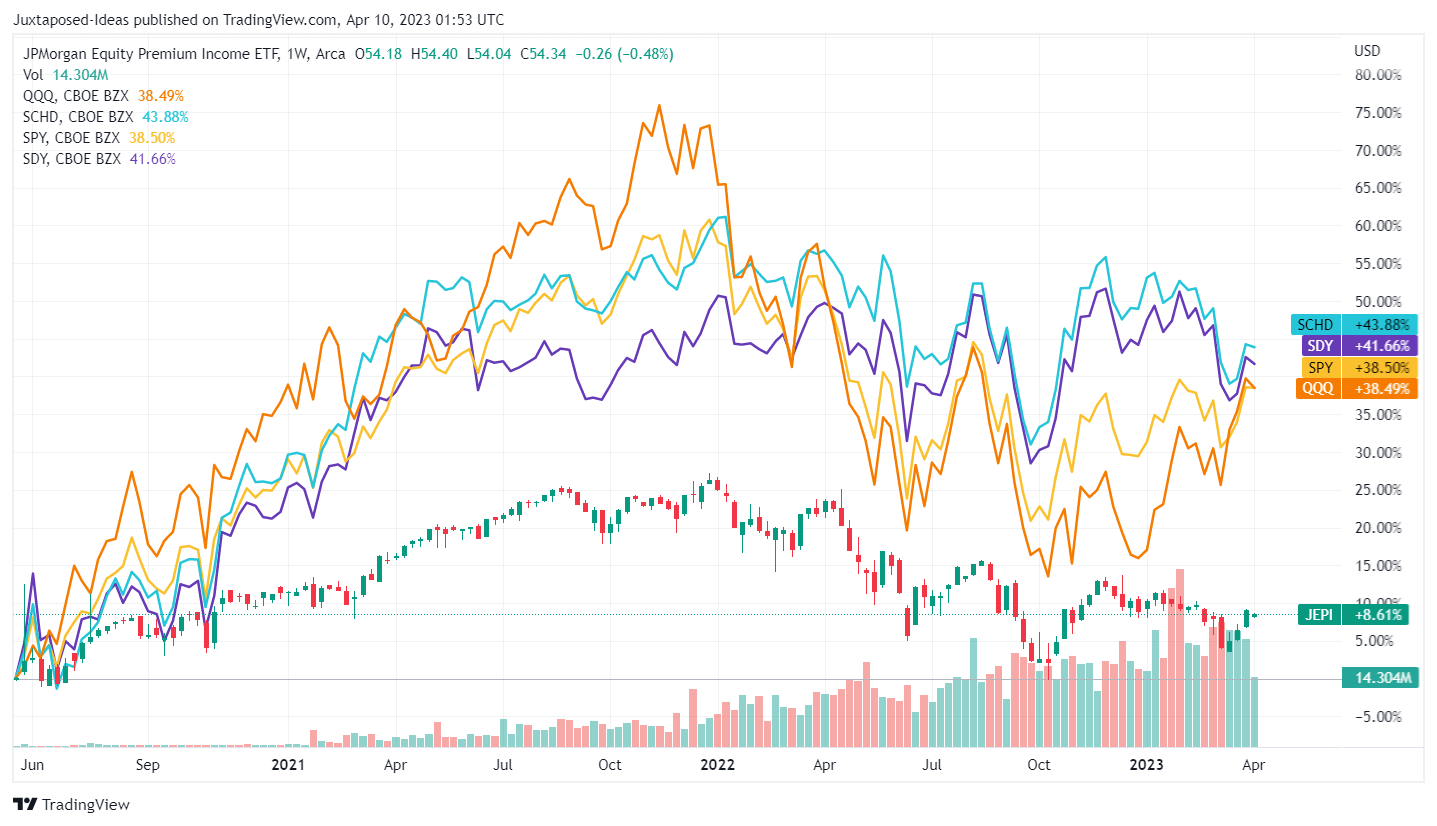

JEPI, SCHD, SDY, QQQ, & SPY 3Y ETF Prices

Furthermore, JEPI had underperformed against its ETF peers over the past three years, recording only an +8.61% gain since its peaks in April 2022, compared to SCHD at 43.88%, SDY at +41.66%, QQQ at 38.49%, and SPY at 38.50%. Otherwise, on an annual basis, JEPI (omitting dividends) only recorded an approximate 3Y CAGR of 2.01%, compared to SCHD at 13.42%, SDY at 12.44%, QQQ at 13.07%, and SPY at 13.46%.

JEPI, SCHD, QQQ, & SPY YTD ETF Prices

Then again, if we were to look at its performance YTD, JEPI only recorded a minimal decline of -0.69% compared to SCHD at -3.29% and SDY at -2.02%, though lagging behind SPY at +7.45% and QQQ at +20.25%.

Furthermore, investors must understand that the ETF is designed for those “seeking consistent premium income with lower volatility” and a “lower beta than the S&P 500 Index” (-37% since inception). At its worst, JEPI only recorded a -19% decline between the December 2021 peak and October 2022 bottom, comparable to SCHD at -17.7%/ SDY at -12.9%, but much improved compared to QQQ at -34.1% and SPY at -24.5%.

Given that JEPI is also a covered call ETF, we reckon it may continue performing excellently over the next year, if not two. Despite capping the upside potential, the covered call strategy also comes with a lower volatility, especially given the well “diversified equity portfolio.”

The ETF also reported 195% of turnover ratio by mid 2022, suggesting that the fund managers had been actively/ aggressively trading to generate improved returns, attributed to the opportunistic market conditions over the past three years. This goes against a buy and hold strategy where returns were more dependent on market movements, despite the higher transaction costs commonly associated with higher turnover rates.

For now, JEPI offers a stellar forward dividend yield of 11.47%, compared to SCHD at 3.62%, SDY at 2.55%, QQQ at 0.68%, and SPY at 1.58%.

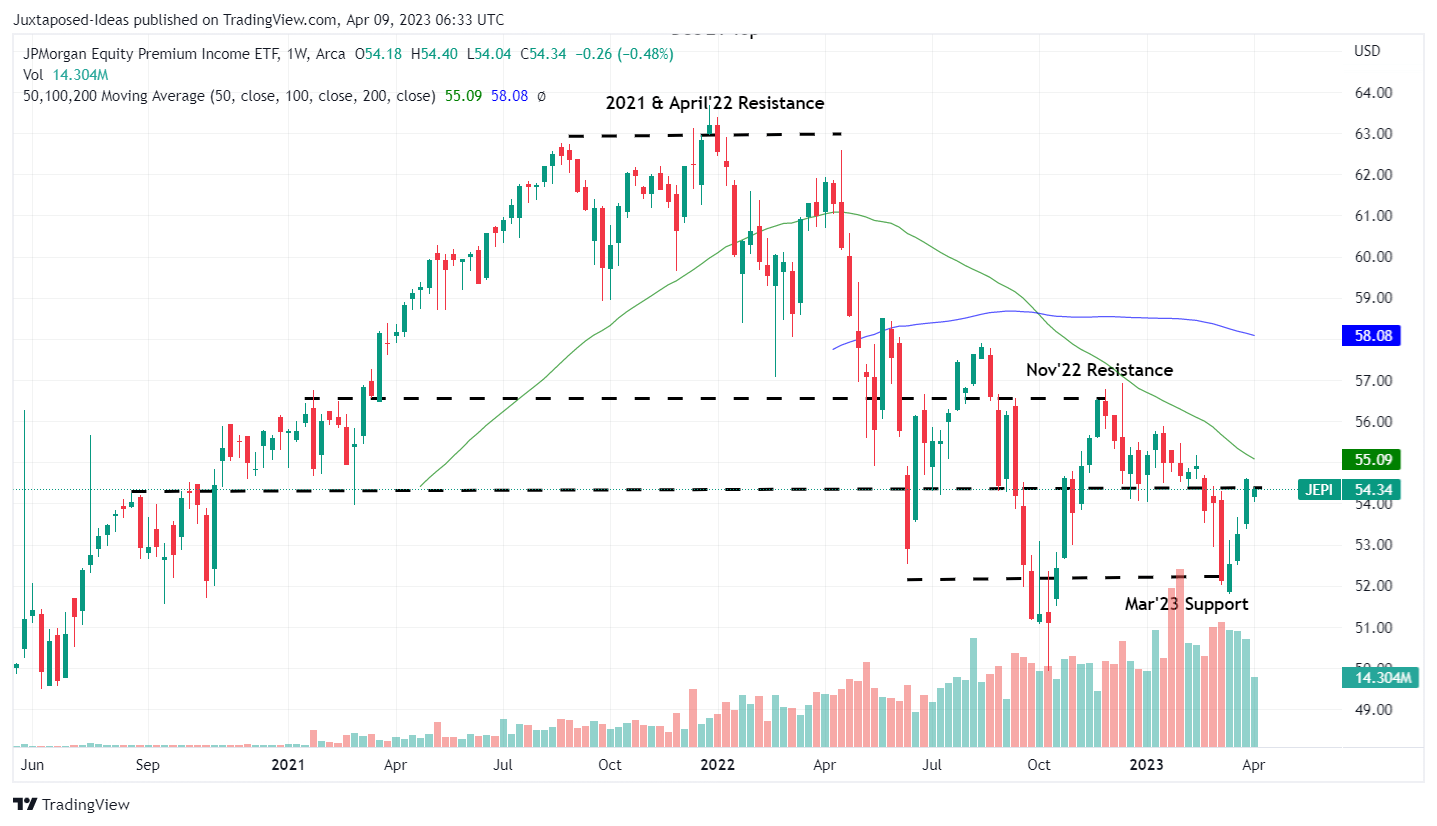

JEPI 2Y ETF Price

Therefore, is JEPI a buy here? We think so, since it remains well supported at the March 2023 bottom of $52. The moderation in its prices has also triggered a nearly doubled dividend yield, compared to its November 2022 levels of 6.6%. Combined with the fact that it is trading well below its 50/ 100 day moving averages, we are rating the ETF as a Buy here.

Naturally, there are risks to this investment thesis, since past performance is not indicative of future results. This is particularly attributed to the JEPI ETF's nascent presence from May 2020, compared to its peers such as SCHD from October 2011, SDY from November 2005, QQQ from March 1999, and SPY from January 1993.

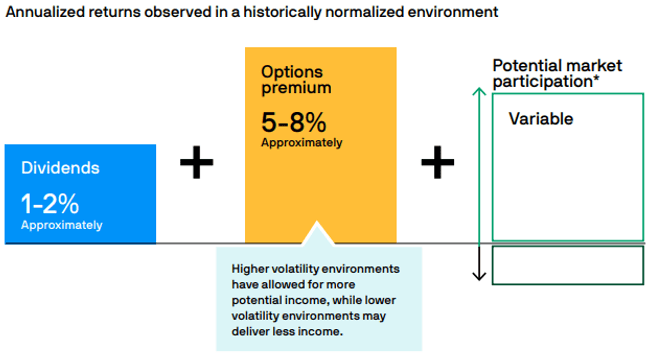

JEPI Dividend Guidance In Normalized Environment

While JEPI may have been delivering stellar dividend yields thus far, we reckon things may moderate moving forward, if/when the volatile, sideways market ends and a potential bull market starts. Based on the management commentary, the ETF is only designed to deliver annualized returns between 6% and 10%, on top of a variable factor, termed as “capital appreciation/depreciation less forgone upside.”

In addition, any distributions from the ETF is taxable, depending on the investors' income threshold/ tax bracket. Based on its SEC filing, long-term capital gains will be taxed at up to 20% federal income tax rate, with net short-term capital gain to be taxed as ordinary income, potentially triggering higher tax rates of up to 37%, based on the 2022 tax year.

Therefore, interested investors will need to perform their due diligence and risk management accordingly, due to the potentially lower yields after accounting for the higher taxes. We reckon it may be more prudent to include JEPI as part of a diversified income portfolio, along with SCHD, SDY, QQQ, and SPY, to balance long-term dividend income and portfolio growth.

Then again, we reckon that the ETF's moderated annual yield of between 4.8% and 8% (after deducting the 20% tax rate) or between 3.78% and 6.3% (after deducting the 37% tax rate) is still decent enough for interested investors, beating the Fed's target annual inflation rate of 2%. Not too bad, in our opinion.