The Indian GDP growth normal has to be in the 8-9% category; it is only at that pace that you can get rid of poverty. – Arun Jaitley

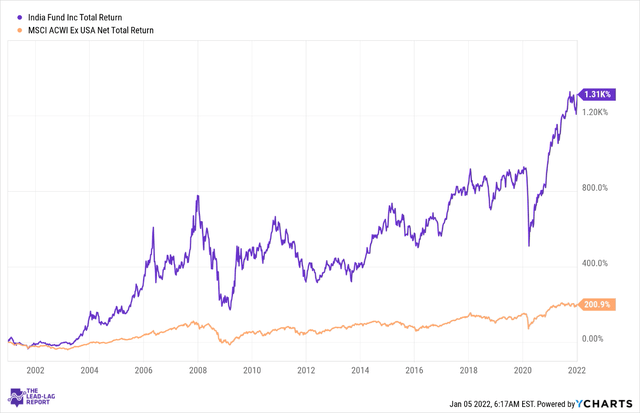

Aberdeen Asset Management’s India Fund (IFN) is one of the most prominent investment products around offering access to one of the fastest-growing, if not the fastest-growing, major economies in the world. The fund has been around for a long time, nearly 28 years, and has been a very dependable source of alpha-generation; over the last two decades it has comfortably outperformed the MSCI ACWI ex USA Index – a global index that covers over 2,300 large and mid-cap stocks from 49 International markets (comprised of 22 Developed markets and 27 Emerging markets).

Source: YCharts

Indian GDP

According to the IMF, India would likely have finished 2021 delivering GDP growth of 9.5%; prima facie, this is an impressive feat but don’t underestimate the benefit of weak comps from the previous year. Can the country come back and deliver 8-9% growth in 2022, on the high base of 2021?

As things stand, the expectation is for 8.5% growth; by all accounts an impressive prospective number, particularly when you consider that global GDP growth is only likely to come in at 4.9% and emerging markets are only expected to grow at 5.1%. But do consider that this outlook was provided in October 2021, and since then we’ve had quite a few economic developments that have altered the economic landscape not just in India but globally.

Regardless, here are some considerations that could impact India’s growth potential as well as the prospects of IFN.

Indian financials

The performance of the Indian financial sector will be rather instrumental for IFN as it accounts for the largest share of the portfolio. If we look at Indian banks’ aggregate loan growth trends, we can see that since the advent of the pandemic, this metric has tended to oscillate within a band of 5-7.5%. Encouragingly, in the second half of 2021, we’ve also seen decent sequential progress with loan growth in recent weeks hitting the 7.3% levels. Still, given the growth potential of the country (7-9% levels), you’d want to see the country gravitate towards much higher credit penetration with loan growth closer to the double-digit levels. Without double-digit growth in the loan book, you’re probably asking too much from the fee-based income or the treasury income aspect of banks to help cushion earnings.

Source: Trading Economics

That’s why the recent Omicron scare could put a spanner in the works of what is an otherwise nascent recovery. Major metros in India are already putting in place restrictions and the fear is that country could soon be on the cusp of a third wave. The MSME (Micro, Small and medium enterprises) segment remains a key source of hope for Indian banks’ financing prospects, but this is a segment that is likely to be most acutely impacted by any potential lockdown restrictions. In a report published late last year, encompassing results of its stress tests, the central bank of India had flagged the potential for NPAs (Non-performing assets) of Indian banks to increase from 6.9% at the end of Sep 2021 to 8.1% by September 2022 under a base line scenario and 9.5% under a severe stress scenario. Encouragingly, even if the adverse scenario were to pan out, the Indian banks have built up adequate minimum capital to cope with the consequences.

Indian banks are also awaiting some policy normalization in terms of interest rate hikes (and what this could do for their Net interest margins), but this will likely have to wait given the risk of the Omicron variant which could derail the growth momentum.

Rupee trajectory

As pointed out in this week’s edition of The Lead-Lag Report, even though the 6-month run of the dollar index may look like its petering out in the near term, I still believe this is more a case of stabilization rather than any reversal in the trend. Certainly with US treasuries offering comparatively higher interest rates than most other regions around the world and with the Fed poised to hike rates by anything between 2-3 times next year, I’d expect demand for dollar-denominated assets to remain steady throughout the year.

Also consider that India is not in any pressing need to hike rates given that the latest CPI inflation reading at 4.9% is well within the central bank’s comfort range of 2-6% (incidentally it has been within this range for the last 5 months). Much of this inflation is a function of non-seasonal rains which dampened food supply; I’d expect this to be normalized soon enough.

Regardless, as the US Fed begins its tightening mechanism, I’d expect pressure on the USD/INR, more so as the country’s trade deficit position remains quite elevated at $22bn (in Nov it was at a record high of $23bn). Worryingly, also note that India’s current account deficit (CAD) currently stands at 3.4%, up from 1.3% a quarter ago.

Whilst potential rupee depreciation could eat into IFN’s holders, some mitigation may well be expected from the Indian IT sector, which is the second largest sector within IFN with a 20% weight. Most of the tech holdings of IFN derive a large chunk of their revenue from the US markets and an appreciation in their dollar should help boost their reported numbers.

Reforms could be stalled until UP election results

It’s also important for a high-potential emerging market such as India to churn out ample economic reforms to help bring more foreign capital to the country, but I think the government will likely think twice before pressing any button particularly given the failure of the Modi government to push ahead with the recent farm laws. What also makes things particularly tricky is the onset of elections in Uttar Pradesh – India’s largest state. If the BJP party loses elections there, you could see it resort to more populist measures and less reformist measures, which could hurt the economy in the long run.

Conclusion

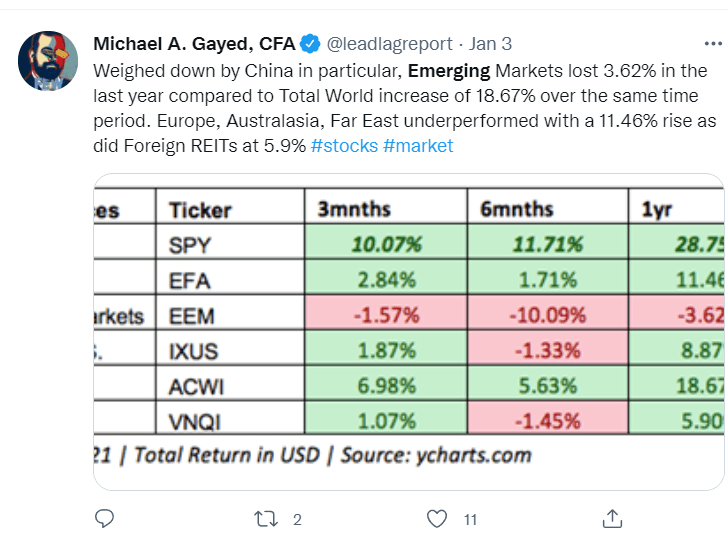

Source: Twitter

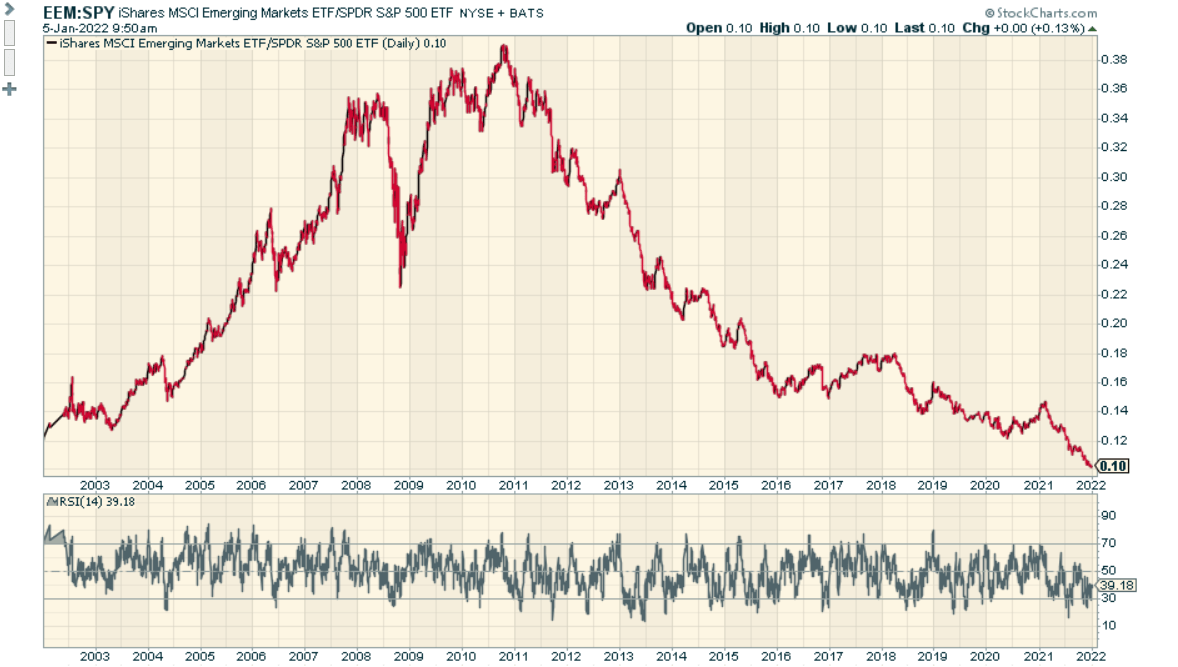

As highlighted by a data table that I put out in The Lead-Lag Report, emerging markets have had to take it on the chin in the last year or so and have underperformed Europe, Australasia, Far East and Foreign REITs. In fact, a ratio measuring the strength of emerging markets and the SPY has collapsed to levels never seen before!

Source: StockCharts

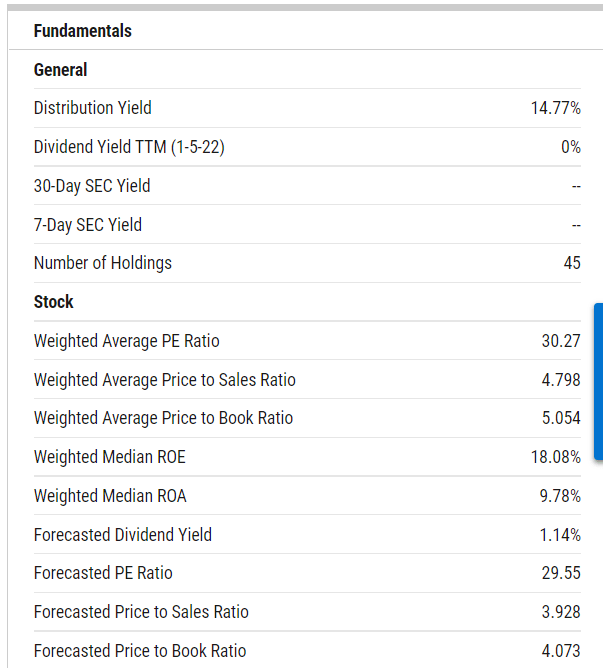

Given this scenario, bargain hunters could be looking for value opportunities within the EM landscape. Unfortunately, I can’t sit here and state that the India Fund is one of those value-oriented investment options; as you can see from the image below, IFN currently trades at exorbitant forward valuations, be it on a P/E basis (29.5x), P/BV basis (4x) or P/S sales (3.9x).

Source: YCharts

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.