What Does AI Look Like?

There is a big difference between “mentioning” and “implementing” AI initiatives, but let’s look at what AI means across paradigms:

1. AI is integrated into existing software. Virtual meeting tools like Microsoft Teams and Zoom improved transcription, summaries and even action points of meetings. Cybersecurity is another important area, with more and different types of attacks and not enough employees to fill necessary cybersecurity positions.

2. New AI modules are options users can pay for. Microsoft allowed users of Office 365 to pay more and access a version of Copilot directly on its platform. Google Workspace is also vying for users in these productivity enhancers.

3. New tools: ChatGPT was a “new tool,” spawning a lot of additional applications that can take a prompt and create text to “fulfill” said prompt. The same principle was applied to create videos and pictures. Maybe it will become normal for future slide presentations to be given fully by AI—meaning systems create the slides, and the system is also able to narrate the text to draw out the stories. We are transitioning from feeling like “This is cool” to “Can this tech really add value?” As investors, we have to look at increasing revenues, and then cash flows and, ultimately, earnings.

Cloud Software Companies Have Not Participated in 2023’s AI Rally

So far, 2023 has been defined by such stocks as the “Magnificent 7” and Nvidia.

Many of these AI applications require cloud-based computing platforms and services. However, emerging cloud software companies have not participated like the Magnificent 7 in the AI boom of 2023.

• The Nasdaq 100 Index, with its massive weight in the Magnificent 7, has defined 2023 as strongly delivering equity market returns, but there are a number of ways to invest in the growing tech space.

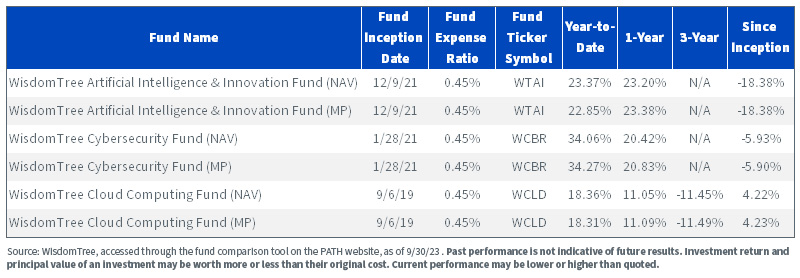

• WisdomTree has the WisdomTree Cybersecurity Fund (WCBR), the WisdomTree Cloud Computing Fund (WCLD) and the WisdomTree Artificial Intelligence and Innovation Fund (WTAI). WCBR and WCLD are largely software-focused, whereas WTAI represents a mix.

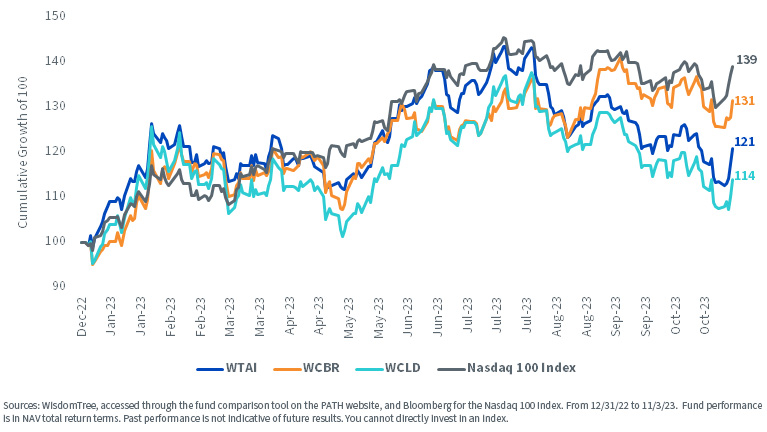

• WCBR has rallied of late. Whenever there is a new technology—this year, generative AI—we believe it is important to also think about how to secure it.

• WCLD has been the relative laggard. Many asked if they “missed” 2023’s AI rally. If our thesis is correct—that many users of AI will use it through cloud software—maybe this portends a reaction in WCLD’s returns as we look forward.

Figure 1a: Standardized Performance

For current holdings, 30-day SEC yield, SEC standardized return and most recent month-end performance, click the respective ticker: WTAI, WCBR, WCLD.

Figure 1b: Emerging Cloud Companies Largely Lagged in 2023

For 30-day SEC yield, SEC standardized return and most recent month-end performance, click the respective ticker: WTAI, WCBR, WCLD.

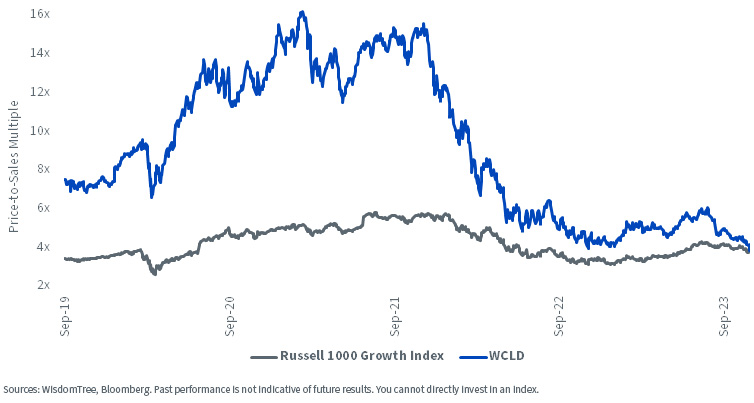

WCLD Dropped below the Russell 1000 Growth Index on a Valuation Basis

Most investors who speak to us never forget about the fundamentals—and WisdomTree’s foundation was built on looking at such fundamentals as dividends and earnings.

However, when we shift the focus to WCLD and the underlying companies defined by the BVP Nasdaq Emerging Cloud Index, it’s clear that those waiting for an “inexpensive valuation” might be sitting on the sidelines for quite a long time. It’s possible that “emerging cloud software” companies never look inexpensive by traditional measures, given their above-average growth rates over the coming years.

At least based on what we have seen since 2021, emerging cloud software stocks like those in WCLD have been very interest rate sensitive. When we see the U.S. 10-Year Treasury note interest rate going up, we tend to see valuations dropping…and performance doing the same. Similarly, when rates fall, performance picks up.

In figure 2a, maybe due to the recent rise in the U.S. 10-Year Treasury note interest rate, we see something new over the live history of WCLD since its inception.

• Usually, the emerging companies within WCLD are defined by their “potential,” and at times, that potential doesn’t yet have positive earnings behind it. When companies are defined by potential, it tends to push up valuations.

• But rising rates have pushed down the multiples.

• WCLD’s price-to-sales multiple actually dropped below that of the Russell 1000 Growth Index for the first time.

Figure 2a: Valuation Opportunity?

Remember the Seesaw: Valuation AND Growth, Not Just Valuation

In our view the true question is actually not whether the companies represented within WCLD are expensive or inexpensive but rather whether those companies are exhibiting strong enough growth to justify their valuations. When we see the higher valuations in figure 2a, investors were pushing those prices up because the demand for software during the height of the pandemic was extremely high.

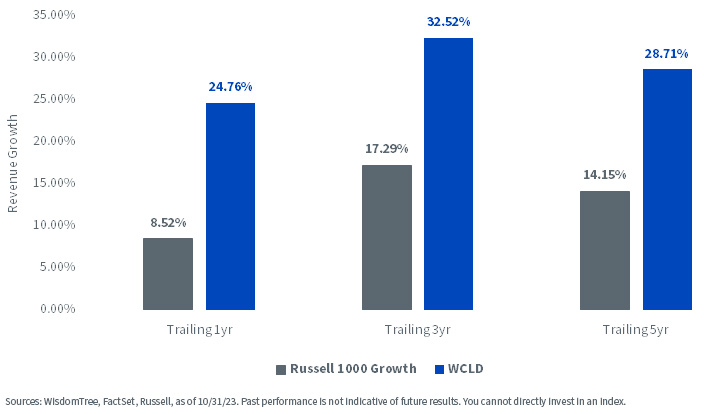

In figure 2b, we show the historical revenue growth as well as the future revenue growth expectations. As with any estimates or expectations, there are never any guarantees, but one thing we are excited about is that the companies within WCLD are continuing to exhibit faster growth than that of the Russell 1000 Growth Index.

Another big picture point to have in mind—the majority of the companies in WCLD are Software-as-a-Service (SaaS) companies, and the customer is choosing to, after due diligence, subscribe to the software to solve a particular business need. In today’s world, these software packages tend to be more associated with efficiency gains than spending more overall. While nothing is “recession-proof,” you might, therefore, say that these subscriptions would rarely be the first things cut in a period of stress.

Figure 2b: The Revenue Growth Side of the Ledger

Conclusion: Did Cloud Computing Companies Become More Interesting in 2023?

While we can never know future performance with certainty, we do know two things about the stocks represented within WCLD as a result of 2023’s experience.

1. Valuations have come down further over the course of the year, even amidst some volatility.

2. AI represents a possible catalyst to get more users in that if the cloud computing software companies can offer AI solutions, it might increase the overall adoption and get companies spending more because they believe there are possibly greater benefits to be had.

We’d also note—most companies will probably never buy an Nvidia H100 (or similar) AI-accelerating chip, but they are likely to select and subscribe to software. We believe Cloud computing represents a very favorable model of software delivery, where companies can pay almost feature by feature and operation by operation in certain cases. AI might lead to more subscriptions over time.

Important Risks Related to this Article

For current Fund holdings, please click the respective ticker: WTAI, WCBR, WCLD. Holdings are subject to risk and change.

There are risks associated with investing, including the possible loss of principal.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.