ECH invests in Chilean stocks.The fund is probably at least modestly undervalued, with a net IRR of over 16% possible.However, the fund’s annualized volatility is high as measured by standard deviation. Meanwhile, idiosyncratic risks prevail for ECH shareholders.On balance, I would opt to take a neutral stance on ECH, given the fund’s high level of concentration.

ECH: Chilean Stocks Offer High Potential Returns But Not Without Volatility

iShares MSCI Chile ETF (BATS:ECH) is an exchange-traded fund that provides investors with exposure to Chilean stocks. The fund seeks to track the performance of its chosen benchmark index, the MSCI Chile IMI 25/50 Index. This is a capped index with the most important point being that the largest position cannot exceed 25%. The uncapped version of the index has a larger position in the leading position of both; that is, Sociedad Quimica y Minera de Chile SA Pref B (SQM) at just under 20% for ECH’s index. More recently though, SQM represented just under 17% of ECH’s fund as reported by iShares themselves as of April 21, 2023.

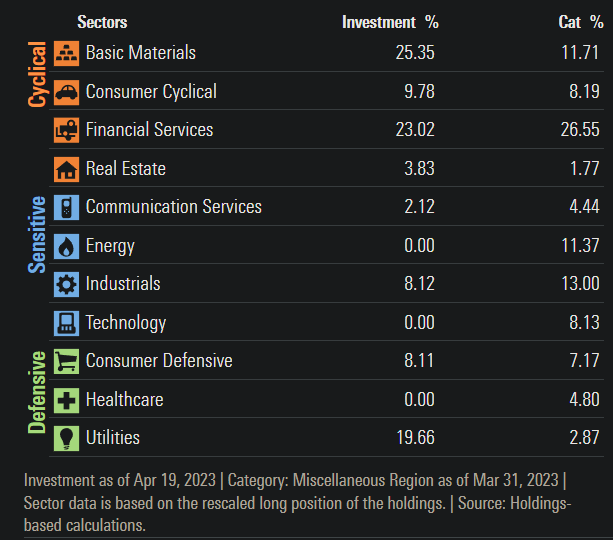

In English, SQM’s company name translates to “Chemical and Mining Company of Chile”. SQM is a chemical company and supplier of plant nutrients, iodine, lithium and industrial chemicals. It is the largest producer of lithium in the world. The company’s natural resources and its main production facilities are located in the Atacama Desert in Tarapacá and Antofagasta regions (both in the North of Chile). The rest of the fund, as per Morningstar’s ECH key sector exposure breakdown, is in a mix of financial services and utilities. This is characteristic of lesser developed nations (or at least less developed equity markets).

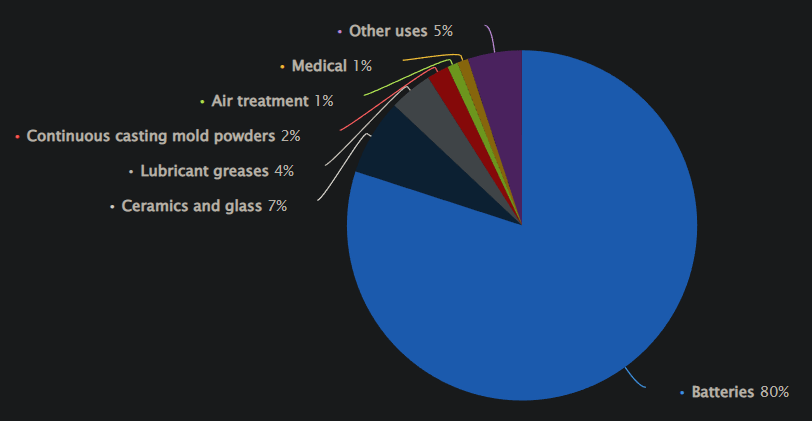

The fund is small and highly concentrated, though. ECH had 27 reported holdings as of April 21, 2023. The significant SQM exposure means that ECH is significantly exposed to worldwide Lithium demand, commodity prices in general, SQM’s production capacity and output, government regulations, global economic conditions, FX fluctuations (especially with respect to the U.S. dollar), and more. Lithium demand is one of the more important factors; in 2022 (as illustrated below) about 80% of demand for the element in terms of end usage was for batteries.

Lithium is used to produce electric vehicle (or “EVs”) batteries and other energy storage applications. A rise in the demand for EVs and renewable energy storage solutions could lead to increase global demand for lithium, which should benefit SQM. So, ECH is generally well positioned for the future in this regard. The demand for lithium is indeed expected to grow over the long term. On the other hand, there are some credible alternatives to lithium for batteries in EVs; most may be in R&D stages, but ECH could certainly take a significant hit should the demand for lithium be supplanted at some point. SQM is a materials company, not a technology company. If a “materially adverse event” occurred for lithium demand, ECH would likely suffer a significant correction.

Chile itself is also a relatively unsophisticated economy, ranking about 74 out of 131 countries for economic complexity. This is supported by ECH’s large exposures to materials, financial services, and utilities (not so much consumer discretionary, technology, healthcare, etc., as you typically see in more developed countries’ equity markets).

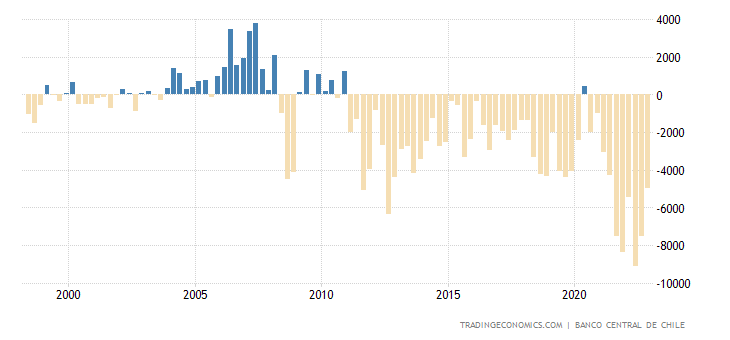

ECH also owns stocks ultimately denominated in Chilean pesos. The Economist’s Big Mac Index considers the peso to be roughly fairly valued, on a GDP-per-capita adjusted basis. However, Chile’s current account is deeply negative, indicative of over-valuation.

While the U.S. current account does not look “good”, either, the U.S. dollar is still considered to have the privilege of being “the” world reserve currency. Having said that, the peso is at around multi-year lows, so I do not think the currency is actually at significant risk as such.

Politics is usually another area of key risk, especially among less developed nations. However, Chilean politics is relatively “stable”. Gabriel Boric, a left-wing leader, was the youngest elected president (December 2021) taking office in March 2022. Nevertheless, while constitutional changes may eventually be made in the country, progress seems to be viewed generally positively (in the direction of supporting rather than hindering democratic ideals), and Boric also set a record for receiving the highest number of votes in Chilean history. We can say that the country is politically stable and well-functioning.

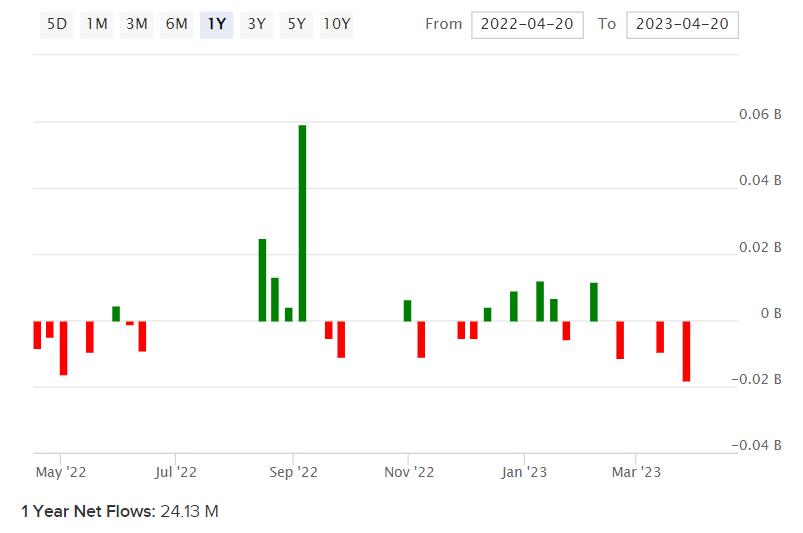

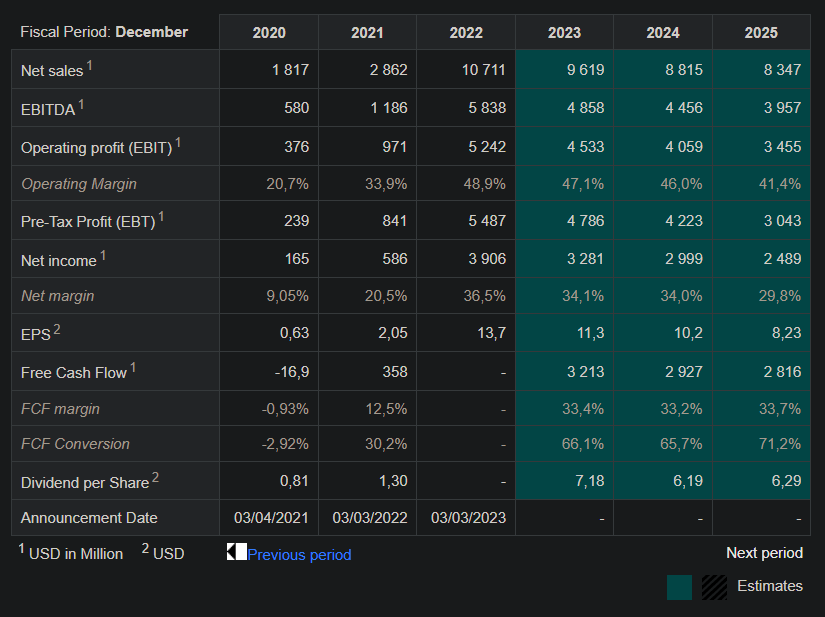

Moving on to the fundamentals of ECH: the fund carries an expense ratio of 0.58%, with assets under management of about $519 million as of April 21, 2023. The fund has seen relatively stable net fund flows over the past year or so, as depicted below.

Morningstar reports a forward projected price/earnings ratio of 6.77x, with a price/book ratio of 1.03x. iShares meanwhile report a trailing price/earnings ratio of about 4.91x. I will hold most factors constant in my projection. However, it is notable that projections from one website for SQM (which sources data from S&P Global Market Intelligence) suggests SQM’s earnings trajectory is downward over the next few years, which is in line with a drop in the overall earnings for ECH over the next year based on the differences in trailing and forward price/earnings ratios I found.

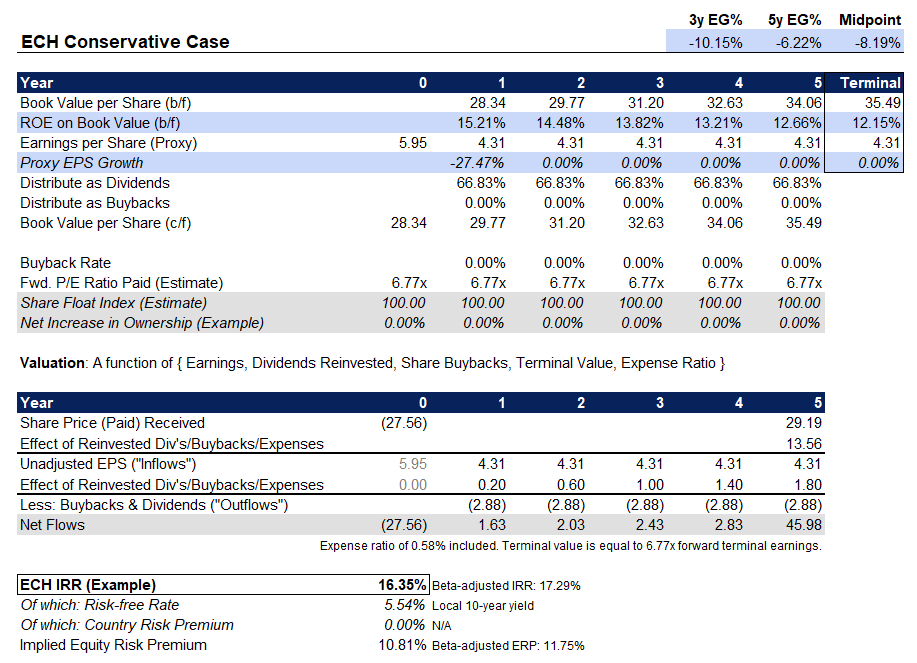

Therefore, I am uncomfortable with Original Postortfolio">Morningstar’s anticipated 8.23% three- to five-year average earnings growth rate. Instead, I am going to use forward earnings as a base and assume 0% earnings growth thereafter, to start with. This sets a baseline estimate.

The upshot is that ECH seems to offer a high return, even assuming that earnings are fixed from year 1 onward. It is true that the previous projections for SQM earnings are even worse than 0% for the next couple of years. Nevertheless, on a portfolio level, let’s assume that ECH maintains flat earnings (this could potentially result in SQM becoming a lesser part of the portfolio). The net IRR potential is some 16.35% per annum, which is high, even in spite of a relatively high local risk-free rate of 5.54%.

However, using historical data for ECH, I calculate annualized volatility of about 30-35%. That means that the net IRR potential, if we assume it is 16% or so, is close to half the annualized volatility, and more like 0.4x if we take into account the current local risk-free rate. This means that while the headline IRR for ECH is strong, the volatility-adjusted return is not nearly as good, and so while ECH might out-perform broader markets, this would be a more volatile bet on a cycling global economic upswing. ECH, as we have covered, is highly concentrated too, and not without that associated idiosyncratic risk.

All considered, I think ECH is probably at least modestly undervalued, given the high IRR beats the sum of the risk-free rate and any reasonable approximation of the equity risk premium (to include Chile’s country risk premium). On the other hand, ECH is not without volatility. On balance, I am neutral on ECH: interesting from the perspective of SQM, but I think more investigation should be placed on that company specifically, if anything. The rest of Chile’s portfolio is not particularly interesting, and I don’t think the fund’s underlying return on equity of circa 15% is attractive for an emerging market. SQM also pays much of its earnings out in dividends, and it is fundamentally not a technology company. I think better opportunities exist elsewhere in ETF investing.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.