Investment Thesis

In my last coverage on Meta Platforms Inc. (META), I reiterated my strong buy call even in the face of a sharp rally, as I believed that the company’s ad engine fueled by AI technology had become a structural growth flywheel that could deliver increasing engagement, conversion efficiency, and advertiser ROI without increasing ad load in any meaningful way.

However, as we now see Q4 results that show increasing watch time for Reels by 30%+, ad impressions up 18%, and pricing up 6%, we now see that the investment needed to sustain this growth is rising at a rate greater than previously thought.

AI-Ad Stack Stabilizes 20%+ Revenue Growth Into 2026

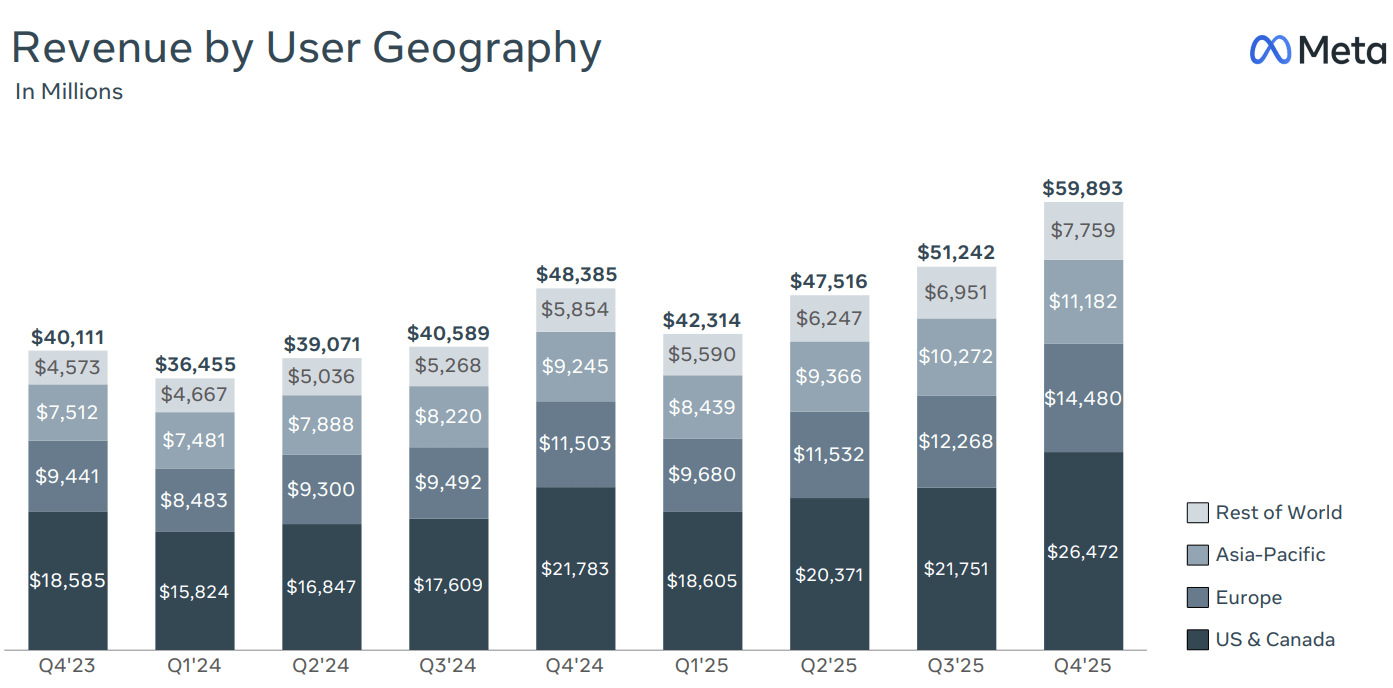

In my view, Meta possesses a highly integrated advertising ecosystem boosted by advanced AI infra. Now I see that AI integration is Meta’s main factor for business expansion. Meta is focusing on the deployment of AI models like the GEM, Andromeda, and Lattice architectures to improve content ranking, recommendation accuracy, and advertising attribution. The application of this tech directly correlates with the 24% YoY revenue increase to $59.9 billion observed in Q4 2025.

This AI tech is increasing user time on the platform and improving the conversion efficiency of advertisements. On the engagement side, Meta is using recommendation systems to surface relevant content. According to Meta’s Q4 earnings call, Instagram Reels watch time increased over 30% YoY in the US, and Facebook video time grew by double digits. Through retaining user attention for longer times, Meta is expanding the inventory of sellable ad impressions. Q4 points to an 18% increase in ad impressions served across services.

Q4 Earnings

Moreover, I think this expansion of inventory provides a larger surface area for monetization without necessitating an aggressive increase in ad load that might degrade user experience. Simultaneously, Meta applies these AI models to the advertising stack to increase the value of each impression. There is a doubling of GPU clusters used to train the GEM model for ads ranking. As I see, Meta recorded a 3.5% YoY lift in ad clicks on Facebook and a gain of more than 1% in conversions on Instagram during the quarter.

Furthermore, the implementation of the new runtime model for Instagram Feed, Stories, and Reels resulted in an improvement of 3% in the conversion rates. This technology upgrade helps advertisers receive better returns on ad spend. I believe advertisers experience better performance and demand for inventory rises. This led to a 6% YoY increase in the average price per ad.

I expect the impact of these tech improvements to extend beyond core ad delivery into the creative content generation. Meta’s video generation tools have now hit a $10 billion annual revenue run rate in Q4. These tools utilize gen AI to assist advertisers in producing creative assets. The incremental attribution feature that optimizes for conversions in real-time drove a 24% increase in incremental conversions compared to standard models.

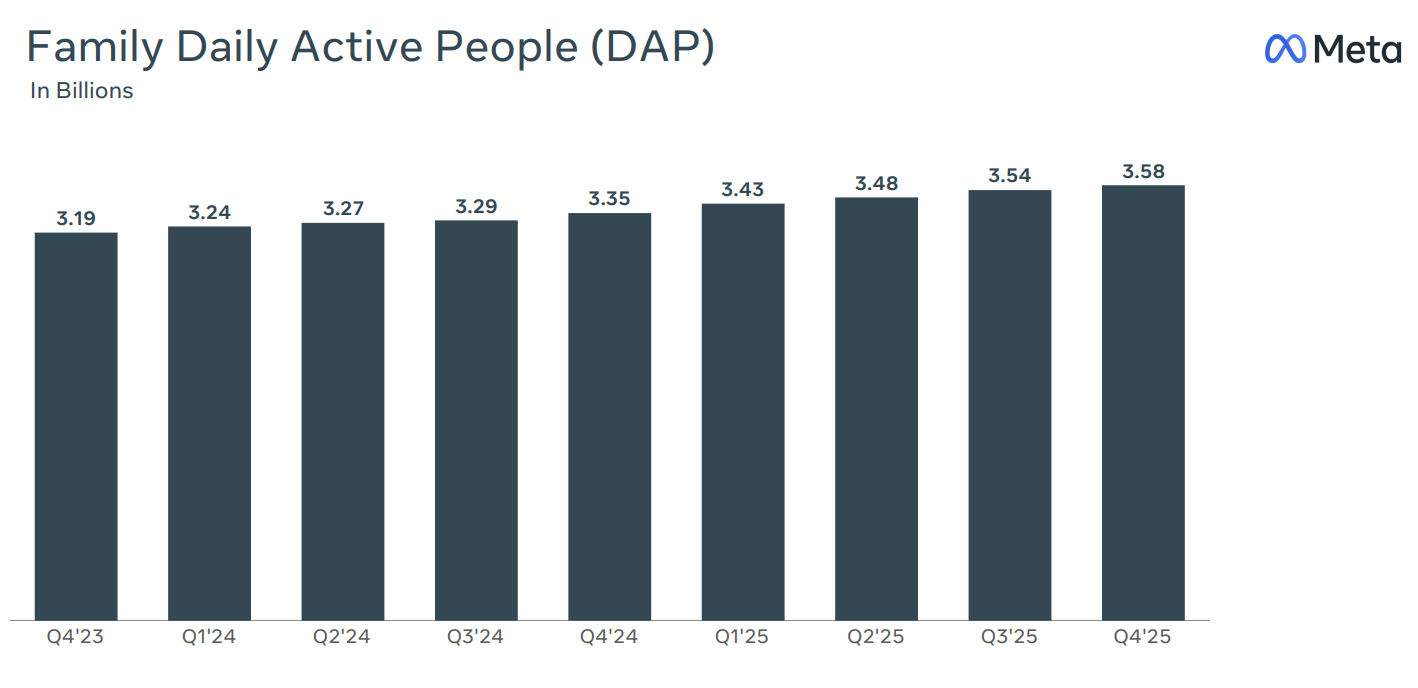

This product alone hit a multi-billion dollar annual run rate within seven months of launch. Furthermore, as Meta invests in infrastructure, the models become more accurate by time. According to Meta’s earnings presentation, higher accuracy leads to better content recommendations and is increasing Daily Active People (DAP) that is currently at 3.58 billion. Larger user bases and longer session times generate more data and further refining the models.

Q4 Earnings

If we look forward to 2026, the guidance projects that Q1 revenue will be between $53.5 billion and $56.5 billion. This, again, is dependent on the effectiveness of these integrations. Meta is planning to scale the GEM training to larger clusters and incorporate LLMs to hold grip content semantics more in-depth. Also, amid aggressive CapEx, the core advertising business derives large cash from operations of $115.8 billion in 2025. Thus, these tech advancements are self-sustainable.

Meta’s $115–$135 Billion 2026 CapEx Puts Margins and FCF at Risk

The biggest risk to Meta is the increase in infrastructure costs and the associated CapEx to support its AI initiatives. This risk, in turn, increases as the huge increase in fixed costs and capital outflows can create a high threshold for ROI on the company’s FCF. Q4 results point to this trend with total costs and expenses rising 40% YoY to $35.1 billion outpacing revenue growth of 24%. This expense is a permanent shift in Meta’s operating model by Meta.

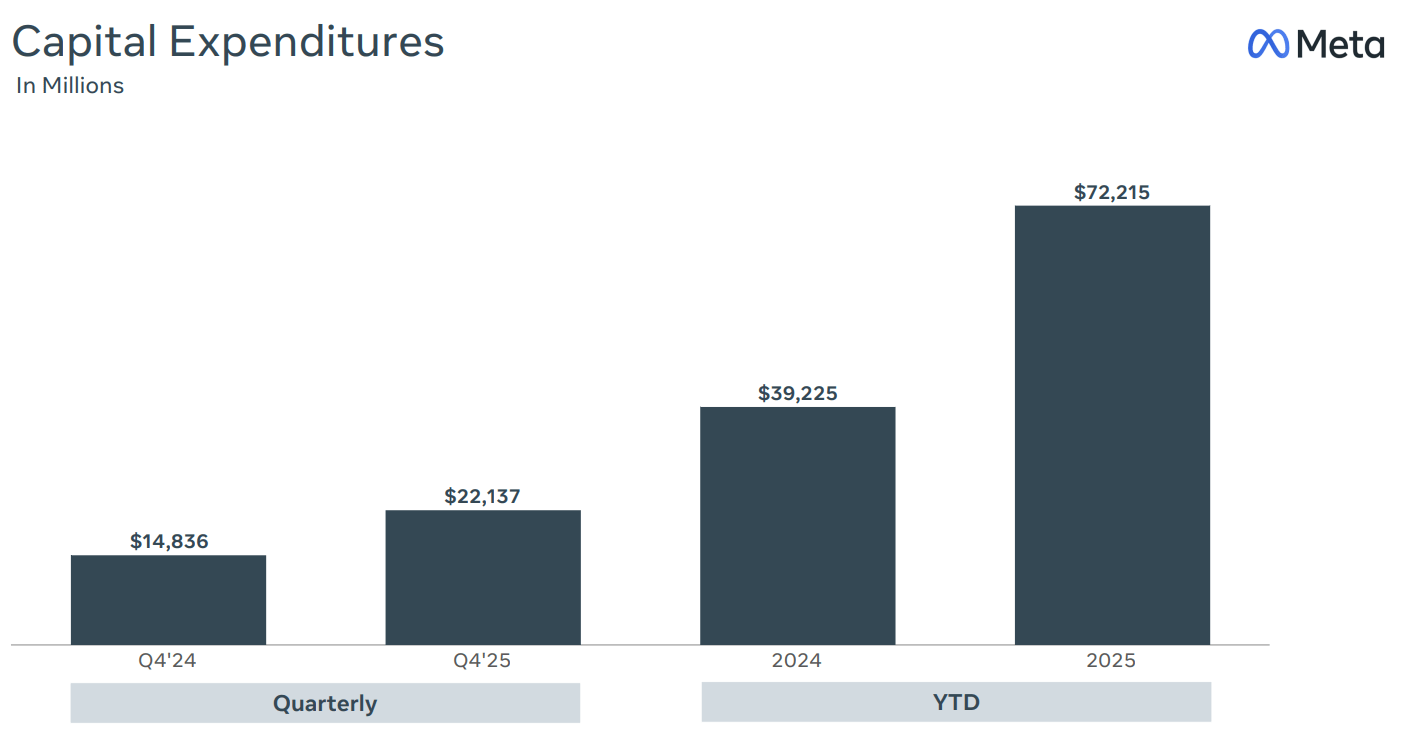

The outlook for 2026 projects total expenses in the range of $162 billion-$169 billion. This outlook focuses on infra costs that include depreciation, third-party cloud spending, and OpEx linked to data centers. The CapEx guidance for 2026 stands between $115 billion-$135 billion that is a large increase from the $22.1 billion Q4 run rate and the $72.2 billion total for 2025. Such a level of capital intensity alters the FCF profile.

Q4 Earnings

The immediate impact of this spending on Levered FCF growth declined on a YoY basis by 51.48%. Forward FCF per Share growth is negative at -17.84%. The projected CapEx for 2026 threatens to consume the majority of operating cash flow. Data centers and GPU clusters represent high fixed costs. If revenue growth decelerates due to macro headwinds and competitive pressures, these costs remain on the ledger and these may lead to rapid margin contraction.

The operating margin in Q4 already compressed to 41% from 48% YoY. Outlook for 2026 assumes that operating income will exceed 2025 levels and yet this depends entirely on revenue growing fast enough to absorb the $162 billion to $169 billion expense load. Any shortfall in the topline may result in a negative leverage effect on the bottomline.

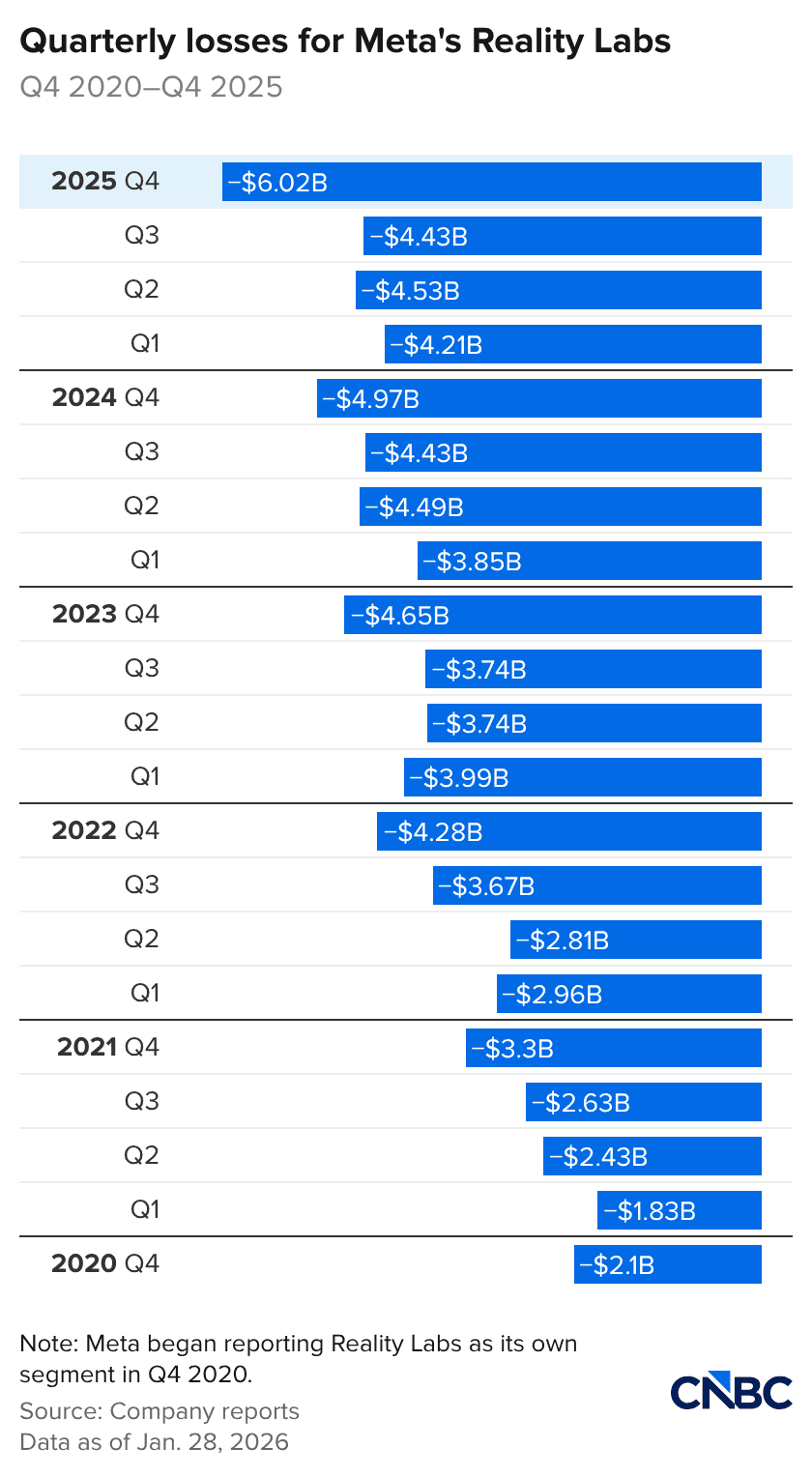

Furthermore, in my view, the Reality Labs segment continues to act as a capital drain without any profitability. Revenue for Reality Labs declined 12% in Q4 to $955 million due to lapping prior launches. Reality Labs’ operating losses in 2026 will remain similar to 2025 levels.

In this case, the management is pouring investment into glasses and wearables. However, the period within which glasses and wearables will make a profit remains uncertain. This business requires continued investment from the ad business profitability, which adds pressure to the overall margins.

Moreover, compute capacity cappings add more layers to this risk. As per the CFO, Meta will remain constrained through most of 2026 on compute resources. To hit on this issue, Meta may utilize third-party cloud providers and incurring higher marginal costs compared to owned infra. This reliance on external cloud capacity is a margin headwind until internal facilities come online.

CNBC

Finally, regulatory and legal risks boost this financial risk. I see continued legal and regulatory headwinds in the EU and the US. Mainly, scrutiny regarding youth-related issues in the US involves scheduled trials that may result in a material business loss. Any substantial financial penalty and restriction may further deplete cash reserves at a time when liquidity is vital for funding the $135 billion upper-end CapEx projection.

Also, the transition to Less Personalized Ads in the European Union injects topline risk. This rollout may reduce the efficacy of the advertising engine in that region and create a topline headwind. If the efficiency of the ads business declines in a major market, the ROI on the massive infra investment deteriorates.

Takeaway

Meta’s investments in AI technology have already led to increased engagement, ad efficiency, and price increases. While spending heavily, Meta’s ad engine growth is accelerating and funding its own infrastructure build-out. As long as returns from advertisers continue to increase with the help of AI, the high growth rate of more than 20% can be sustained by Meta.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.