Introduction

As an avid lurker on Reddit, Inc. (RDDT) and its many subreddits, it is surprising that I never got around to looking at the company in more detail until now. The company has had an amazing run since going public, with no signs of stopping, and I can’t help but draw parallels to another social media company that had an amazing run in the past, but without the negativity surrounding it for now. I am giving Reddit a Buy rating.

Performance

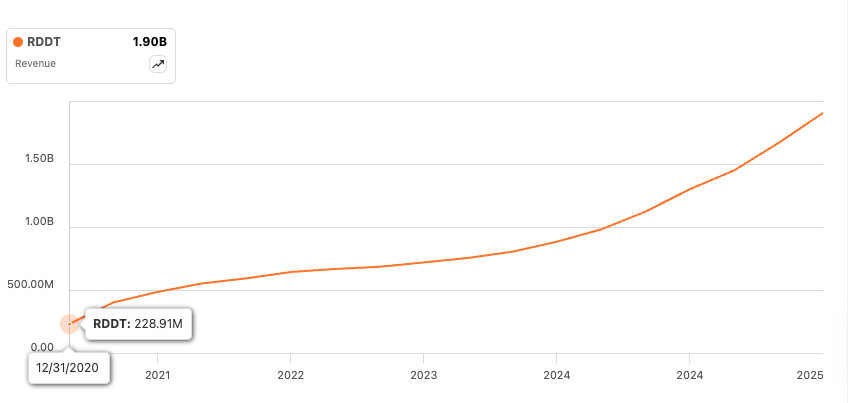

Since I am covering the company for the first time, it is important to check RDDT’s sales performance over its lifetime, and that is not a long life. From the end of 2020, the days of lockdowns and everyone glued to their screens, RDDT’s sales almost 10x’ed, going from around $228m to $1.9B. The latest quarter showed us that the company’s revenues for the nine months ended September 30th stood at around $1.5B, with an additional $660m to be made in the last quarter of ’25, so over $2.1B for the year. Since going public back in March of ’24, the growth remained strong.

Seeking Alpha

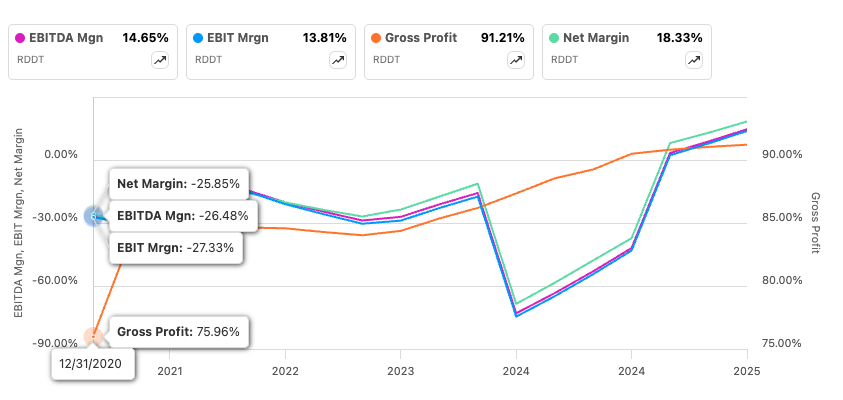

Looking at the company’s profitability, we can see that the company is quite profitable already, but seeing that its gross margins are over 91%, its operating margins, and the rest of the margins are quite low. In Q1’24, the company massively increased its R&D spending, and it’s a good thing that RDDT’s top line grew substantially since then, which helped outgrow the expenses and made it profitable once again. The over 91% gross margin allows for a lot of leverage and scalability in the future, as evidenced by a whopping 68% growth in sales, while expenses grew by around 31%. If the company continues this trend, margins across the board will grow significantly.

Seeking Alpha

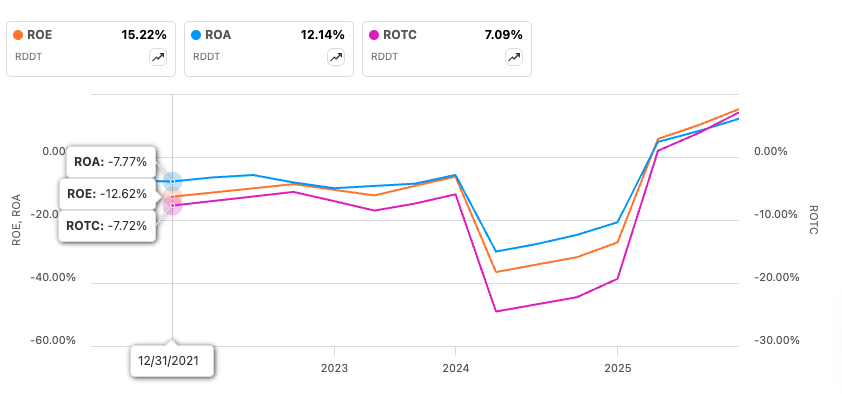

Taking a look at other important metrics to me, specifically the ROE, ROA, and ROTC, we can see that these are rising just as the company’s bottom line is, which are already at decent returns, especially ROA and ROE. ROTC, I believe, will easily climb over 10% over the next few quarters. Reddit has become a lot more profitable in a very short time, and that is due to its massive, engaged customer base. I believe this trend is going to continue.

Seeking Alpha

Looking at Reddit’s financial position as of the latest quarter, we can see it is flush with cash. $2.2B in liquidity available in the form of cash and marketable securities against essentially no debt besides some operating lease liabilities, which are negligible. That is a very strong balance sheet, allowing the company to focus its efforts 100% towards growing the platform, researching ways to monetize the massive, engaged audience, and improving the experience overall.

The growth has been astounding. The social media business model is so lucrative that it doesn’t take many years to be profitable, let alone break even. With such numbers that the company is putting out quarter after quarter, I can see the multiples shrinking considerably over the next few years.

Advertising- The most Lucrative business model

As with all social media companies, or at least the top ones like Alphabet (GOOG) and Meta Platforms (META), RDDT’s business model comprises over 90% of revenues made through advertising. Ad revenue increased 74% this past quarter, making over $549m of total revenues, so it is safe to say that right now, RDDT is an ads business, and there is nothing wrong with that. Such growth in sales wouldn’t be possible without a very dedicated user base. In the latest quarter, daily active unique, or DAUq, continues to grow at a decent pace, around 19%. The international DAUq grew at a respectable 31% compared to the US 7% growth y/y. The Global Weekly average unique numbers grew by 21%, with international leading the way with 37% y/y growth. These numbers are fantastic, which led to average revenue per user, or ARPU, growing substantially across all regions. ARPU in the US grew 54% y/y, international grew 39%, bringing down total ARPU to around 41% y/y. US ARPU leads by a massive difference compared to the international ARPU numbers, as you can see below.

RDDT 8K

It seems that advertisers are starting to like RDDT’s advertising platform for their products, which is evident in over 70% growth in ad revenue. Clearly outpacing the juggernauts of ad revenue like META and GOOG, which saw 26% growth and 12.7%, respectively. However, the low base of RDDT helps it shine here, since other companies are already mature with billions of daily active users under their belts. Nevertheless, advertisers are beginning to see the advantage of RDDT communities. You may be asking why?

There are a couple of reasons why RDDT is becoming the choice of so many advertisers. Probably one of the main ones is that the average cost per mille, or CPM, is much lower than what META and GOOG charge. RDDT uses an auction model, so CPM can range from about $1 to $6 for broader placements, which on average turns out to be around $3.5. Compare this to META’s CPM on average for Facebook was $14.40, and for Instagram, $13.20. Google CPM ranges from $4-$9, which is a lot better than META. So, as costs go, RDDT takes the cake; however, you can say that the reason it is low is because of the reach. Meta and Google have billions of clicks daily, so their reach is superior compared to RDDT, which means most likely in dollar terms, a big company is better off paying for ads on these two platforms and not RDDT. It is also worth looking at the efficiency of these ads. Having such al ow entry point to advertise on RDDT, the return on ad spend, or ROAS, can often be a lot more attractive than META or GOOG.

The conversion rates are quite a bit higher compared to Facebook and Microsoft’s (MSFT) LinkedIn, with RDDT’s rates ranging anywhere from 3%-6%, while Facebook and LinkedIn at 2%-4% and 1%-3%, respectively. The advantage of Reddit’s niche markets and more focused communities, which may be a lot more willing to spend money, is a lot more attractive for advertisers as they get a much better bang for their buck. RDDT’s niche users skew towards higher-income, with 26% of the users earning more than $75k. These people engage in communities like r/personalfinance, which advertisers love to put their ads on due to the nature of the subreddit. Finance pays. If ARPU going from $5.88 to $9 in a year is not proof enough that these users are willing to spend, then I don’t know what is.

I believe advertisers will continue to flock to the platform going forward, as it is going to be hard to beat such numbers. When you can reach fewer people but more efficiently convert them, means you are either doing as well as on the juggernaut platforms or better, since you spent a lot less. The company is constantly improving ads platform using AI to see where it is best to put an ad that will grab the most eyes. In the most recent conference calls, the executives said that AI/ML optimizations helped boost lower-funnel performance by 20%.

Back in Early October of last year, the company’s shares slid for two days straight because, in September, ChatGPT data showed that RDDT’s content dropped to just 2% from around 10% earlier, sparking a massive panic selling. That was a bad couple of days for investors; however, recent articles have cited Reddit’s content as the top in AI search in over 20%, up to as much as 40%. So, there was no need for panic. The company’s shares promptly recovered.

Parallels to Facebook

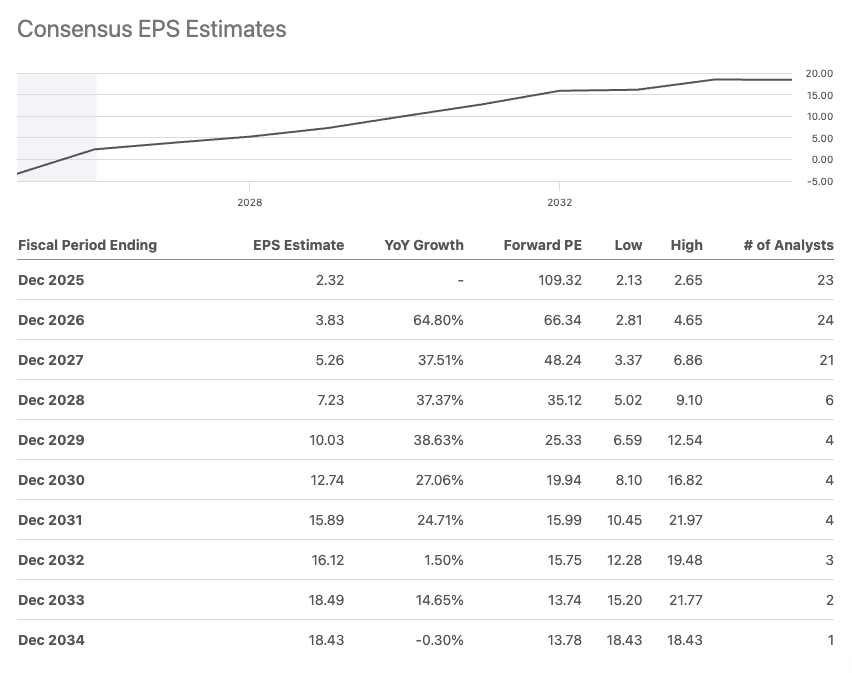

I can’t help but draw comparisons to the early Facebook days. Both leverage hyper-engaged communities to target ads and are doing it rather successfully. Right now, it seems that Reddit is trading at a massive forward P/E ratio of 109. That is expensive; however, there were times when Facebook’s P/E ratio was astronomical, too. When it IPO’ed, its P/E ratio was over 1300, as its EPS was essentially nonexistent, at around 2 cents. The following year, it dropped to 88x as its EPS went to 62 cents, and then it continued to fall, at one point during the massive scandals I remember going as low as 10x when its business continued to be a massive cash cow.

Fullratio website

I think we are seeing the same here with Reddit. Sure, a 100x P/E ratio is expensive, no doubt about it, but when you look at it from a long-term perspective, Reddit is still in its growth phase. As revenues from ads continue to grow, with minimal operating expenses to boot, the multiples will contract so quickly that these triple-digit ratios will be forgotten in an instant. Analysts are already projecting FY26 FW P/E ratio to be around 66, which will continue to fall a lot more over the following years.

Seeking Alpha

What Reddit has going for it right now that Facebook doesn’t anymore is the public’s perception of the platform. Reddit right now enjoys a lot more positive sentiment than Meta Platforms. The regulatory scrutiny, privacy scandals, and advertiser boycotts that plagued Meta for many years and continue to plague it to this day are very different from what Reddit experiences. Anywhere you look, many people say the world would be better off without Meta. The doom-scrolling on its platforms is not helping anyone, while Reddit fuels conversation so people learn from different perspectives, which is a lot more productive than the AI slop I see appearing more and more on Instagram, which is one of the main reasons I haven’t been on it in a long time. Reddit, on the other hand, I am part of the Logged in DAUq metric.

Meta is a cash cow, and will most likely remain one, and I still wouldn’t hesitate to invest in it if it drops substantially on another privacy scandal. Reddit’s just getting started.

Valuation

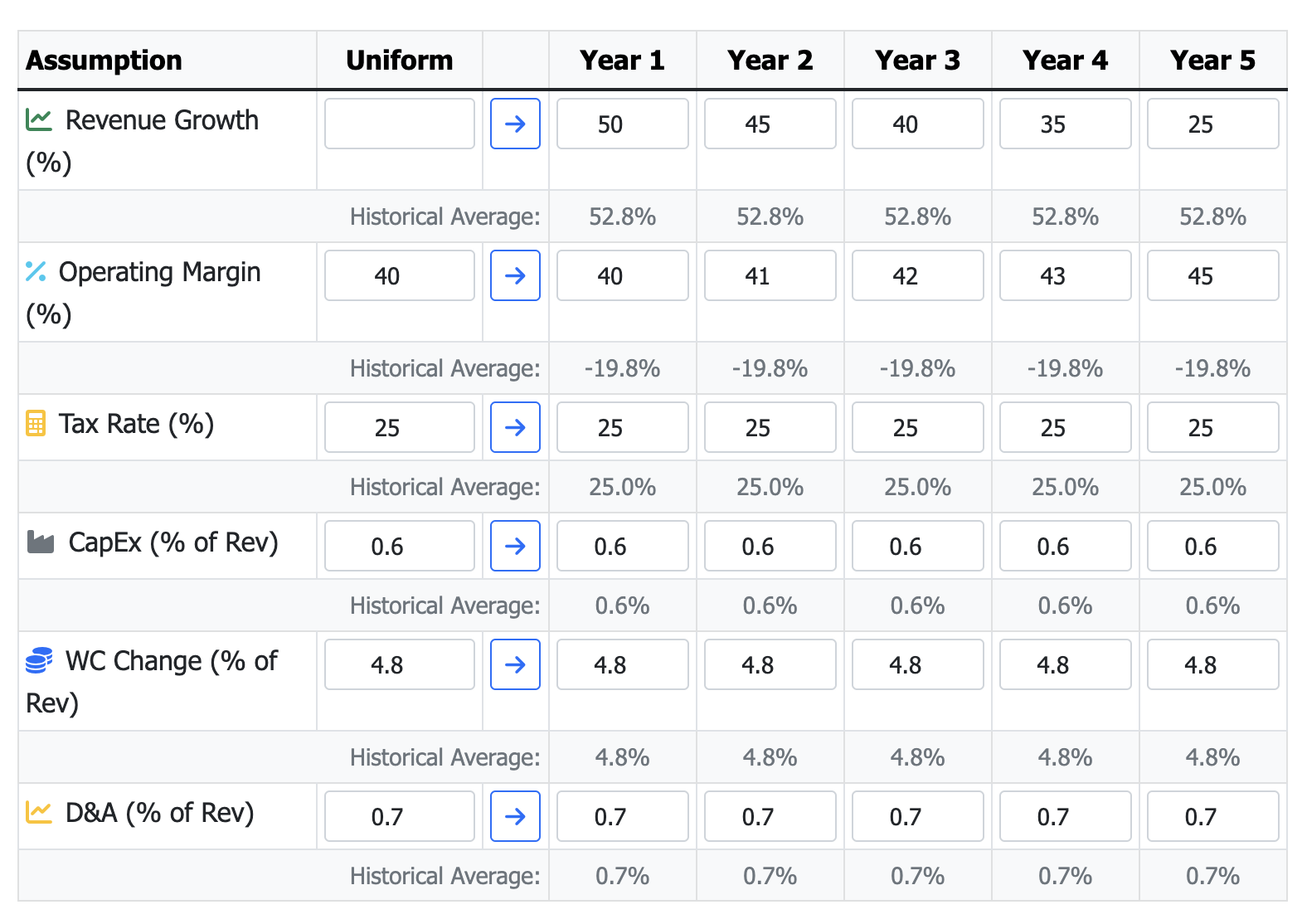

So, it is hard to model a company that is still in its what I would call a hyper growth phase, but let’s look at some quick projections for the next 5 years. Below you’ll see the assumptions I used.

Author’s Build

As you can see, these are rather optimistic. Revenue growth is very high, but I don’t think it is unreasonable given how its platform has been growing recently. Operating margins, however, are all speculation because right now, it is at around 22%, I believe, but since it is in that growth phase where margins will massively improve over time, I decided to go with what is achievable for Reddit. How do I know this is achievable? I looked at Meta’s operating margins.

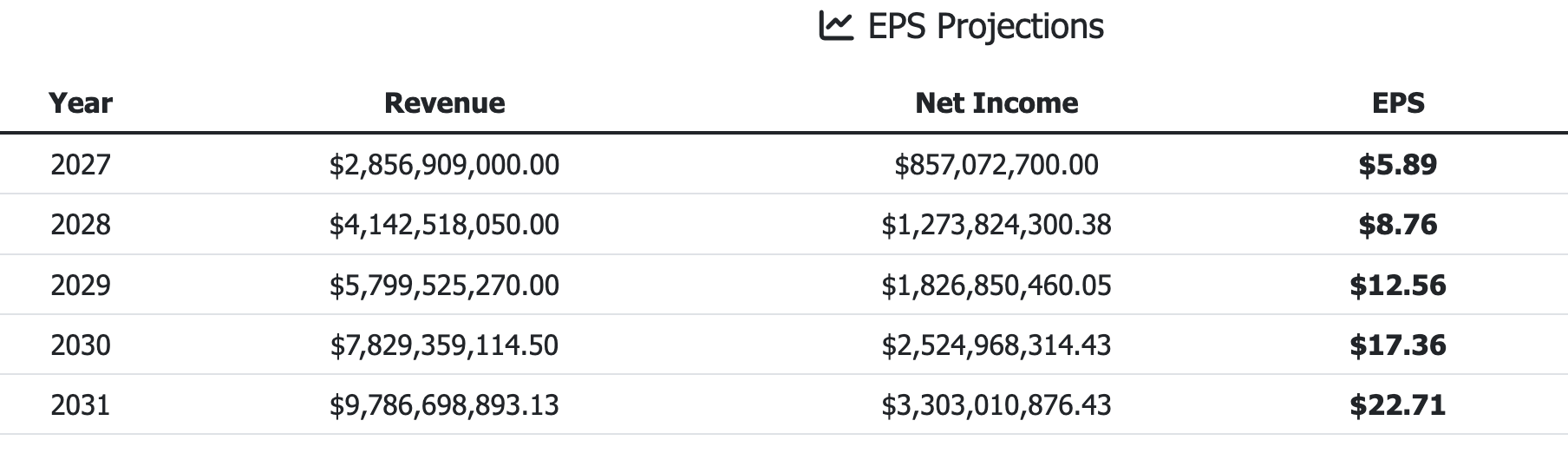

In the most recent reports, GAAP operating margins were around 40% on around 82% gross margins. These margins are also down from the highs of around 48% because Meta is spending billions on AI capex. So, it isn’t unreasonable to think that, given RDDT’s 90%+ gross margins, it cannot reach at least 40% over the long term. The company’s adjusted EBITDA margin was already at 40.3%. The rest I am fine with going with its historical averages, as well as its WACC of 8.5% is decent. With these assumptions, we get the following EPS projections.

Author’s Build

And with these projections, we get an intrinsic value of around $275 a share

Author’s Build

Risks

The assumptions on profitability may take a hit if, for some reason, growth decides to slow down significantly.

Competition for advertisers could make them leave Reddit for something that is even better at converting clicks to paid customers, leading to a slowdown in the top-line growth and a loss of operating leverage.

The company currently has quite a high short interest of around 14%, which can bring a lot of volatility, and if the company reports anything but perfection, double-digit drops in share price are not out of the question.

The platform could see some regulatory scrutiny eventually, as did Meta, which will most likely make the shares a lot cheaper.

Users could become disgruntled with the way the platform works, and moderators begin to strike if there’s a change in the algorithm that alienates users.

AI citations once again could be a major threat in the future, and since the company is dependent on advertising, another advertiser winter can impact its operations considerably.

Investor Takeaway- High Risk, High Reward

I believe the platform is going to be around for many years to come. Now that it is publicly traded, I can see the growth continuing for a much longer time. This is one of those picks that I consider high risk, high reward. I will not be going all in, but will be opening a starter position as I believe multiples will contract significantly over the next couple of years, and the company will not look this expensive. I even think such a high P/E ratio is still justified given how much growth the company has had over the last few years.

Eventually, the 90%+ gross margins will translate into much higher operating profits and bottom line. So, I am giving Reddit a Buy rating. I think it is worth the risk.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.