The US economy is expected to enter the recession in Q2 2023.The S&P 500 is still overvalued, and earnings expectations don’t yet reflect an imminent recession. Thus, there is a considerable downside to SPY.

S&P 500: The Recession Expected To Start Next Week (NYSEARCA:SPY)

The Phase 2 recessionary selloff approaching

I separate the full bear market into the three phases:

- Phase 1 is the Fed-induced Liquidity selloff. During this Phase 1, the Fed tightens the monetary policy, which bursts the asset price bubbles and causes the contraction in PE multiple. The 2022 selloff was the Fed-induced Liquidity selloff, which caused the contraction of S&P 500 PE ratio from 35 to 18, and busted the bubbles in cryptocurrencies, meme stocks, tech, and other speculative bets.

- Phase 2 is the Recessionary selloff. The Fed’s tightening policy usually causes a recession, during which corporate earnings decline, and the PE ratio further contracts. We are about the enter this stage, as I will explain in this article.

- Phase 3 is the major Credit Crunch caused by the deeper and longer recessions, during which the credit spreads spike, as the overleveraged corporate/consumer/government sectors default on loans, hedge funds collapse due to margin calls, and the counterparty risk freezes the credit markets. Not all recessions end with the credit crunch, and it’s too early to predict whether the current cycle will produce the major credit crunch.

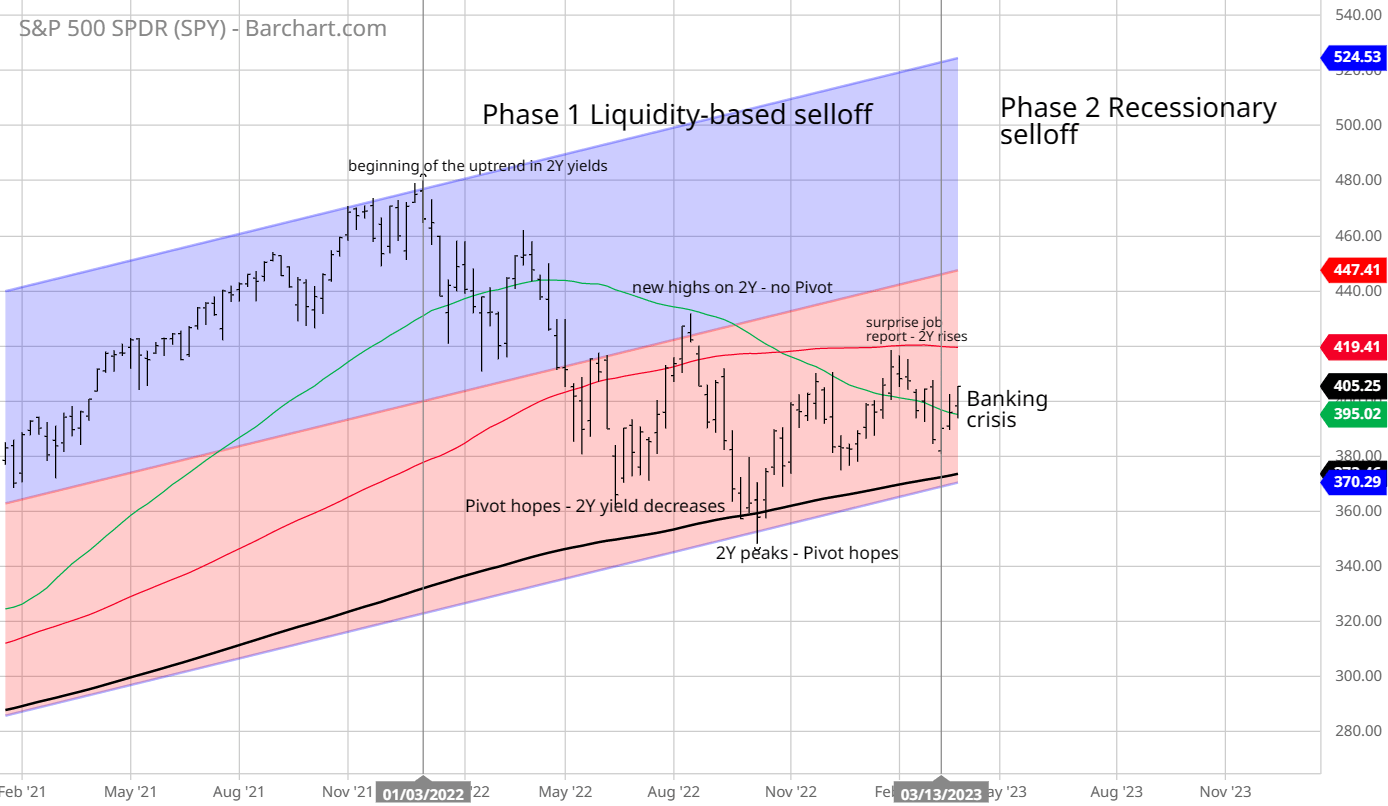

This is the chart for the ETF that tracks the S&P 500 (NYSEARCA:SPY). The Liquidity based selloff started with the rise in 2Y yields in January 2O22 due to expectations of monetary policy tightening. There have been two major bear market rallies based on the expectations of the “Fed pivot”. The Banking Crisis in March of 2023 is the turning point, which transitions the Liquidity Selloff into the Recessionary selloff – as it acts as the catalyst for recession due to the resulting credit tightness.

When is the recession coming?

People always ask me for the timing: when is the recession coming, and how long will it last? I don’t try to predict the actual timing, but I react as the preliminary signals emerge. I also closely monitor the opinions and research of Wall Street analysts, just to make sure my opinion is not as contrarian, even though I do tend to see things before the others. So, this is the sample of what appears to be the consensus on Wall Street at this point:

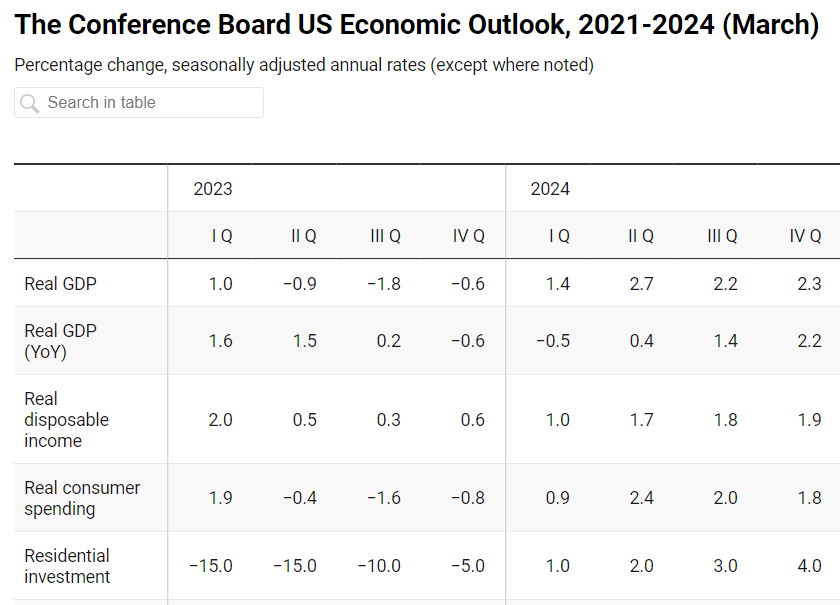

The Conference Board sees the recession starting in Q2 of 2023, and last for three quarters, until Q1 2024. Here is the quote and the recent forecast:

US GDP growth defied expectations in late 2022 and early 2023 data has shown unexpected strength. The US economy, and especially the US consumer, has resisted the duel headwinds of high inflation and rising interest rates. Because of this, we are increasing our Q1 2023 forecast to 1 percent. However, we continue to forecast that the US economy will slip into recession in 2023 and expect GDP growth to contract for three consecutive quarters starting in Q2 2023. These changes to the quarterly forecast result in an upgrade to our annual forecast for 2023 and a downgrade to our annual forecast for 2024.

ING agrees, they also see the US recession in Q2 2023 and lasting for three quarters:

Blackrock weekly commentary as of March 27th, 2023 not only sees the recession forthcoming, but also sees the Fed keeping the monetary policy tight during the recession:

Markets have been quick to price in rate cuts as a result of the banking sector turmoil and the Fed signaling a coming pause. We don’t see rate cuts this year – that’s the old playbook when central banks would rush to rescue the economy as recession hit. Now they’re causing the recession to fight sticky inflation – and that makes rate cuts unlikely, in our view. Stocks have held up due to hopes for rates cuts that we don’t see coming.

This is a sample, but it represents the Wall Street consensus, the US economy is likely to be in a recession, possibly in Q2 2023 – that’s next week. Also, Wall Street seems to agree with the Fed, there will be no rate cuts this year, despite the recession.

Implications for S&P 500

S&P 500 is exiting the Fed-induced Liquidity selloff with still overvalued forward PE ratio at 18. More importantly, the earnings for S&P 500 have not been revised lower by bottom-up analysts. Thus, not only we can expect the selloff due to the expected downside revisions of corporate earnings, but also the selloff due to further contraction of the PE ratio down to the 15 level. Thus, there is a considerable downside to S&P 500.

The chart above shows that SPY has been stuck in the range which corresponds to about 3700-4200 on S&P 500 (SP500).

The October bottom was due to the expected Fed pivot – before the recession arrives, which I considered as a possible scenario, but at this point this is extremely unlikely due to (at this point really) an imminent recession.

SPY is up around 5.5% YTD in 2023, but the gains are unproportionally driven by the big tech stocks in Communications (XLC), Discretionary (XLY) and Technology (XLK) sectors. This could be due to the specific AI theme, also due to lower interest rates since October, but I think it’s mostly a bear-market bounce from the deep selloff in 2022 and driven by short-covering and retail investor inflows.

In fact, Goldman Sachs states in the March issue of Market Pulse that the stock market performance this year is driven by short-covering:

MOMENTUM: This year’s rally has been driven by short covering, fueling a liquidity comeback. We anticipate momentum and technical factors to further elevate market volatility. In this environment, we believe managed futures may be able to exploit such opportunities.

What’s next?

The near-term recession will have to be confirmed with the data. Wall Street does not expect a sharp increase in the unemployment rate, but we do have to see some weakness in the weekly initial unemployment claims.

More importantly, the earnings season will have to support the expected decline in earnings via downgrades in earnings guidance from the cyclical companies, and especially the banks, which have to confirm the expected credit tightness.

Longer term, all recessions end with the policy support: monetary and fiscal. This time, however, the monetary policy support is limited by sticky inflation, which I expect to remain above the 2% target due to the unfolding trend of de-globalization. Further, the political divide in the US political sphere will make it very difficult to pass any effective policy support – especially before the 2024 election. In my view, this increases the probability of a much deeper and longer recession.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.