I previously covered Palantir Technologies Inc. (PLTR) (PLTR:CA) in November 2025, discussing its robust AI monetization prospects and its highly strategic partnership with Nvidia (NVDA) during an ongoing AI boom.

Despite the double-beat FQ3’25 performance and the raised FY2025 guidance, the notable divergence between the stock’s outsized rally/overly expensive valuations and the decelerating growth profile/underwhelming consensus forward estimates had triggered risks to its investment thesis, as observed in the post-earnings correction, resulting in my reiterated Hold rating then.

In this article, I shall discuss why I am reiterating my Hold rating for the PLTR stock here, despite the dip-buying opportunity arising from the recent ‘Software Armageddon‘ meltdown and their robust profitable growth trends as observed in the FQ4’25 outperformance/promising FY2026 guidance.

My caution is attributed to the potential capital losses from the stock’s still expensive valuations and the volatility from the higher beta coefficient notably negating its high growth, SaaS investment thesis.

PLTR Proves Its AI Beneficiary Status

PLTR 1Y Stock Price (TradingView)

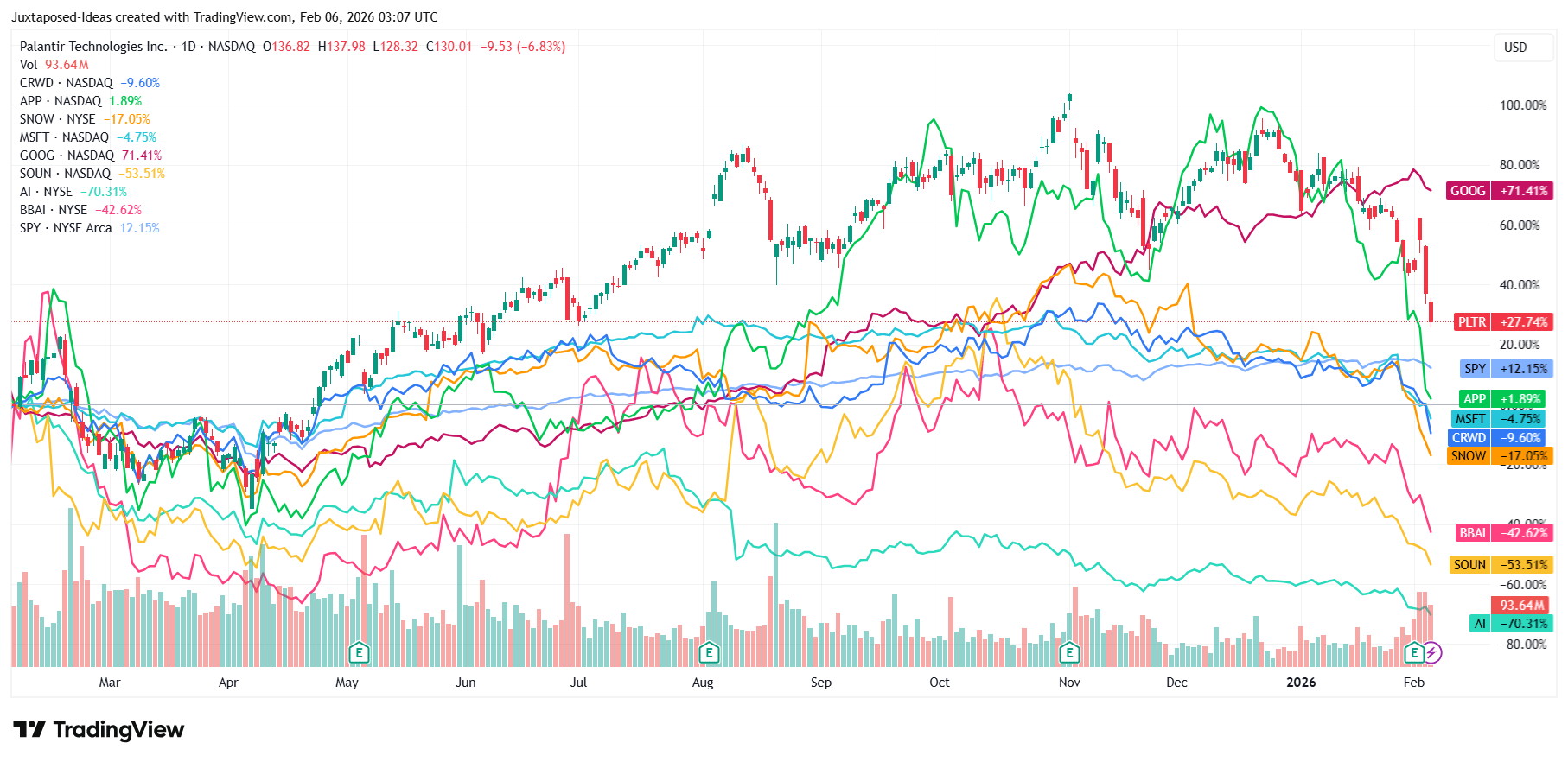

Since my last Hold rating, PLTR has indeed deeply retraced as posited in the third potential outcome discussed in my last article, with the stock already losing -37.3% of its value since the 52-week highs.

Part of the pessimism may be warranted after all, with the market seemingly concerned about their SaaS growth headwinds “if artificial intelligence improves productivity but results in the elimination of jobs.”

This is worsened by the AI tool seemingly making “some SaaS tools less important” as “many of these software products analyze and draw connections between data sets, help businesses manage their workflow, and generate reports. AI firms are increasingly developing and selling tools that perform similar tasks without the need for a dedicated platform.”

These are valid fears indeed, since it may negate PLTR’s Foundry Subscription business at a monthly rate of $100K per unit and an overage of $50K per unit, with it perhaps explaining the deep selloff as similarly observed in its AI SaaS peers in varying degrees.

Thanks to the selloff, the stock has finally experienced a much needed moderation in its (still expensive) FWD P/E valuations from the recent highs of 270.28x to 105.58x by the time of writing – with it lending credibility to my prior caution.

Otherwise, it goes without saying that PLTR continues to report robust performance metrics in the FQ4’25 earnings call, with the excellent revenue growth to $1.4B (+69.9% YoY) accelerating against the FY2025 levels of $4.47B (+56.2% YoY).

Much of the tailwinds are attributed to the robust US commercial revenue growth to $507M in FQ4’25 (+136.9% YoY) and the growing US commercial Remaining Deal Value [RDV] of $4.38B (+245% YoY), as “AIP continues to fundamentally transform how quickly our customers realize value, collapsing the time from initial engagement to transformational impact.”

At a time of increasingly volatile geopolitical environment, PLTR has also benefitted from the robust defense spending as observed in the US defense revenue growth to $570M in FQ4’25 (+17.2% QoQ/+66.1% YoY) and the overall defense revenue growth to $730M (+15.3% QoQ/+60.4% YoY).

This is an impressive development indeed, despite the prior government shutdown lasting from October 1, 2025 through November 12, 2025, with the robust US defense revenue growth building upon those observed in FQ3’25 by +14% QoQ/+52% YoY while directly contrasting against some of its AI SaaS peers’ impacted revenue trends.

These developments underscore PLTR’s great success in displacing competitors, with the company notably emerging as a winner during the ongoing AI SaaS consolidation, as similarly highlighted by an executive from Thomas Cavanagh Construction:

We’ve gone all in so much so that every other software must justify its existence. And so far, they haven’t been able to. 97% of our employees use Foundry every day. Foundry is our operating system…

The Ontology is the secret weapon. Nothing else comes close. And not only are we getting rid of third-party software, we’ve replaced their functionality and then beaten them to new features all within the year because of the Ontology. (Seeking Alpha)

Combined with the growing customer count by +34% YoY and the expanding Net Dollar Retention of 139% in FQ4’25 (+19 points YoY), it is unsurprising that PLTR has reported an improved operating leverage at Rule of 127% performance (+46 points YoY, arising from FY2025 revenue growth by +70% YoY and adj operating margin of 57%).

This is on top of the SaaS company’s richer Free Cash Flow generation at margins of 51% in FY2025 (+7 points YoY), with it directly contributing to the richer balance sheet at a cash position of $7.17B (+37.3% YoY).

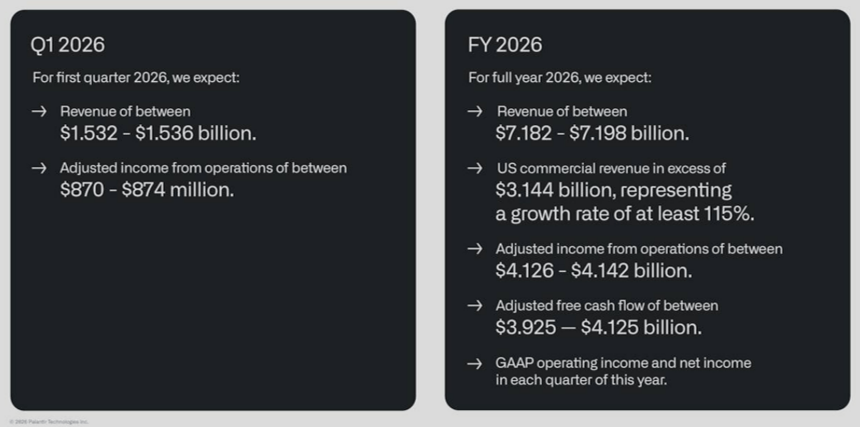

PLTR’s Guidance (PLTR)

For now, PLTR has already offered an ambitious FY2026 revenue guidance of $7.19B at the midpoint (+60.8% YoY), with it well outperforming the FY2025 growth profile at +56.2% YoY and the historical growth profile at a 5Y CAGR of +32.6%.

Based on the richer FY2025 adj. net income margins of 42.7% (+7.8 points YoY) and the last shares outstanding of 2.57B, I am estimating an outsized FY2026 adj. net income of $3.07B (+60.7% YoY) and adj. EPS of $1.19 as well (+58.6% YoY) – with it apparent that the SaaS company remains a key beneficiary of the ongoing AI boom, despite the recent market fears of a ‘SaaS apocalypse.’

The Consensus Forward Estimates (Seeking Alpha)

If anything, based on the current consensus, FY2026 adj. EPS growth estimates of +76.2% YoY, it is apparent that the market is pricing further beat and raise performances over the next few quarters.

The same has been similarly observed in the thrice-raised FY2025 guidance in prior earnings calls and the historical double beat performances over the past consecutive ten quarters, with it hinting at further outperformance despite the tougher comparison from FY2025’s already explosive growth profile.

This development implies that PLTR’s recent meltdown is seemingly sentiment driven arising from its lofty valuations, despite the robust fundamentals arising from the profitable growth prospects and the healthier balance sheet.

PLTR Remains A Hold Here

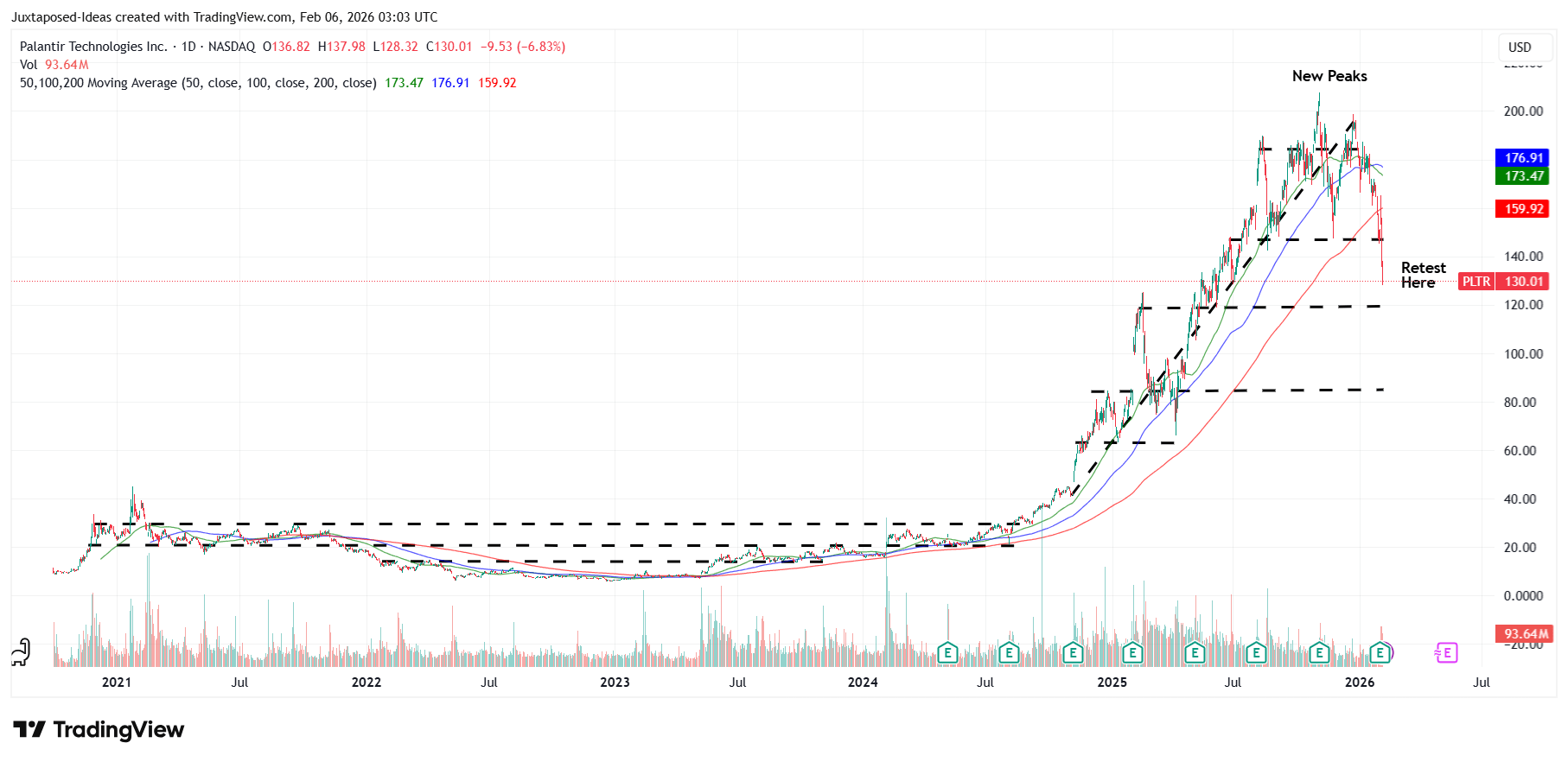

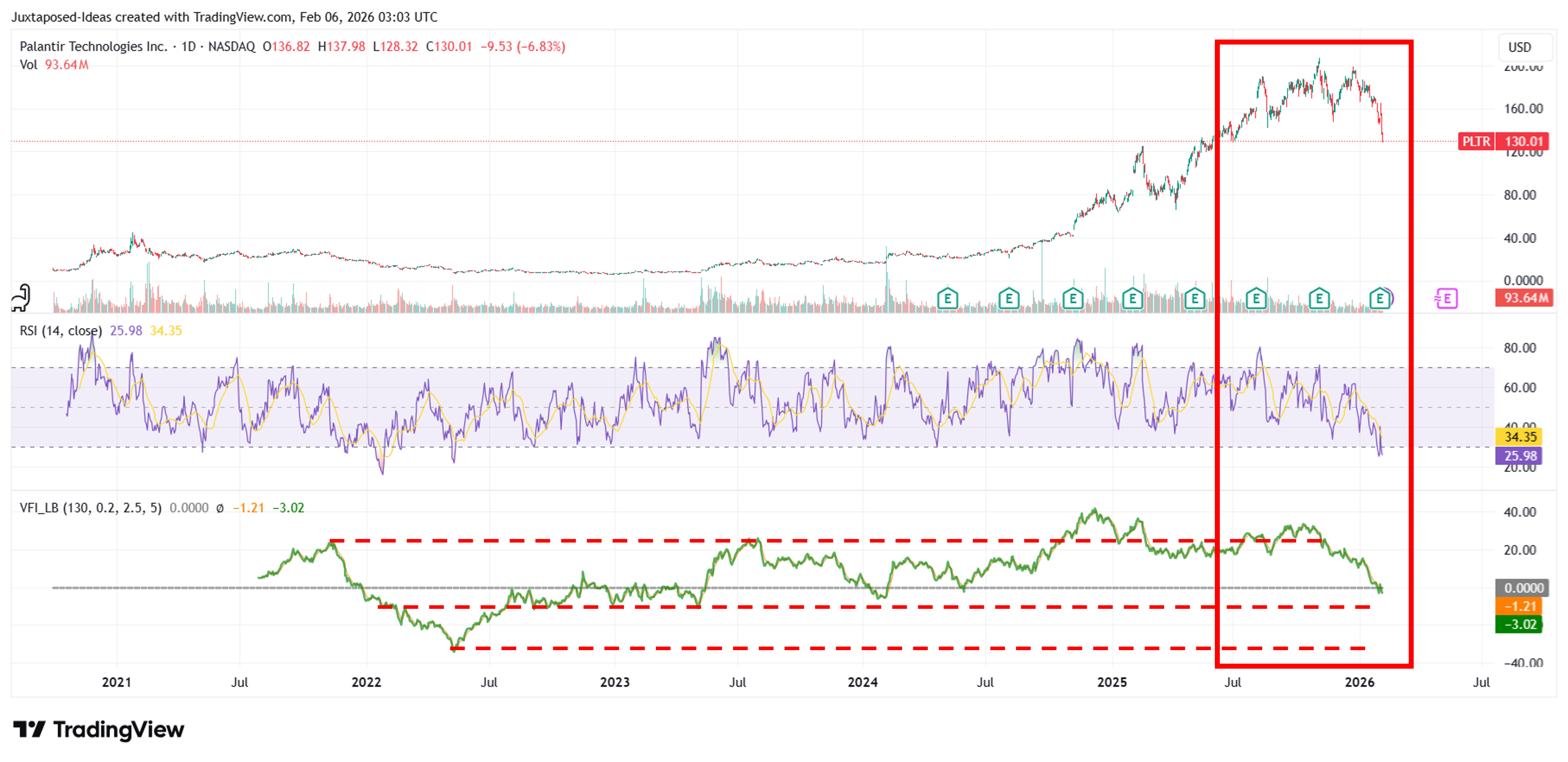

PLTR 5Y Stock Price (TradingView)

For now, PLTR has notably lost most of its H2’25 gains, with the stock also breaching numerous support levels and the 50/100/200 day moving averages by the time of writing.

PLTR Technical Indicators (TradingView)

It is unsurprising, then, that PLTR has also entered oversold territories by the time of writing, as similarly observed in the moderating RSIs and trading volumes, with it remaining to be seen when the bulls may defend a floor as the market-wide sell off continues.

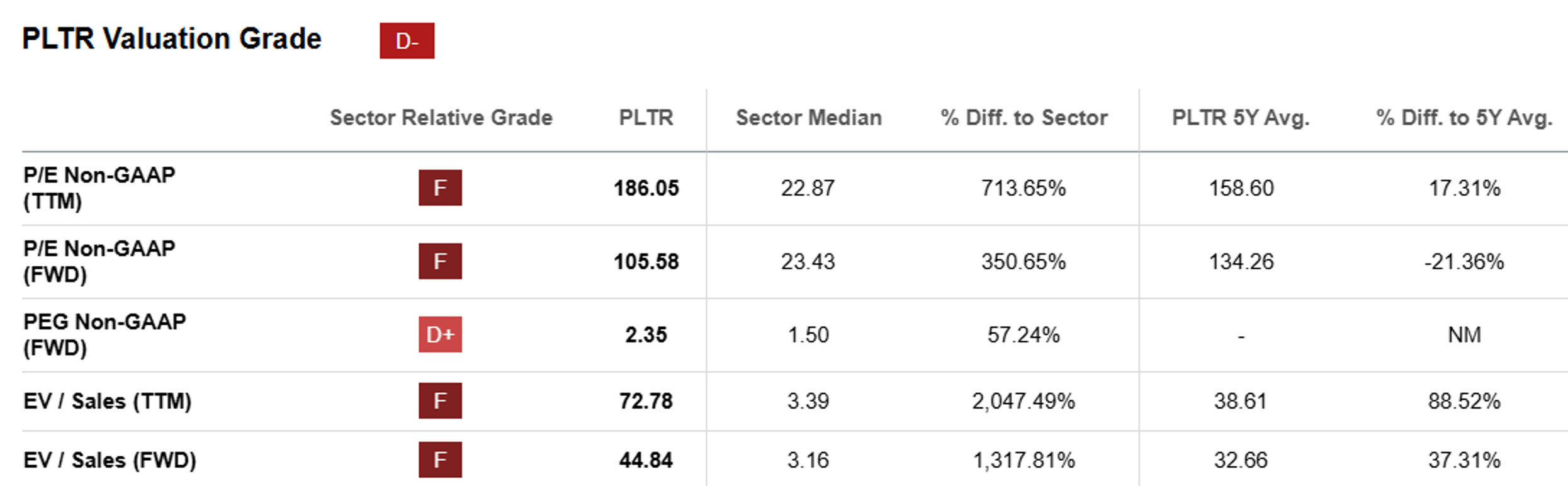

PLTR Valuations (Seeking Alpha)

On the one hand, thanks to the ongoing meltdown, PLTR appears more compelling at my estimated 3Y PEG non-GAAP ratio of 2.10x, based on the consensus adj EPS growth estimates at a 3Y CAGR of +50.1% and the FWD P/E non-GAAP valuations of 105.58x.

This is down from the recent PEG highs of 5.39x and the 5Y mean of 4.18x, while nearing the sector median of 1.50x, with the steep correction seemingly triggering a great dip buying opportunity.

On the other hand, it goes without saying that PLTR remains rather expensive at FWD EV/Sales valuations of 44.84x based on the Rule of 127% performance, with a similar conclusion also derived when comparing it to its direct AI SaaS peers, including:

- enterprise/federal focus – C3.ai (AI) at 3.18x/-87% (YTD revenue decline by -19% and YTD adj. operating margins of -68%)

- conversational call center/customer service focus – SoundHound AI (SOUN) at 18.66x/70% (YTD revenue growth by +127% YoY and YTD operating margins of -57%),

- federal focus – BigBear.ai Holdings, Inc. (BBAI) at 11.15x/-144% (YTD revenue decline by -12% YoY and YTD operating margins of -132%),

- enterprise data analysis/workflow focus – Snowflake (SNOW) at 11.78x/38% (YTD revenue growth by +28% YoY and YTD adj. operating margins of 10%),

- cloud computing/enterprise focus – Alphabet (GOOGL) (GOOG) at 8.53x/47% (FY2025 revenue growth by +15% YoY and FY2025 operating margins of 32%),

- cybersecurity focus – CrowdStrike (CRWD) at 20.97x/42% (YTD revenue growth of +21% and YTD adj. operating margins of 21%), and

- customer relationship management focus – Salesforce (CRM) at 4.51x/42% (YTD revenue growth of +8% and YTD adj. operating margins of 34%), respectively,

with it apparent that PLTR presents a mixed investment thesis at current levels, worsened by the ongoing market noise surrounding the ‘SaaS apocalypse.’

Does this mean that I am reiterating my Hold rating for the PLTR stock here?

Yes indeed, since the growth premium embedded in PLTR’s stock prices/valuations already priced in the SaaS company’s high double-digit, profitable growth trends over the next few years – as similarly observed in my estimated FY2028 P/E valuation of ~41x (still expensive compared to the sector median of ~23x).

These present the stock’s potential dead money investment thesis, if not further capital losses, assuming the deterioration in its performance metrics and/or the maturing of its growth prospects, as observed in the consensus decelerating forward estimate growth from FY2027 onwards.

If anything, PLTR’s underwhelming price performance over the past seven months already demonstrates the inherent capital loss risks associated with chasing overpriced stocks.

Barring a further correction to the P/E levels of ~75x (to emerge near the sector PEG median of 1.50x), I am of the opinion that there remains a minimal margin of safety at current levels, worsened by the potential volatility arising from the beta coefficient of 2.23x.

Given the estimated -29% downside from current levels, I believe that a Hold (Neutral) rating is appropriate for PLTR here.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.