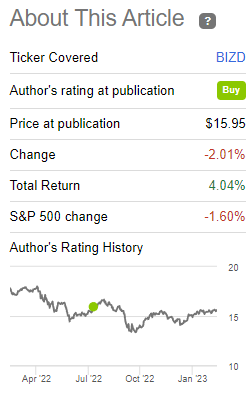

BIZD is a BDC index ETF. The fund offers investors a strong, growing 10.2% yield and a cheap valuation. Fundamentals have improved these past few months too, even as the fund outperforms the competition.

BIZD: BDC Index ETF, Strong, Growing 10.2% Yield, Cheap Valuation, Improved Fundamentals

I last covered the VanEck Vectors BDC Income ETF (NYSEARCA:BIZD), a business development company, or BDC, index ETF, in mid-2022. In that article, I argued that BIZD’s strong, growing yield and cheap valuation made the fund a buy. The fund has outperformed since, as expected.

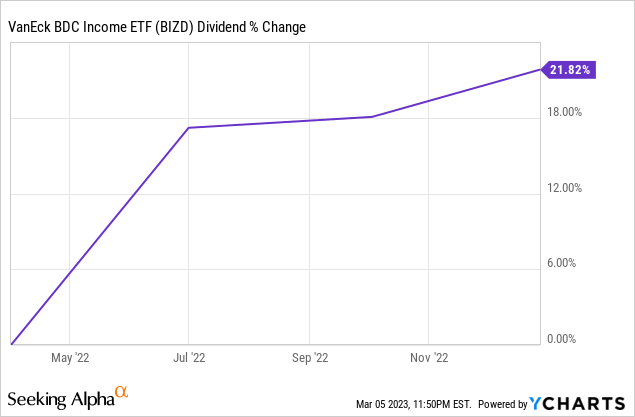

Since my previous article, BIZD’s dividends have seen very healthy growth, while performance and fundamentals have slightly improved.

BIZD’s strong, growing 10.2% dividend yield, cheap valuation, and improved fundamentals make the fund a buy.

BIZD – Quick Overview and Investment Thesis

A quick look at the fund before a more in-depth look at how it has performed these past few months, and at its improved fundamentals.

BIZD is a U.S. BDC index ETF. BDCs are financial institutions which provide funds, generally loans, to small and medium sized enterprises. BDCs are generally diversified, although less so than the average mega-cap bank, and smaller too.

BDC loan portfolios are effectively always of below-average quality, due to focusing on smaller, riskier issuers. Default rates are higher than average, and tend to spike during downturns and recessions. Expect significant losses and underperformance during these, as was the case in 1Q2020.

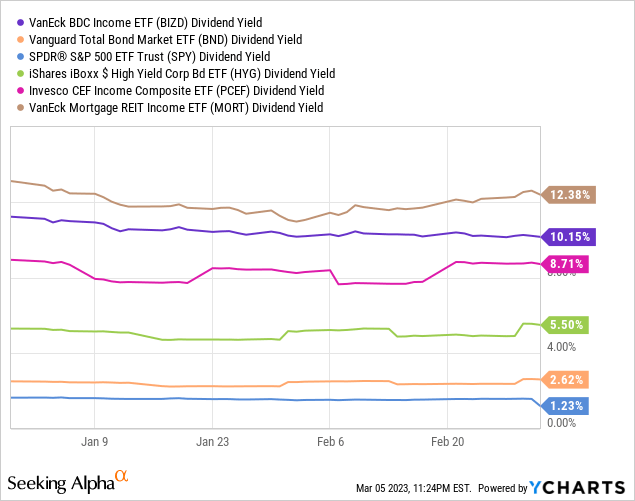

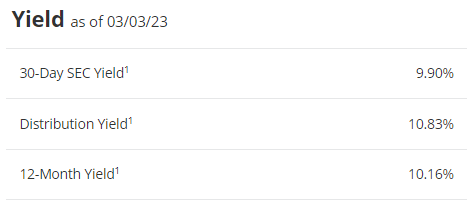

BDC loans are risky, but also relatively high-yielding, with interest rates in the 8.0% – 12.0% range. BIZD itself yields 10.2%, an incredibly strong figure, significantly higher than the yield offered by most asset classes, and comparable to that of the highest-yielding income assets.

BDC loans tend to be variable rate loans, and so tend to see higher coupon rates when benchmark interest rates increase. Increased interest rate payments flow to the BDCs, which flows to BIZD, which ultimately flows to BIZD’s investors as dividends.

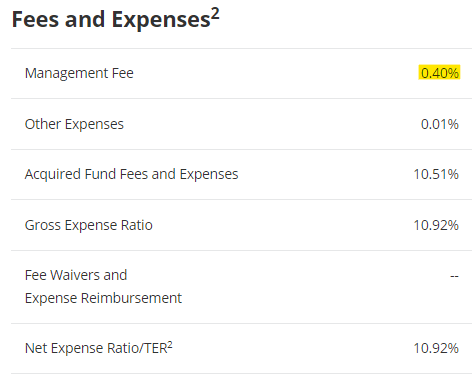

BIZD has a management fee of 0.40%, somewhat higher than average for an index fund, but about average for a niche industry fund. For regulatory reasons, BDC expense ratios must include operational expenses, meaning salaries and the like. Due to this, BDC / BDC fund expenses ratios are incredibly high, but not comparable to those of other funds. BIZD itself has an expense ratio of 10.9%, but its 0.40% management fee is the more pertinent metric.

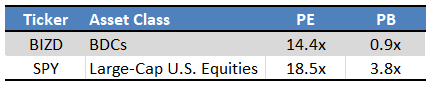

BIZD sports a below-average valuation right now. Said valuation could lead to significant capital gains moving forward, a benefit for the fund and its shareholders.

BIZD’s investment thesis is quite simple. The fund offers investors a strong, growing 10.2% dividend yield, and a cheap valuation, so income, capital gains, and total returns are, potentially, all quite strong.

With the above in mind, let’s have a closer look at how fundamentals have evolved these past few months.

BIZD’s Improved Fundamentals

Stronger, Growing Dividends

BIZD’s dividends have seen very healthy growth since at least early 2022. Quarterly dividends have grown over 21.8% since the same, 13.2% on a TTM basis.

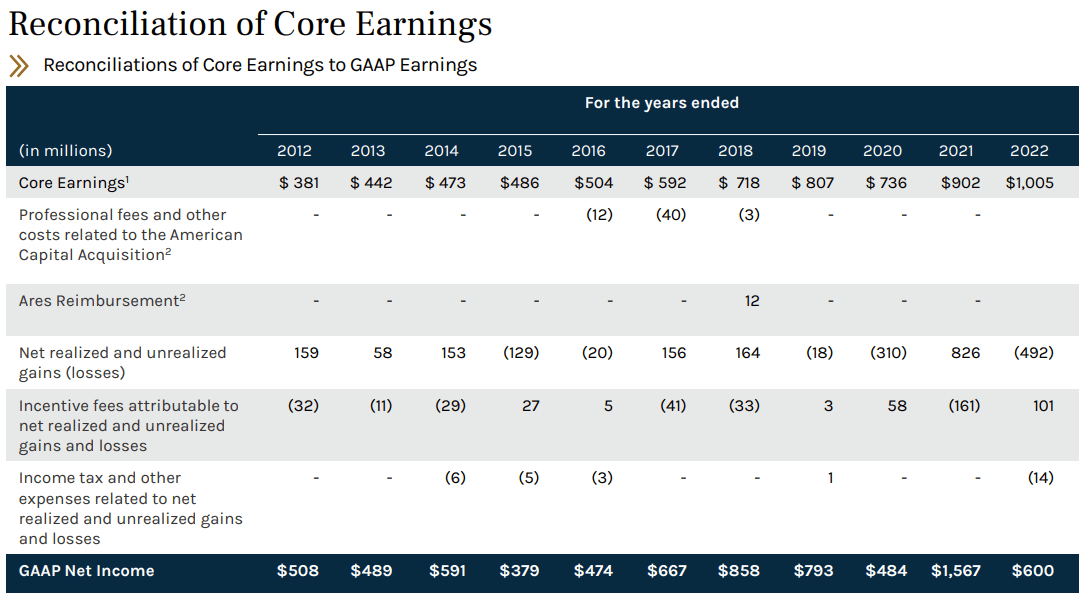

Dividend growth was almost entirely due to Federal Reserve interest rates which, as BDCs focus on variable rate loans, quickly leads to higher BDC loan interest rates, higher BDC income, higher BIZD income, and (finally) higher BIZD dividends. I do hope the process makes sense, it is a bit lengthy but quite logical, and surprisingly smooth. BDCs themselves have said that higher interest rates are beneficial to their portfolios and financial performance. As an example, we have Ares Capital (ARCC), BIZD’s largest holding:

Our 2022 earnings significantly benefited from the increase in market interest rates driving a 17% increase in net interest and dividend income per share as compared to 2021.

BIZD’s dividends are likely to see further growth moving forward, for two key reasons.

First, due to the delayed impact from recent interest rate hikes. It generally takes a few months for variable rate loans to reset their coupon rates, a few more months for BDCs to hike their dividends as their interest rate income increases, and a few more months for BIZD itself to hike its dividends. As such, past interest rate hikes should lead to strong dividend growth for at least a couple more months.

Second, due to the possibility of further interest rate hikes. As per AP, investors seem to be expecting around 0.50% in further hikes, compared to 0.75% for Federal Reserve officials. Said hikes would almost directly lead to higher variable rate loan rates, and hence higher BIZD dividends. This is, of course, contingent on future Fed policy, which is not set in stone.

Finally, fund dividends are almost entirely covered by underlying generation of income, as per the fund’s 10.1% SEC yield. Around 0.1% of the fund’s yield is not covered, but this is almost certainly due to volatility in income, interest, share prices, etc.

BIZD’s strong, growing 10.2% yield is a significant benefit for the fund and its shareholders.

Stronger Performance

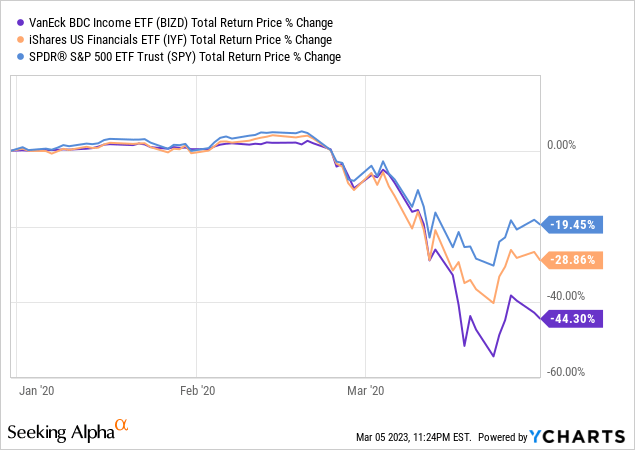

BIZD’s long-term performance track-record is somewhere between adequate and sub-par, with the fund underperforming the S&P 500 since inception. Performance is rapidly improving, with the fund only slightly underperforming these past five years and outperforming since early 2021.

BIZD’s improved performance is due to the fund’s growing dividends, and a market shift towards value stocks and income, and away from growth and tech. The fund underperformed ten years ago, when yields were in the 6.0% – 7.0% and tech was riding high, but it is outperforming today, with yields in the 9.0% – 11.0% range, and with renewed investor demand for these and other income assets.

BIZD’s improved performance track-record benefitted investors in the past, and is a positive signal for investors right now / in the future. The fund is performing much better now that its yield is higher and growing, and performance could very easily continue into the future.

BIZD Other Recent Developments

Valuation

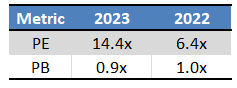

BIZD’s valuation has evolved in, well, complicated ways these past few months.

PB ratios are slightly down, mostly due to underlying BDC portfolio growth (larger portfolios = higher book value per share).

PE ratios, on the other hand, have more than doubled, due to significant capital losses (negative earnings) from lower bond prices. Prices are down due to higher interest rates and widening credit spreads. These capital losses will almost certainly prove to be (mostly) temporary, as loans must always be repaid in-full at maturity. Underlying interest rate income is up, even as accounting earnings are down. As an example, ARCC saw double-digit core earnings growth in 2022, in large part due to higher interest rates.

As BIZD’s higher PE ratio is mostly due to accounting conventions, I don’t really see it as a negative per se. Still, thought it important to analyse these metrics.

Recession Fears

Economic conditions have worsened these past few months, as skyrocketing interest rates reduce consumer demand and increase borrowing costs. Conditions remain quite good, with strong economic growth in 4Q2020, job growth in January. Conditions are expected to worse, with most analysts expecting higher defaults rates this year. Base case scenario for most analysts is a shallow recession, with a moderate increase in defaults, but with these remaining within normal parameters.

Worsening economic conditions and higher default will almost certainly be a headwind for BIZD this year. If conditions were to significantly worsen, the fund would almost certainly see significant capital losses and dividend cuts. A more shallow recession would have a smaller, although still negative, impact. Do remember that BDC loans do sometimes enter into default. BDCs expect at least some defaults, and are, or should be, well-prepared for a small number of these. I’m quite bullish, so I don’t see these recession fears as a deal-breaker. More bearish, conservative investors might disagree, and might prefer to focus on higher-quality, safer funds.

As a final point, do remember that investors were concerned about a recession in 2022, and the economy did slow down during the first half of the year, and BIZD did just fine regardless. The same could very well be true in 2023.

Conclusion

BIZD’s strong, growing 10.2% dividend yield, cheap valuation, and improved fundamentals make the fund a buy.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.