Torsten Asmus

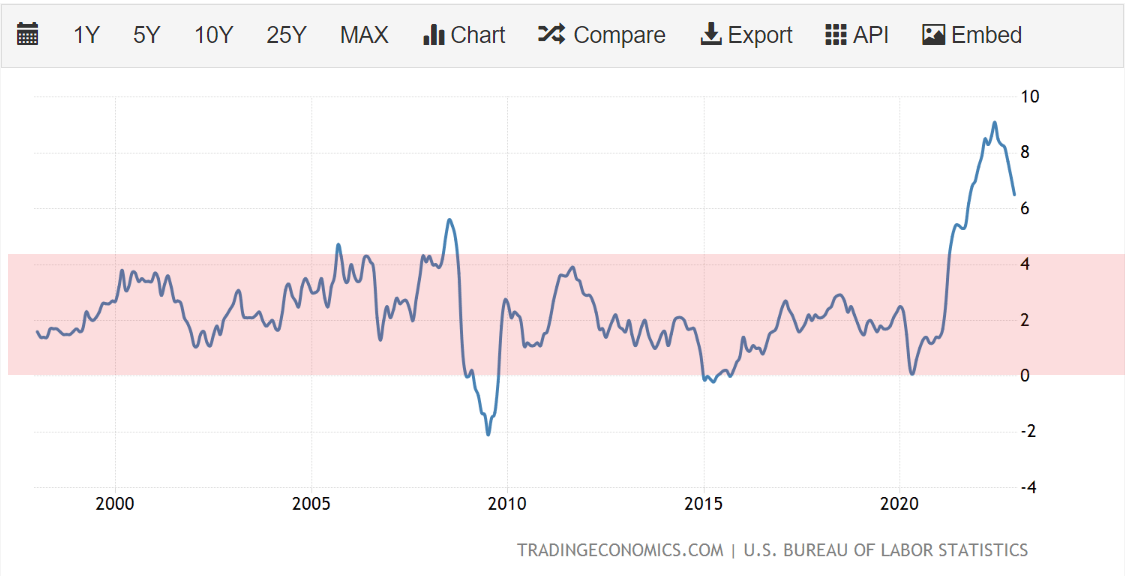

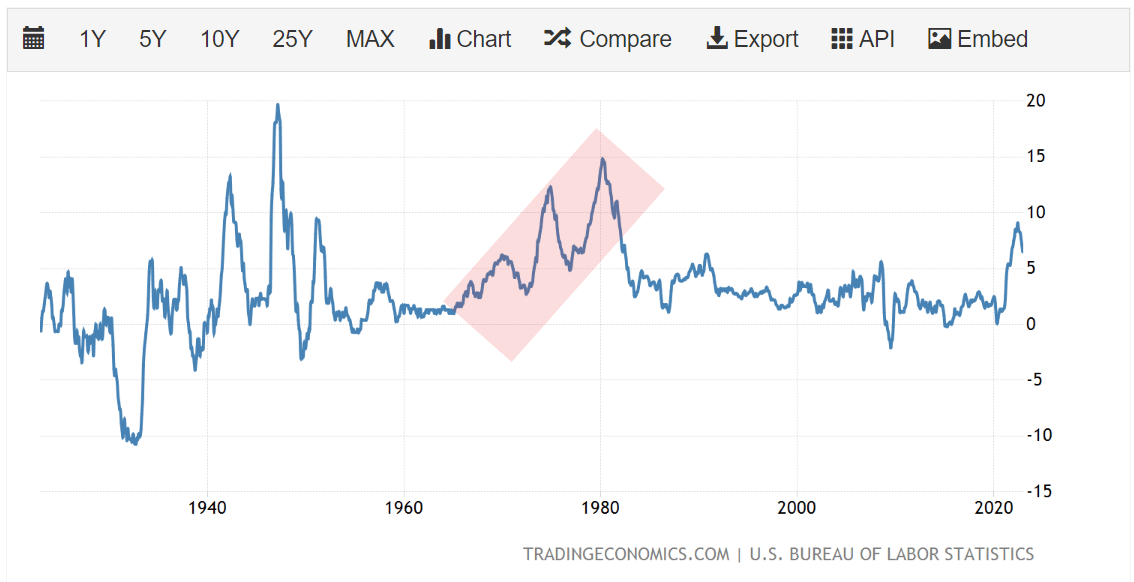

Much has been said about the peak in YoY CPI inflation figures in the past few months, with many market participants anticipating the sharp decline of headline inflation from 9.1% in June 2022 to 6.5% in December 2022 to signal that the inflation scare is over and we can quickly return to the investment regime we have enjoyed from the past 30 years. For much of the past few decades, CPI inflation was well contained within 0% to 4% (Figure 1).

Figure 1 – CPI Inflation was well contained for decades (tradingeconomics.com)

However, I believe there are a number of large macro trends in play that could change this low and steady inflation dynamic. One of the best way to play this ‘higher for longer’ inflation trend is through the ProShares Inflation Expectations ETF (NYSEARCA:RINF), which is a duration hedged bet on 30Yr TIPS bonds. I wrote about the mechanics of the ETF in a prior article that may be of interest to readers.

Three Reasons Why Inflation May Be Structurally Higher

First, in the short term, energy prices are likely to reaccelerate in 2023, adding to the inflation fire.

China Re-open To Boost Energy Prices

By now, readers have probably read countless articles on the re-opening of the Chinese economy and how it could have major consequences for commodity prices and demand. As I wrote in a recent article on the United States Brent Oil Fund (BNO), one of the largest consequences of a China re-opening is going to be a surge in demand for energy commodities like crude oil and gasoline:

China’s re-opening has lifted the prospects for crude oil, with the International Energy Agency (“IEA”) recently forecasting in its January outlook report that China’s re-opening could lift oil demand by 1.9 million barrels per day to a record 101.7 mmbpd, with more than half of the growth coming from China. Similarly, OPEC is expecting Chinese demand to grow by more than 500,000 bpd in 2023.

Higher oil demand from China will lead to higher energy prices globally.

Russia Oil Embargo Will Crimp Supplies

While China is affecting the demand side of energy commodities, the ongoing embargo on Russia crude oil and oil products is going to affect the supply side of the equation.

The EU’s embargo on Russia oil went into effect in December. This meant that countries in the EU can no longer import Russian crude oil, thus they must be shipped to non-embargo countries like China and India. Due to a lack of transport capacity, investment banks like Goldman Sachs is expecting Russian oil production to drop by ~600k bpd due to the oil embargo.

However, a more important wrinkle that has not been talked about is the impending embargo on Russia oil products. After enacting an oil embargo in December, EU countries are now going to introduce an oil products embargo starting in February.

Currently, the EU imports 450k bpd of diesel from Russia. Once the products embargo goes into effect, the EU will have to source diesel from other countries like the U.S. and Saudi Arabia. This will drive up fuel prices for American consumers.

More importantly, the displaced diesel from Russia will struggle to find a home. Countries that are not part of the EU’s oil/fuel embargo will likely not want to import this displaced Russian diesel because they can import heavily discounted Russian crude oil (Russian Urals discount recently widened to ~$40 / barrel) and capture the enormous crack spreads that can be achieved by refining their own diesel.

If Russia cannot find a home for this diesel, then they must shut-in part of their oil production. The most common refining crack spread is the 3-2-1 spread, where 3 barrels of crude oil produces 2 barrels of gasoline and 1 barrel of diesel. Therefore, 450k of displaced diesel could cause Russia to shut-in ~1.3 mmbpd of oil production. Altogether, the EU’s embargo could lead to ~2 mmbpd of reduced global oil supplies just when the supply / demand balance is tightening with China’s re-opening.

Higher Energy Prices Will Re-Ignite Inflation

Already, we are starting to see wholesale gasoline prices in the U.S. bottoming out and trending higher (Figure 2).

Figure 2 – U.S. wholesale gasoline prices (tradingeconomics.com)

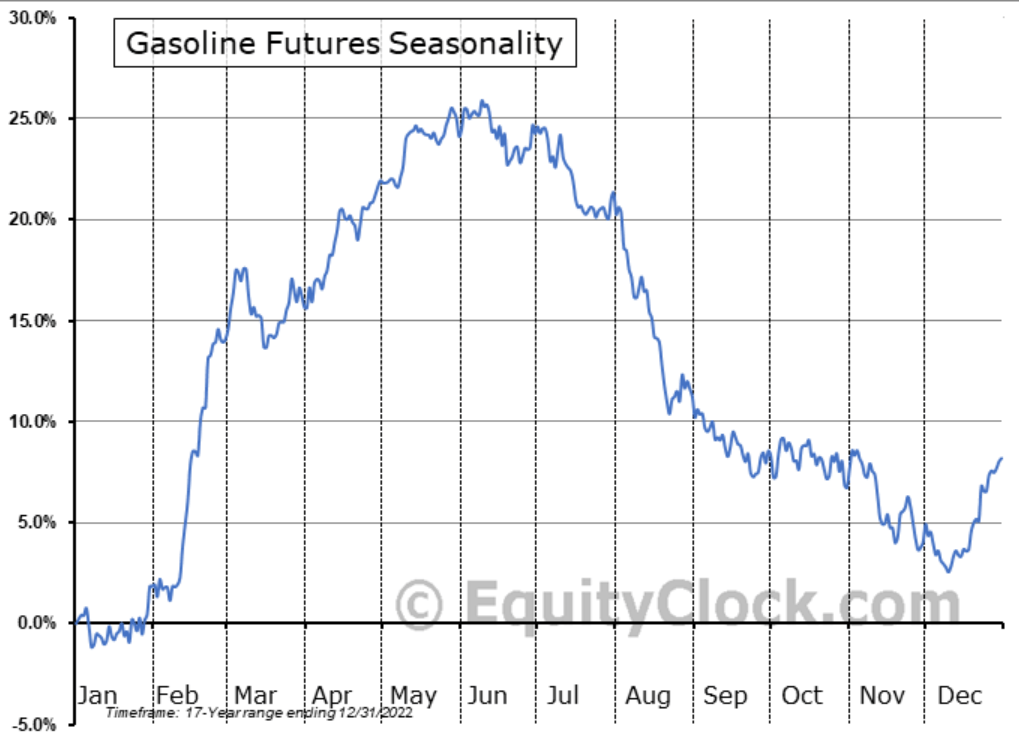

As we enter the spring and traders start to bet on the upcoming summer driving season, we could see gasoline price reaccelerate to the upside (Figure 3).

Figure 3 – Gasoline seasonality (equityclock.com)

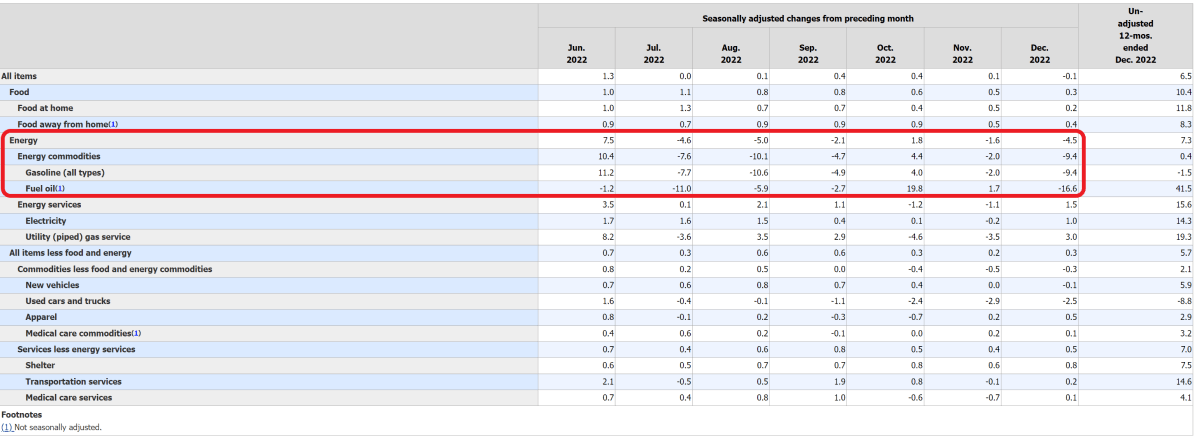

Energy prices, which had subtracted from MoM inflation figures in the past few months will start to become additive again (Figure 4).

Figure 4 – Energy inflation is set to rebound (bls.gov)

Low Net Immigration Causing Labour Shortages And Wage Inflation

In the medium term, inflation may be structurally higher due to a lack of immigration into the U.S.

The 2020 COVID-pandemic caused great disruption in the normal migration of people, especially those from other countries. I believe this disruption in net immigrants into the U.S. is a major cause of the labour shortages and wage inflation we are witnessing right now.

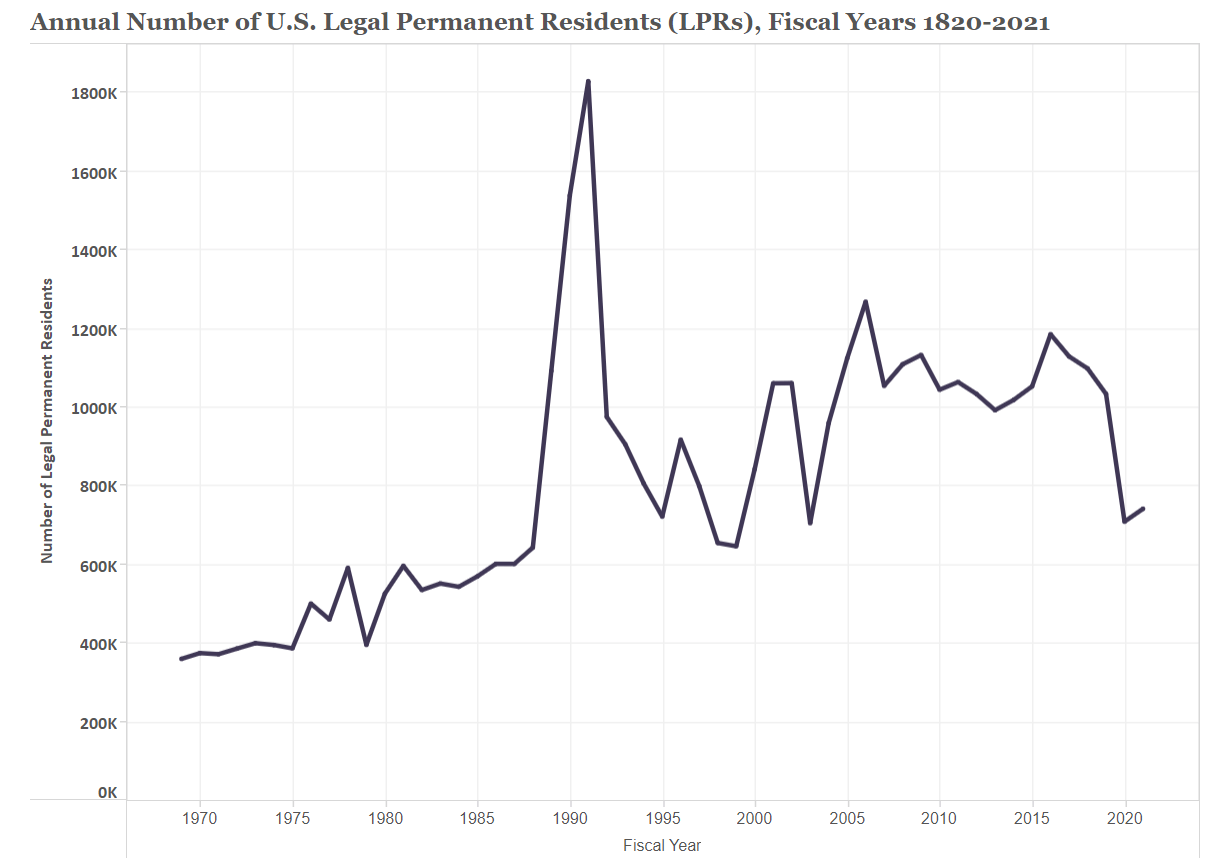

Data from migrationpolicy.org shows that net immigration into the U.S. in 2020 and 2021 fell to the lowest levels since the early 2000s as the COVID-pandemic kept many foreigners at home (Figure 5).

Figure 5 – Net immigration to U.S. plunged in 2020/2021 (migrationpolicy.org)

However, from the data, we can also see net immigration was already declining well before the pandemic. The reason is mainly because of former President Trump’s tough immigration policies, which reduced legal immigration to the U.S. by close to 50%. For example, denial rate on H1-B visas for highly skilled workers rose from 6% in 2015 to 30% in 2020.

According to the Federal Reserve, Trump-era immigration policies have kept labour markets tighter than usual, fueling wage inflation. In a recent Brookings Institute speech, Jerome Powell commented that “the combination of a plunge in net immigration and a surge in deaths during the pandemic probably accounts for about 1-1/2 million missing workers.”

Unfortunately, with Republicans in charge of Congress and a presidential election coming up in 2024, immigration policies may continue to play a restrictive role in the U.S. labour market in the medium term. A tighter labour market is inflationary.

China Rapidly Aging Leads To Long-Term Inflation

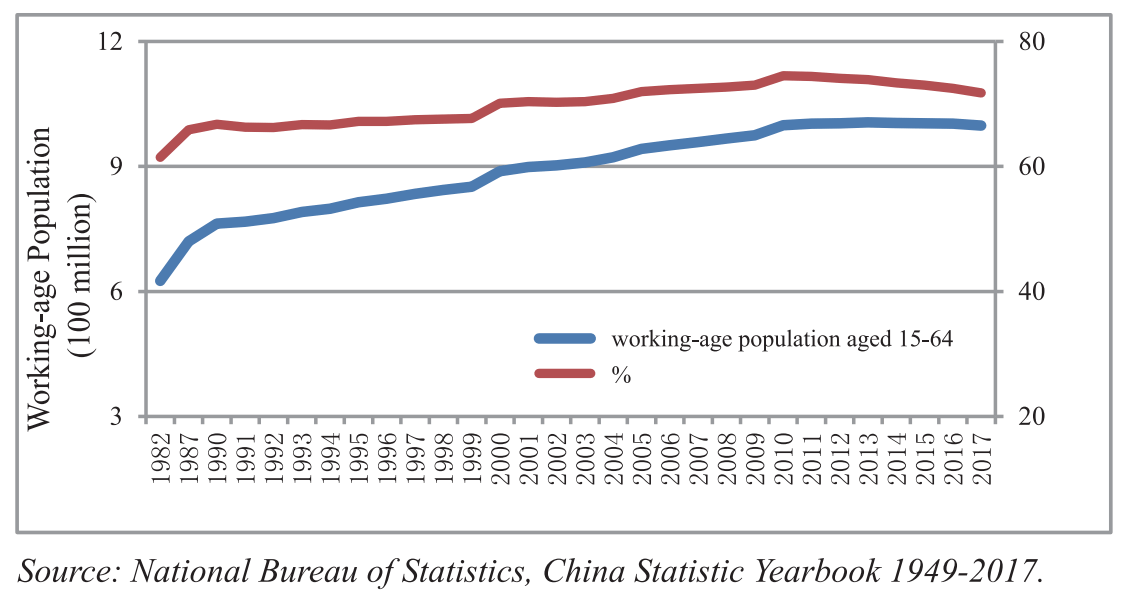

Finally, the effect of China’s demographics on global inflation cannot be overstated enough. During the 2000s, the global economy enjoyed the fruits of China’s demographic dividend. China’s one-child policy rapidly changed the age-structure of its population, creating a 1 billion strong labour force with low dependency ratios (Figure 6).

Figure 6 – Chinese labour force (china.unfpa.org)

To keep this labour force occupied, China opened up its economy and became the world’s factory, manufacturing everything from baseball caps to iPhones.

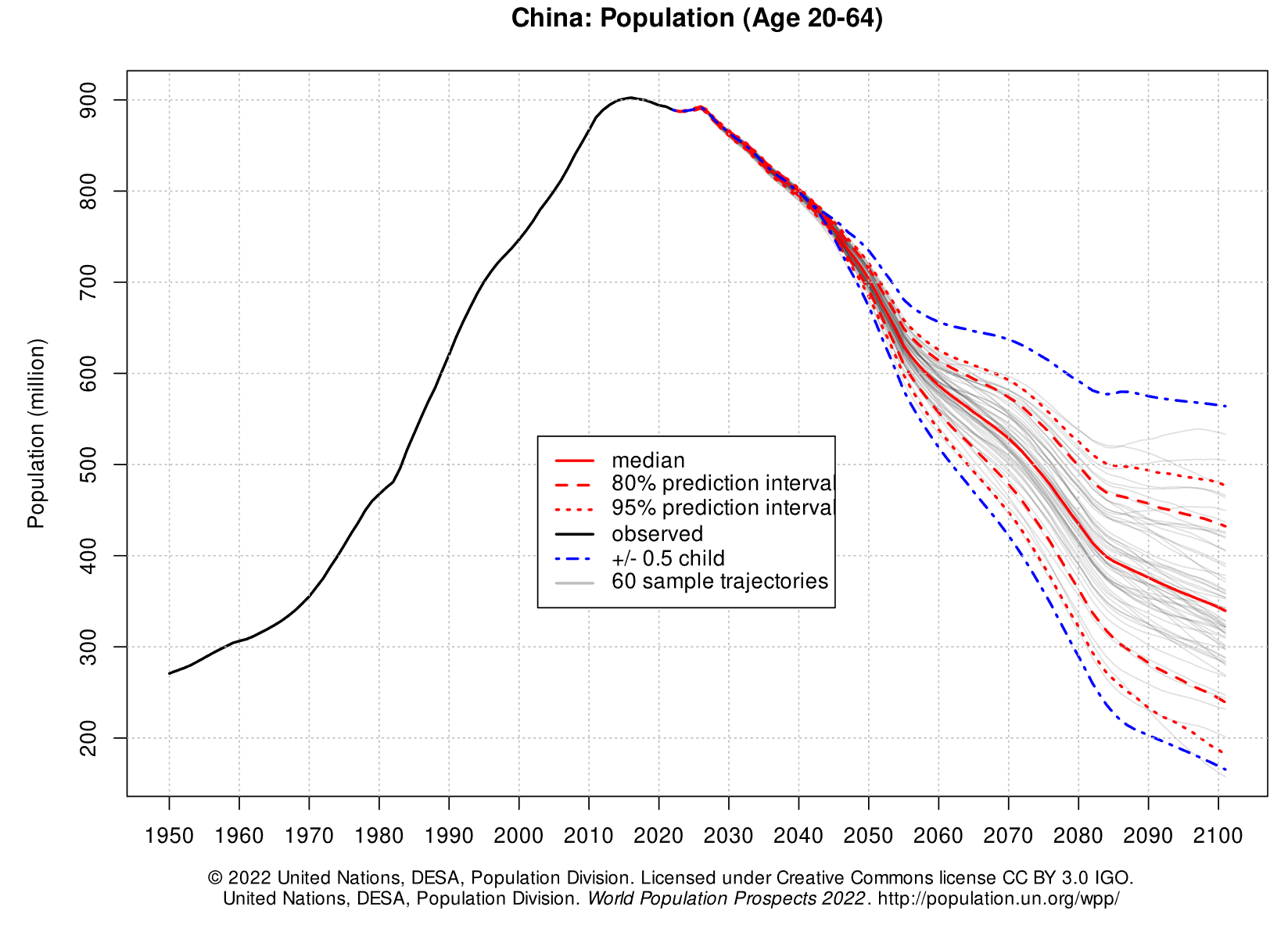

However, China’s demographic dividend is about to reverse, as China’s population is rapidly aging. According to data from the UN, China’s working age population has already peaked and is going to decline swiftly in the coming decades (Figure 7).

Figure 7 – Chinese working age population peaked and is set for rapid decline (population.un.org)

Without cheap and plentiful labour from China, consumers around the world may see steadily increasing prices of manufactured goods in the coming years.

De-globalization To Further Increase Costs

Along with a shrinking Chinese labour force, the global economy will also have to deal with a de-coupling of the global economy. For example, President Biden recently launched a semiconductor chip-war with China, banning the export of advanced semiconductors and technologies to China. This threatens to increase the production costs of semiconductors and lengthen the supply chain of manufactured goods like cars and computers, as many companies will have to look at building semiconductor plants outside of China to avoid the export bans.

If globalization and the coupling of global supply chains with China led to decades of deflationary tailwinds, then the coming de-globalization of global supply chains should lead to decades of inflationary headwinds.

Could We See A Replay Of The 70s?

While the recent moderation of inflation figures are welcome, I worry it is only a cyclical decline and we could see a decade of structurally higher inflation like the 1970s due to the short, medium, and long-term drivers I mentioned above (Figure 8).

Figure 8 – Historical CPI inflation (tradingeconomics.com)

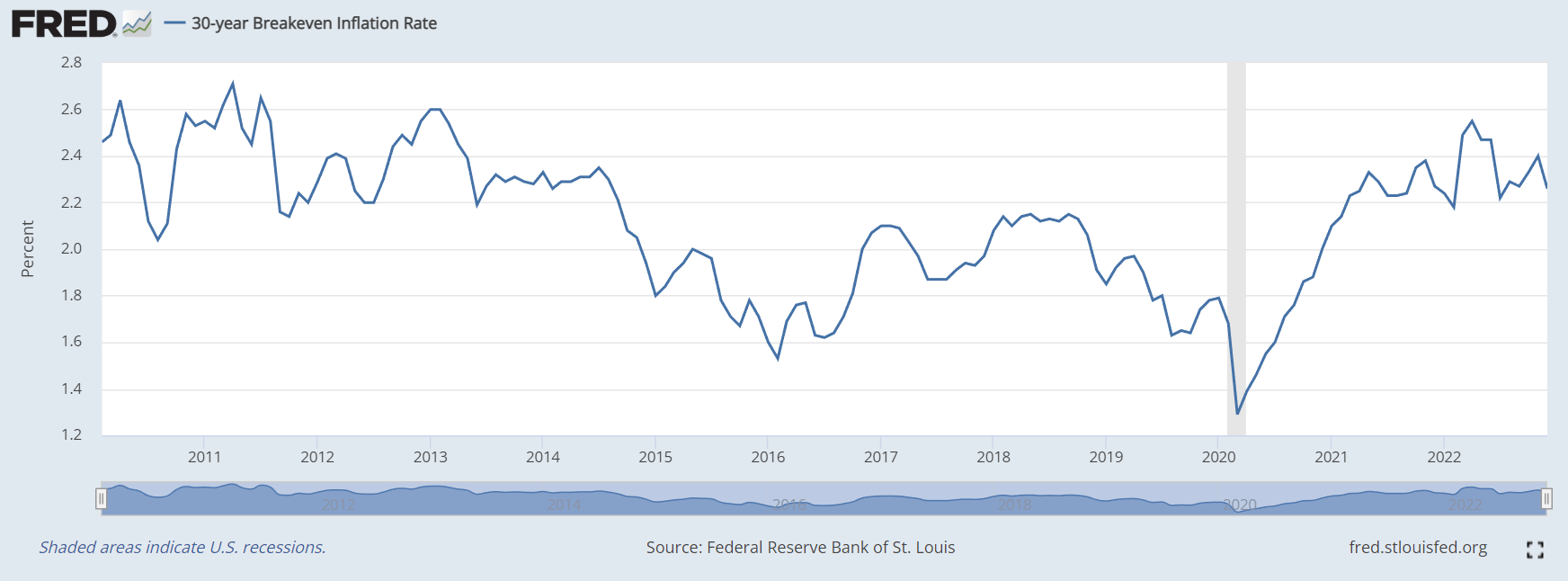

If this thesis plays out, long-term inflation expectations should go much higher, which would be positive for the RINF ETF. Note that although CPI inflation was as high as 9.1% YoY in 2022, 30Yr inflation expectations were still relatively well anchored, peaking at just 2.55% in April 2022 (Figure 9). There is a lot of room for long-term inflation expectations to rise.

Figure 9 – 30Yr inflation expectations still well anchored (St. Louis Fed)

Risks

The short-term downside risk to my call is if the Fed’s monetary tightening in 2022 has been so restrictive that it actually pushes the U.S. economy into a recession, causing a cyclical bout of deflation. A cyclical deflationary period would be negative for the RINF ETF.

In the medium term, perhaps whoever wins the presidency in 2024 will introduce more welcoming immigration policies. That could help alleviate labour shortages and wage inflation.

Longer-term, I see a scenario where India supplants China as the world’s manufacturing hub as it is forecast to have the largest working age population for the next few decades. Cheap Indian labour can replace Chinese labour and manufactured goods can continue to be cheap and plentiful.

Conclusion

While headline inflation has softened in the last few months, I fear it may just be a cyclical decline in a structurally higher inflation trend. In the short-term, China’s reopening and a Russian oil embargo is going to push energy prices higher, fueling a rebound in inflation. In the medium term, poor immigration policies in the U.S. is leaving the labour force short of workers, leading to wage inflation. Finally, in the long-term, China is set to flip from being a deflationary force to an inflationary force, as its population rapidly ages.

One way to protect against structurally higher inflation is through the RINF ETF. It owns a duration hedged position on 30Yr TIPS bonds. If structural inflation is higher in the coming quarters, then RINF should perform well.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.