In the history of televised debates between U.S. presidential contenders since 1960, the recent one held between the incumbent President Joe Biden and the challenger former President Donald Trump stood leagues apart from the first ever televised debate that was held between Richard Nixon and John F. Kennedy. In the first, participants were fairly convivial with each other while in the most recent one, participants were abrasive and held back from talking/shouting over each other by moderators muting each participant’s microphone while the other was speaking. In the first, rebuttals were delivered with a modicum of calm and respect while in the latest, one contender called the other a “sucker” and “loser” with the “morals of an alley cat”. Viewers of the first-ever televised debate were fairly split on who made the best points; in the latest, overall viewer (and analysts’) perception was that President Trump (born roughly one year after the end of World War II) sounded relatively much more coherent than President Biden (born roughly two years before the end of World War II) and little else by way of consensus.

During the course of this highly testy spectacle, President Biden asserted the conclusions made in an open letter signed by 16 Nobel-winning economists released two days prior to the debate thus: “…if Trump is re-elected, we’re likely to have a recession, and inflation is going to increasingly go up.”

The markers signifying a “recession” have been in place for some time. Market trajectories, meanwhile, are quite nuanced and not necessarily a prediction for a recession at first blush.

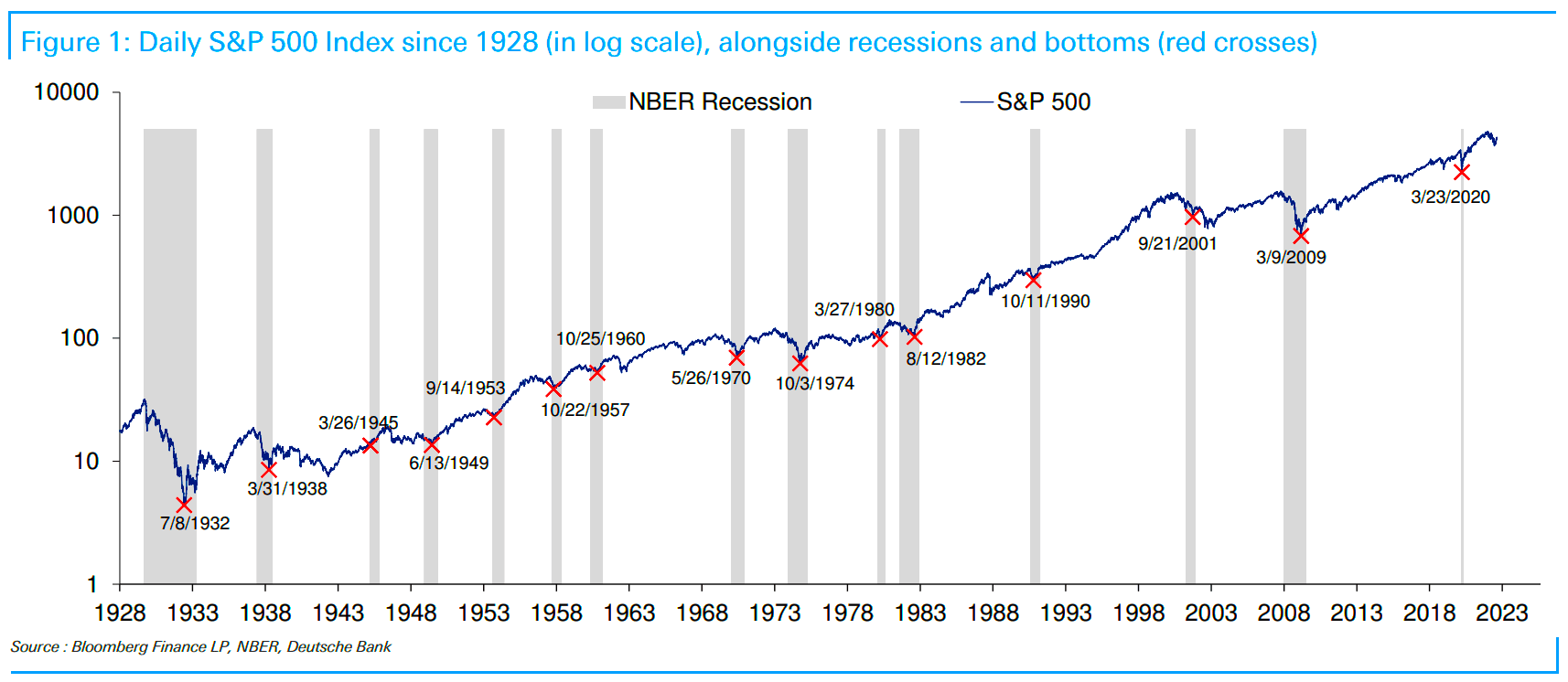

Markets vs Recession

Any notion that markets tank (or stay) during a recession could best be called a “misremembering”: while markets do tend to drop at some point during a recessionary period, there is also a bullish trend for a substantial period of time.

Source: Deutsche Bank

Even if it is argued that the “dot-com” bubble and the advent of tech stocks as a frontrunner for the U.S.’ equity universe fundamentally changed market behaviour and investor convictions, a trend that has generally persisted over a century has been that markets rapidly run high before tumbling and then picking up a bullish trend while a recession is still underway.

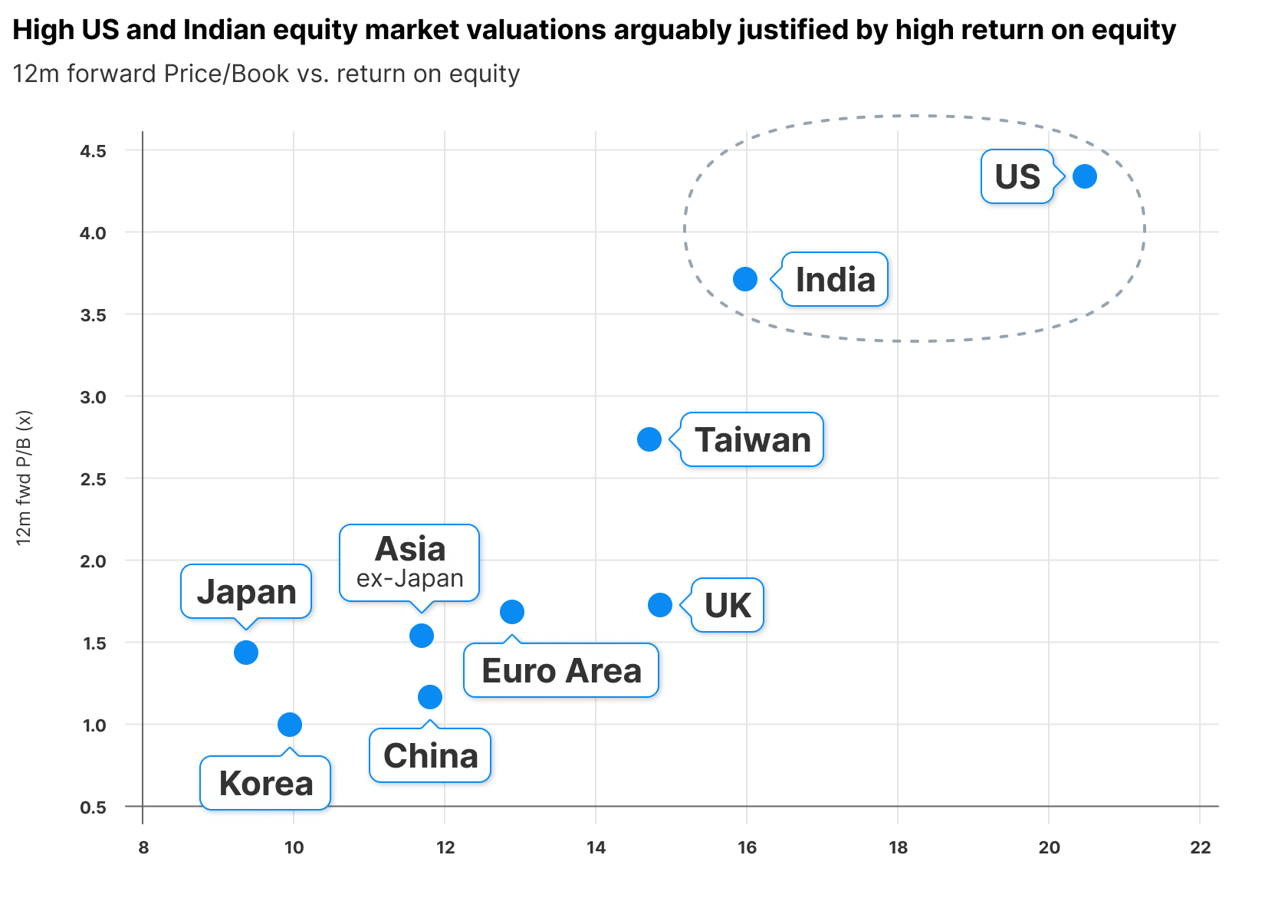

Standard Chartered Bank, in its recently released H2 2024 outlook, asserts that markets will remain mostly bullish till the end of the year. Of all major economic regions, overall U.S. equity valuations are deemed to be arguably justifiable on a forward-looking basis relative to return on equity. At a close second are Indian equities.

Source: Standard Chartered

The valuation story between these two countries, however, are markedly different. Indian indices have been rising on a year-on-year basis for over a quarter century, with economic policies in place for over a decade that prioritize domestic production to meet rising consumption by a growing populace rising above the poverty line on now-record levels. The rise of the U.S.’ S&P 500 (SPX in index form and SPY in ETF form), on the other hand, could best be described as a flight of capital that has been increasing in volume.

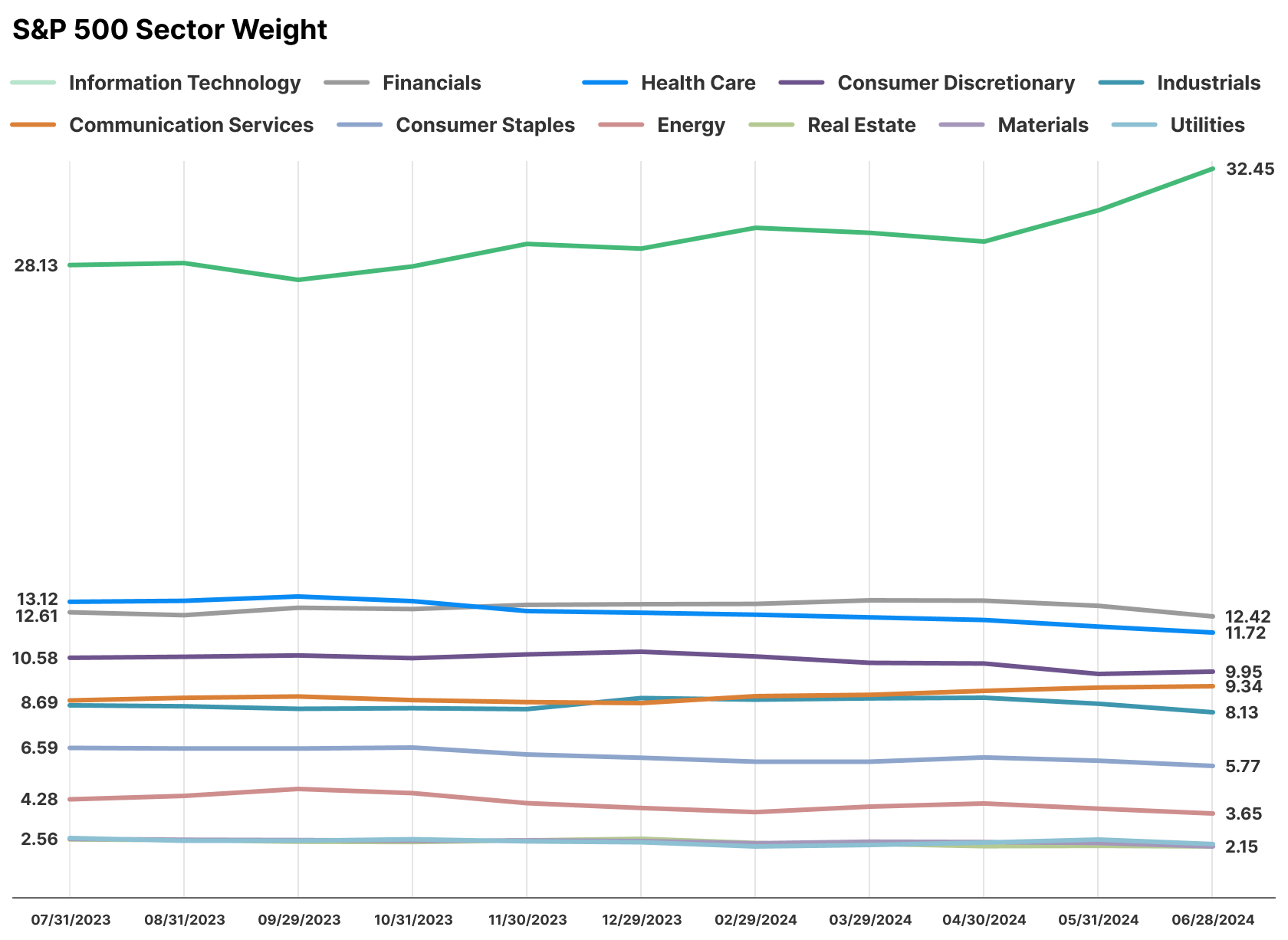

Source: Created by Sandeep G. Rao using data from Bloomberg (Chart Design: Courtesy of Leverage Shares)

As early as H2 2023, “tech” – which employs nowhere close to the number of U.S. residents as many other service and product-related industries – already accounted for well over a quarter of total index composition. As of H1 2024, it was well over a third. Over the past several years, “tech” had become increasingly more relevant to U.S. market trajectory at a cost to nearly every other sector of the American economy, global-facing or otherwise. Arguably only two other sectors have largely held their own in a more-or-less resilient fashion: energy and financials.

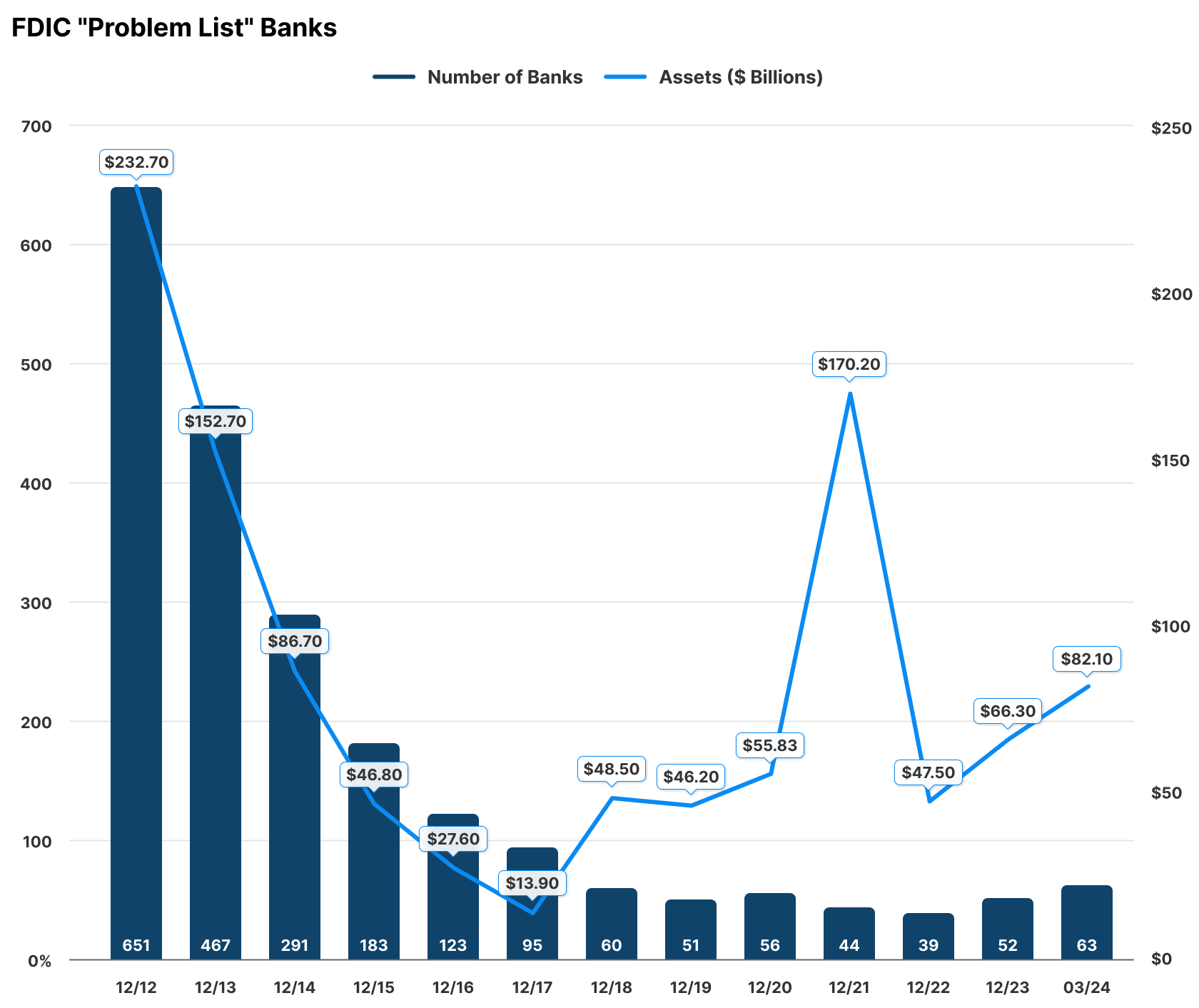

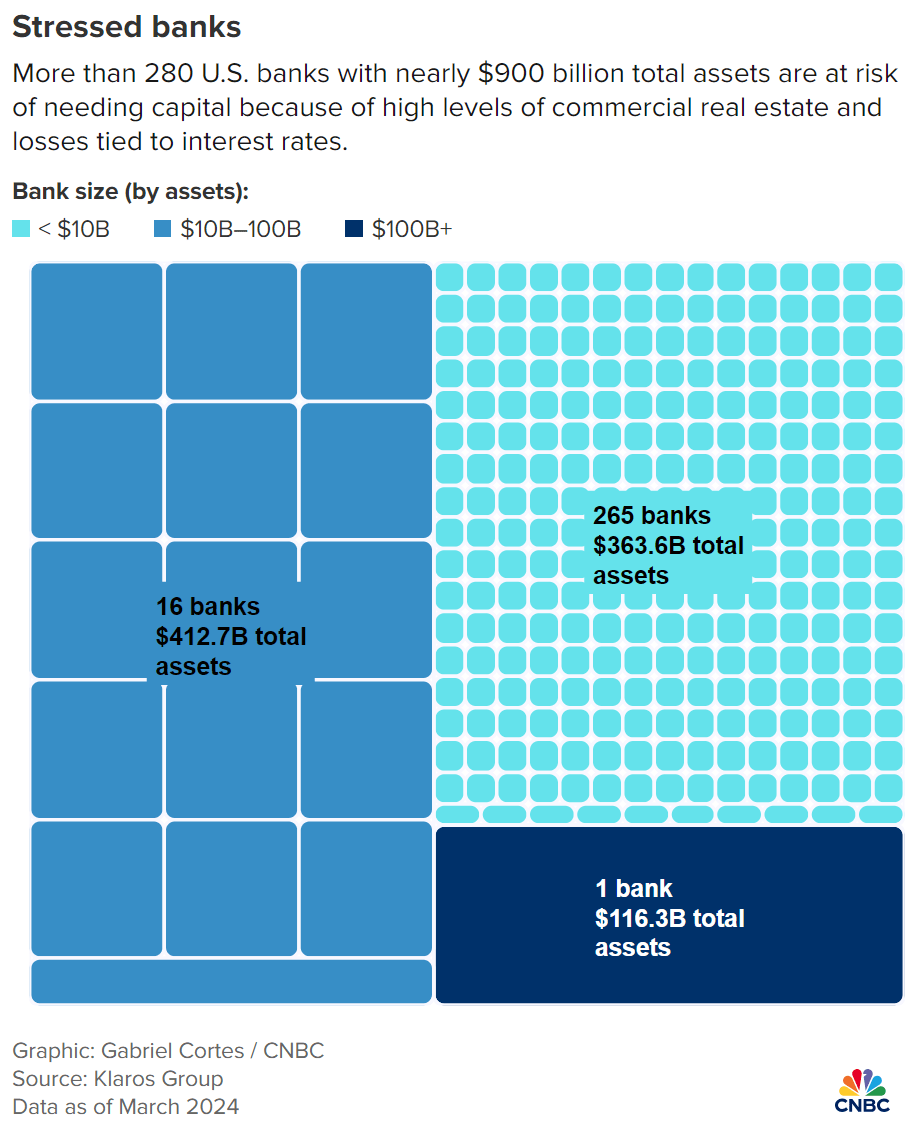

Within financials, however, all is not well. As per the Federal Deposit Insurance Corporation’s (FDIC) Quarterly Banking Profile – which is published approximately 55 days after the end of each quarter – for Q1 2024, the number of banks in its “problem list” as well as assets held in them has grown by a little under twice in number and size respectively relative to the end of 2022.

Source: Created by Sandeep G. Rao using data from FDIC (Chart Design: Courtesy of Leverage Shares)

As of the end of Q1 2024, the FDIC listed a total of 4,577 banks in the U.S. After hiking rates 11 times through July, the Federal Reserve has yet to start cutting its “benchmark rate”, leaving hundreds of billions of dollars of unrealized losses on low-interest bonds and loans on banks’ balance sheets which, when combined with potential losses on commercial real estate facing increasingly higher non-occupancy levels, leaves the banking sector increasingly vulnerable. Across Q1 2024, consulting firm Klaros Group analyzed 4,000 U.S. banks to gauge this combinatorial risk factor to arrive at the conclusion that 282 of those surveyed are likely to be in dire need of capital.

Source: CNBC and Klaros Group

Be it in choice of publicly-listed equity or consumer bank, “size” seems to matter more than ever. Top-of-the-line “tech” companies have grown in their ability to attract investor conviction, with big banks and globe-spanning energy firms remaining resilient for the past few years and even showing a slightly bullish trend in conviction across the past two weeks.

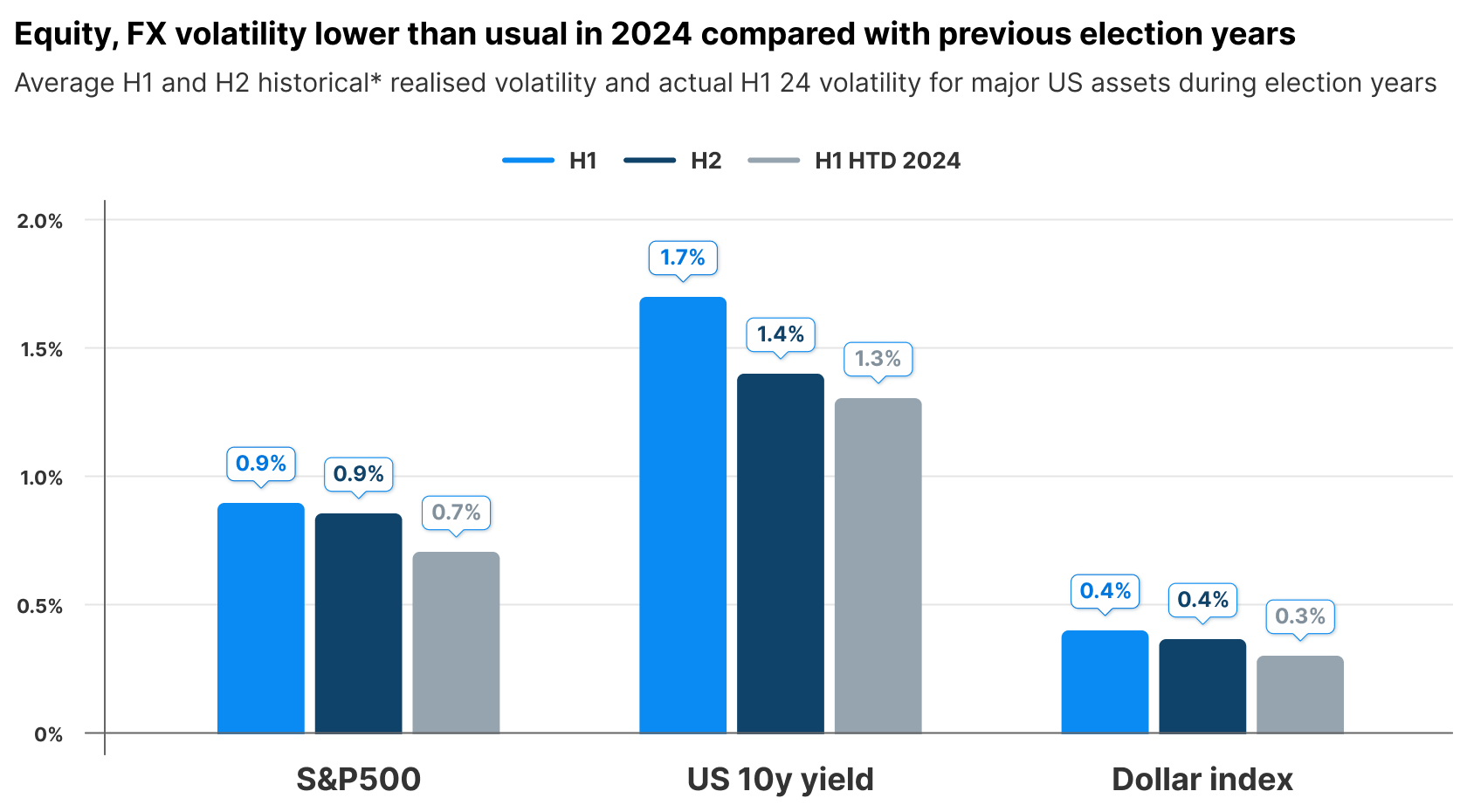

The “flight of capital” to these massive companies, with top-of-the-line “tech” companies in particular attracting conviction multiples larger than the rest of the batch in their sector/cluster, cannot reasonably be construed as a sign of the markets being healthy. As it stands, both equity and foreign exchange (FX) volatility have been lower in 2024 relative to average volatilities seen in previous years.

Source: Standard Chartered

Volatility is a key measure of market health in that it could either indicate a high level of price discovery in play from diverse pool of market participants or a sense of panic/resignation by a shrinking pool of investors. Overall, market participation trends with respect to equity choices hint more of the latter than the former and more of a “resignation” as opposed to “panic”.

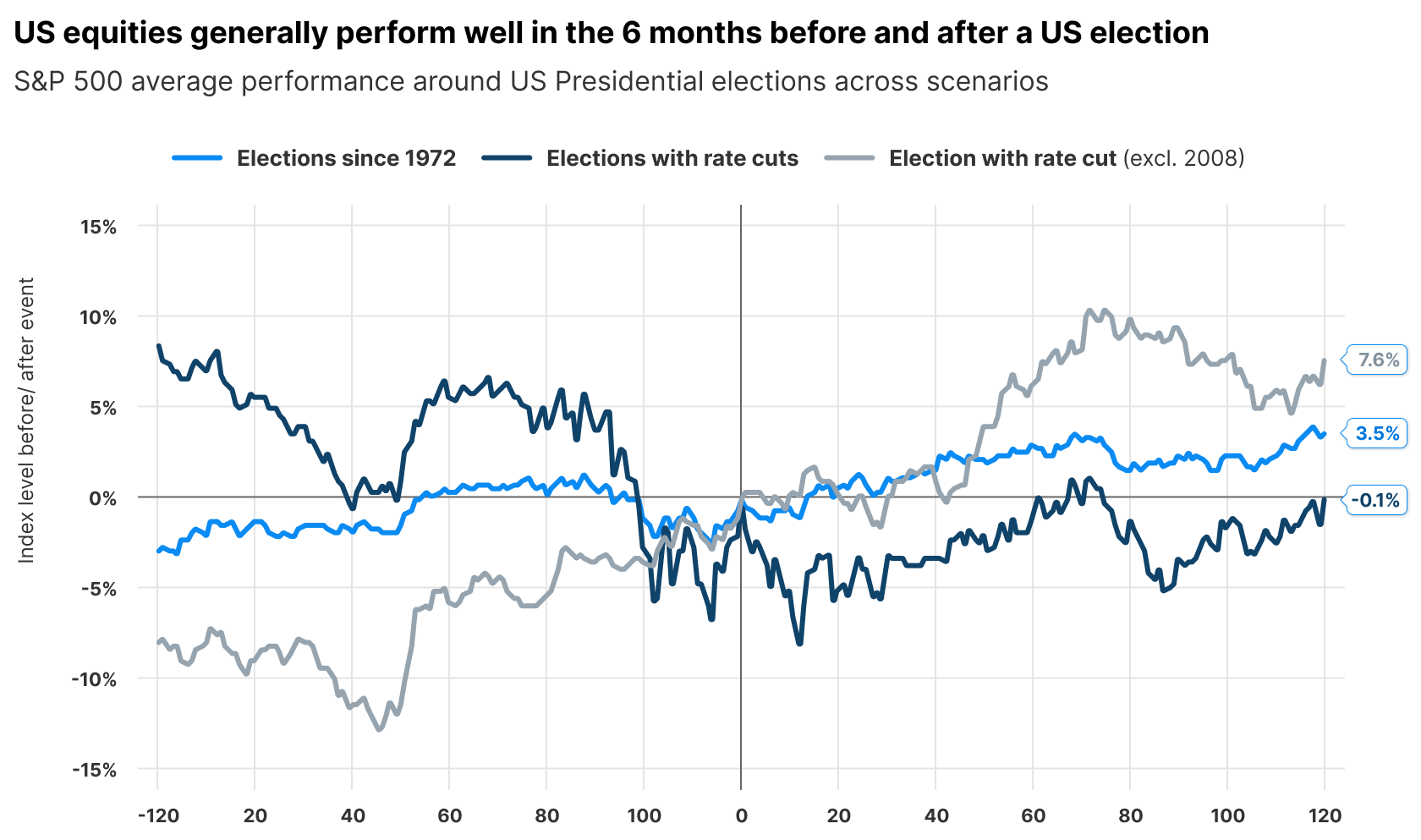

It also bears noting that, regardless of underlying economic conditions, market trends tend to be bullish both immediately before and after a national election in the U.S.

Source: Standard Chartered

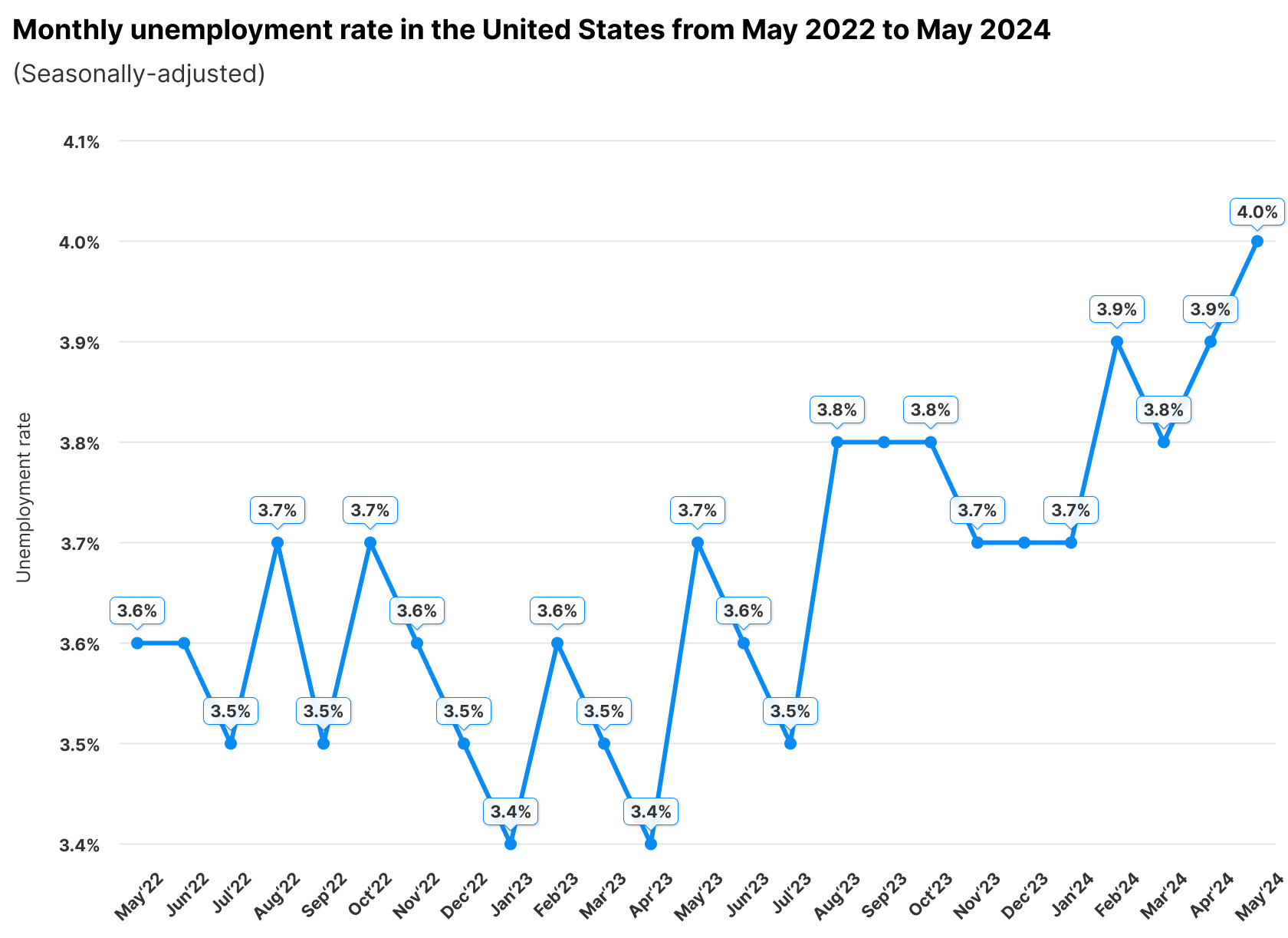

A “recession” is defined by the National Bureau of Economic Research (NBER) under very specific conditions, in which a softening labour market is a key requirement and is generally evidenced by the unemployment rate. There are early signs of a trend emerging here long before a second Trump presidential term has been determined.

Employment vs Recession

Given that economic health must factor in population participation, the unemployment rate is a key factor. In May 2024, the unemployment had risen nearly 11% relative to the same month in 2022 to reach 4%.

Source: Statista (Chart Design: Courtesy of Leverage Shares)

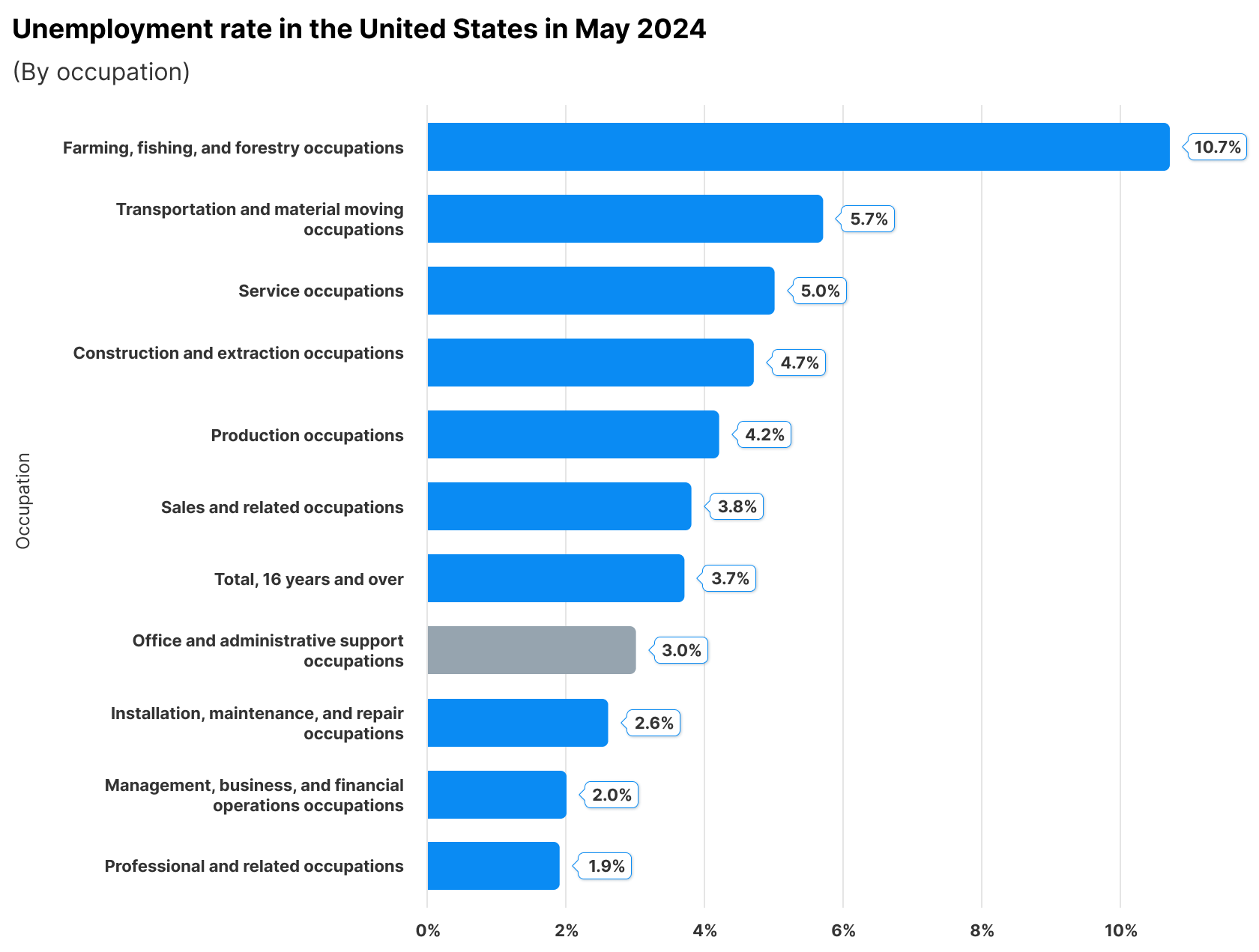

There’s a clear striation in the employment levels vis-à-vis the nature of occupation: professional and managerial workers have the lowest level of unemployment while labour-driven professions have the highest.

Source: Statista (Chart Design: Courtesy of Leverage Shares)

On the 5th of July, the U.S. Bureau of Labor Statistics (BLS) estimated June’s unemployment rate at a slight uptick to 4.1%. This implies that unemployment rate has registered a resilient uptrend across Q2 2024.

The term “estimation” is entirely appropriate in this context. Rather than considering, say, the number of applicants filing for unemployment benefits versus those making 401k contributions, the filing of W2 tax forms by employers and so forth in a nation of more than 330 million people of which at least two-thirds are adults, the BLS calculates its metrics via a survey – a method in play since before World War II. The BLS currently samples 60,000 households across 2,000 pre-determined geographical areas, which translates to approximately 110,000 individuals.

Given the rise and rise of volatile “gig economy” jobs and the potential for disparate circumstances between survey respondents and other residents within said geometric area or representative population, it could be argued that – despite BLS’ assertions regarding the accuracy of its methods – the true extent of unemployment cannot be or isn’t currently being accurately depicted.

In Conclusion

To be fair to the 16 Nobel-winning economists, there is some merit in arguing that President Trump’s promise to cut taxes would be the wrong direction to go in a country wherein (as described in an earlier article) around a trillion dollars of additional debt is being added every one hundred days. In a similar vein, cheap imports from China and other countries help prop up (and make affordable) sales in a country with the highest per capita consumption of nearly every major good and service. For President Trump to do so without lasting economic damage, it could be concluded that the way the U.S. government conducts itself (which is frequently a biparty consensus) and the way the citizen class consumes both need to change. This is necessarily an “evolution” rather than a “revolution”; the sooner it happens, perhaps the better.

While tax cuts might be a cause célèbre among his ostensible Republican colleagues on America’s “Political Right”, President Trump’s positions aren’t entirely orthodox. For instance, his promise to grant permanent residency to all foreign graduates of American universities is ostensibly a cause dear to his foes on the “Political Left”. Unlike many other countries, however, the United States government isn’t a monolith centered on the President’s diktats; parliamentary consensus is a byzantine road rife with compromise. As it stands, his “green cards for foreign graduates” proposal was instantly and roundly rejected by leading lights amongst his ostensible colleagues. Thus, regardless of promises, it might be somewhat early to prognosticate economic risk for the United States solely on President Trump returning to the White House. Instead, it bears remembering that the seeds of economic stress were sown and growing within the United States for a number of years now regardless of who was sworn into the White House.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.