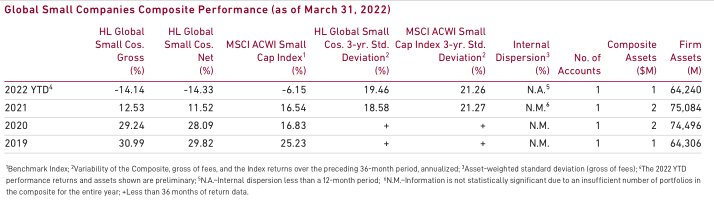

Composite Performance: Total Return (%) — Periods Ended March 31, 20221

| 3 Months | 1 Year | 3 Years2 | Since Inception2,3 | |

| HL Global Small Companies Equity (Gross of Fees) | -14.14 | -3.18 | 12.67 | 16.35 |

| HL Global Small Companies Equity (Net of Fees) | -14.33 | -4.05 | 11.67 | 15.31 |

| MSCI All Country World Small Cap Index4,5 | -6.15 | 0.04 | 12.21 | 15.56 |

1The Composite performance returns shown are preliminary

2Annualized Returns

3Inception Date: December 31, 2018

4The Benchmark Index

5Gross of withholding taxes.

Please read the above performance in conjunction with the footnotes on the last page of this report. Past performance does not guarantee future results. All performance and data shown are in US dollar terms, unless otherwise noted.

1Includes countries with less-developed markets outside the Index.

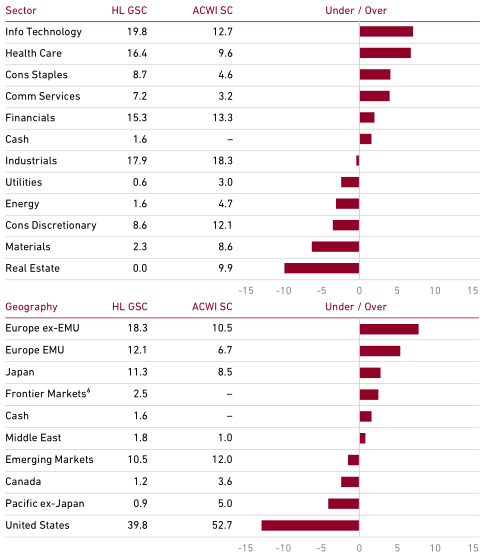

Sector and geographic allocations are supplemental information only and complement the fully compliant Global Small Companies Equity Composite GIPS Presentation. Source: Harding Loevner Global Small Companies Equity Model; MSCI Inc. and S&P. MSCI Inc. and S&P do not make any express or implied warranties or representations and shall have no liability whatsoever with respect to any GICS data contained herein.

Market Review

Stock markets fell in the quarter, as the world watched Russia’s invasion of Ukraine in horror. Global small caps declined 6.15%,1 underperforming global large caps modestly.

The reaction to the invasion by Western governments was swift and emphatic as they sought to tread a delicate balance between punishing Russian aggression and avoiding an escalating military conflict. The US and its allies enacted crippling economic sanctions against Russia, including freezing a significant share of the Russian central bank reserve assets, cutting off many of the country’s banks from the SWIFT global financial messaging system, and outlawing the export of a variety of industrial and luxury goods.

The revulsion at Russian aggression also provoked an exodus of Western companies from Russian markets. The sanctions initially led to a collapse in the ruble, forcing the central bank to raise overnight interest rates to 20% per annum to bolster the currency, while the Moscow stock exchange closed

for almost a month before re-opening for domestic investors only. With foreign investors effectively unable to trade, major market index providers expunged all Russian securities from their broad market indices. Prices for a wide range of commodities for which Russia is a major producer—including oil, gas, grains, and metals—surged on fears of disruption, prompting billions of US dollars in margin calls to cover futures positions.

MSCI ACWI Small Cap Index Performance (USD %)

| Geography | 1Q 2022 | Trailing 12 Months |

| Canada | 5.8 | 20.0 |

| Emerging Markets | -4.3 | 6.0 |

| Europe EMU | -8.4 | -1.0 |

| Europe ex-EMU | -13.7 | -4.5 |

| Japan | -7.0 | -11.9 |

| Middle East | -0.6 | 32.9 |

| Pacific ex-Japan | -0.2 | 7.1 |

| United States | -5.9 | -0.3 |

| MSCI ACWI Small Cap Index | -6.2 | 0.0 |

| Sector | 1Q 2022 | Trailing 12 Months |

| Communication Services | -8.3 | -7.8 |

| Consumer Discretionary | -13.5 | -14.7 |

| Consumer Staples | -5.0 | -8.4 |

| Energy | 34.0 | 61.8 |

| Financials | -3.8 | 5.0 |

| Health Care | -13.9 | -19.4 |

| Industrials | -7.1 | 2.5 |

| Information Technology | -11.6 | -1.1 |

| Materials | 2.0 | 10.9 |

| Real Estate | -4.4 | 11.6 |

| Utilities | 2.0 | 11.3 |

Source: FactSet (as of March 31, 2022). MSCI Inc. and S&P.

Headline inflation, which had already been rising rapidly around the world prior to the invasion, received a fillip from the shock to energy and food supplies stemming from the war, increasing the pressure on central banks to tighten monetary policy. The Bank of England—along with the South Korean, South African, and Brazilian central banks—continued raising short-term policy rates to beat back rising prices.

In the US, the Federal Reserve lifted rates for the first time since December 2018 and signaled a willingness to do whatever it takes to bring inflation under control, announcing an aggressive rate hike path for the months ahead. The yield curve flattened dramatically; in March the US two-year yield briefly exceeded the ten-year yield for the first time since 2019, flashing a recession warning as bond investors bet that higher yields would crimp growth.

The prospect of tighter monetary conditions further undermined the case for highly priced growth stocks, whose expected cash flows, in lying further out into the future, are more sensitive to interest rates. The MSCI ACWI US Small Cap Growth Index declined over 10%, while its value counterpart was only down about 2.5%, highlighting the impact of increasing economic uncertainty from higher inflation and the war in Ukraine. High- quality companies were no refuge from the sell-off of growth companies, with the highest quality quintile underperforming the lowest by nearly 11%.

Sector performance reflected the meteoric rise in commodity prices caused by supply shocks from war and sanctions, with both Energy and Materials finishing in positive territory. Demand for commodities could be set to fall, though, given that consumer confidence (critical to the slumping Consumer Discretionary sector) and business confidence (a big influence on swooning Information Technology, or IT, stocks) seem to be flagging. Health Care was dragged down by the double whammy of a post-COVID-19 slowdown in health care funding and higher interest rates.

Canada was the best performing region, helped by its heavy weight in Energy and Materials stocks. Proximity to the war in Ukraine, and, for some, lack of NATO membership, weighed on several European countries including Finland and Sweden.

In Emerging Markets (EMS), exceptional returns in several commodity-rich countries, such as Peru, Brazil, and Chile, were offset by weakness in China, which faces an economic slowdown aggravated by difficulties in maintaining its zero-COVID policy and the government’s attempts to deflate its colossal real estate bubble. China’s “no limits” friendship with Russia also threatened to expose the country to retaliatory Western economic sanctions.

Worsening the sentiment toward China, the US Securities and Exchange Commission began the procedural implementation of the Holding Foreign Companies Accountable Act, identifying several US-listed Chinese companies whose latest financial reports fail to adhere to US audit standards and could be subject to delisting. Shortly after, Chinese officials signaled room for compromise on a mutually agreeable auditing framework, suggesting this is at least one area where the sentiment is likely worse than reality.

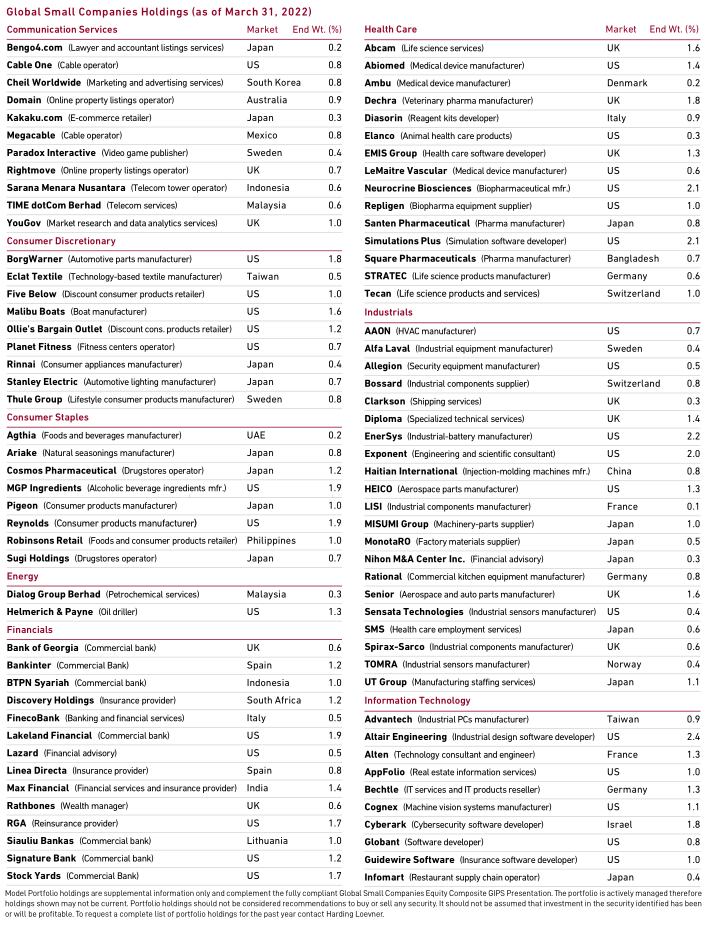

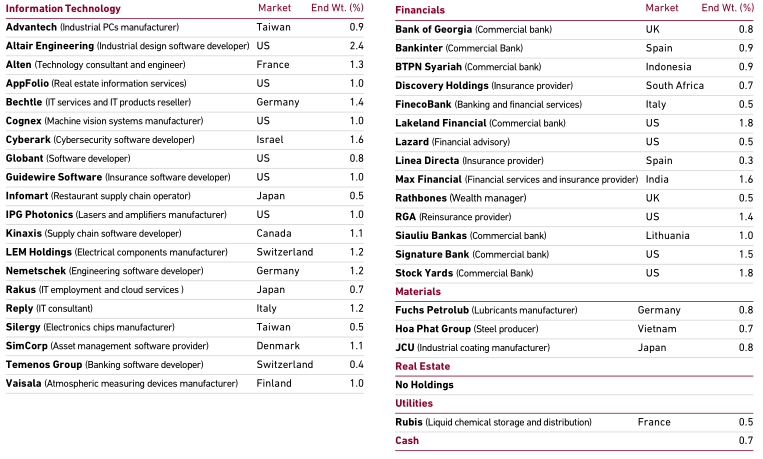

Companies held in the portfolio at the end of the quarter appear in bold type; only the first reference to a particular holding appears in bold. The portfolio is actively managed therefore holdings shown may not be current. Portfolio holdings should not be considered recommendations to buy or sell any security. It should not be assumed that investment in the security identified has been or will be profitable. To request a complete list of holdings for the past year, please contact Harding Loevner.

A complete list of holdings at March 31, 2022 is available towards the end of this report.

Performance and Attribution

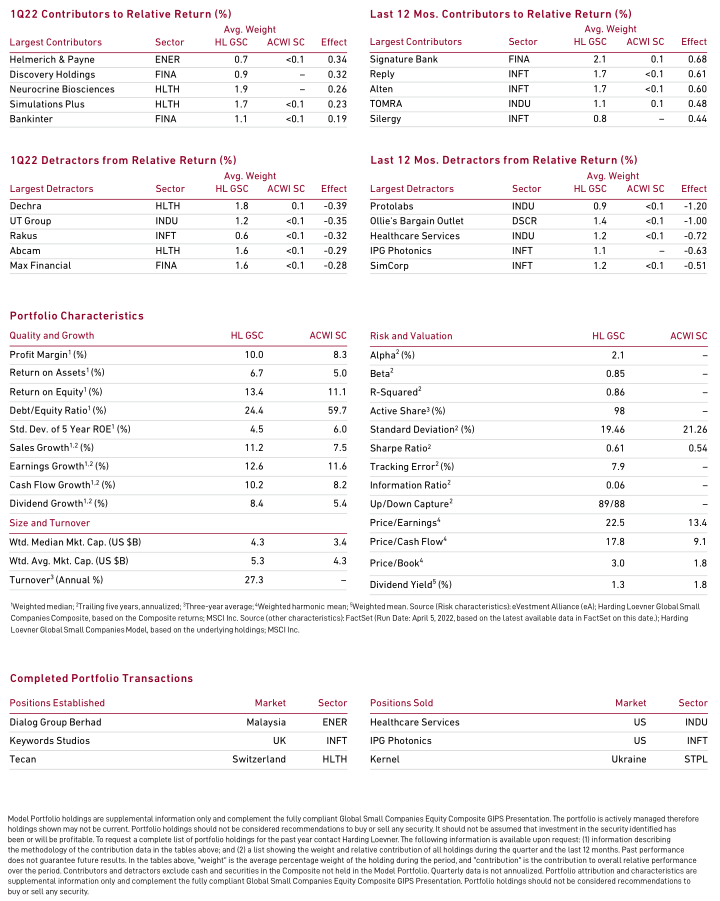

The Global Small Companies composite returned -14.1% gross of fees, well behind the -6.2% return of the MSCI All Country World Small Cap Index.

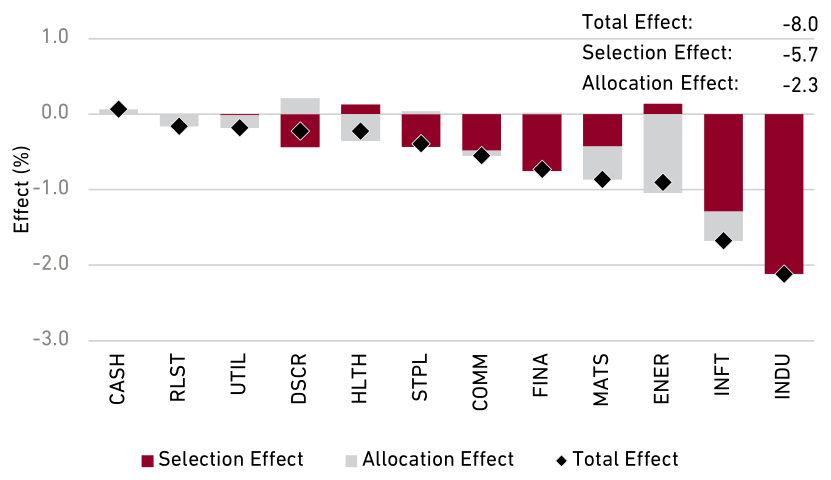

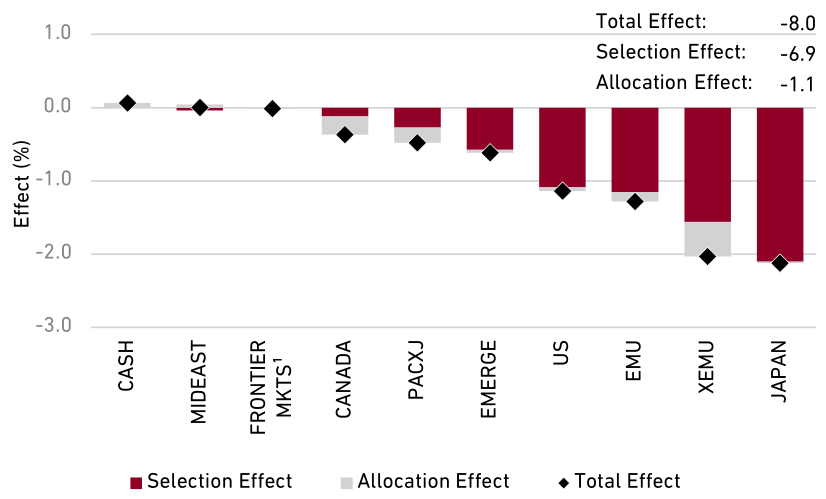

First Quarter 2022 Performance Attribution

Sector: Global Small Companies Equity Composite vs. MSCI ACWI Small Cap Index

Geography: Global Small Companies Equity Composite vs. MSCI ACWI Small Cap Index

¹Includes countries with less-developed markets outside the index. Source: FactSet; Harding Loevner Global Small Companies Equity Composite; MSCI Inc. and S&P. The total effect shown here may differ from the variance of the Composite performance and benchmark performance shown on the first page of this report due to the way in which FactSet calculates performance attribution. This information is supplemental to the Composite GIPS Presentation.

The portfolio’s concentration in expensive stocks, a hazard of our commitment to investing in the stocks of high-quality rapidly growing businesses, hurt relative performance in a quarter during which investors fled from richly priced companies. So stiff was this style headwind that, when viewed through the standard lenses of sector and geographic attribution, our portfolio underperformed within most sectors and most regions. Walking through sector by sector or region by region would add little to that overarching explanation.

A more informative parsing of sources of underperformance comes from viewing our returns according to cohorts defined by growth, quality, and valuation. Viewed through the lens of our quality and valuation rankings, the portfolio’s emphasis on the fastest-growing companies—or, inseparably, its tolerance of their rankings among the most richly priced cohorts—accounted for about 60% of the underperformance in the quarter. Our parallel emphasis on quality provided no defense in the period.

But within these higher quality and richly priced cohorts, some of our holdings performed even worse than their peers. Their shares, having previously been priced for perfection, saw imperfections that were revealed by these companies in the quarter seized upon amid the market’s general retreat from high- priced shares. This combination was particularly toxic for our Japanese holdings.

Rakus, a provider of cloud-based productivity software tools, reported robust revenue growth, but more aggressive marketing spending depressed profit margins. SMS, a leader in nurse recruiting and placement services, announced disappointing earnings as hospitals and eldercare-facilities saw reduced demand for elective procedures and avoidance of group- care settings amidst the pandemic.

Nihon M&A Center Inc. (OTCPK:NHMAF), which otters M&A services for small- and medium-sized businesses, had to restate its earnings for 2021 after some employees falsified reports to accelerate 2022 revenue into 2021. Management has at least been forthcoming in disclosing the incident, and it has tightened its internal controls.

Within the market’s higher quality and richly priced cohorts, some of our holdings performed even worse than their peers.

Poor relative returns for some of our many software and services companies also hurt. In addition to Rakus, Danish financial software company SimCorp (OTC:SICRF) lagged after issuing weaker profit guidance due to increased R&D spending on its next generation of products. Shares of Nemetschek (OTC:NEMTF), a German provider of design software for the building and construction industry, performed poorly on concerns that rising interest rates would threaten to curtail cyclical growth in construction, despite the company raising its growth projection for this year.

Perspective and Outlook

Well before the Ukraine crisis, headline inflation had been rising almost everywhere and intruding on the discount rates used to value shares. The energy and food shocks emanating from the conflict and consequent sanctions have supercharged the existing trends for expected inflation, bond yields, and equity discount rates, and the prospects for tighter monetary policies to combat the rise in prices.

These trends have the largest effects on the present value (and therefore the current price) of distant future earnings—and thus pointedly on the price of growth stocks whose expected cash flows lie far in the future. The damage from these style headwinds was almost as great in the first quarter of 2022 as in the prior 14 months, during which the first COVID-19 vaccine was approved and the retreat began from higher growth and quality towards less-expensive, lower-growth companies that will earn more of their cash flows in the near and medium term.

The damage from the style headwinds was almost as great in the first quarter of 2022 as in the prior 14 months.

The monetary policy tightening now underway by central banks is intended to dampen speculative or less productive demand for goods, services, and assets by raising borrowing costs. Those policies, when combined with the demand destruction likely to emanate from soaring food and energy prices, may contain the seeds of their own reversal.

If consumer and producer confidence take more than a temporary hit from the war in Ukraine and its ramifications, a recession—either in Europe or more globally— could conspire to reduce the inflationary impulse from COVID-19 re-openings and offset some of the need for monetary tightening. We’re not in the business of making such forecasts but, were that scenario to unfold, it’s possible that the headwinds for our quality/ growth investment style would abate.

Much has been written recently about “the end of globalization” being another result of the war in Ukraine, and about the reluctance of some large countries—notably China and India—to sign onto the sanctions imposed by Western and Asian-Pacific governments. We, like many observers, worry that China, ostensibly aiming to be neutral, might risk some consequences by facilitating sanctions workarounds for Russia, and misjudge the West’s resolve.

The economic disincentives would appear to work against the possibility. China’s total trade with Russia in 2020 was around a tenth of its US$1.4 trillion total trade with the US and Europe. Given China’s flagging growth as it manages its deflating property market—a multi-year prospect, if previous property bubbles are anything to go by—and its stated priority to improve “common prosperity” for its people, the last thing it’s likely to want is to impair its access to the global trading system and court rejection by its largest customers.

Indeed, the statement by economic policy czar and Vice Premier Liu He on March 16th affirming the importance of economic growth and markets, offered insight into the government’s leanings and helped reverse a dramatic swoon in Chinese stocks that had coincided with reports that China might be contemplating military aid to Russia. The separate salutary comments from the Chinese securities regulator regarding its ongoing negotiations with the US over audit inspections added to the more reassuring narrative (although, we’ll note, the US legislation that sparked the whole audit and delistings issue has a long fuse that could allow negotiations and decisions to be tortuously slow).

While risks of unforeseen consequences arising from the Ukraine conflict are high, on this front we are cautiously optimistic that China will work hard to maintain its neutrality in a credible way, as it is a huge beneficiary of trade with the rest of the world, especially developed nations. We think it likely that China, along with India, will continue to buy oil and gas from Russia (just as Europe, at least for now, plans to keep its gas pipelines open), and do not expect that fact to alter China’s trade relations with the West much.

Nevertheless, we must contemplate that our optimism is misplaced on the importance of membership in the global network of exchange. If our central and optimistic case—admittedly an educated guess—is wrong, then we’d need to modify our views of which companies in our opportunity set will face new barriers to profitable growth, and which might stand to benefit, relatively, from a further receding of globalization. (Global trade, after all, has never matched the peak share of GDP it reached in 2008, before the global financial crisis.) We’d expect such a world to be less efficient, as the cold logic of comparative advantage is demoted as a determinant of which goods or services are produced and where.

That would lead to a less prosperous world, since exploiting comparative advantage is a cornerstone of wealth creation. If regional blocs began to raise limits on the movement of capital as well as goods, we’d need to parse which of our companies were at risk of declining sales from increasingly hostile, siloed countries.

For example, Bossard, a Swiss fastener distribution and logistics company, has built its business upon today’s web of global supply chains. Its specialty is helping a company like Tesla (TSLA) obtain for each model the optimal fasteners, whether bespoke or ready-made.2 It sources them from its network of 4,500 manufacturing partners, ensuring that Tesla always has the ideal level of inventory as cheaply as possible. It would throw a considerable monkey wrench in Bossard’s business if some of its best suppliers, many of which are located in China, were to find themselves trapped behind new Western tariffs or trade sanctions.

At the same time, we need to be careful not to underrate the ability of Bossard or its automobile and other manufacturing customers to prepare for and adapt to such scenarios. Tesla, for one, makes increasing numbers of its cars in China, destined for the domestic market, for which it could continue to source locally; and, in the case that Bossard runs into difficulty servicing the company’s factories in California and Texas, it has plenty of suppliers in Mexico it can turn to. In a world of new barriers and shifting trade patterns, it would become more difficult for companies to manage their fastener sourcing internally.

Bossard had a record year in 2021, growing revenues by 22%, as more manufacturers sought out its specialized expertise to help them contend with seized-up supply chains.

For Bossard, a Swiss fastener distribution company, it would throw a considerable monkey wrench in the firm’s operations if its best suppliers in China were to find themselves trapped behind new Western tariffs or trade sanctions. At the same time, we shouldn’t underrate the ability of Bossard or its customers to prepare for and adapt to such scenarios.

Kinaxis (OTCPK:KXSCF), an Ottawa-based supply chain management software company, could directly benefit from near-shoring initiatives and other efforts to build more resilience into supply chains. The company saw strong demand in response to the pandemic’s logistics challenges, and in its March update management said demand continues to pick up. Their guidance is now for 2022 revenue growth of between 34%-38% and improving profitability.

While some small companies are heavily geared toward globalization or helping with the transition toward some retrenchment away from it, others have more of a domestic focus. Indeed, around 56% of revenues for small companies come from their home markets, compared to 40% for large companies, which means small companies are somewhat less exposed to the risk of losing foreign customers.

For some small companies with a high foreign sales revenue, sources may align neatly with the trading bloc in which they are likely to find themselves. Take Diploma, another stock that performed poorly during the quarter. While the UK-based controls, seals, and life science equipment supplier only generates 15% of its sales from the UK, it generates a further 62% of its sales in Continental Europe and the US, markets to which the UK will remain tightly bound.

Portfolio Highlights

With the volatility of stock prices this quarter, portfolio activity picked up as a handful of high-quality growth companies we had long admired but regarded as too expensive saw their valuations fall into range.

In Health Care, the sector that declined the most during the quarter, we made a new purchase in Switzerland-based Tecan (OTC:TCHBF), a leading provider of lab automation products. Labs that use its equipment to replace slow and error-prone humans can significantly increase volumes and reduce turnaround times. The company’s recent acquisition of Paramit, a leading manufacturer of medical devices, diagnostics, and life science instruments, provides new verticals with important synergies with Tecan’s core lab systems.

Sales are currently focused on the US (46%) and Europe (37%) but are growing in Asia (16%), including China. In its 2021 annual report, Tecan highlighted the growth potential for the company in China, whose health care market is already one of the world’s largest despite per capita health care spending just a fraction of what’s spent in Western industrialized countries.

We also saw an opportunity to add to Energy stocks of companies we expect to benefit from a government focus on energy security, sparked by the invasion of Ukraine. While the world strives to transition to renewable forms of energy, natural gas—the cleanest fossil fuel—will continue to play an important role in meeting energy needs for the foreseeable future.

We established a new position in Dialog Group Berhard (OTCPK:DGUPF) of Malaysia, the operator of the largest oil and gas storage terminal and liquefied natural gas (LNG) transfer hub in the country, the Pengerang Deepwater Terminal. Opened eight years ago to handle overflow from the nearby Singapore LNG hub, Pengerang has quickly become a major node its own right. It is now one of the main facilities for regasification of LNG from the Middle East, which is then piped up into other parts of the region or stored for later use or for arbitraging by energy traders.

On the outbound route, gas from Malaysia’s own fields is liquefied for export to other markets like Japan and South Korea along with oil and petrochemicals blended at the site. The realization of management’s goal of creating the “Rotterdam of Southeast Asia,” a facility on par with Europe’s main LNG gateway, looks within reach.

Video gaming boomed during the pandemic as people sought in-home entertainment. While its growth is normalizing, video games are played by an estimated 3.1 billion people, or 40% of the world’s population.

Microsoft recently announced it would purchase developer Activision-Blizzard (ATVI) —known for its Call of Duty and Warcraft titles—for US$68.7 billion. The deal is just the latest of several major acquisitions by Microsoft and chief rival Sony as each seeks to draw new users for its cloud gaming service with differentiated content.

Ireland-based Keywords Studios (OTC:KYYWF) is an indirect beneficiary of this content arms race as the largest outsourced services supplier to video game publishers, supplying 23 of the 25 largest. As games increase in complexity, large gaming enterprises like Microsoft and its new subsidiaries don’t want to employ thousands of testers or the dozens of designers and developers required to create, say, all the furniture in a vast open-world game.

Instead, these companies increasingly turn to Keywords, which has 9,000 employees located in dozens of studios around the globe performing everything from QA testing to translation to ongoing customer support to art and software development. Unlike generalized IT outsourcers like Infosys or Cognizant, Keywords is focused only on gaming, helping it provide these specialized services cheaply and reliably. Because it works with so many different companies, Keywords grows with the industry instead of depending on any one game becoming a hit.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.