Predicting financial markets is tough, especially in the short term, but the behavioral habits of the average investor are remarkably consistent in reducing performance. Fortunately,

Predicting financial markets is tough, especially in the short term, but the behavioral habits of the average investor are remarkably consistent in reducing performance. Fortunately,

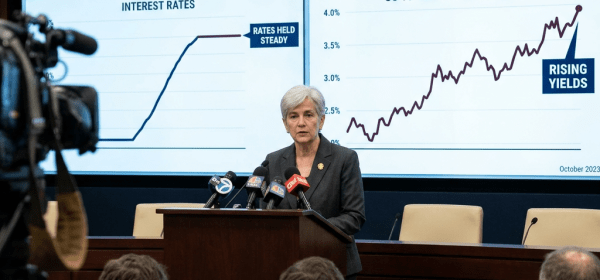

The Federal Reserve maintained its policy rate at 3.50% to 3.75%, emphasizing its commitment to inflation control. Chair Warsh aims to reshape monetary policy communication by eliminating forward guidance, encouraging markets to internalize uncertainty and adjust behavior. Rising Treasury yields reflect this strategy, indicating active market participation in restoring price stability.

Michael Burry’s critique of AI companies focuses on three main arguments: overstated earnings, circular financing, and revenue issues. While the first two present valid concerns, the claim regarding revenue not generating returns is flawed. Investors need to differentiate between cash flow risks and genuine revenue, with careful pricing considerations in the AI sector.

Microsoft reported impressive quarterly earnings, exceeding expectations with an EPS of $4.74 and $90 billion in revenue, primarily driven by Azure and Copilot growth. This strong performance positively influenced ETFs, especially large-cap and tech-focused funds, while maintaining stable capital expenditures amid pressures faced by competitors like Meta and Alphabet.

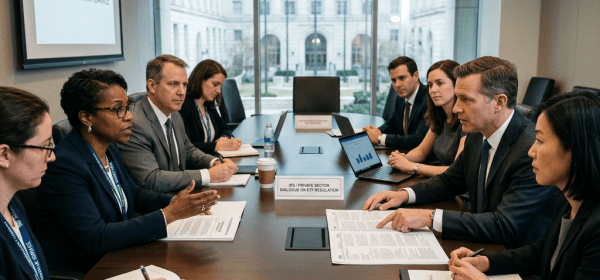

On July 21, 2026, IRS and Treasury officials met with tax professionals to discuss concerns about certain ETF transactions involving tax provisions like section 852(b)(6). While expressing interest in various strategies that seemed suspicious, officials did not endorse any specific transactions. They sought input from the investment community for future regulatory guidance.

The equity bull market is projected to persist through the latter part of 2026, driven by resilient U.S. growth and AI investments. While inflation remains a concern, the Fed is expected to maintain its current policy stance. U.S. small caps present attractive opportunities due to favorable valuations and potential recovery.

The rise of AI in financial advice presents challenges and opportunities for advisors. While many Millennials and Gen Z investors utilize AI tools, the advice can often be unreliable. Financial advisors must embrace AI by guiding clients, developing tools, and maintaining the human touch to navigate a future where AI plays a significant role.

Artificial intelligence is transforming financial education for retail traders by simplifying complex concepts and organizing vast data sets. AI tools enhance learning, enabling users to understand various asset classes and market sentiments more effectively. However, human judgment remains crucial for interpreting AI-generated insights, emphasizing the importance of continuous education and thorough research.

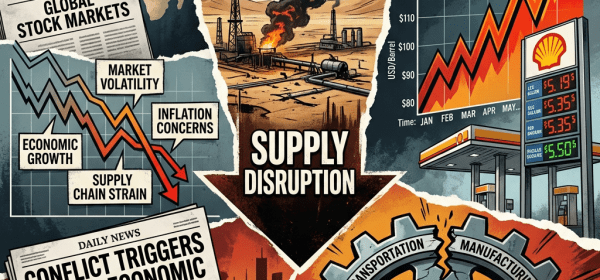

The oil market’s recent calm has been disrupted by renewed U.S. military actions against Iran and concerns over a collapsing peace deal. Traders may explore the Direxion ETFs—ERX for bullish positions and ERY for bearish—amid potential supply constraints and geopolitical tensions affecting global oil prices and energy stocks in the near term.

This year, concerns over AI disruption in the software industry have led to increased redemption requests from private funds, causing many to limit withdrawals for liquidity. However, analysis suggests that realized losses in private credit remain low, offering potential investment opportunities in high-quality lenders despite market sentiment that may be overreacting.

Michael Burry, known for his successful bet against the housing bubble, may not acknowledge the “Burry effect,” where his investment moves influence market trends. As he shorts high-flying stocks like Micron and Nvidia, analysts suggest his actions may provoke sell-offs. If successful, his influence could strengthen over time.

The June FOMC statement marked a shift from forward guidance under Chair Warsh, reducing word count and indicating less information from the Fed. This hawkish hold suggests a potential rate hike by year-end, impacting market volatility. As expectations shift, the Fed’s minimized communication challenges investors to navigate an evolving landscape.

Kevin Warsh, the new Fed Chair, emphasizes a serious commitment to achieving a 2% inflation target, prioritizing credibility and independence. His leadership signals a shift towards innovation and accountability within the Federal Reserve, aiming for adaptability in rapidly changing economic conditions. Long-term strategies remain intact, anticipating the Fed’s evolving role.

The Middle East conflict’s duration and impact on oil prices are uncertain, affecting consumer purchasing power, particularly for lower-income households. While higher energy prices won’t likely trigger a U.S. recession due to reduced energy spending, labor market constraints are affecting job growth. Investment strategies remain focused on U.S. equities amid the economic landscape’s resilience.