Tesla, Inc. (NASDAQ:TSLA) announced its financial results for Q1 2024, and in this article, I review the results in light of the framework I laid out in my earnings preview titled, “Tesla’s Q1 Results Will Be Riveting, But Let’s Focus On What Matters,” in which I recommended investors to Hold Tesla stock into the earnings release.

Tesla’s Margins Will Remain Depressed

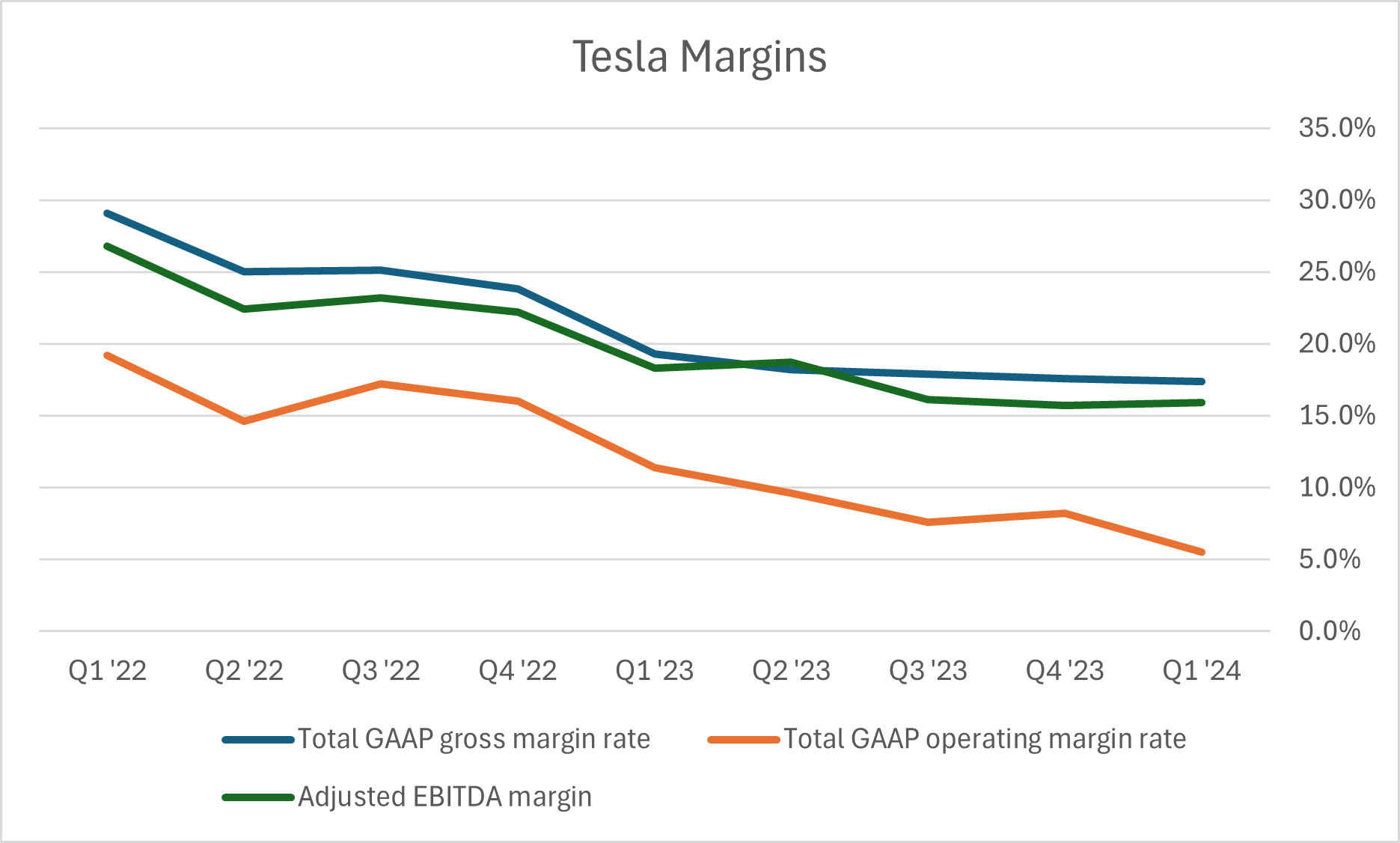

Tesla’s Q1 2024 results missed both top-line and bottom-line estimates, and as you’ve likely read the many headlines, I won’t rehash them here.

I discussed Tesla’s pricing strategy in “Tesla: Here’s Why It’s Down 24%” and predicted that the company’s profit margins would be pressured “for at least the first quarter,” and that’s what happened in Q1:

Seeking Alpha

Interestingly, Elon Musk contradicted my forecast for Q2 with his “We think Q2 will be a lot better” remark during the earnings call, and he may prove right. Cox Automotive points out that “new-vehicle affordability factors moved in support of consumers again in March.” As I illustrated in my earnings preview, however, the decline in Tesla resale values continued even as industry-wide resale values improved in the last 30-day period. Thus, I remain skeptical about Q2.

So why was the Tesla stock price up more than 10% the day after the earnings release? Let’s focus on what matters, specifically, the fundamental items I listed in my earnings preview.

Cybertruck Production Reached Volume

I said in my earnings preview that Cybertruck “is an important product that could change the narrative,” and Lars Moravy, the VP of Vehicle Manufacturing, said the Cybertruck production rate reached “1K a week” a couple of weeks ago. Tesla’s production ramps have historically been difficult, and this one is no different. However, if Tesla can continue this rate of progress with the Cybertruck, I expect the Cybertruck to reach breakeven profitability in Q2 and contribute meaningfully to Tesla’s gross profits starting in late 2024.

Lars Moravy also provided investors with several critical updates on Tesla’s 4680 battery production ramp (emphasis mine):

4680 production increased about 18% to 20% from Q4 reaching greater than 1K a week for Cybertruck, which is about 7 gigawatt hours per year as we posted on X. We expect to stay ahead of the Cybertruck ramp with the cell production throughout Q2 as we ramp the third of four lines in Phase 1, while maintaining multiple weeks of cell inventory to make sure we’re ahead of the ramp. Because we’re ramping, COGS continues to drop rapidly week-over-week driven by yield improvements throughout the lines and production volume increases. So our goal, and we expect to do this, is to beat the supplier cost of nickel-based cells by the end of the year.

Tesla kicked off in-house battery production in late 2020, and although Tesla failed to achieve its target of 100 GWh per year by 2022, Tesla’s 4680 battery production continues to ramp at a steady rate. It’s notable that Tesla could potentially “beat supplier cost” in a few years after it started, as Tesla’s battery suppliers have had years of head start in battery production: For example, LG Energy Solution, which will supply 4680 batteries to Tesla, was one of the earliest players to enter the lithium-ion battery industry, beginning R&D as early as 1992 and mass-producing in 1999.

In summary, Tesla’s production ramps are moving in the right direction, and I expect the Cybertruck to contribute meaningfully to Tesla’s profits later this year, but in Q2, I expect Tesla’s Automotive margins to remain depressed. Having said that, the next section is what matters the most to my analysis.

Tesla Is An Artificial Intelligence Company

During the first earnings call since the exit of top-level management talent at the company, Tesla’s Director of Autopilot Software, Ashok Elluswamy, took center stage with critical commentary, and I expect that to continue in future quarters. The following are my takes on AI-related developments.

Optimus Program Is Progressing

Optimus, Tesla’s humanoid program, is progressing, and Tesla aims to use Optimus in its factories by the end of 2024. Elon Musk added that Tesla “may be able to sell it externally by the end of next year,” but I believe investors will wait to see how internal testing progresses throughout 2025 and 2026 before potentially adding Optimus into their forecasts for the outer years.

Tesla Rigorously Developing Full Self-Driving (“FSD”)

Ashok Elluswamy presented for three minutes, starting at 25:20, about Tesla’s data-oriented, methodical, multi-tiered approach to internally testing the safety of each FSD update before pushing it out to its external customer cars. Ashok noted that Tesla trains “hundreds of neural networks” and tests them using millions of safety-critical clips collected from external customer cars and the internal QA fleet, as well as simulation systems that do the same in a closed-loop fashion. I recommend reading this paper published by Alphabet Inc.’s (GOOG), (GOOGL) Deep Mind in March 2022 to build the necessary knowledge base to fully appreciate Ashok’s comments on “scaling laws.” Specifically, Ashok said:

In terms of scaling laws, people in the AI community generally talk about model scaling laws where they increase the model size a lot and then their corresponding gains in performance, but we have also figured out scaling laws and other access in addition to the model side scaling, making also data scaling. You can increase the amount of data you use to train the neural network and that also gives similar gains and you can also scale up by training compute, you can train it for much longer or make more GPUs or more Dojo nodes and that also gives better performance, and you can also have architecture scaling where you count with better architectures that for the same amount of compute for produce better results. So a combination of model size scaling, data scaling, training compute scaling and the architecture scaling, we can basically extract like, okay, with the continue scaling based on this – at this ratio, we can sort of predict future performance.

The above quote by Ashok Elluswamy was, in my opinion, the most critical comment made yesterday because it applies to both the development of Full Self-Driving and Optimus programs. Sadly, but not surprisingly, I have not seen it mentioned in any article or discussed in any interview. I’ve been laser-focused on Tesla’s AI efforts recently, and I’d gladly answer any questions you may have on the topic, the above quote, or the Deep Mind paper that, I believe, will prove critical to forecast a reasonable timeline for FSD software adoption and the capability of the Optimus humanoid in future years.

Tesla Investors Will Need To Be Patient

I note the following two materials, company-specific risks to Tesla investors.

First, Tesla’s AI efforts are unlikely to help financial results in the near future, as I expect Tesla’s robotaxi service to take years to develop and scale. Further, I do not expect a material, step-change in FSD software adoption until Tesla demonstrates to regulators that its fleet-wide, safety-critical interventions are materially below the accident rate of human-driven vehicles. According to the FSD disengagement data, visualized by this crowdsourced tracker, I do not expect Tesla to achieve this milestone in 2024 or 2025.

Second, despite Elon’s comment on the call that even if he “got kidnapped by aliens tomorrow, Tesla will solve autonomy,” I expect the FSD adoption, the scaling of a robotaxi service, and the Optimus program to require more effort than simply getting the technology to perform as intended, and without a strong, technically oriented but still visionary leadership at the helm, I find it unlikely that Tesla would be able to realize wide-adoption of its AI products and services. In short, Tesla’s potential carries material key person risk.

The Bottom Line

Tesla’s Cybertruck and 4680 battery production ramps are moving in the right direction, so the worst for Tesla’s bottom line is likely behind us; however, Tesla’s AI products and services will not materially contribute to its financial results in the near term, and I believe market participants will wait to see continued progress. I continue to rate Tesla stock HOLD and look forward to respectful debates in the comments below this article.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.