Introduction

A Chinese site, newcar.xcar.com.cn, lists domestic discounts; it’s dynamic, so the numbers in late May are different from my May 2nd screenshot below. In that screenshot, I focus on the mid-range price brackets relevant to NEVs (new energy vehicles). Units are 元10,000 or about US$1,400, so the top right car (the VW Tiguan) has a discount of $5,600 or 24% on a $23,000 vehicle. I won’t translate, but you can pick out a few model names if you’re a car gal or guy. Of course the Model Y doesn’t show a discount, because Tesla has lowered the list price directly. [If you read Chinese, you can navigate the website to find details of discounts down to specific trim levels.]

The takeaway: discounting is rife. That’s nothing new. In China, the US and Europe cars get discounted as the model year progresses, with the biggest discounts employed to clear inventory before the launch of a successor model. But current Chinese discounts are large, and are on best sellers such as the Honda CR-V (225,000 sold in 2022) and the VW Tiguan L.

Car Discounts in China (newcar.xcar.com.cn)

Given discounting, what’s happening to sales? The disappointing bottom line: not enough. The conclusion is straightforward: if gross margins are 10% of sales, then double-digit discounts erase all profits.

Details follow. I present data through April 2023, from a database I’ve built up that covers 75 manufacturers and 787 domestically produced passenger models, of which 599 models and 61 manufacturers remained in Q1. That’s right, since I began collecting data in January 2020, 14 firms have folded, including 12 that focused on EVs.

More bankruptcies will follow.

[Note that my data exclude commercial vehicles and imports, respectively of 3.3 million and 800,000 in 2022. Add in 20.6 million domestic passenger vehicles, and the total Chinese market in 2022 was 24.7 million units. Europe including Russia and Turkey was 15.1 million units, USMCA was 16.9 million units. Sources: my database for China, and OICA.net for Europe and USMCA.]

Overall sales are up, but modestly

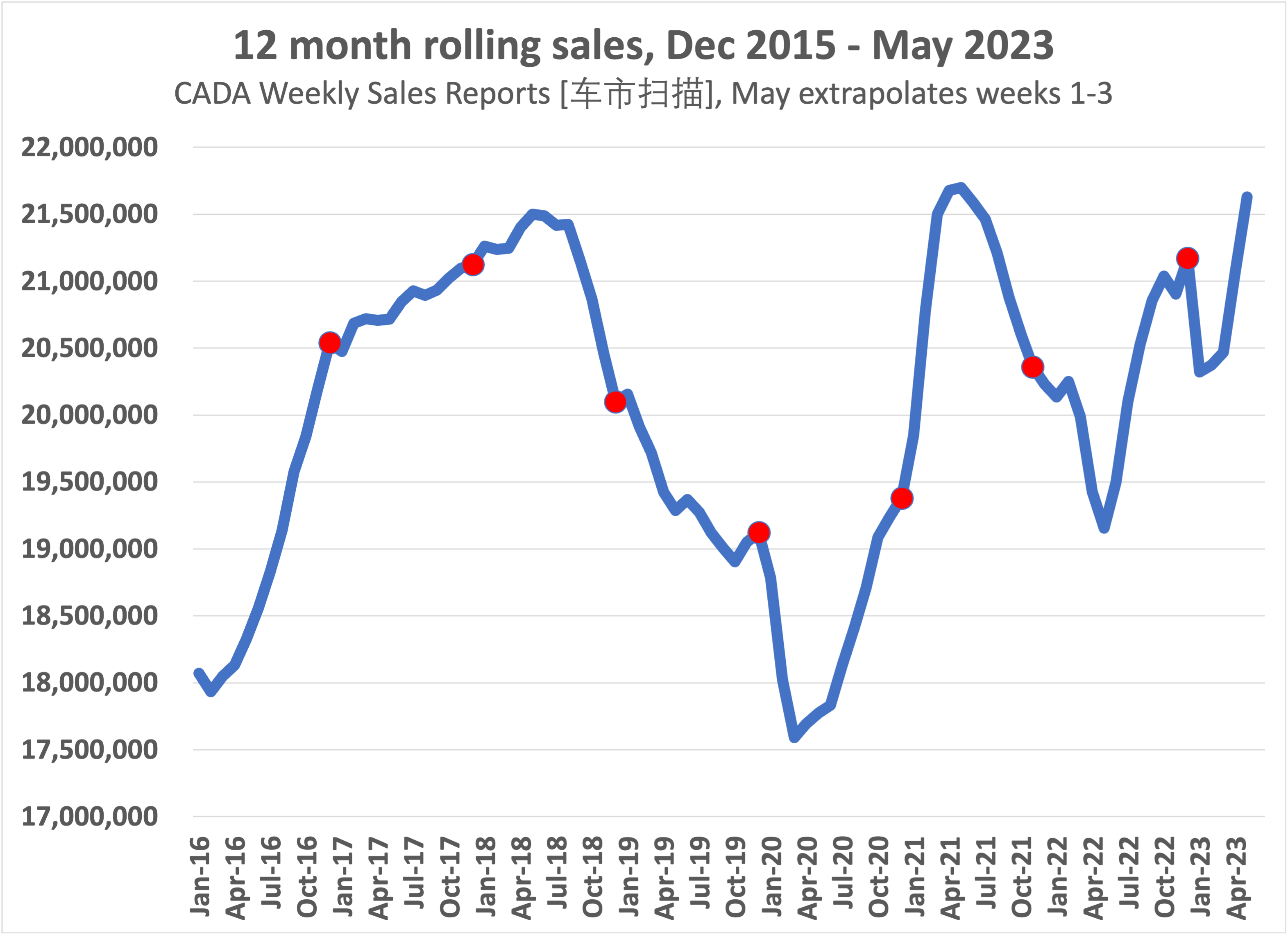

The vehicle market in China peaked in 2017, and demographics, the end of rural-urban migration, and slowly rising consumption mean sales will remain flat going forward. While incomes will continue to rise, and hence the rate of car ownership, most of the 273 million passenger vehicles on the road are less than 10 years old (2020 OICA data). The current sales rate thus supports a continued increase in the total “parque”. I thus believe that the modest economic growth in China’s future will not lead to a steady rise in the sales of new vehicles, unlike in Japan, where sales are steady despite the decline in the driving-age population.

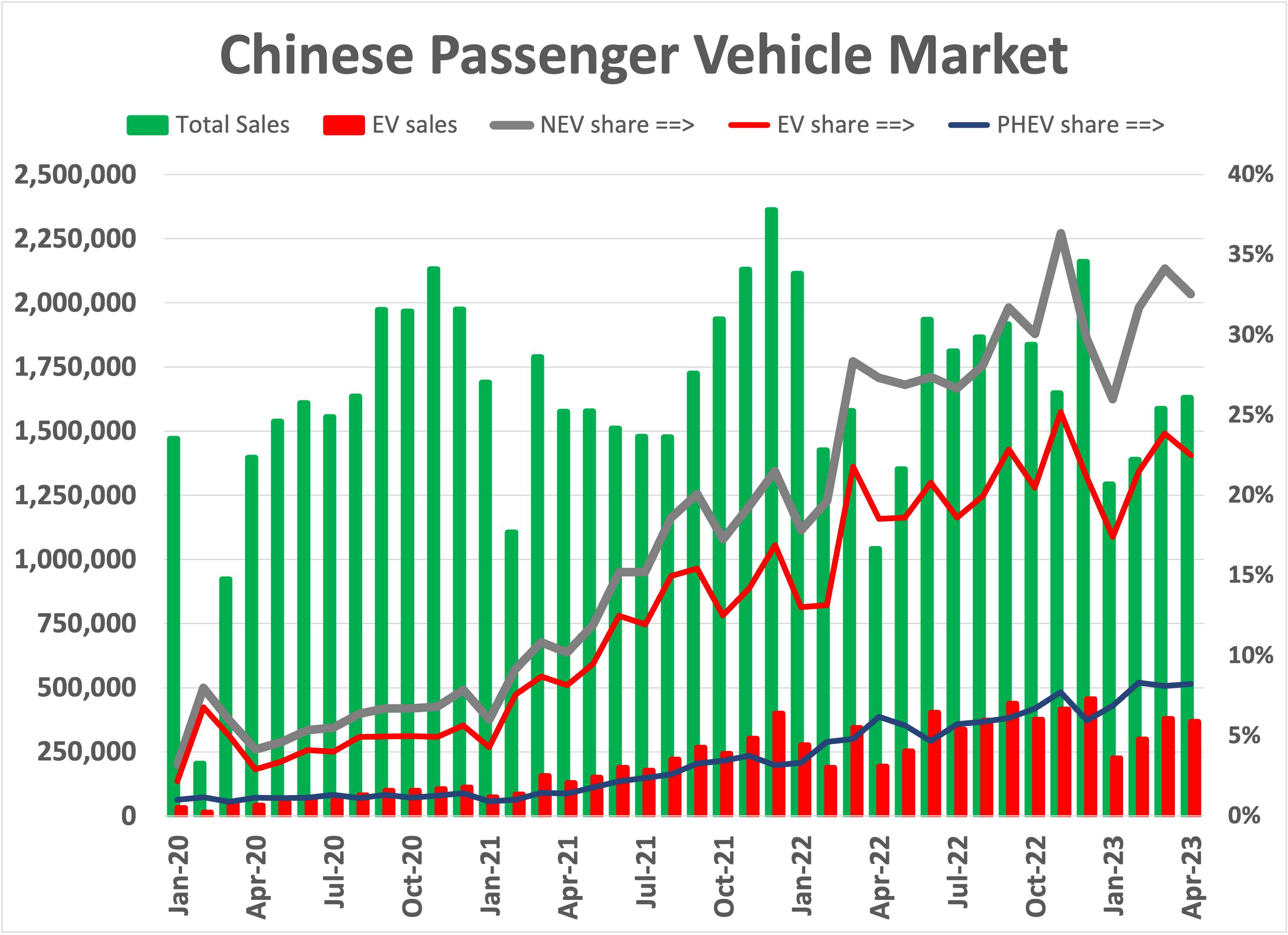

Two graphs illustrate this. The first gives monthly sales since January 2020 – I won’t have detailed data for May for another 3 weeks, ca June 15. Of particular note is that the steep increase in the share of NEVs is muting. Indeed, over the past year the share of EVs is flat. Without a rising tide, EVs have to capture market share to increase sales, and the big, wealthy urban markets already have a high share of EVs – in January NEVs were 45% of Shanghai passenger vehicle sales. NEVs don’t fit every consumer’s use case (or budget), and I believe that we are seeing the saturation of the biggest NEV markets, which are in Shanghai, Guangzhou, and a handful of other major urban agglomerations.

Chinese Passenger Car Sales (Author’s database, various underlying sources)

Now forecasting is hard, or there’d be no “alpha” to pursue. For the Chinese auto market, Covid sales incentives and longstanding NEV incentives both ended on January 1st, pulling sales from early 2023 into late 2022. At the same time, covid lockdowns affected sales in many parts of China, so not everyone who wanted to buy a car could. Sales did indeed plummet in January, but they were also affected by an early Chinese New Year, when most businesses closed. Even with hindsight, that makes teasing out what has happened so far this year hard.

(Aside: the NEV exemption from the national 10% vehicle acquisition tax will continue through Dec 31st, 2023. In addition, some two dozen prefectures, large cities, and city districts provide ad hoc trade-in subsidies, additional license plate allocations, and subsidies for purchasing a locally produced model. Many are set to expire by end-summer 2023. I don’t track in detail, and don’t have local sales data that would allow me to evaluate their impact.)

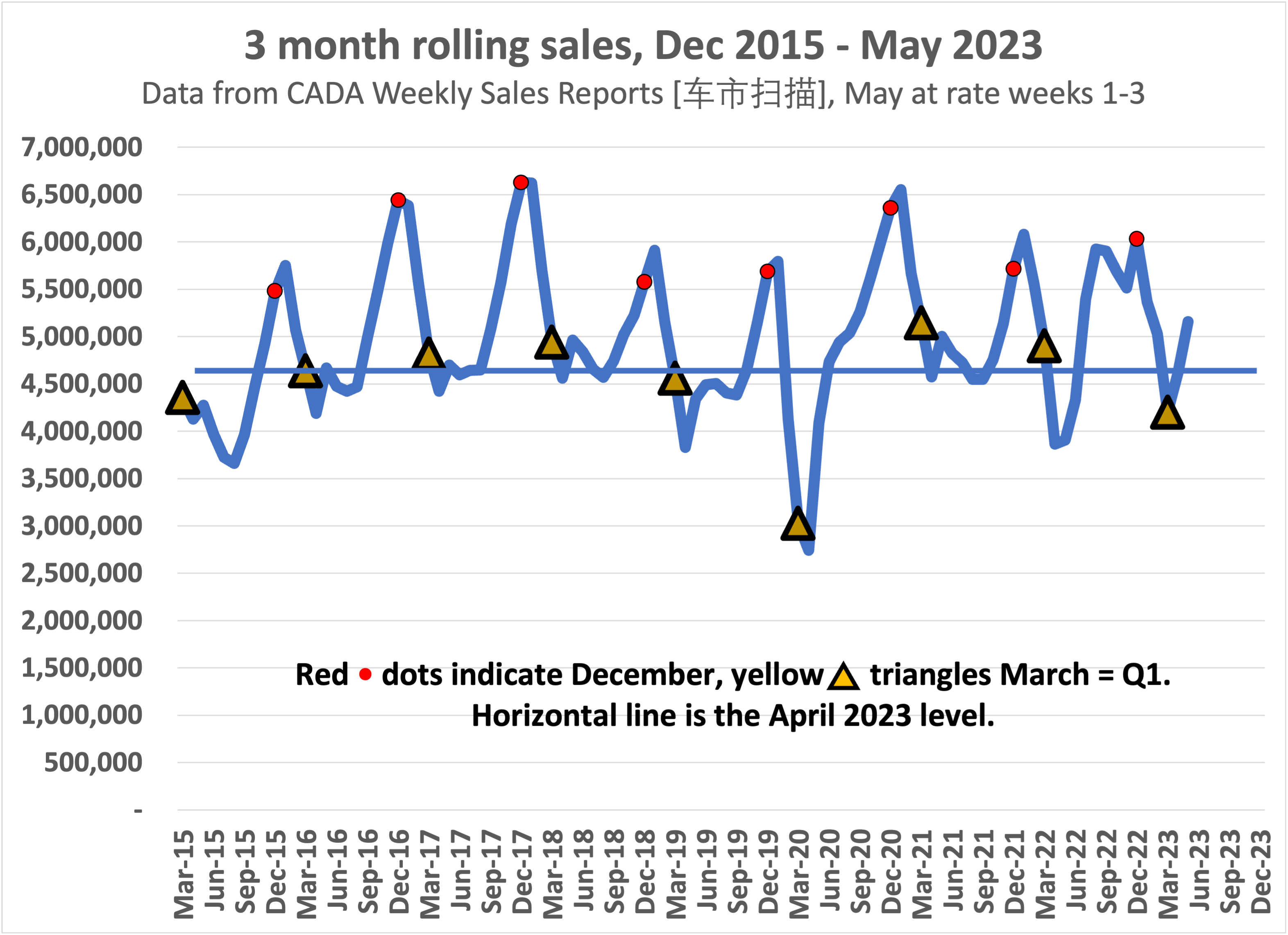

So are we seeing a rebound? Maybe. 2023Q1 sales were the worst since 2015 (as 2020Q1 was exceptional, reflecting China’s nationwide covid lockdown). However, projecting from April and the first 3 weeks of May, we are not seeing the normal pattern of lower late spring sales. In addition, I (and other industry observers) expect the normal fall sales uptick. So 2023 looks likely to set a new sales peak. But don’t get excited: some portion of volume indicates sales of heavily discounted vehicles that won’t meet the new China 6b emissions standards that take effect July 1st. Absent those models, Fall 2023 sales will be good, not great.

To reiterate: in the top graph, the share of EVs is stagnant. The recent increase in the New Energy Vehicle (NEV) share is due to the uptick in plug-in hybrid sales (PHEVs). Car companies are acting accordingly. So far in 2023, that is through the 3rd week of May, we’ve seen the launch of 28 new EV and 21 PHEV models. By this point last year there were 20 new EVs but only 10 new PHEVs. Competition in the EV segment is stiffening, but the industry is increasingly looking to PHEVs. (Source: CPCA data, my categorizations of 258 new models. My EV/PHEV count excludes those that represent minor changes to existing models, such as additional trim levels, modified exterior fascias and updated interiors.)

Rolling 3-month sales (Author’s database, various underlying sources)

Rolling Annual Sales (Author’s database, various underlying sources)

Source: My database. Red dots indicate December and hence calendar year sales levels.

Major Players, Major Shifts: BYD up, Global OEMs down

Given China’s outsize role in the global market, who is doing well matters. Analyst reports (I’m not free to cite them) note that has been particularly important for global OEMs, in particular VW (OTCPK:VWAGY). As the sales leader, VW has earned huge direct profits from China, but they also earned indirect income from licensing and from Chinese sales spreading R&D spend across bigger volumes.

Of course most of the output of VW and the other global players comes through joint ventures. (VW does own outright its EV-focused plant in Anhui Provice, acquired from JAC.) Domestic partners share in the profits garnered through sales, and earn additional sums through plant leases and management fees. In the case of VW, their big partners are SAIC (Shanghai Auto Industry Corp, controlled by the government of Shanghai) and FAW (First Auto Works), controlled by the national government. SAIC is also GM’s major JV partner, and GM is the #2 player in China. FAW is also one of Toyota’s two main JV partners. Dongfeng (OTCPK:DNFGF) has Honda (HMC), Nissan (OTCPK:NSANY), Peugeot Citroen (Stellantis STLA) and makes the Dacia Spring EV (Renault RNSDF). GAC (OTCPK:GNZUF) has JVs with Honda, Toyota (TM) and (for buses) BYD (OTCPK:BYDDY), though their JV with Fiat-Chrysler collapsed in 2022. This list of JVs goes on and on.

Global OEMs are now launching NEVs with gusto, but their product offerings are still slim relative to Chinese domestic OEMs, and many won’t have EV-specific platforms with the economies those bring until 2025. In addition, domestic Chinese OEMs are gradually learning branding and sales management, alongside their existing ability to engineer and assemble vehicles to global standards. In reading the Chinese press, Chinese OEMs also lead the global industry in providing the infotainment features Chinese consumers desire. Add in recent lackluster models from global OEMs, and domestic OEMS are gaining share. Details follow.

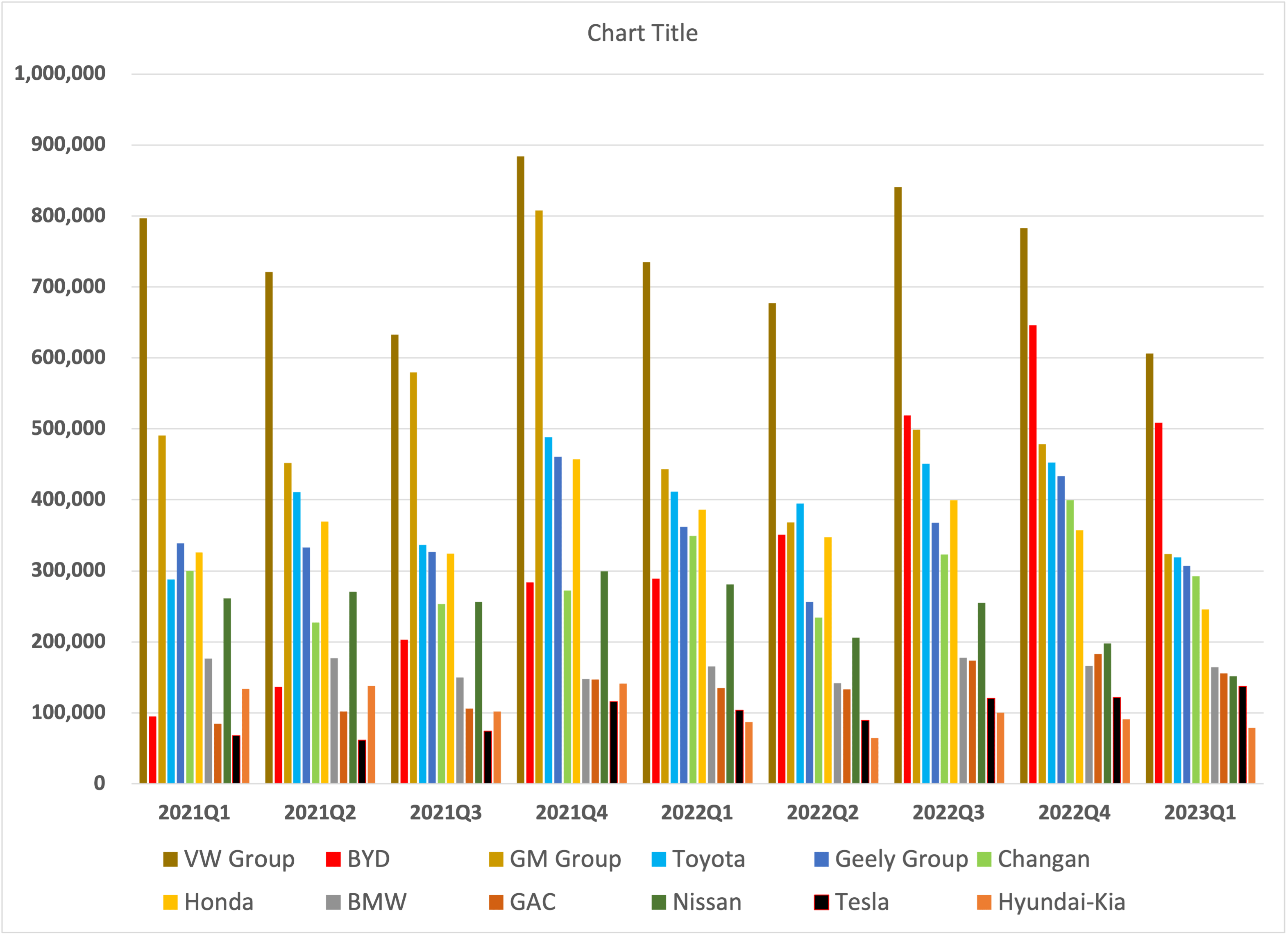

First, while likely hard to read, here are sales for the last 9 quarters of the top 10 players. The rise of BYD in red is clear, as is the decline of VW (dark brown) and GM (GM) (light brown).

Recent sales, China market leaders (Author’s database, various underlying sources)

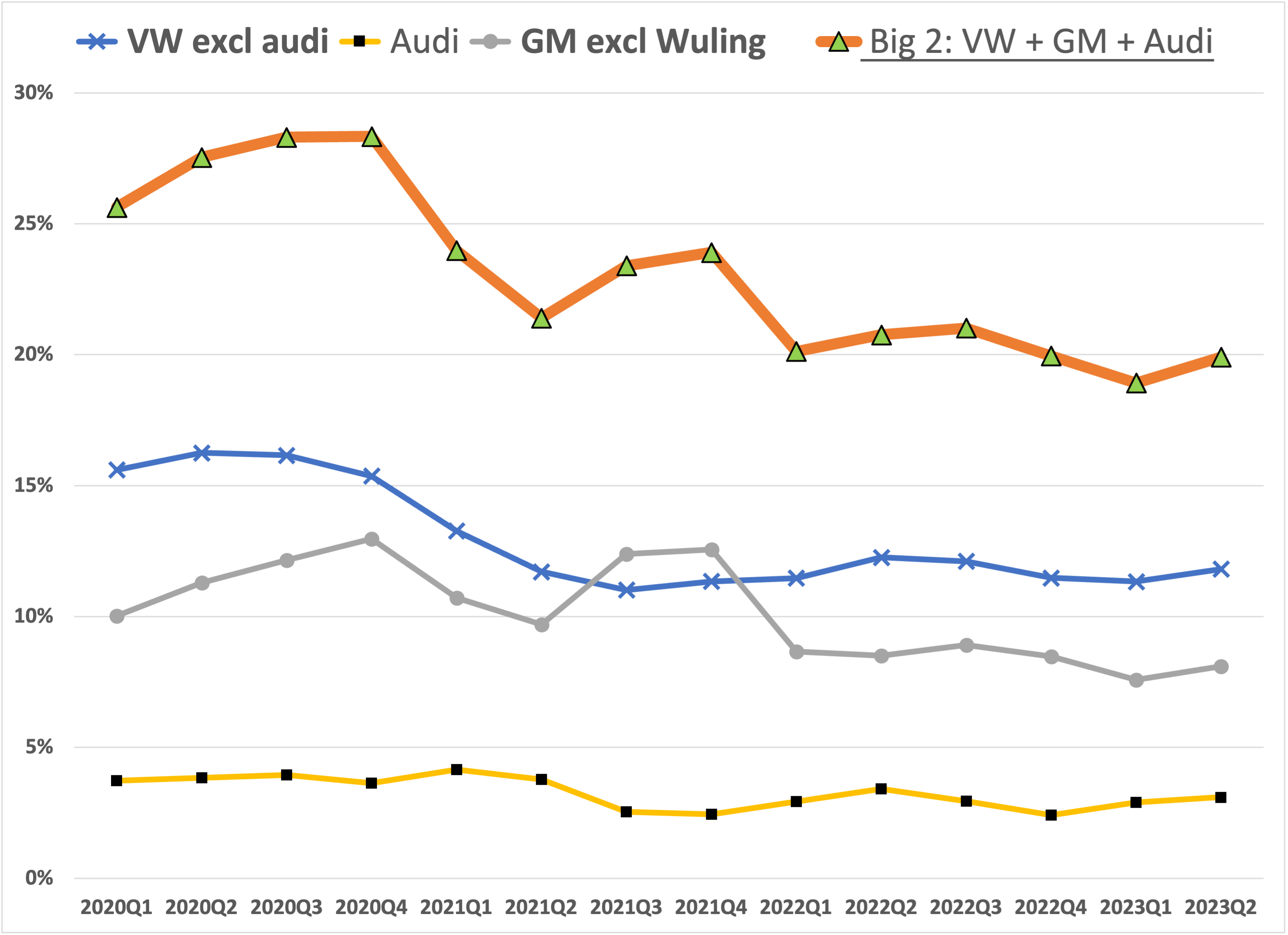

Let’s look at the two historic market leaders, VW and GM, in more detail. Audi has held up OK, and of course is the most profitable major VW brand. (Porsche (OTCPK:POAHY) has is in fact increased its China sales, but I only have a shorter time series for the brand and no model-level data, as no models are assembled domestically. 2023Q1 imports of Porsche were 22,181 and Audi 12,674, down slightly from 2022Q1.) From the recent peak in 2020Q4, VW and GM combined have lost a full 8 percent points of market share, a huge shift.

Recent sales, VW + GM (Author’s database, various underlying sources)

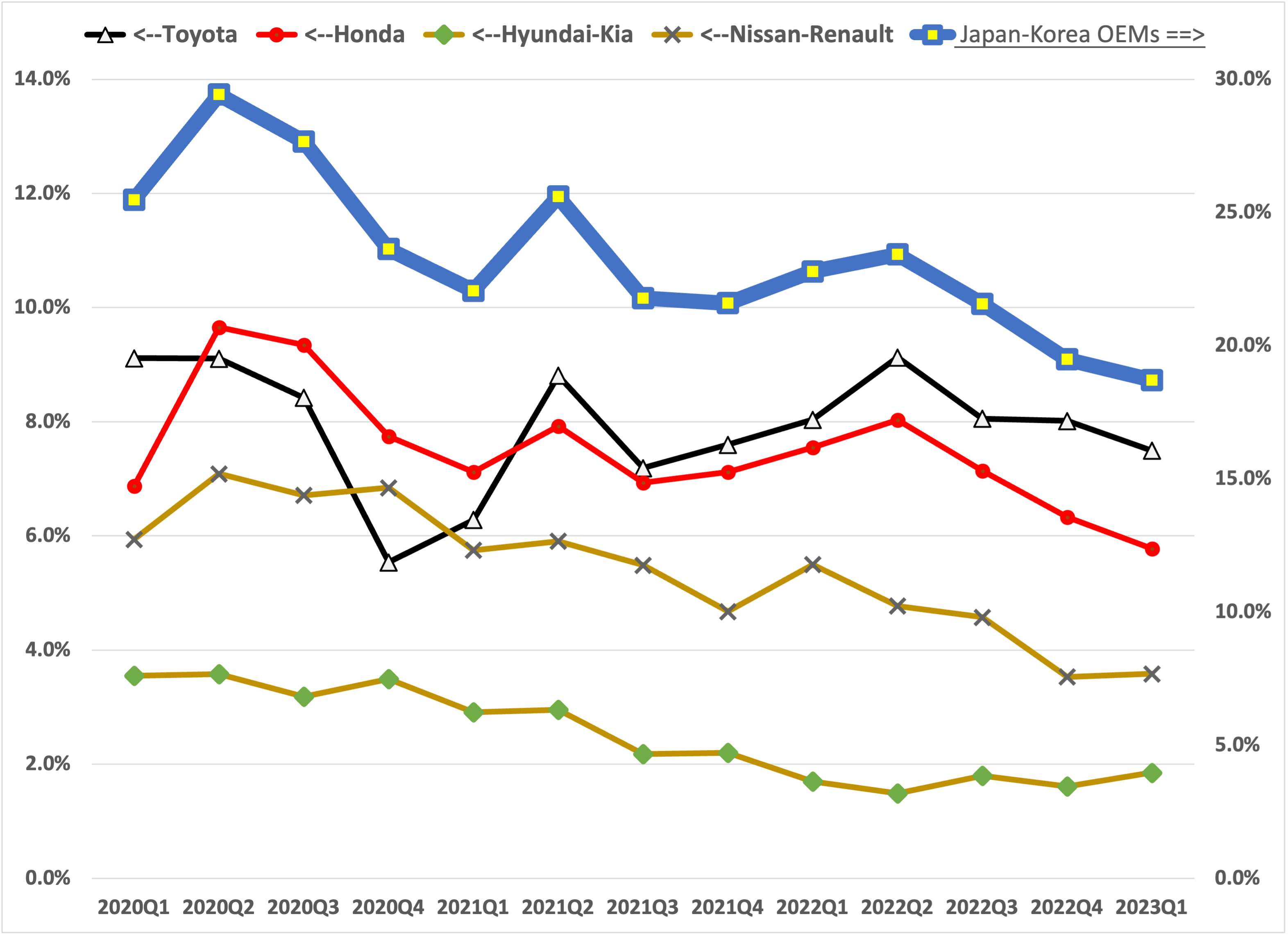

Toyota has fared better, with 8.4% of the market in 2023Q1, not including 38,000 imports, almost all of which are Lexus models. Overall, however, in the aggregate (the right-hand scale) Asian brands have dropped from 29% of the market to 20%, a full 9 percentage points. Again, this represents a huge shift for automotive, where in the US in the 1960s the Detroit 3 battled for fractions of a percentage point.

Recent sales, Asian car companies (Author’s database, various underlying sources)

Combined this is a 17 percentage point decline in market share for global OEMs, and equally for their domestic Chinese joint venture partners. After all, the local partners of global OEMs have been able to show decent profits without having to do well with their own brands. The main exception is Guangzhou Auto, which has the Aion brand, and Toyota (rather than VW or GM) as a JV partner. But FAW [not publicly traded], Dongfeng, SAIC [not publicly traded], BAIC [not publicly traded] and Changan [not publicly traded, Ford is a JV partner) will all suffer.

The NEV Players

On SeekingAlpha the main interest in the automotive sector of course is Tesla (TSLA), but also includes the NEV new entrants that have been able to manage IPOs that make their shares readily available to foreign investors. That means NIO (NIO), XPeng (XPEV) and Li (LI).

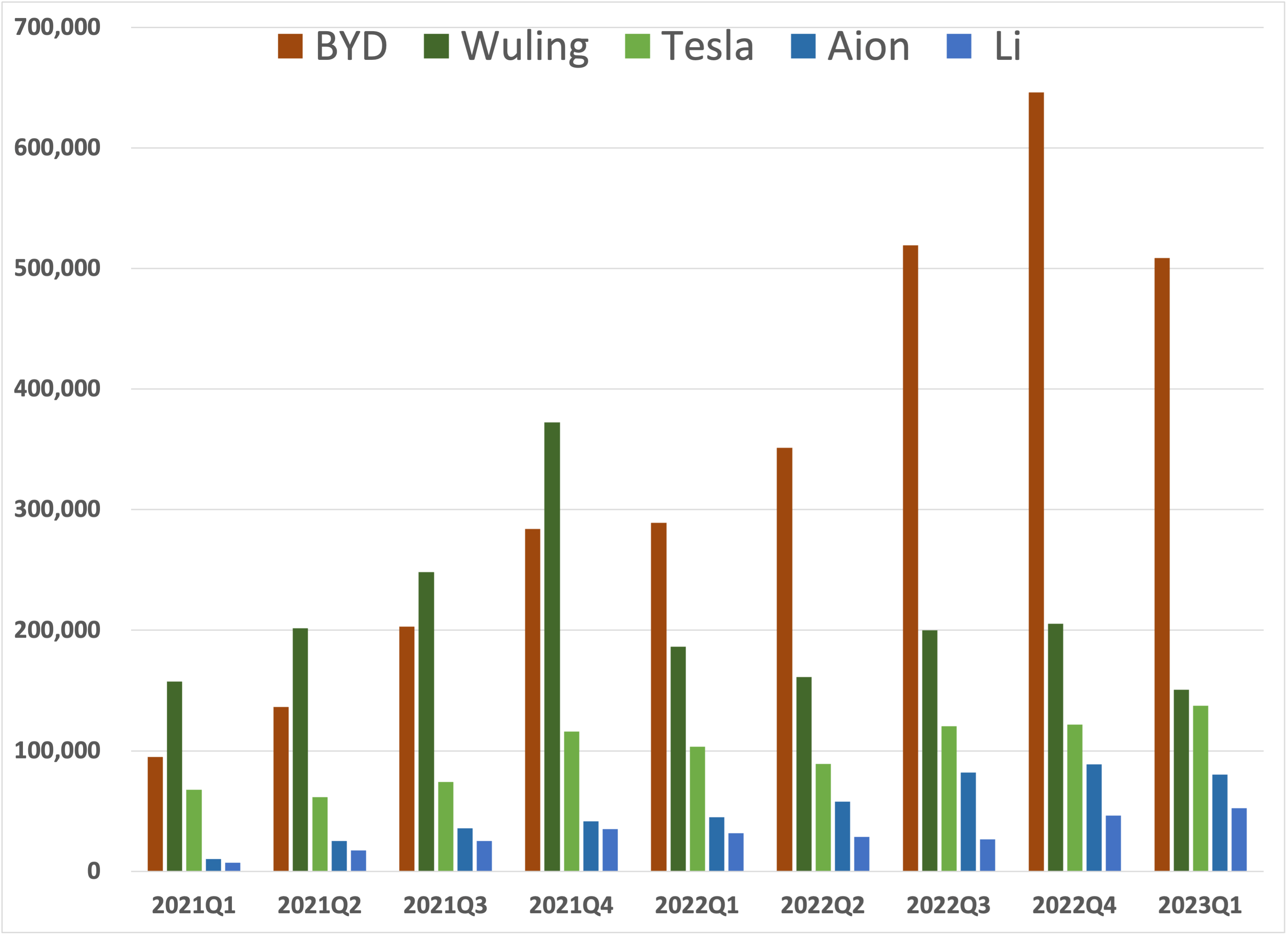

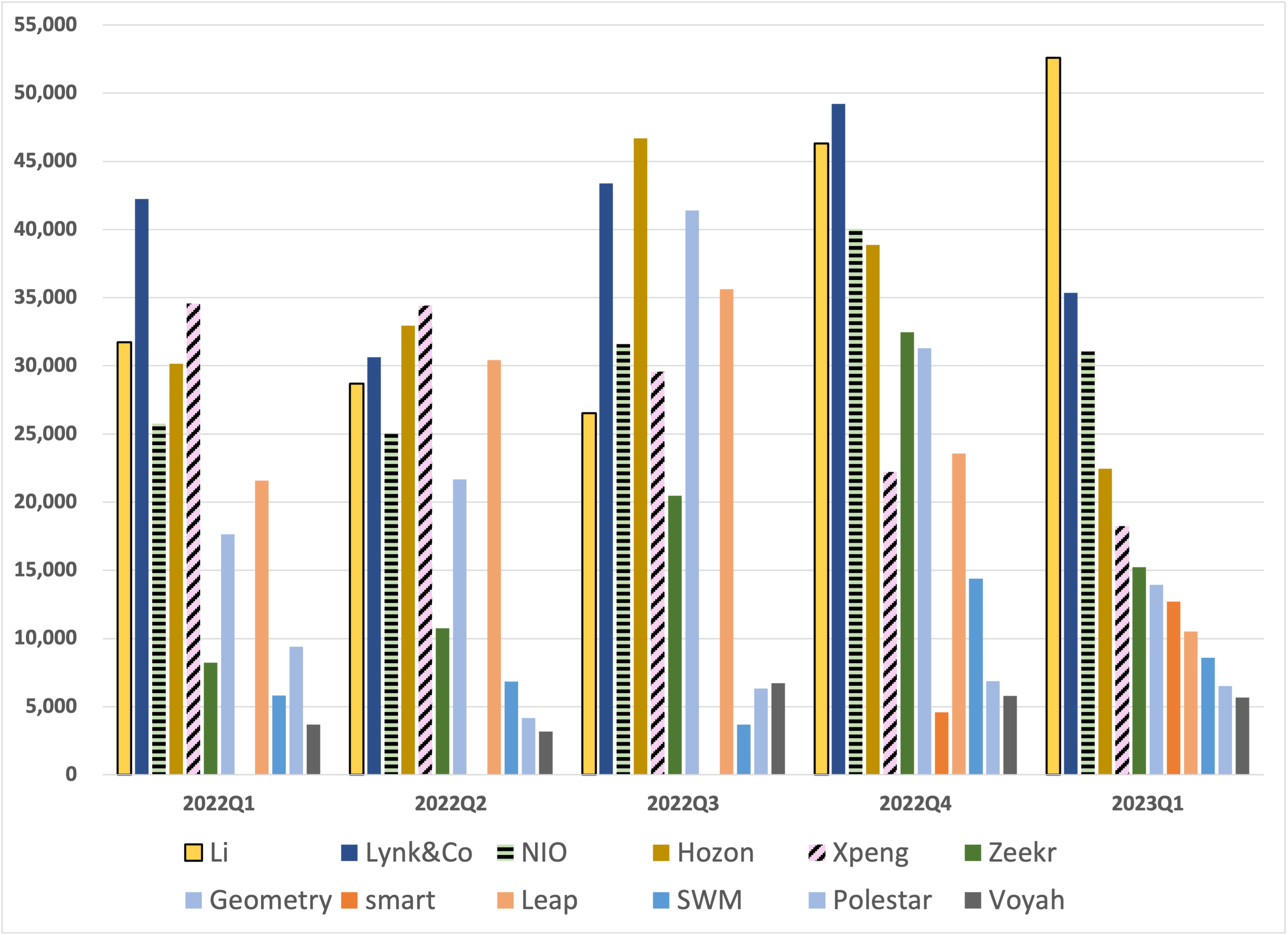

First, below are two charts tracking major and minor EV brands. I include Li in both, to give a sense of the disparity in performance between the major players and the also-rans. Note that new entry continues, with a Daimler-Geely (OTCPK:GELYF) JV producing a smart [branding has it lower-case!] EV from December 2022. Among the smaller players, only Li has increased sales in each of the past 3 quarters, and it is also the volume leader.

Will all these smaller players survive? Wuling [not publicly traded] continues to launch new models, but small, inexpensive cars generate small profits, so it won’t move the needle for GM. However, it is the one potentially disruptive player in the original Clayton Christensen sense of the term, launching a less capable, lower priced model that has created a platform capable of moving up-market. So it remains important to watch over the next couple years, to see whether it achieves such inroads. Wuling also has a base of light commercial ICE sales, and so has a broader market portfolio than the new entrants in China’s NEV market.

Of the others, SeekingAlpha data show only Li to be cashflow positive, and earning a positive net profit. In contrast, NIO’s battery swap business model requires heavy investment in non-vehicle assets, a drain on cash flow relative to its competitors. SA does not have recent cash-flow data, but in 2022Q4 the change in net receivables less payables plus (negative) profits was (negative) US$2 billion against cash of US$5.7 billion. Without a turnaround or major cash infusion, I expect them to collapse by early 2024.

Recent Sales, Major NEV players (Author’s database, various underlying sources)

Recent sales, minor NEV players (Author’s database, various underlying sources)

Exit and More Exit

Exit isn’t a hypothetical, it in fact is prevalent in the Chinese market. My dataset tracks 78 NEV brands with sales at some point between January 2020 and April 2023. Of these, 12 are gone, even though in 2021 they collectively had 130,000 in sales or 4% of the then-much-smaller NEV market. In April 2023 another 18 brands had sales under 1,000 units. At the opposite end, only 6 brands have averaged sales of 10,000 units a month during Jan-Apr 2023. Three other brands exceeded 10,000 in April 2023, Denza (a BYD brand), Hozon and the VW ID brand. Of the 8 firms with monthly sales averaging over 10,000 units – see the table below – only Li and Tesla are pure EV firms, as almost half of BYD group sales are PHEVs, and the other players also sell ICE models. Geely is an interesting player given its strength through Volvo and Polestar in Europe and the USMCA, but I believe it has too many brands. They appear to share a small number of platforms, a big plus from the standpoint of engineering and production costs, but I do not know enough about the complicated ties among the various corporate entities to judge whether they fit together in a way that provides an investment case.

12 Defunct players: Hanteng, Karry, Letin, Lifan, Lingtu, Southeast, Weltmeister, Yema, Yujie, Yundu, Zedriv, Zotye

18 Players with under 1,000 units a month: Kia, Mazda, Polestar, Aiways, Jiangling, Hyundai, Haima, Enovate, Yantai, Renault, Audi, JLR, Ford, MG, Landian, Maxus, BMW, Guojin. [Note my data do not include NEV imports, so global brand sales are undercounted.]

8 Players with substantial NEV sales

|

Apr-23 |

Jan-Apr 2023 |

|

|

BYD group |

193,902 |

702,608 |

|

Tesla |

39,956 |

177,385 |

|

GAC group |

46,592 |

129,985 |

|

GM group |

35,407 |

115,238 |

|

Geely group |

31,905 |

97,429 |

|

Li |

25,681 |

78,265 |

|

Changan group |

12,309 |

56,830 |

|

VW group |

15,228 |

45,529 |

Source: Author’s database, various underlying sources.

Conclusions

The prospects for 2023 sales are good – playing around with my spreadsheets, I project a 7% increase in CY2023 over last year. This will not however turn into healthy profits, as heavy discounting undermines that possibility. For example, the double-digit discounts by Tesla that set off the price war reduce its 20% gross margins to under 10%. That’s over a 50% reduction, and while discounts have allowed Tesla to preserve its volumes, they have not led to the 50% increase in sales that would be required to offset the impact of lower margins on overall profits.

It’s worse for others. Major domestic players still depend on JVs for profits. GAC, for example, does not make money on its own brands, though as a firm it is profitable once JV earnings are factored in (source: SeekingAlpha summary of quarterly financials). So even though GAC’s NEV-only Aion brand is doing well, the price war is a profit disaster, for it and across the industry.

EVs face a particular problem, in that the era of rapid expansion has reached an end. A modest expansion on top of a good overall sales year might mean a 15% increase, driven however by greater sales of PHEVs and of lower-priced EVs in Tier II and Tier III cities. Those are not the markets where Tesla and the other premium EV players do well. That bodes well for BYD, with a broad product lineup and a national distribution network. It bodes poorly for NIO, which sits at the premium end of the market and is focused on the Tier I and top Tier II cities that are approaching EV saturation. Tesla is positioned below NIO in price, albeit Tesla has a stale lineup and only 2 models selling in any volume. Exports account for 42% of the sales of its Shanghai plant, so Tesla’s capacity utilization is at risk from any slowdown in sales in Europe. It will see a collapse in profitability in 2023, along with the rest of the Chinese auto industry.

Finally, this article represents a continuation of my ongoing coverage of the Chinese NEV market. Earlier articles are:

Of course anyone considering an investment in one of the NEV firms discussed above needs to look at the SA coverage of individual companies, and should follow the Chinese investment environment and economy, which entail additional risk factors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Why Capturing China in an EV Investing Strategy Matters

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.