Oil and Gas Outlook

Energy is one of, if not THE MOST important issue in society today. Fossil fuels are a hotly debated topic these days and trying to make sense of the outlook and future of fossil fuel markets can be overwhelming – especially between politics, climate change regulation, and the global chaos in the world today. As a Nobel Prize in Literature recipient once said, “The times, they are a changin’.” And Bob Dylan couldn’t have been more right about that.

With advances in technology, administration policy in the United States, and continued geopolitical conflict, there are myriads of external variables that could alter the oil & gas markets quite drastically in the coming months and years. In this article, I’ll explore some of the major events and circumstances clouding the uncertainty of the energy sector and how these factors could affect specific oil & gas markets in the United States and their overall effects on oil pricing.

As it stands today, the Brent crude oil spot price in the EIA (Energy Information Agency) forecast averages $85/bl in 2023, up $2/bl from last month after OPEC announced supply cuts. The higher price reflects a forecast for less global production in 2023 and a relatively flat year-over-year global consumption outlook. Additionally, Brent crude spot average in 2024 is currently $81.21/bl. Some in the industry think the EIA data may be more bullish than the market and world events reflect.

The Biden administration announced in April the intention to repurchase crude oil for the Strategic Petroleum Reserve, at a price level between $62-$72 dollars per barrel. With last year’s 180 million barrel sale from the SPR, the stockpile is at its lowest level since 1983. But these purchases cannot be made until the U.S. fulfills its congressional mandate to sell 26 million barrels in fiscal 2023. In the event of a further global conflict breaking out, it’s quite feasible to think the price of oil could once again visit the $100/bl benchmark.

About this article: This article is not intended to be a definitive guide or the absolute truth. It’s intended to be speculative in nature and to start a discussion on the possibilities surrounding the oil markets, specifically as they concern my intended audience – the dividend investor. It is also intended to be written in a simple and accessible manner for all investors, and not just industry gurus. Please give me a follow for more analysis on dividend focused energy companies.

Now let’s get into it!

Price Uncertainties

There are numerous external variables that could have major effects on the oil markets in the near future. All of these variables have the potential to greatly alter the direction of the market so it’s important for investors to understand what these potential effects might be.

OPEC+

OPEC+ supplies approximately 30% of the world’s oil and they currently own about 80% of the world’s reserve crude oil. Comprised mostly of members that are not friendly to the United States, the organization routinely cuts or increases supply to inflate or manipulate oil prices. If oil prices decline due to a recession look for OPEC+ to announce an additional surprise production cut to keep prices inflated. Conversely if prices rise significantly they may increase production so they can take advantage and reap higher profits.

Climate Change & Regulation

Climate change is another massive issue facing the oil & gas industry. With increasing regulation seemingly every day, the government is driving the cost of production up for American drillers. While many would argue regulation in this arena is an overall positive for the world, increasing the cost of production for American shale producers will certainly not help their ability to counter OPEC+ market manipulation. Additional regulation hits some regions harder than others, so it’s important for investors to understand the areas where producers operate and pay attention to breakeven pricing in the region.

Recession Fears

Many would argue that the recession in the U.S. has already arrived, but regardless of your opinion on the timing, a recession has a certain probability of occurring here in the US. Unemployment numbers are expected to rise (the FOMC predicted 4.5% in 2023 in the last SEP), and consumer demand will likely go down, barring global conflict. We’re already seeing pre-emptive layoffs in sectors that have no demand decreases as employers brace for a potential downturn. This means that oil prices will likely continue to fall, in which case I would expect a surprise production cut from OPEC+ members to inflate prices.

Geopolitical Tensions

It’s no secret that geopolitical tensions are higher than they’ve been in decades, arguably worse than the cold war. With the recent drone attack on the Kremlin, the world seems to be on the cusp of WWIII. With any further escalation of conflicts, we can assume oil prices will rise significantly and remain higher through the duration of the conflict based on supply disruptions and increased demand. Ukraine and Russia are not the only countries at odds right now with more and more reports of an imminent conflict looming between the United States and China over Taiwan. Whether that happens or not is up in the air, and seems unlikely to occur, however the mere thought of it can cause increased pricing in the futures markets.

Recession Effects

Naturally, oilfield service providers would be among the hardest hit companies in the event of a lasting recession and decreased global demand. And this is true across all sectors of the oilfield – upstream, midstream, and downstream. Producers would likely curb new drilling activity substantially and be forced to shut down certain areas of production or look at vertically integrating to lower operational costs and shield themselves from the effects of low prices.

Upstream

Producers in the United States are more vulnerable to price dips compared to OPEC+ members as the cost of production for North American shale is much higher than, for example, Saudi Arabian oil. The average breakeven price for shale producers in the Eagleford Shale (one of the most prominent shale formations in North America) was around the $48/bl level for new wells. In comparison, it costs somewhere around $10/bl to drill a well in Saudi Arabia. Comparatively, the average breakeven price for existing wells in the Eagleford Shale is around $23/bl.

In the event of a recession, prices would likely drop to begin, followed by OPEC+ output cuts to raise prices. While oil prices may be artificially supported for a period of time, new drilling activity would likely decline significantly, particularly in North American shale plays.

Producers would likely scramble to improve efficiencies in drilling processes and drive down operational costs by any means necessary – including through key mergers and acquisitions. Existing wells should continue to produce but with a likely added cost of storage in some situations.

Midstream

Just like the rest of the oilfield, midstream companies would see a slowdown in gathering, processing, and transporting needs as well. However, the midstream market is a bit more shielded from recession and market woes as regardless of demand, oil and gas will still be processed and transported, and the revenue collected by midstream companies isn’t as directly dependent on oil prices.

Additionally, storage would become a big priority for producers, as was the case in 2016 when bids and costs for above-ground storage hit record highs. Storage is a big reason midstream companies would be less negatively affected. In my opinion, the savvy dividend investor would do well to focus their efforts in this area of the energy sector.

Downstream

A recession would also hit refineries in the downstream segment of the oil and gas industry negatively as consumer demand for the thousands of end-use products would slow and total output would slow.

However, downstream companies could be more shielded from negative effects than producers as refineries can maintain higher margins with lower pricing, even when consumer pricing is also lower. The bigger worry for downstream companies would be geopolitical conflict and drastic supply shortages in the short-term.

Likely Scenario

Assuming cooler heads will prevail and WWIII doesn’t end up breaking out, let’s take a look at the likely scenario for the short-term future of the oil & gas market. Banking fears are here to stay for the moment, and markets are currently reflecting that – having already wiped out all the gains from OPEC+ production cut announcements. With the prospect of a light recession looming over the next year, investors can assume spikes in unemployment and curbs on oil demand are on the horizon. And this means that oil prices are likely to decline in the near term.

Even with the worst economic reporting likely, I don’t see oil prices bottoming out much below the $55/bl range in 2023, especially with the commitment to refill the SPR. At this level, producers should continue pumping existing wells, and companies in more favorable shale plays will likely proceed slowly and cautiously with new drilling.

The more likely scenario that will happen is that oil prices will drop to somewhere around $60/bl in the short term. Following the drop, I expect oil prices to rebound with an artificial “surprise” OPEC+ supply cut and increased demand to hover between the $65-$75/bl range, ultimately reaching somewhere between $75-$80/bl by the end of the year.

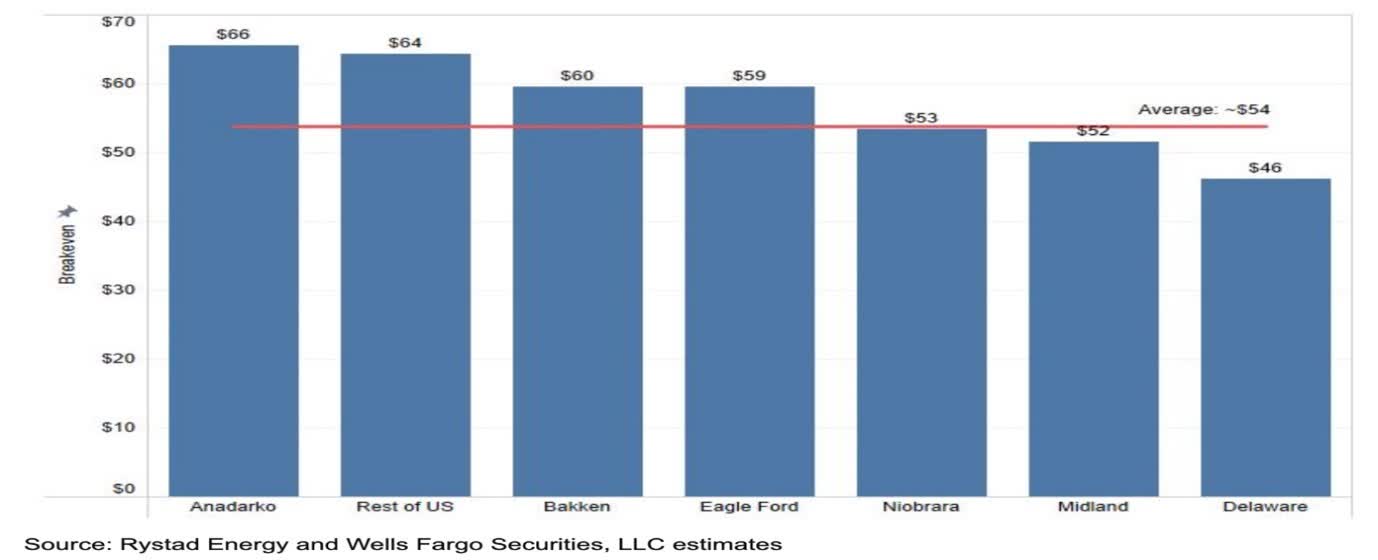

Breakeven prices for a few basins in the US (Rystad Energy and Well Fargo Securities, LLC)

The average breakeven price for American shale drilling is around $54/bl for new wells. The Anadarko shale is one of the most expensive areas to drill in North America, whereas the Delaware basin is the least expensive area to drill. Basically, the lower breakeven price the better at the moment for investors who want to shelter against a downturn.

Conclusion

Companies exposed to operations in higher breakeven areas will be the first affected by a recession. You need to be mindful of production areas. You should take a close inspection of your upstream holdings and ensure that they’re in the right places for – low breakeven basins.

You should look closely at the company’s investor presentations as they almost always contain this critical breakeven information. Many Seeking Alpha analysts also include it in their articles on the company in question. See if they can continue drilling at lower oil price points, or if they will need to stop entirely. For example, Anadarko basin companies are going to have a very tough time drilling and expanding at these price levels.

If your position is in a high breakeven area, and the position is in profit, then you may want to consider taking your gains and reinvesting in midstream or lower breakeven plays. You want to make sure the company you’re in can keep up their dividends even in a downturn.

I would strongly recommend a focus on midstream for any new entries into the market for the dividend-minded investor as well. Midstream will be less affected by a potential downturn and should be much more able to continue paying base and variable dividends.

An additional focus on midstream companies with high storage capacity and low current utilization would be a plus to take advantage of additional revenue streams that could come from an economic slowdown. I recently reviewed a midstream company, HESM, that you might want to take a look at.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.