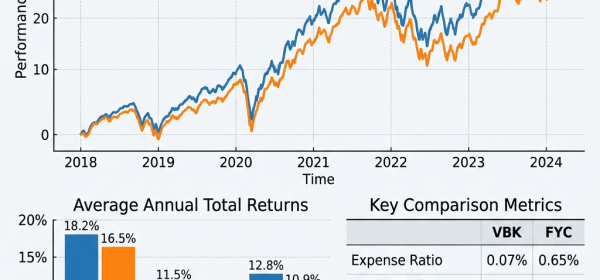

The Vanguard Small-Cap Growth Index Fund ETF (VBK) tracks the CRSP US Small Cap Growth Index, featuring 550 stocks and a low expense ratio of 0.05%. Launched in 2004, it emphasizes growth in industrials and technology. While competitive with peers since 2013, key competitor FYC may offer better long-term returns.