ASML (NASDAQ:ASML) reported a continuation of the cycle downturn for q1’24 with anticipation of a continued decline into eq2’24 before realizing an upswing in the back half of the year. As the semiconductor manufacturing industry shifts production to more advanced chip nodes, transitioning to EUV is highly anticipated to cater to the demand. With both Intel (INTC) and Taiwan Semiconductor (TSM) receiving financing through the CHIPS Act to build new advanced node chip foundries in the US, I expect significant investments to flow through to ASML for their advanced high NA machines. I provide ASML shares a BUY recommendation with a price target of $1,134/share at 32.49x EV/EBITDA.

Operations

ASML reported a continued cyclical decline in topline growth in q1’24 with strong guidance going into the back half of FY24 through FY25. The driving factor behind ASML’s growth strategy revolves around the adoption of EUV technology for manufacturing advanced chip nodes. I anticipate that both Intel and Taiwan Semiconductor will be two of the customers falling in this category as they seek to expand their advanced chip manufacturing capacity, especially with their domestic foundries that are in development with financial assistance through the CHIPS Act. Patrick Gelsinger, CEO of Intel, dubbed the next era of chip manufacturing “post-EUV” for advanced chip manufacturing. Considering that Intel has plans to focus their domestic efforts on their series of advanced nodes, such as the 20A, 18A, and Intel 7, I anticipate the firm to be a primary customer for ASML as they develop their US-based foundries and upgrade older foundries. Management had voiced their plan in rolling out the next generation of semiconductors in their five nodes in four years plan and anticipates utilizing EUV in bringing 18A to market. The same can be said with TSM in manufacturing their N7+ node using EUV. It is clear that Intel has some catching up to do with TSM when it comes to utilizing EUV technology for manufacturing advanced nodes. Given Intel’s roadmap for semiconductor development, I anticipate the firm to be one of the major purchasers in early 2025 as they ramp up production of 20A and begin the post-development production stages of 18A. I believe this will be a driving factor for Intel in upgrading their equipment to compete with TSM for business as well as chip designers for AI processing.

Though I do not anticipate non-EUV chips to slow down in production and utilization, management at ASML expects non-EUV business to be down in 2024, driven by lower emerging system sales when compared to 2023. In their q1’24 earnings call, management outlined that mature nodes will be an important factor for the next generation of industrialization and electrification. They anticipate more semiconductors to be utilized in power transmission and power generation as more renewable resources create larger baseloads on the grid. This is something that has been discussed for a few years now as intermittent energy sources do pose a major problem for power generation. In short, the grid was designed for constant flow of power generation and the addition of intermittent power sources may cause stress and/or disruption. For energy transmission, base stations will need to become more sophisticated in transitioning from one fuel to the next with minimal downtime; i.e. once solar or wind stop production for a period of time, natural gas or coal must pick up to keep the power generation at a constant. This will require more advanced systems, more semiconductors, and potentially more advanced semiconductors for data processing. This challenge will only be exasperated as AI applications become more heavily utilized. Pairing energy transmission with GenAI adoption, the IEA suggested that the typical Google search uses 0.3 watt-hours of electricity vs. 2.9 watt-hours for ChatGPT requests.

With this in consideration, there are also a host of new data centers sprouting up to cater to the heightened demand for AI-enabled applications. For example, Oracle Corp. (ORCL), is planning to invest $10b in eFY25 for building and expanding their regional data center footprint to cater to this growing demand. This should drive growth for storage and logic chips and, in turn, drive up demand for manufacturing equipment. I anticipate both data center and energy transmission to drive significant growth across mature and next-generation chips that will cater to ASML’s longer-term sales target in the range of EUR44b-60b for 2030.

Management remarked in their q1’24 earnings call that their low NA EUV tools will be driving much of the growth in the back half of 2024 while transitioning to high NA EUV, such as the NXE:3800E in 2025. Given that this more advanced machine has the capabilities of increasing production by 37% to 220 wafers per hour, I expect this product will be well received as chip manufacturers face capacity challenges and race to attain a competitive edge.

Corporate Reports

Looking ahead to financials, I anticipate tailwinds to begin forming in the back half of eFY24 while accelerating into eFY25 as new domestic chip foundries begin building out their equipment needs and as existing fabs upgrade their equipment to the latest EUV technology. As discerned in my report covering Nvidia (NVDA), Taiwan Semiconductor is addressing the capacity challenges and anticipates resolution by the end of CY24 with doubled CoWoS capacity. In addition to this, Intel is pressing down on the gas to build out foundry capacity for both internal and contract chip manufacturing as the firm seeks to compete on the same scale as Taiwan Semiconductor. Though I do not anticipate the firm to reach scale as soon as management has addressed, as denoted in my above-mentioned report covering the ticker, I do anticipate the firm to make the investments in building out their foundry network to more effectively compete with Nvidia on advanced nodes designs. Management anticipates strong margin expansion going into eFY25, with gross margins expanding from 51% in FY22 & FY23 to 54-56%. This would mark a major step up in financial performance for the firm and has the ability to lead to significantly higher cash flow generation. Given the firm’s rollout of their low NA EUV machines, I believe that they will be able to achieve these margins as these more sophisticated machines can deem higher margins as a result of the additional value-add for the customers.

Management mentioned that operating cash flow may continue to remain suppressed for another quarter as they build up inventory in anticipation of the rollout of their next-generation machines. I anticipate inventory levels to be resolved as the firm exits eFY24 paired with strong sales generation as a result of upgrades and new deployments. This should be a major turning point for ASML’s free cash flow generation and may lead to stronger shareholder returns.

Lastly, ASML is in talks with the Dutch government in taking steps to grow future operations in the region. The city of Eindhoven signed a letter of intent to spend $2.7b for infrastructure improvements to maintain their strong relationship with ASML and house 20,000 employees. I believe that ASML focusing on their employees both in and outside of work goes to show that the firm values its staff and doesn’t just see them as a number.

Valuation & Shareholder Value

Corporate Reports

For valuation purposes, all figures are converted to USD unless otherwise stated.

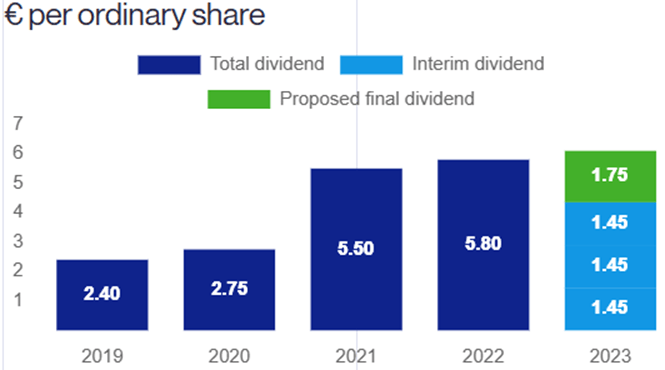

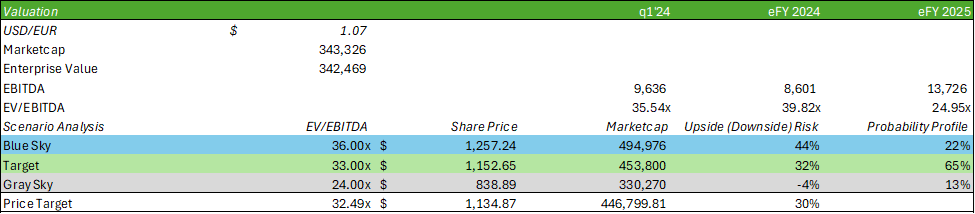

ASML currently trades at a rich premium of 35.54x EV/EBITDA on a trailing basis, suggesting that the firm may be near the bottom of the cycle. I anticipate ASML shares to trade into the midcycle going into the end of eFY24 and gain strength in eFY25 as the firm rolls out their high NA technology. ASML pays out a quarterly dividend that equated to EUR6.10/share in CY23 and regularly increases their dividend rate.

Corporate Reports

Despite the high valuation, I expect this to normalize as we navigate through the cycle, making the current valuation more appealing as a point of entry. Based on my multi-scenario analysis, I provide ASML shares with a BUY recommendation and value the shares at $1,134/share at 32.49x eFY25 EV/EBITDA. A blue-sky scenario would be the result of stronger than anticipated margin expansion and a pull-forward effect in EUV sales. A gray-sky scenario would be the result of further macro challenges and delays in EUV upgrades and deployments.

Corporate Reports

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.