Functionally, these ETFs pay you back your own capital and call it “Yield”. Income will shrink over time for long term investors as principal erodes as a result of the funds' flawed underlying mechanics. In reality, these funds don't offer much to investors in terms of portfolio construction efficiency. It's time to dump these funds in the trash and wait for better products from ETF companies that allow for more discretion in managers' decision making.

QYLD ETF: The Yield Is A Mirage (NASDAQ:QYLD)

Ahhhh, Global X NASDAQ 100 Covered Call ETF, NASDAQ:QYLD. Our old friend. At some point in everyone's investing career, it's hard not to become obsessed with this ETF, along with its cousins, Global X Russell 2000 Covered Call ETF, RYLD and Global X S&P 500 Covered Call ETF, XYLD. A 12% sustainable yield? Who could fault that. Downside protection in bearish and sideways markets? Sounds like a dream.

Unfortunately for the modern investing public, this tantalizing income is nothing but a mirage. Long term holders will see nothing but principal erosion due to the mechanics of these funds' main strategy, and thus we rate these ETFs a Strong Sell. They're a terrible choice for retirees or other income seekers, and they are mediocre hedging tools even in an ideal market environment.

This makes them a failure for both income seekers and those looking to use them as a tactical portfolio construction tool. For simplicity's sake, we'll explain our argument via QYLD, as it's the most well-known fund, although the exact same principles apply to all three.

A Terrible Choice for Income Seekers

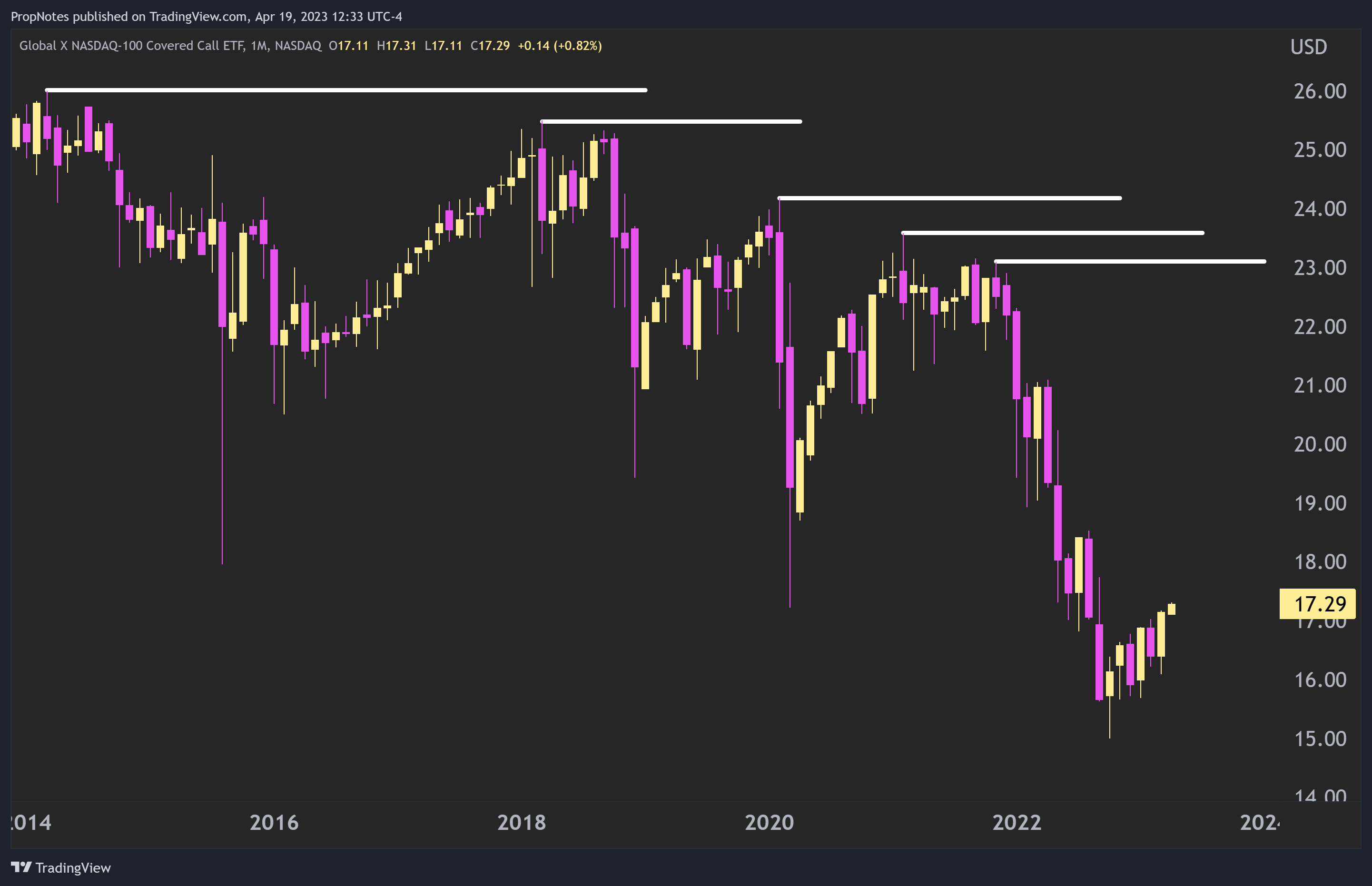

Let's start off with some basic facts. Since inception, the share price of QYLD has basically gone straight down.

In fact, since inception, it's dropped more than 32%, while the underlying asset, Invesco QQQ ETF, QQQ, has gained more than 261%. At this point, alarm bells should already be ringing in your head.

“Ah!”, you may exclaim. “But that's just the share price, have a look at total returns!”. Well, yes, that's true. Let's look at that.

If you add back in the income that QYLD pays out over time, it looks something like this:

Almost 80%! While it's certainly not the +293% in total returns that QQQ earned, it's definitely not negative. However, think about this argument.

If you're a retiree with a lot invested into QYLD, it's likely that you're not re-investing this income into the market. In fact, it's likely that it's already out the door, gone to pay for living expenses.

In that case, all you're left with is the shares you purchased, which are now worth less than you paid for them.

In other words, instead of seeing continued growth and income, an investor with a static position will see unrealized losses, and also declining income. Given that the yield has remained mostly steady around 12% since inception, as shares decline in price, the yield paid on them will decrease as well. Yield, in this case, is a function of the option strategy, which directly depends on investor principal to produce results.

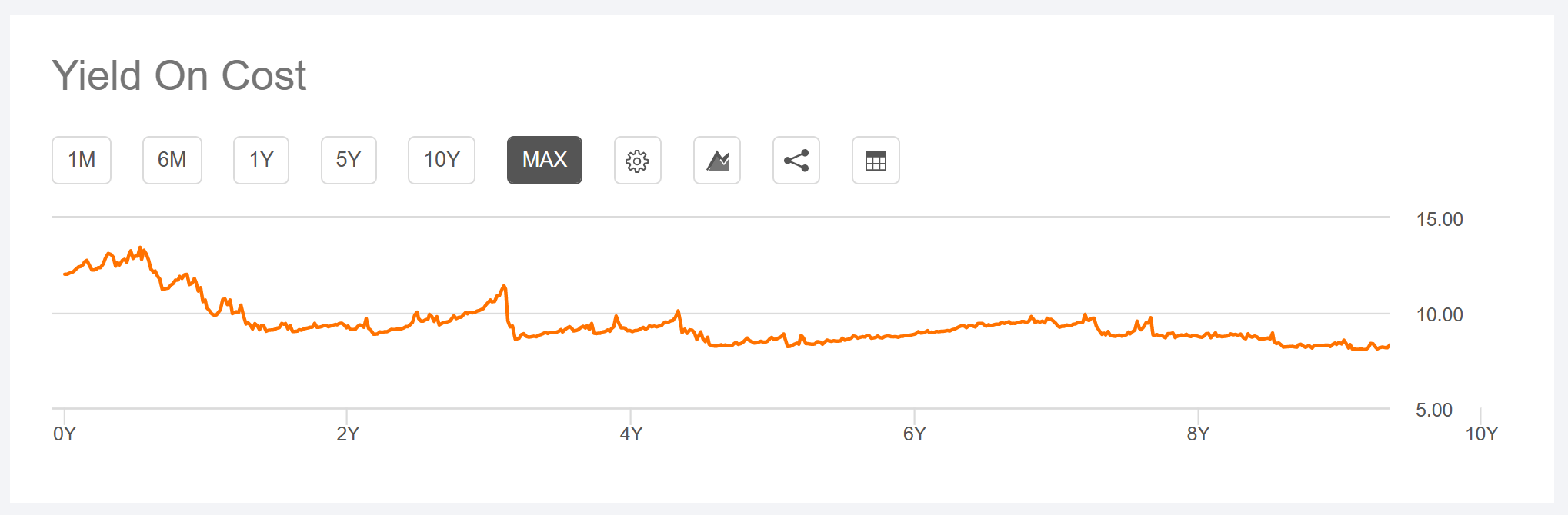

To see this in action, check out this yield on cost graph, which shows that investors in the ETF have seen their income drop by nearly 36% since inception – in almost a straight line.

Nominally, you can see this in the actual dividends paid out.

In 2018, QYLD averaged a 0.22c payout per share per month. In 2022, It averaged 0.18c per share per month. Income is slowly shrinking.

This is highly different to the income produced from dividends. For example, check out this Yield on Cost graph of Original Post>

While dividends come from the profits of growing, productive enterprise (at least in theory), QYLD yields come from churning the capital in a subpar strategy. More on this in a minute, but it's important to remember: not all yield is made equal.

In essence, Covered Call ETFs take your capital and pay it back to you in the form of “yield”.

“But wait!”, you may exclaim. “Covered Call ETFs actually have a robust income generation strategy that uses covered calls to generate yield on quality underlying stocks.”

Again, you're right. However, it's this very strategy, and its implementation, which is dooming these funds to permanent decay.

Here's why.

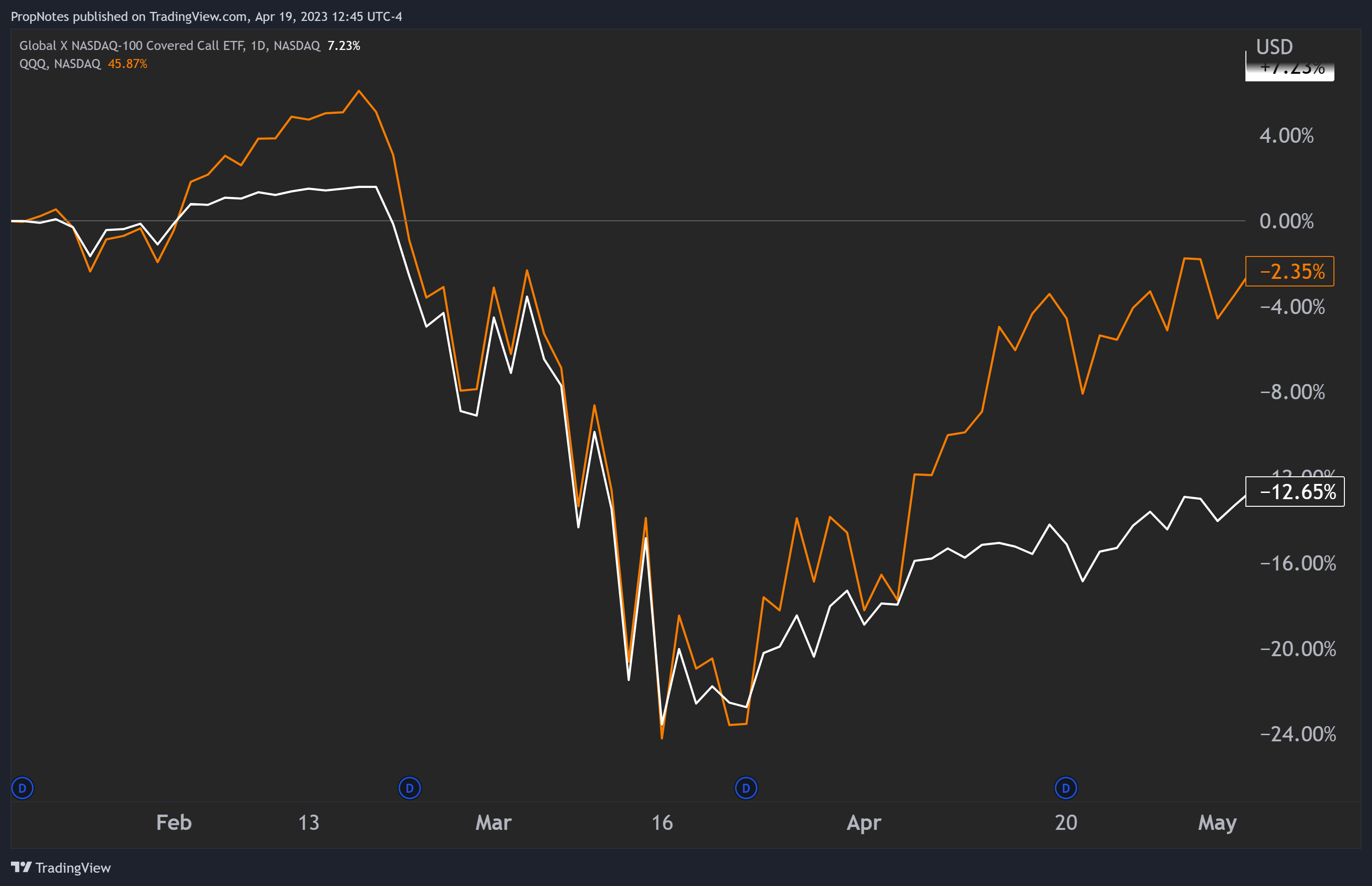

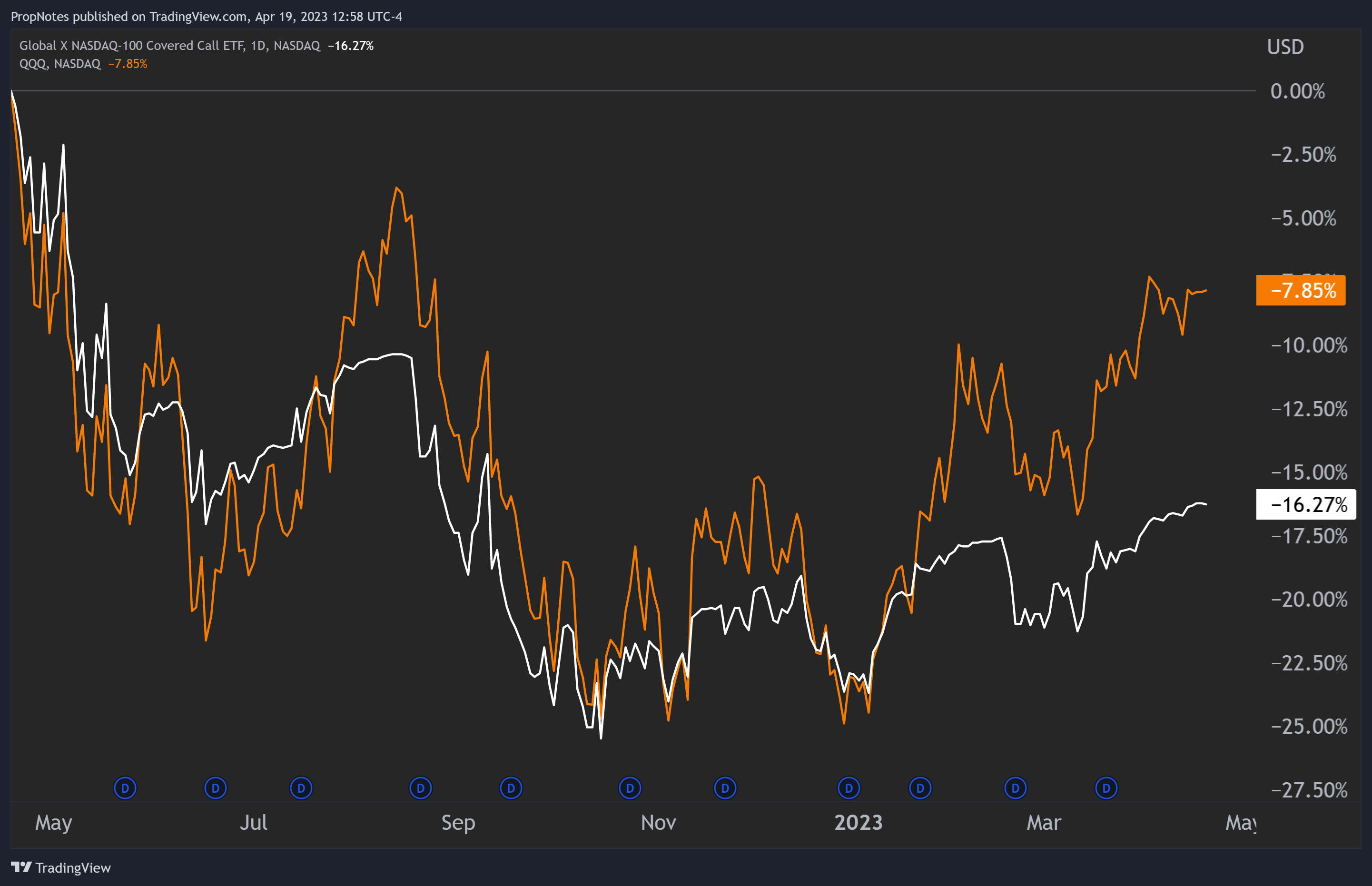

Take a look at this chart and you'll see it. See it right here?

In the orange, you'll see QQQ – the underlying asset – and its performance this year. It's had, broadly, 2 strong periods, with a weak period in March in the middle. As a result, it's up ~21% so far YTD.

However, QYLD has had two tepid periods of growth (circled), and the same weak period in March. Why?

When you see QYLD‘s price action getting all bunched up like that, it means that the underlying assets are desperately trying to go higher (and follow QQQ), but the options the fund has sold are counteracting this P/L, causing constriction. Theoretically, these options the fund sells should be providing solid yield, and they do.

However, what it means is that every time QQQ finishes an option expiration at a higher price than the strike QYLD sold, the functional cost basis of QYLD's underlying assets increases. Sometimes, by a lot. When it comes to investing, you want to be getting your cost basis lower, not higher.

Then, in the example above, the fund sells new options, and the underlying assets are open to participate in the downside, which is only slightly protected by the option credit.

On top of all of this, let's be real. In the case of QQQ, it goes up more often than not, which means that QYLD is constantly making its own assets more expensive so it can pay you the 12% yield you want.

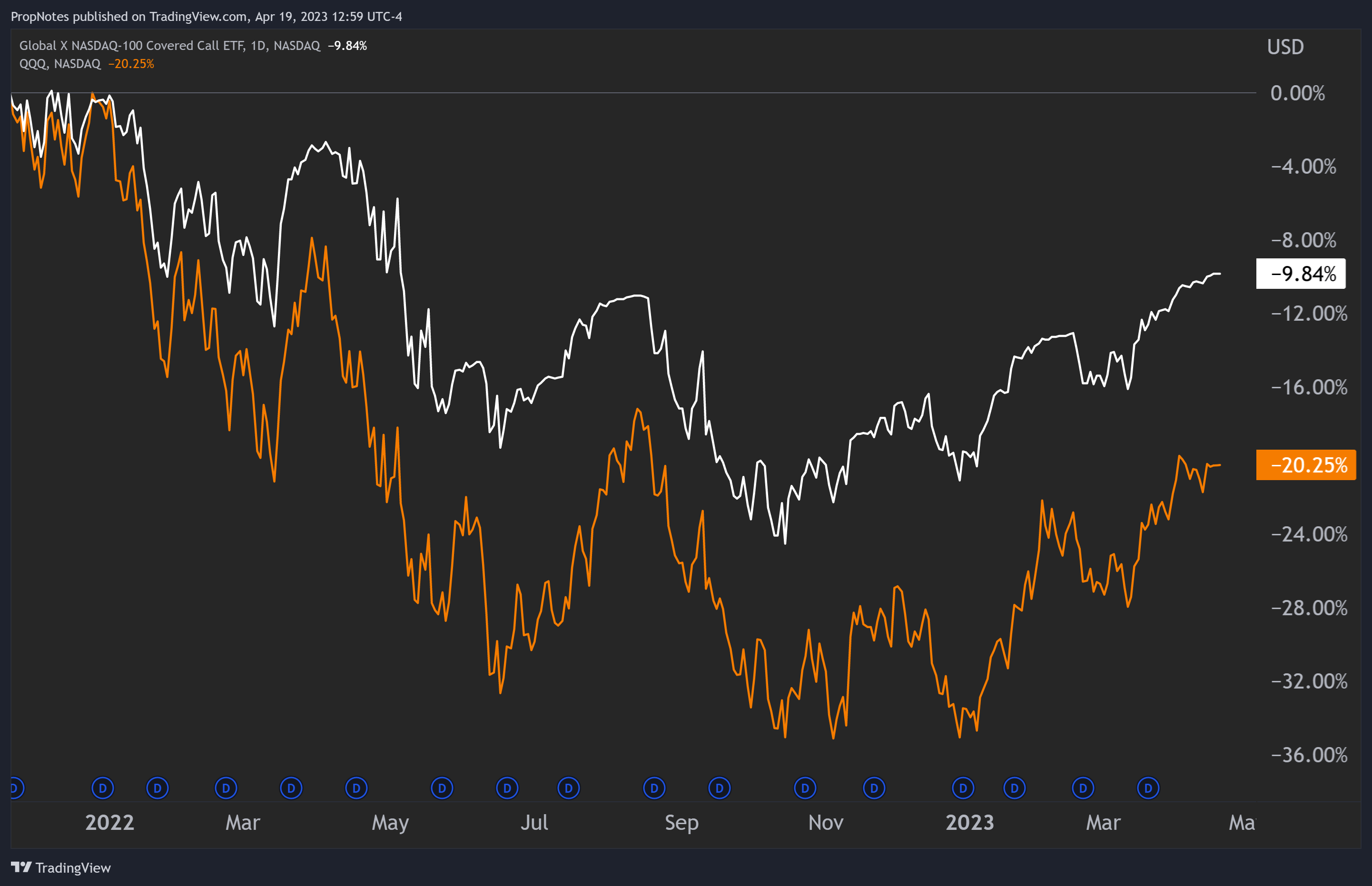

This is why QYLD can never make new highs:

So, while it's not literally paying back your capital to you in order to pay a yield, functionally, it might as well be. The strategy the fund uses to choose sold options is too mechanistic. They're using a hammer, while a scalpel would be far more effective.

It's unfortunate too, because a strategy similar to this with a little more discretion afforded to the manager might be able to produce some really fantastic returns.

A Subpar Choice for Portfolio Construction

“Alright”. You may say. “Fine. It's not a great option for long term investors. But it's still a good choice for people who want to reduce risk in a portfolio for a given period of time.”

To that, we also disagree. Here's a chart of QYLD during the pandemic selloff in 2020:

The option the fund was short expired in late Feb – just in time to allow the fund's assets to participate in the full drop. Then, at dead lows, the fund sold another covered call, which massively hampered investors from recovering with the rest of the market.

Ok. Maybe it's not good for crashes. What about the last year? It's been a choppy, volatile, sideways year. Surely QYLD would have outperformed?

Barely. While it's had a lower drawdown, this performance chart also assumes that the manager is doing something with the cash they're getting. If they just sit on it, or it goes out the door to pay for expenses, then QYLD is underperforming big time:

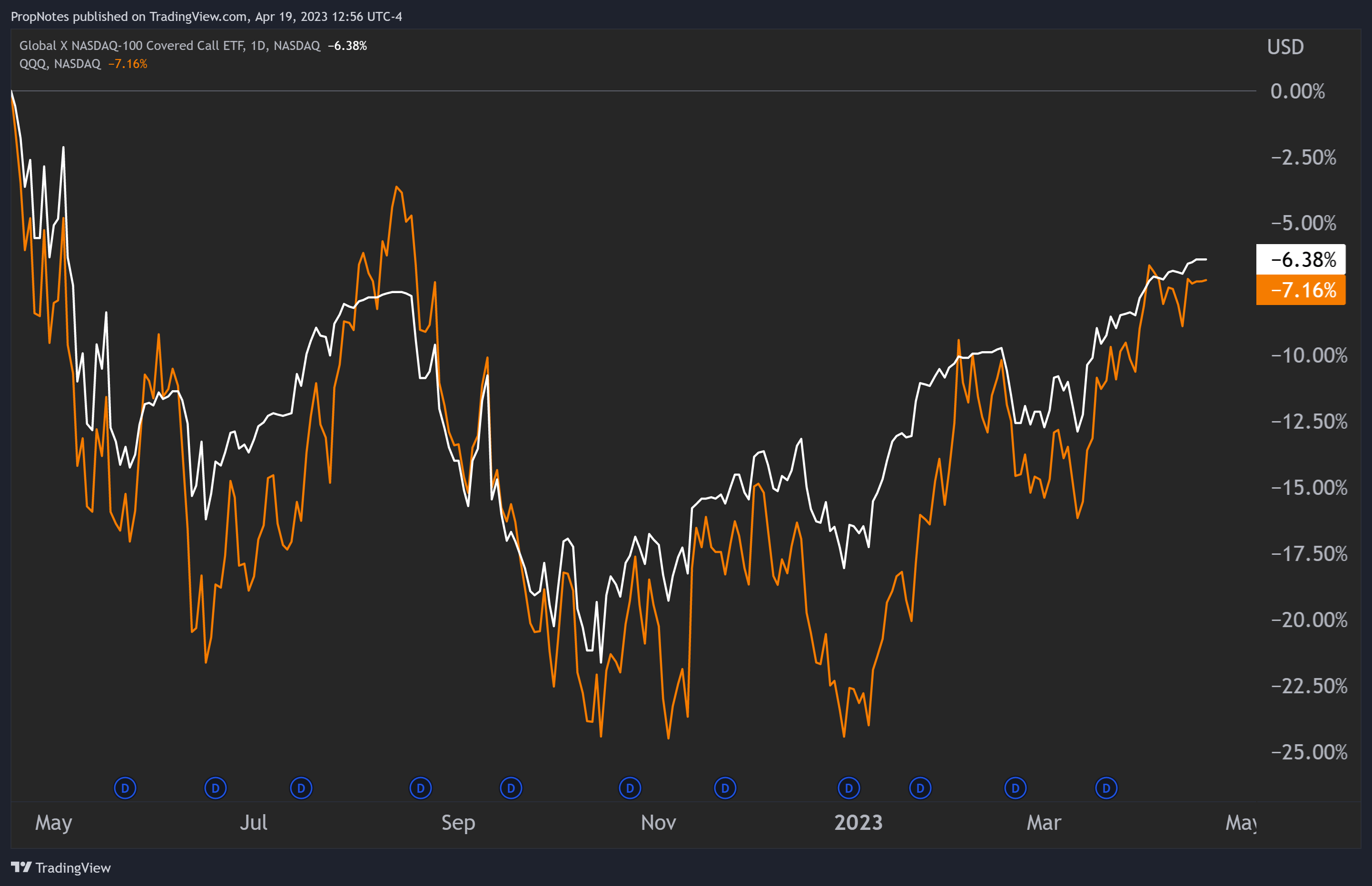

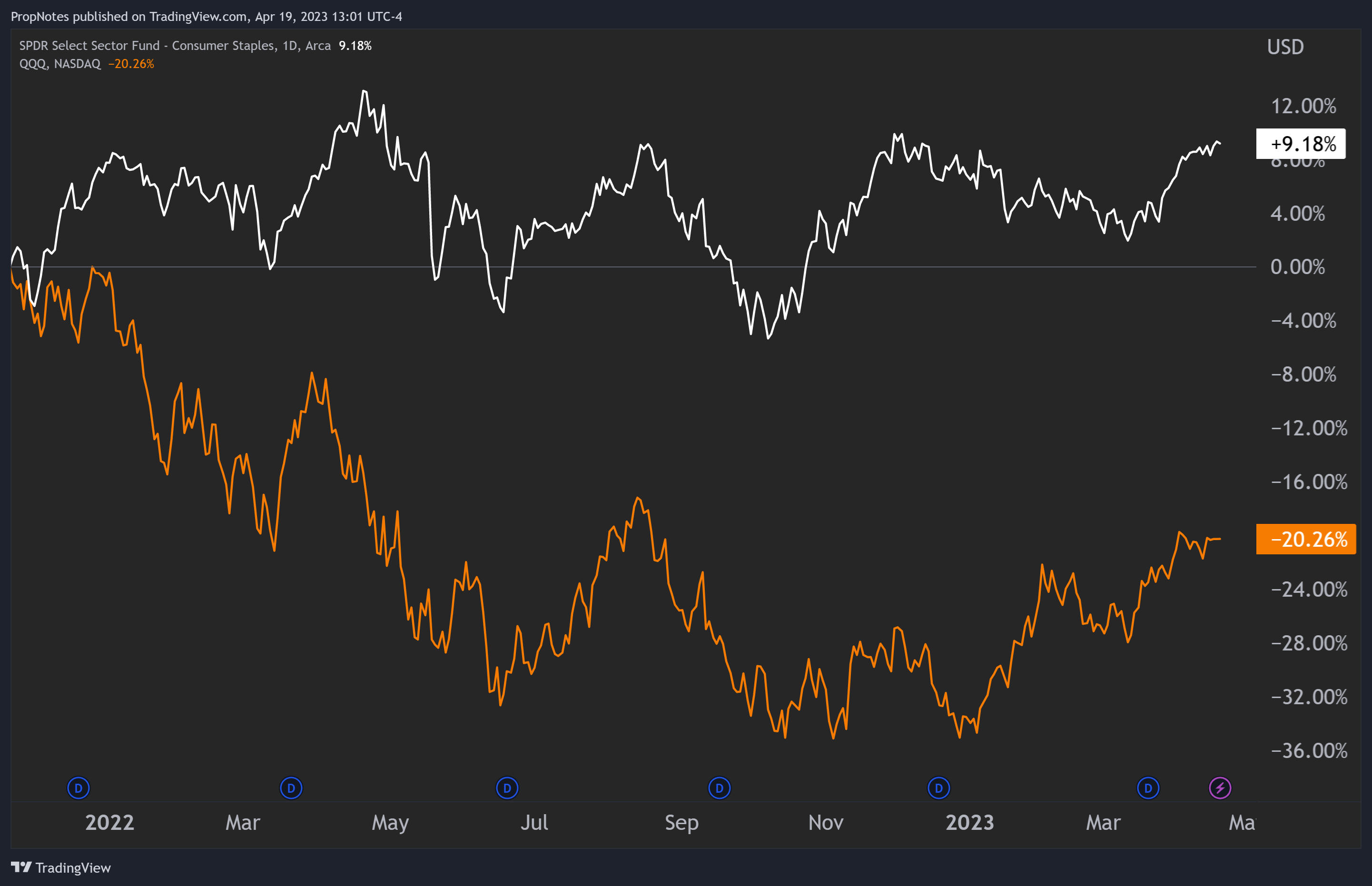

In fact, the only rolling period of time that QYLD has offered investors material outperformance above QQQ is the period between the top of the market in late 2021, through present day:

However, in our view, if you're good enough to rotate into this vehicle at just the right time, then you're probably good enough to rotate into something better. Perhaps Consumer Staples?

Anyway, we digress.

In Summary

Hopefully this was an understandably presented argument for why you, and we, collectively, should all move on from Covered Call ETFs. They present almost no material advantages from a portfolio construction or income perspective, but they come with loads of downsides.

Here at PropNotes, we love option income generation, and that's why a good chunk of our articles focus on selling options for yield. However, it has to be at the right time. If you're utilizing an options strategy with such an indiscriminate approach, it's hard to make it work.

Until next time!