Investment thesis: With more and more talk of a recession or at least a severe global economic slowdown this year, even as the Federal Reserve is still signaling interest rate hikes, safe haven investment opportunities tend to become more popular. The iShares Core U.S. Treasury Bond ETF (BATS:GOVT) is seemingly a classical safe haven play. When the stock market is suffering, US government bonds are often seen as a safe haven refuge. The thesis may seem sound, except for a very important detail, namely the increasingly dramatic shift out of USD-denominated FX reserves, which seems to be gaining steam around the world. The trend could trigger a global rush for the exits, out of US treasuries, which could happen at any moment, with an unknown level of magnitude.

About the GOVT ETF fund

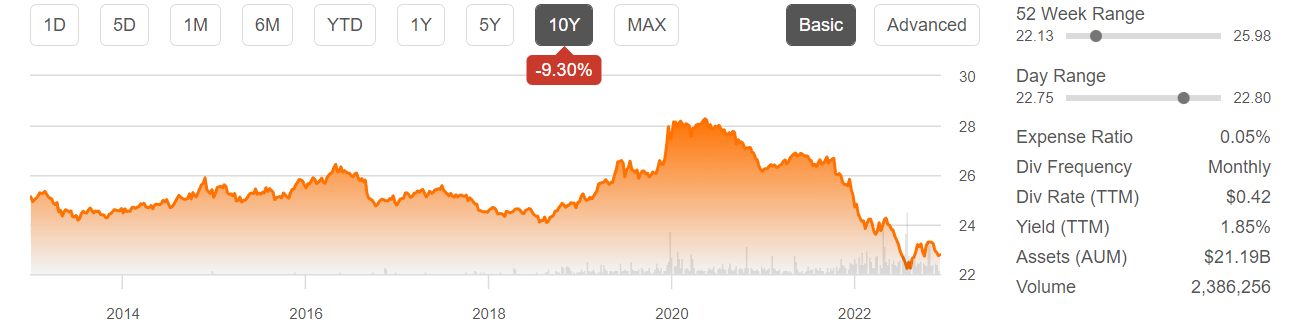

The GOVT ETF Fund is a straightforward investment opportunity available for investors looking to gain convenient exposure to US debt holdings in their portfolio. It provides exposure to US government bonds, with an average maturity of 7.7 years, and an average coupon of just over 2% currently. The fees are .05%. As for its history, one would have not gained much by holding this fund in the past ten years.

Seeking Alpha

The GOVT ETF share price has been trending downward lately and is at lows not seen in the past decade, which by itself is a potential signal to consider buying. Though it may make sense to make the buying argument at this juncture, other factors suggest that there may still be significantly more pain ahead.

The argument for buying GOVT ETF shares

Considering the downbeat outlook for the global economy, as well as the assumption that at some point, perhaps as soon as this year, the Federal Reserve will have to shift from inflation-fighting to fighting an economic downturn, this may be a good time to buy GOVT ETF shares. In theory, buying now would lock in higher yields, while the GOVT fund’s price would rise in the event that the Federal Reserve will switch to monetary easing mode.

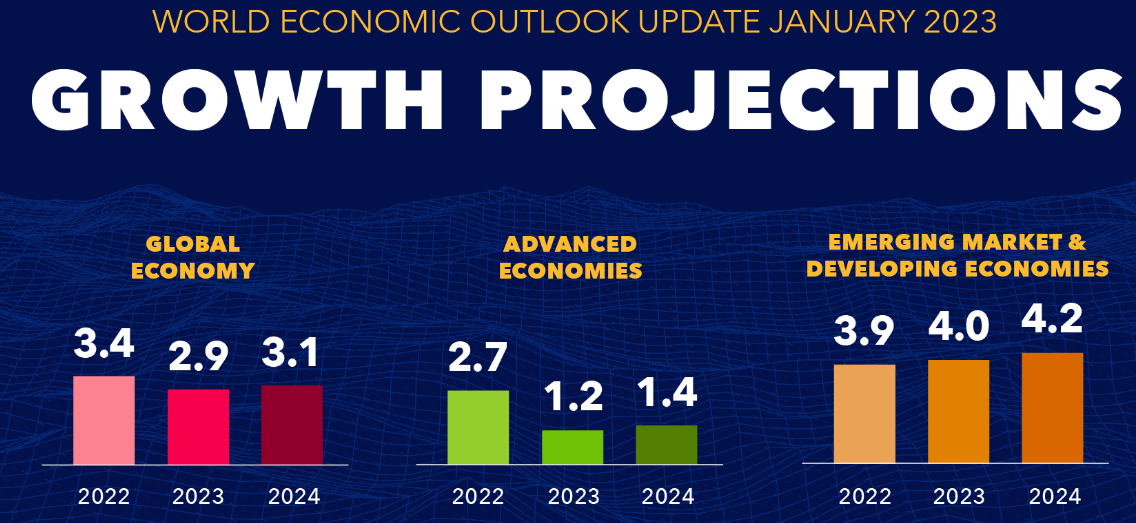

The economic argument for this potential outcome seems increasingly solid, given the already downbeat global economic growth forecasts for this year, such as the one from the IMF.

IMF

It should be noted that this is after the 2020-2021 global economic downturn triggered by the COVID lockdowns, meaning that in the early stages of global recovery after such a dramatic downturn, one might expect a more robust rebound than what we are seeing. My view is that within the context of such a feeble post-COVID global economic recovery, there is a very significant chance that we will see a global double-dip recession, perhaps as soon as this year. It would not take much at all to make it happen. An energy price shock to the system is a very real possibility given the economic Russia-NATO confrontation over Ukraine. In its aftermath, monetary easing would probably follow.

The argument against investing in this fund as a safe haven

While the trend of de-dollarization in global trade has been acknowledged last year, it mostly came with assurances that there is no chance that a major shift in global financial reliance on the USD as a medium of exchange and as FX reserves is impending. The speed with which new announcements of currency swap deals, a broadening of currencies being accepted as payment, and other moves are being announced in the past year, should give people a reason to pause and reflect.

Of particular concern should be the fact that net exporters of oil, such as the UAE, Iraq, Iran, and, of course, Russia are increasingly moving away from dealing in US dollars. Oil, natural gas, and petrochemicals, which are what these countries mostly sell, are indispensable imports for nations around the World. For much of the post-WW2 global order, nations took it for granted that they can use the US dollar to buy such crucial supplies. Now, countries like Russia are increasingly refusing such payments, while also looking to purchase imports in other currencies than the US dollar. India has been frantically working to build non-US dollar institutions through bilateral deals with many trade partners. China might arguably deal the biggest blow to US dollar-denominated FX reserves if the talk of Saudi Arabia moving to accept the Chinese currency as payment for its oil exports will come to pass.

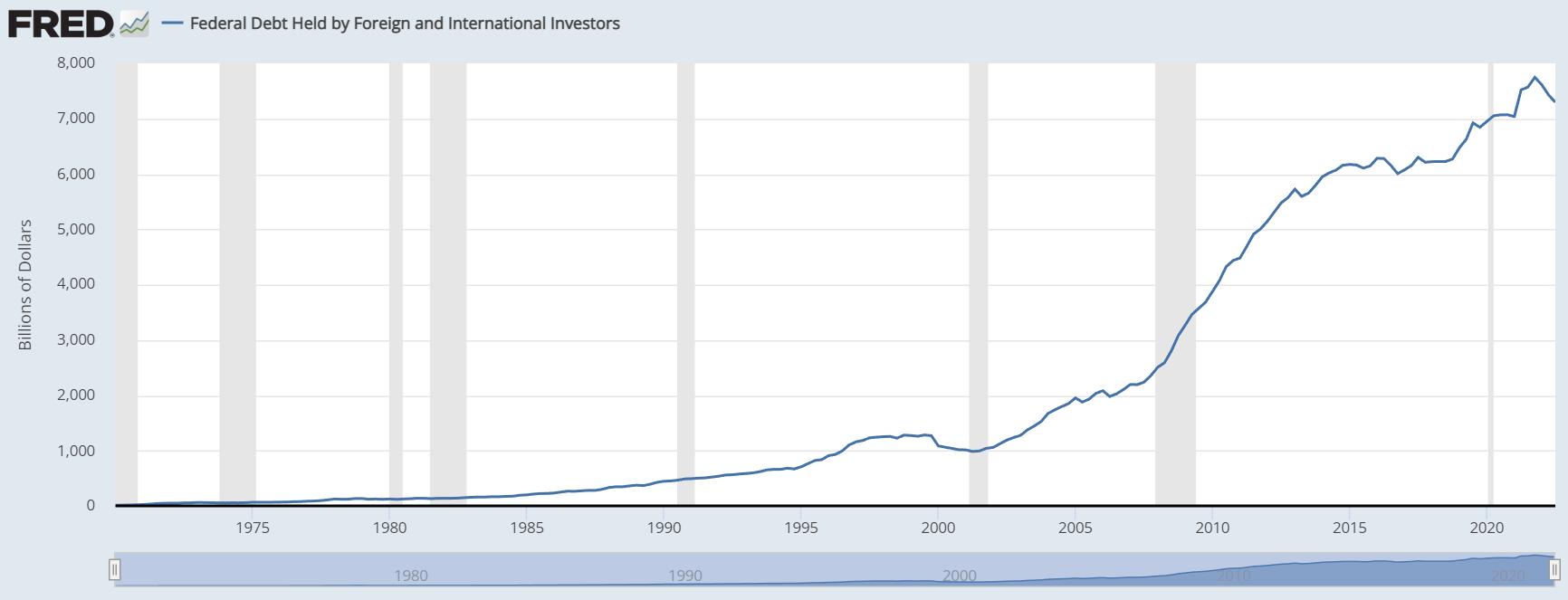

St. Louis Fed

Last year, foreigners were net sellers of US government debt to the tune of over $400 billion. It is unclear why last year foreigners reduced their US debt holdings to such a great extent, but it does coincide with the freezing of Russia’s USD and euro-denominated assets, and talk of outright confiscation. The fact that it was an economically very challenging year for many countries around the world, could have played a role as well. Many governments might have just used up some FX assets to shore up their currencies, or to cover trade deficits.

The risk is that at some point we will see a dramatic acceleration of the trend of net selling of US debt held by foreigners. A trigger event could easily occur. It could be manufactured, by for instance the Chinese government dumping a very large volume of US debt onto the market in a very short time period. The market action could in turn cause a global market panic, and domestic holders of US bonds will most likely join in the selling. If this were to occur, which is in my view a growing possibility, US bond prices would decline dramatically, sending the GOVT fund down with it.

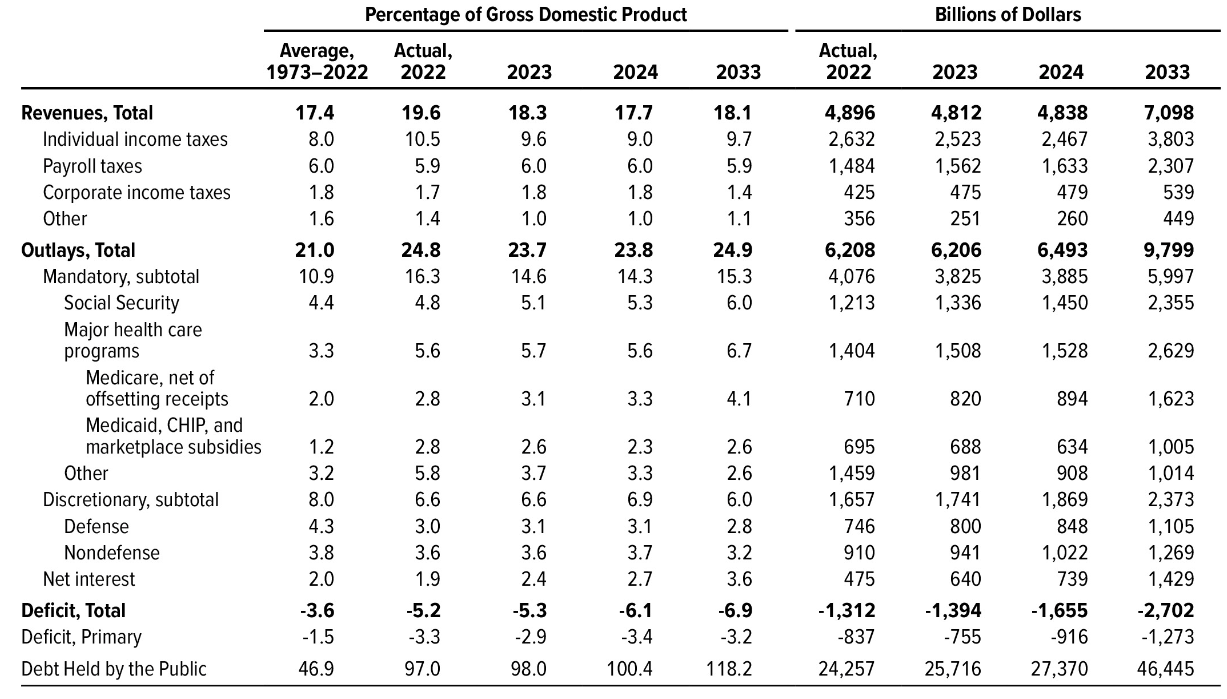

Even as there is growing evidence that foreign governments and other actors are increasingly exploring ways to circumvent USD-based financial institutions, thus potentially reducing global USD-denominated FX demand, the CBO is predicting that the US government is set to nearly double the amount of US federal debt held by the public.

CBO

The issuance of new debt seems massive, which raises serious questions about the market’s ability to absorb it. I think it would be difficult to see such a large volume of debt absorbed by the global markets, even in the event that none of the other outstanding issues I mentioned would be surfacing and picking up steam.

Investment implications

Given the uncertain times we are seeing unfold, with geopolitical events heating up, the global financial situation seemingly deteriorating, while the global economy is starting to misfire under the strain of the various pressures we are seeing, it is important to start identifying potential safe haven investment opportunities. History is on the side of US bonds, and by extension for the GOVT fund. Since the post-WW2 world order, US-denominated assets ranging from cash to bonds have been seen as a safe haven asset, with the trend being self-reinforcing and seemingly unbreakable.

On the other hand, the unraveling of the post-WW2 world order seems to be picking up pace, and the magnitude of the shift is now arguably growing exponentially. The weaponization of our financial and tech dominance is eroding trust, and as we can now see, it is leading to alternate institutions being born and spreading, perhaps faster than most originally thought that it would. The main flaw in this approach to foreign policy is that the sanctions are aimed at a country like Russia, which is the world’s largest net exporter of commodities as well as intermediary products derived from those commodities. The world cannot stop trading with Russia, without suffering great economic and social harm, therefore new institutions and entities are inevitably born out of the need to go around some of the sanctions that were imposed.

The mere freezing and declared intent to try to find ways to outright confiscate Russia’s central bank assets is also causing most countries around the world reason to pause and ponder what it means to them. When we declare our willingness to cross the line, sacrificing the institution of respect for property in the name of ethical judgments, which could arguably set a dangerous precedent, it leaves most countries feeling exposed and vulnerable. We are thus potentially looking at a situation where investors and entities sitting on trillions of dollars’ worth of US debt are losing faith in our willingness to uphold property rights and are therefore looking to find alternatives and then unload their current positions. In the event that there will be a new flight to safety this year, in response to bad economic news coming our way, it is unclear at this point in time whether US debt will still serve as the historical flight to safety go to investment position, therefore, the GOVT ETF fund is now arguably a somewhat risky safe haven play.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.