Investment Thesis

Baidu (NASDAQ:BIDU) is a Chinese internet and technology firm. BIDU has market leadership in China for search engines, with a market share representing some 700 million monthly active users – close to 80% market share. Not only a domineering position for the Chinese internet but represents a family of over a dozen applications and companies across sectors. Infrastructure as a service, self-driving, AI research, and advertising.

BIDU holds an effective government-enforced monopoly for search. As China’s premiere face of technological innovation, Baidu benefits from policies promoting domestic innovation and technological advancements. Additionally, the growth of China’s middle class is set to hit 700 million people in FY23 and is driving growing usage of internet services have created a favorable environment for spending and Chinese economic growth.

Due to the nature of the Chinese economy, BIDU is the AI and search company. It represents the core of the Chinese internet behind the “great firewall”. There are obvious risks for investing in Chinese equities through a VIE (which we will discuss in depth in the risks section), but if you want exposure to one of the fastest-growing information economies in the world, BIDU is an excellent choice.

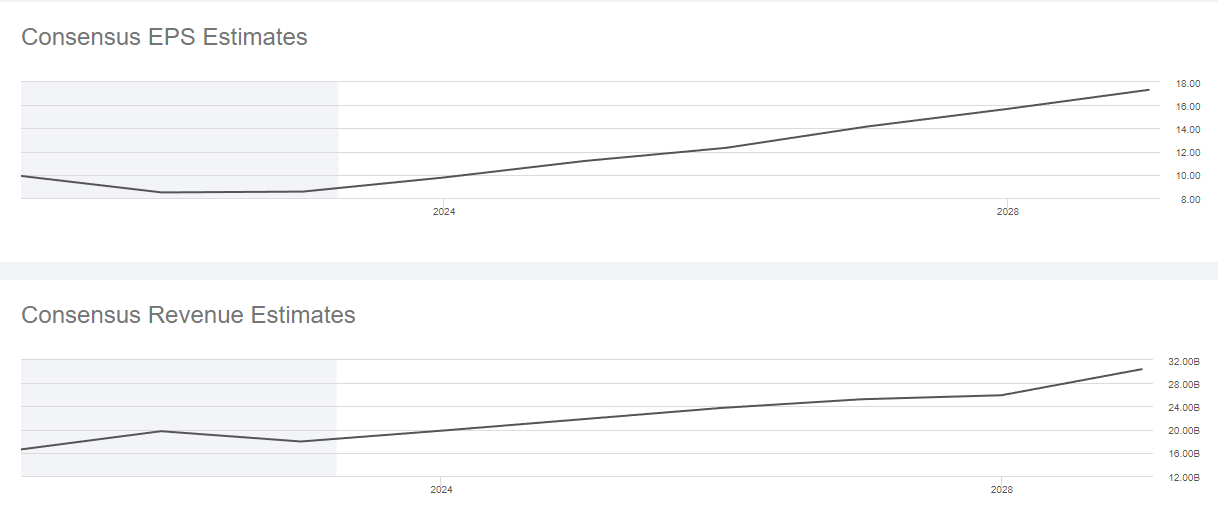

Estimated Fair Value

EFV (Estimated Fair Value) = E24 EPS (Earnings Per Share) times PE (Price/EPS)

EFV = E24 EPS X P/E = $10.80 X 19.2 = $207.36

We have erred near the consensus for FY24 EPS. We put our P/E higher due to BIDU’s dominant position domestically, and government-supported position.

SeekingAlpha

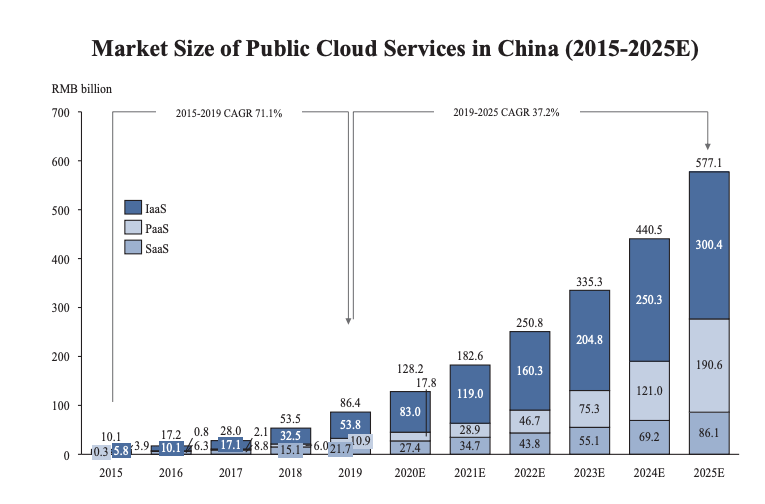

AI Cloud

While AWS and Azure dominate globally, Chinese firms expressed a 70% preference for Chinese-owned providers. While the dynamics of this industry are still developing, BIDU’s AI cloud revenue has grown 18% year over year in FY22. AI cloud offers the standard set of IaaS, SaaS, and PaaS (infrastructure, platform, software as a service) one would expect from a cloud company. In 2021, Baidu’s AI Cloud was the 4th largest in China and increased its market share by 55%.

BIDU, CIC

Chinese internet infrastructure for companies is still largely dominated by traditional internal server architecture, with the SaaS market remaining tiny at just $5.2 billion For reference, the US market for SaaS is over $120 billion. Internal server architecture is extremely limited in how quickly it can expand. The market for offloading cloud workloads to external providers is growing. The total addressable market for cloud service providers is expected to grow to $30 – $70 billion per year by 2025 with public cloud accounting for 45% of this addressable market and 55% being private cloud.

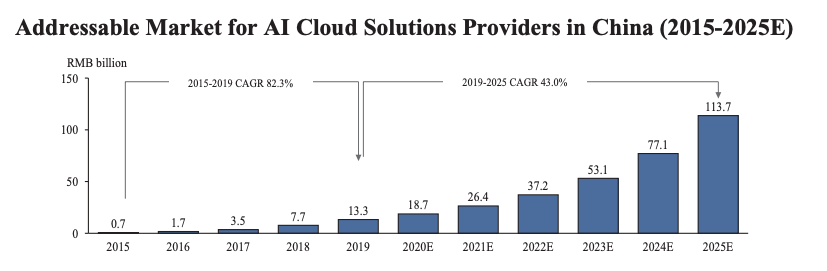

With ChatGPT dominating headlines and artificial intelligence seeming closer than ever, it is important to understand why China differs. China has had a slew of AI based laws and policies be implemented very recently, including byzantine regulations on its implementation in advertising, BIDU’s core revenue maker. Since FY19 machine learning and AI have been critical components of BIDU’s services. BIDU’s massive userbase and relationship with the Chinese Government enable the company to navigate the regulatory landscape easily. In this way BIDU has a distinct home-court advantage over foreign startups like OpenAI when it comes to AI penetration in China.

BIDU, CIC

Self-Driving

Apollo Go is Baidu’s autonomous driving development which is already providing ride hailing service. Apollo Go has had 1.5 million accumulated fully autonomous rides since its launch in 2017, expected to reach 2 million by the end of 1Q23. In Early 2022 the Chinese government granted Baidu a permit to collect cab revenues from the Apollo Go service in Beijing, followed by Chongqing and Wuhan. It is now present in 10 cities in China, including all of the largest cities in the country (often called “tier 1 cities” in Chinese news outlets). This completely dwarves any other project domestically in China or internationally. While specific data on the revenues of the company are not yet available, it is unlikely this division is yet profitable.

The Chinese autonomous vehicle market is expected to grow from $1.5 billion in 2021 to $100 billion in 2030. This represents a 60% CAGR.

Advertising and the Mobile Ecosystem

BIDU is the search engine in China, holding a similarly dominant position to Google. The fundamental core of the BIDU mobile ecosystem is the Baidu App with 648 million MAU (monthly active users). Instead of being a simple search engine on mobile, the app also provides third parties with the ability to provide native mobile experiences. The entire portfolio encompasses just over a dozen apps from shopping to social media.

BIDU, CIC

Traditional impression advertising has traditionally made up a large share of Baidu’s revenue. However, the novel Managed Page grew 10% year over year in FY22 to move up to 45% of Baidu’s core marketing revenue. Managed Page allows developers and website owners alike to provide Baidu users with a native experience without needing to spend money on development or maintenance. In addition, the Managed Page includes CRM software, facilitating small business sales.

For FY22 it accounted for 27% of the core segment’s revenue, up 500bps from FY21. However, total revenue has fallen by 6% year over year in the marketing area due to weak demand from advertising. Generally, during economic recovery periods, advertisers prefer to spend on performance-based ads rather than bulk brand ads. The decrease in advertisers utilizing the platform did not decrease meaningfully. During the 4Q22 earnings call, BIDU management stated that so far in 1Q23 they had experienced a “recovery” in online advertising revenue. Particularly recovery after the Chinese New Year celebrations.

iQIYI

Established in April 2010 and acquired in 2013, iQIYI has rapidly grown to become one of China’s leading streaming services. 9 out of 10 Chinese adults utilize online video services daily, spending an average of 2 hours per day on video content. iQIYI has the dominant market share with 68% of Chinese adults reporting utilizing the service in FY22.

S&P Market Intelligence

iQIYI provides a tiered membership system, with an ad-supported free version being the default. The paying subscriber base in FY22 grew to 111.6 million, a 9.4% increase over FY21. However, total revenue for iQIYI was down 5% for FY22, Online marketing revenues for iQIYI fell 25% in FY22. BIDU stated it is because of fewer variety shows advertising products and a challenging macro environment.

Risk

Baidu has very little reach outside of China and mainly operates within the “walled garden” of the Chinese internet. While they do have the lion’s share of Chinese domestic traffic for many services, their expansion outside of China has been limited. In China, Baidu has approximately 80% search market share, whereas outside of China, it drops to an insignificant less than 2%.

Baidu is listed on the NYSE through a legal structure known as a VIE (Variable Interest Entity). VIEs are a workaround to bypass Chinese regulations prohibiting foreign investment in certain industries, allowing international investors to participate indirectly in the Chinese market. However, the VIE structure is a loophole in Chinese law. The Chinese government may decide to crack down on or disallow the use of VIEs. If this were to happen, it would likely directly result in a de-listing. The U.S. government has also been tightening regulations for foreign companies listed on American stock exchanges. The HFCAA (Holding Foreign Companies Accountable Act) requires foreign companies to comply with various US reporting standards and regulations or face delisting.

Final Thoughts

For FY22 R&D expenditures align with what they have been, stepping up to 19% of total revenues. We expect flat capex. AI cloud is expected to trim some offerings and standardize others to increase margins. Total capital expenditures are relatively low compared to previous years likely resulting from the relatively weak Chinese economy and slow recovery. BIDU has a manageable debt level, with a debt-to-EBITDA of 2.5x. This is higher than American counterparts in similar market positions, but BIDU does generate a large amount of free cash flow.

SeekingAlpha

BIDU is well positioned for good results in FY23 with Chinese macroeconomic conditions improving significantly as of 1Q23. BIDU has a dominant market share in several hypergrowth segments, and the upside outweighs the potential risks.

China ETFs Have Been Outperforming

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.