2026 has been a surprisingly volatile year for high-flying growth stocks, with investors now treating AI as a net risk rather than a tailwind. The S&P 500 has managed to cling close to all-time highs, but that has been buoyed by traditional companies in the energy and materials sectors. Many software and internet companies, meanwhile, are in deep bear market territory.

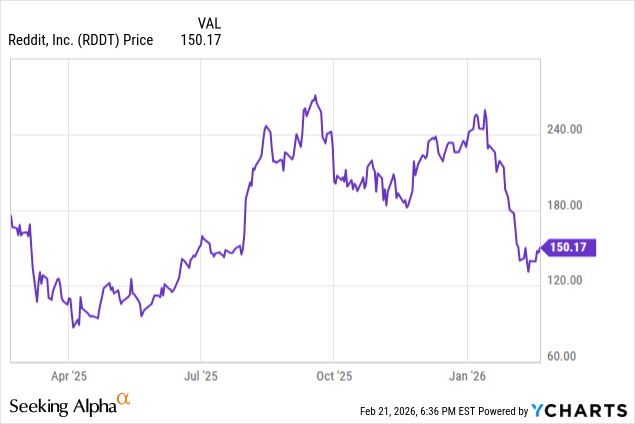

While I certainly agree that Reddit (RDDT) had some valuation premium that it needed to burn, we have to ask ourselves now: with Reddit down nearly 40% since the start of January alone, at what point can we declare that the stock is oversold? The company also just released incredibly strong Q4 results that featured not only acceleration in revenue but also a continued pickup in U.S. users; nevertheless, shares remain stubbornly in correction territory.

I last wrote a buy rating on Reddit in November, when the stock was trading just under $210 per share. Reddit’s fall to the $150s doesn’t faze me; in fact, it’s a fantastic opportunity for me to add to my position and dollar-cost average my cost basis downward. The company has continued to make terrific product improvements that are clearly having an impact on not only user acquisition but also boosted engagement as well. I’m reiterating my buy rating here and encouraging investors to add on this dip.

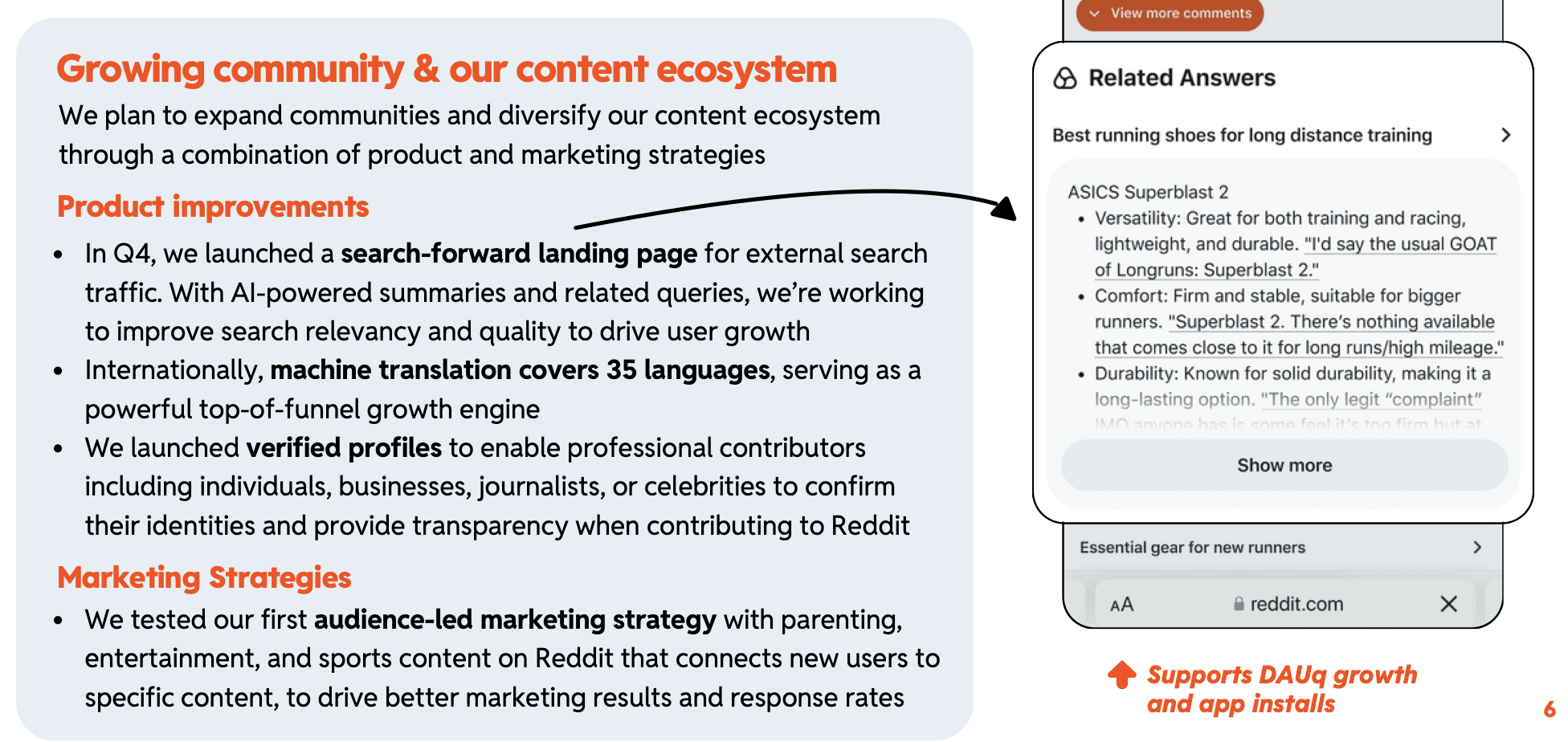

The first catalyst that investors should be aware of is the fact that Reddit is making consistent product improvements that are yielding strong results. In the fourth quarter, Reddit revamped its platform to make it more search-forward. In the age of AI chatbots, users are now becoming used to beginning all of their web experiences with a search query. A platform’s ability to serve the user with relevant content is the prime test of whether that user will be retained.

Reddit product updates (Reddit Q4 shareholder letter)

Other updates are aimed at improving the Reddit experience. The company is launching verified profiles for celebrities and experts to confirm their identities when providing insights, similar to X/Twitter. The company’s machine translation efforts have also expanded to 35 languages, now making Reddit content more accessible globally and a major catalyst for international DAU expansion. The company has also launched a new lower-funnel ads product called Reddit Max campaigns, which is boasting higher conversion rates and lower cost per click for advertisers.

We note that amid all of Reddit’s improvements (which are driving strong revenue and user trends, discussed in more detail in the next section), the stock’s recent crash has positioned its valuation far more favorably.

At current share prices near $150, Reddit trades at a market cap of $28.69 billion. Netting off the $2.48 billion of cash (against zero debt) on Reddit’s most recent balance sheet gives us an enterprise value of $26.21 billion.

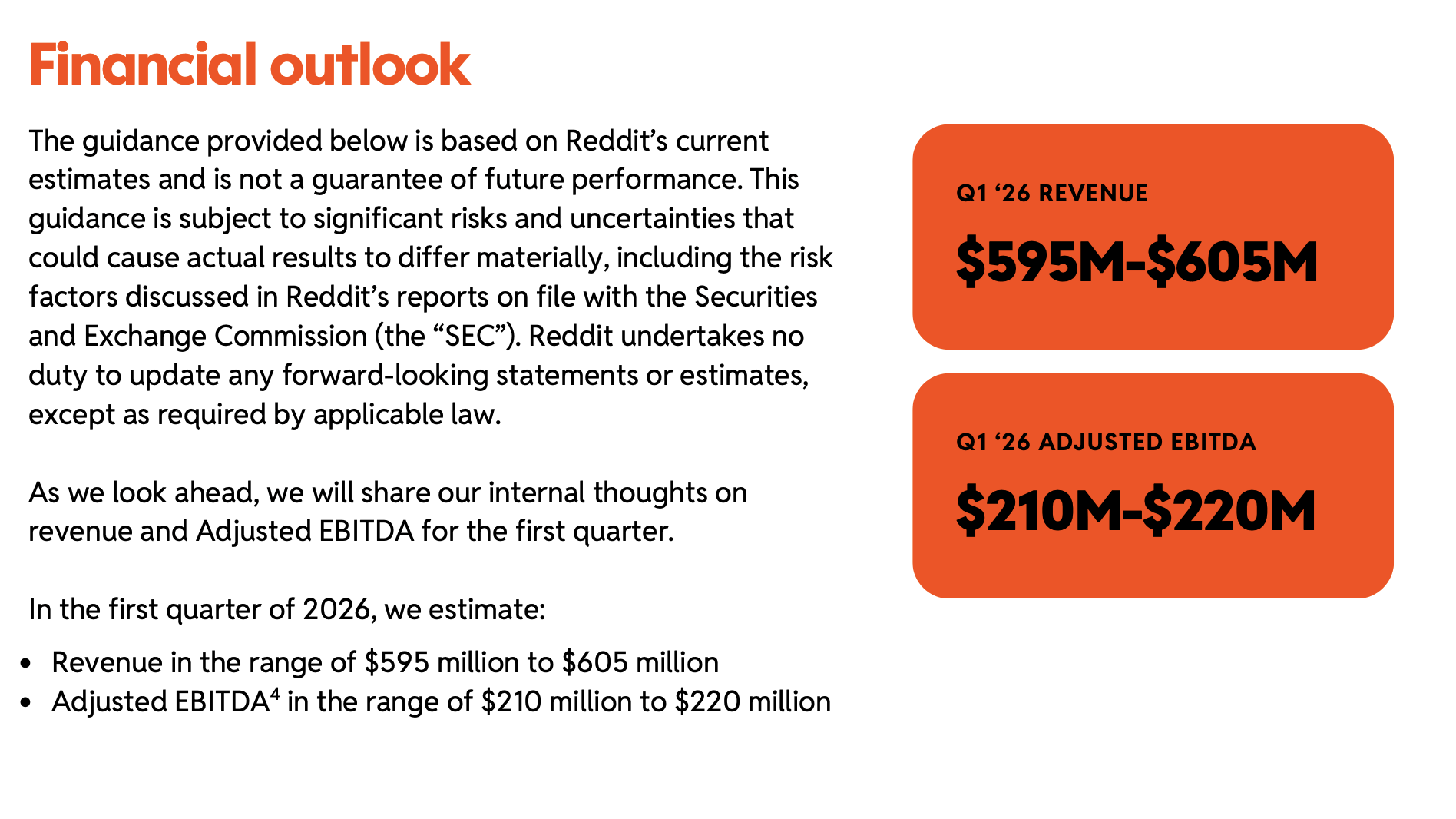

Reddit only guides one quarter out at a time, but for Q1, the company has guided to $595-$605 million in revenue, the midpoint of which reflects 53% y/y revenue growth (note that we take Reddit’s top-line guidance with a grain of salt, as the company usually beats its ranges significantly, as Q4 demonstrates). It’s also calling for a midpoint adjusted EBITDA of $215 million, or a 35.8% margin that’s up 640bps y/y versus 29.4% in Q1’25.

Reddit Q1 outlook (Reddit Q4 shareholder letter)

For the full year FY26, Wall Street is expecting Reddit to hit $3.15 billion in revenue, or 43% y/y growth. If we assume a ~6 point increase to full-year adjusted EBITDA margins (to 44.4%), in line with the company’s Q1 guide, the company’s full-year adjusted EBITDA would be $1.40 billion (+66% y/y). This would also be in line with historical profit seasonality: in FY25, Q1 adjusted EBITDA of $115 million contributed 14% of full-year EBITDA of $845 million.

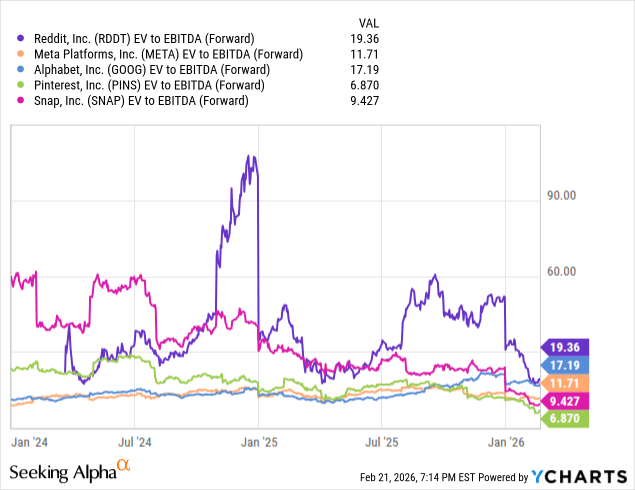

Using these assumptions, Reddit trades at 18.7x EV/FY26 adjusted EBITDA. The correction has sharply dented Reddit’s premiums to a very buyable level: a high teens adjusted EBITDA multiple, in my view, is quite a deal for a company that is currently growing revenue at a ~70% clip and adjusted EBITDA at >2x y/y. Yes, we note that Reddit trades at a premium to other social media/internet stocks, but its growth profile will allow the company to grow quite easily into its multiples:

Stay long here and use the dip as a buying opportunity.

Q4 Download

Let’s now go through Reddit’s latest quarterly results in greater detail. The Q4 earnings summary is shown below:

Reddit Q4 results (Reddit Q4 shareholder letter)

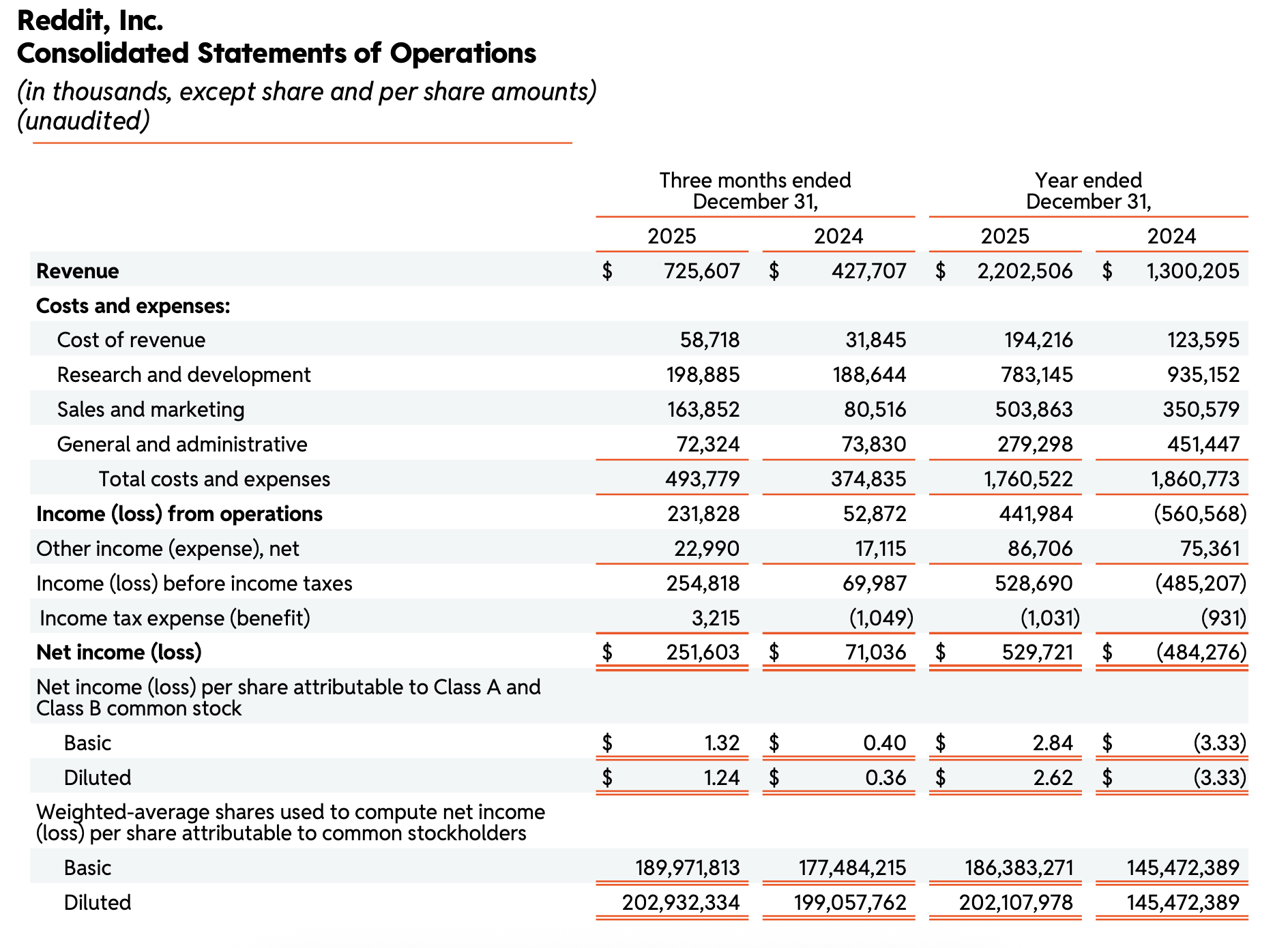

Reddit’s revenue grew 70% y/y to $725.6 million, beating Wall Street’s expectations of $667.1 million (+56% y/y) by a huge fourteen-point margin. Revenue growth also accelerated slightly versus 68% y/y growth in Q3.

Growth was fueled by both user growth as well as increased penetration of ad revenue. The company’s daily active user counts rose to 121.4 million, adding 5.4 million net-new DAUs in the quarter and growing 19% y/y. We think it’s meaningful as well to note that U.S. user counts grew by 0.9 million sequentially. Earlier in the year, particularly after the company’s Q4’24 earnings print, in which U.S. users temporarily dipped by 0.2 million due to a periodic change in Google search traffic, investors had worried that Reddit had reached a saturation point in the U.S. Evidently, the company’s slew of product updates, plus its clear differentiation against other social media platforms, has helped Reddit to continue building its domestic audience.

Reddit DAU trends (Reddit Q4 shareholder letter)

Meanwhile, machine translation is also opening up Reddit to more users overseas, helping to add 4.5 million net-new international DAUs sequentially.

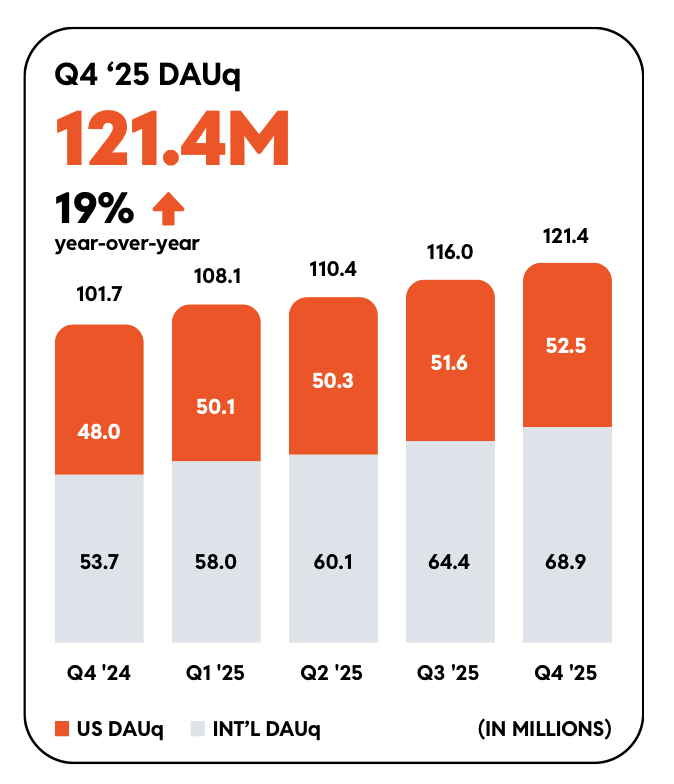

Meanwhile, average revenue per user is also skyrocketing. Total ARPU rose 42% y/y to $5.98, with the U.S. growing 53% y/y to $10.79 thanks to the launch of more campaign options like Reddit Max.

Reddit ARPU trends (Reddit Q4 shareholder letter)

Importantly, management notes that it’s overall growth in impressions (ad views) that drove revenue growth, which is an important signal of strong user engagement. Per CFO Jennifer Wong’s remarks on the Q4 earnings call:

Four revenue drivers fueled our growth. First, performance ads outperformed and revenue from lower funnel objectives such as purchase conversions and app installs doubled year-over-year, as we see the benefits of our investments in ML and new ad formats like shopping ads start to pay off. Second, we saw strength across channels with year-over-year growth ranging from mid- to high double digits within both our large customer segment and scaled segment, which includes mid-market SMBs. SMB revenue doubled year-over-year. Third, we saw broad strength across verticals. 11 out of our top 15 verticals grew revenue by 50% or more year-over-year, led by retail, pharma, financial services and tech. And fourth, we saw strength across geographies. U.S. revenue grew 68% and international revenue grew 78% year-over-year.

Our ML and signals optimization efforts are making every impression work harder. In Q4, impression growth was the main driver of revenue growth, while pricing grew year-over-year as we delivered more outcomes and efficiency for advertisers. We also continue to expand our advertiser base. Total active advertiser count grew by over 75% year-over-year in Q4 as we added new accounts across all channels, including large, mid-market and SMBs.”

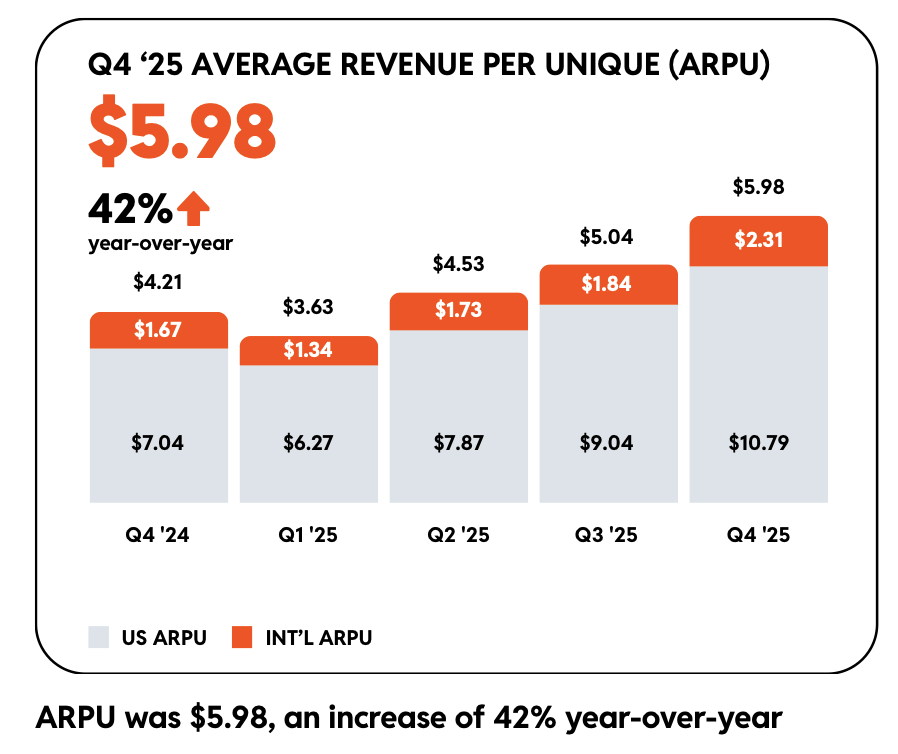

On the cost front, we note that pro forma operating expenses (excluding stock comp) rose only 41% y/y to $340.1 million despite 70% revenue growth (and we also note that with deflating share prices, stock comp was also down -6% y/y, which should provide relief for investors worried about dilution). This has helped Reddit drive adjusted EBITDA of $327.0 million, up 112% y/y, and hit a 45.1% margin that improved 9 points y/y.

Reddit adjusted EBITDA (Reddit Q4 shareholder letter)

Risks and Key Takeaways

Of course, we should be aware of the risks that Reddit faces as well. A growing number of countries are proposing or have already implemented social media bans for under-16s, which could reduce traffic from younger users for Reddit. We note as well that a weaker macroeconomy and tepid consumer spending could put a dent in ad budgets, and lower ad pricing, which will have an offsetting impact against recent impressions growth trends.

That said, I think Reddit’s tailwinds far outweigh its risks, especially at a more reasonable ~18x forward adjusted EBITDA multiple. Stay long here and buy the dip.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.