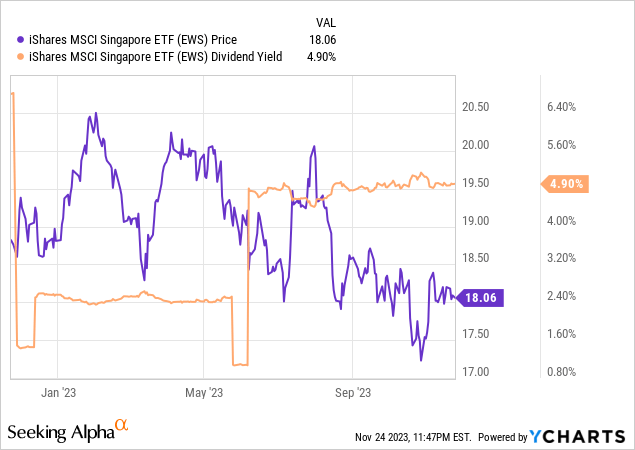

From an income perspective, you’d be hard-pressed to look beyond the well-covered 5% yield offered by iShares’ MSCI Singapore ETF. Yet, capital growth, including dividends, continues to be lackluster amid macro and industry-wide headwinds.

Barring a much deeper valuation discount, owning a fund as bank-heavy as EWS into a monetary easing cycle doesn’t seem all that appealing.

The iShares MSCI Singapore ETF (NYSEARCA:EWS) has seen further weakness since I last covered the fund, and justifiably so, given the deteriorating domestic and external macro picture. Having only just avoided a recession in Q2 before recovering (albeit to a still sluggish +1.1%) amid a regional trade downturn, inflation has, yet again, reared its head. In addition to the +60bps acceleration in headline consumer prices (+4.7% YoY), core CPI inflation also accelerated to +3.3% YoY, indicating the ‘stickiness’ of the country’s underlying inflation drivers. This elevated inflation trend isn’t likely to ease anytime soon – domestically, labor markets are tight, while imported monetary easing next year (the Fed sees 50bps of cuts in 2024), a result of Singapore’s exchange rate-targeting, could further complicate matters.

As we move closer toward monetary easing, the bank-heavy composition of EWS’ portfolio will work against it. Even with the sector benefiting from near-term net interest margin support amid the Fed’s ‘higher for longer’ stance, this tailwind will eventually revert once rates reverse course. In turn, bank dividends, the lynchpin of EWS’ distribution, could well be pulled lower next year. Further compounding rate uncertainties are ongoing issues around slower loan growth and weaker fee income following the implementation of stringent anti-speculation measures for property (another key EWS sector exposure).

The price still doesn’t adequately reflect the risks, in my view, at the current ~11x earnings multiple – not cheap relative to consensus MSCI Singapore earnings growth of ~2% next year. Pending a meaningful de-rate, I still don’t see a compelling risk/reward here.

iShares MSCI Singapore ETF Overview – Still a Highly Concentrated, Bank-Heavy Portfolio

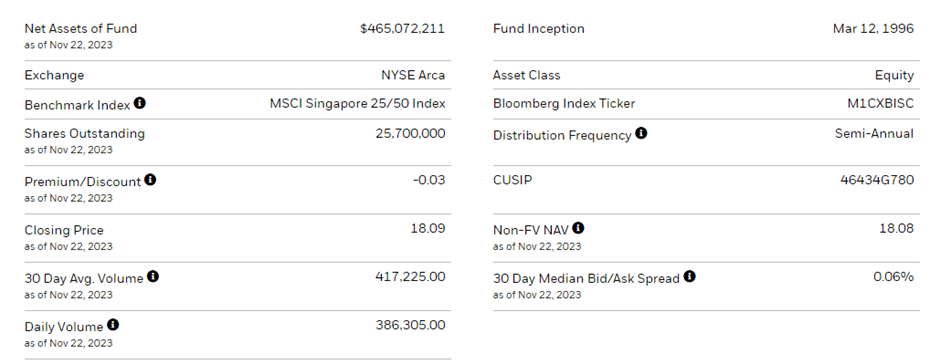

The iShares MSCI Singapore ETF tracks (pre-expenses) Singapore’s mega-cap stocks via the MSCI Singapore 25/50 Index, subject to two key concentration limits – 1) that any individual stock holding cannot exceed 25% and 2) the sum of all 5% positions should not cross 50% of total assets. The ETF has seen its net assets decline to ~$465m over the last quarter, reflecting investors’ increasingly downbeat sentiment on the geography. Its expense ratio remains competitive, however, at 0.5% despite the scarcity premium associated with being the only US-listed Singapore investment vehicle.

Despite its weightage limits, the 23-stock EWS portfolio retains an outsized sector exposure to Financials at 49.0%. The second largest sector exposure is listed as Industrials (17.7%), a catch-all classification covering everything from diversified conglomerates like Keppel (OTCPK:KPELF) to airlines (Singapore Airlines (OTCPK:SINGY)), and tech (Grab Holdings (GRAB)). EWS’ other key sector exposure is Real Estate at 16.5%. Along with Communication (8.7%) and Consumer Staples (3.1%), the fund’s top five sectors account for ~95% of the portfolio, making this a very top-heavy ETF. That said, the fund’s bank-heavy composition also makes it a particularly defensive one, with its equity beta remaining low at 0.76 to the S&P 500 (SPY).

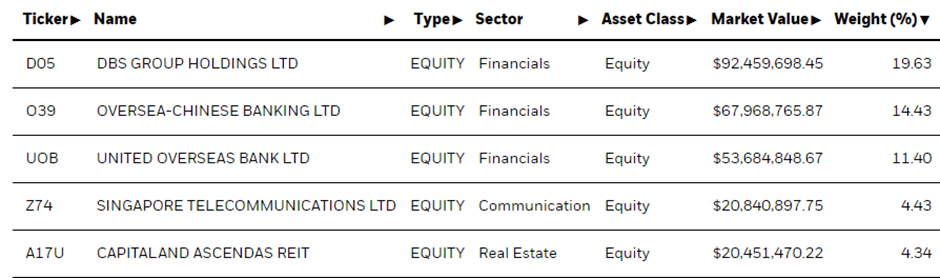

Unsurprisingly, the single-stock allocation also remains skewed toward Singapore’s big banks – EWS’ top-three holdings comprise DBS Group (OTCPK:DBSDF) at 19.6%, Oversea-Chinese Banking Corporation (OTCPK:OVCHY) at a higher 14.4% and United Overseas Bank (OTCPK:UOVEY) at 11.4%. The ex-banking portfolio has seen some reshuffling, with e-commerce/digital entertainment company Sea Limited (SE) and flag carrier Singapore Airlines (OTCPK:SINGY) dropping out of the top five. Instead, telco Singapore Telecommunications (OTCPK:SGAPY) and CapitaLand Ascendas REIT (OTCPK:ACDSF) are now the largest non-bank holdings. With EWS’ top-five holdings contributing an outsized ~54% of the overall portfolio, the fund’s fortunes remain closely tied to a handful of stocks.

iShares MSCI Singapore ETF Performance – Headed for Another Down Year

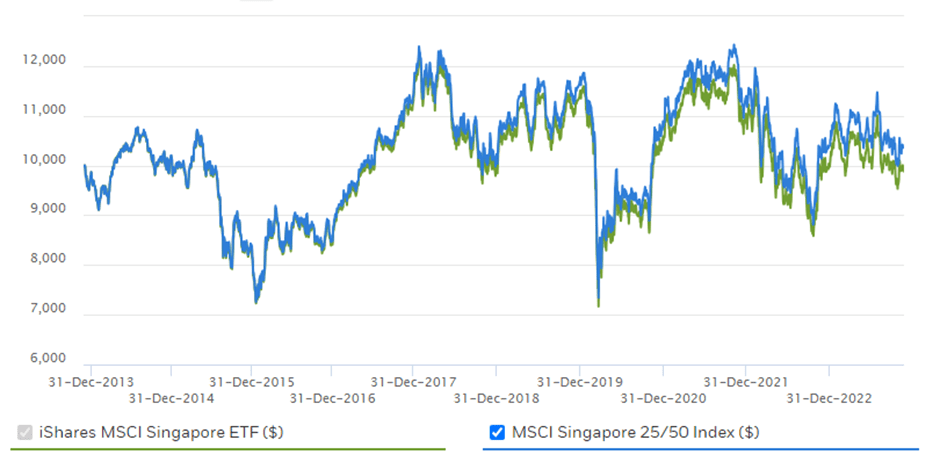

Following another string of down months on the back of poor guidance updates and sluggish macro data, EWS’ return to date has turned negative at -1.2%. Unless we get some positive surprises next month, the fund appears headed for another down year (note the fund declined by -9.2% in 2022) – disappointing after starting the year on a strong note. In turn, the overall return since inception has also moved lower to +2.1% annualized (market price and NAV terms). Like many of its Southeast Asian counterparts, though, much of the capital growth was achieved in the fund’s early years; over the last decade, EWS has actually lost -0.5% on an annualized basis.

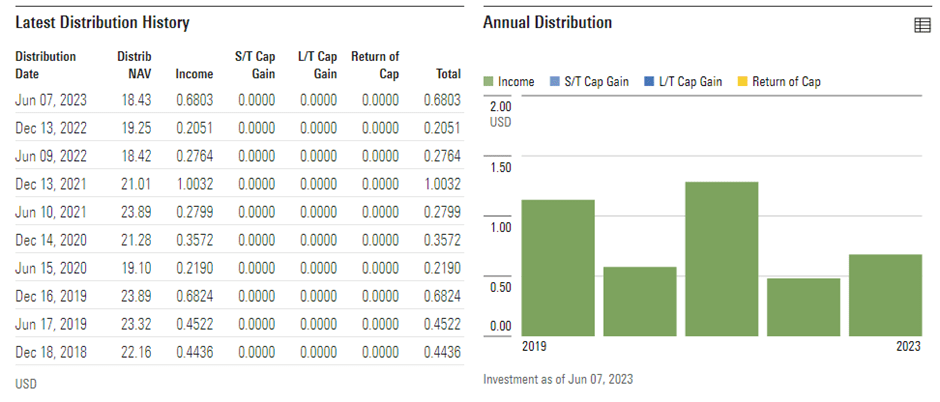

The poor track record comes despite EWS maintaining one of the highest distribution yields in Asia, currently at 5.1% on a trailing twelve-month basis. Coming off a strong H1 2023 distribution and with key Singaporean bank earnings still riding high on elevated rates, I remain hopeful of more yield upside heading into year-end. Beyond this year, however, I question the sustainability of EWS’ distribution, particularly with its bank holdings poised for some margin compression as we enter a monetary easing cycle. Hence, lower yields seem likely beyond 2023, a view reflected in the continued de-rating of EWS’ portfolio valuation. At ~11x P/E (~30% premium to book) relative to consensus estimates for ~2% earnings growth next year and a 4-5% pace beyond that, though, the fund reflects more optimism than pessimism, in my view.

Fundamental Headwinds to Outweigh the Attractive 5% Yield

Singaporean equities have long been an income favorite – perhaps for a good reason, given the ~5% EWS dividend yield currently. The issue, however, is capital growth, a key factor behind EWS investors realizing a negative total return over the last decade.

From a macroeconomic standpoint, Singapore’s economy isn’t going to offer much support – the country did return to growth mode in Q3, though the sluggish +1.1% pace indicates many of the external headwinds that weighed on growth aren’t going away. More worryingly, domestic inflation is accelerating and ‘sticky’ due to a tight labor market, leaving little room to loosen the strict property-related restrictions implemented earlier this year.

These policies will inevitably bite hard, so even if Singapore ‘imports’ the Fed’s monetary easing next year (via its exchange rate-focused monetary policy), EWS’ property exposure could still underwhelm going forward. Banks, the other key component of the fund’s portfolio, also tend to perform poorly in easing cycles and will likely be a key drag on returns as rates decline.

In contrast, EWS is still priced at a relatively pricey low-teens multiple of earnings vs consensus expectations for ~2% earnings growth next year – this seems fairly optimistic to me. Pending a meaningful de-rate, I don’t see a compelling reason to be long EWS.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.