By Muhammet Mercan, James Wilson

Turkey at a glance

- The Central Bank of Turkey (CBT) has taken steps to ease liraisation targets and security maintenance requirements. While some of them are automatic adjustments, i.e, a rise in soft caps on lending rates with policy rate hikes, or aiming to reduce the impact of TRY weakness on deposit liraisation targets, a pivot to more conventional policies will take time.

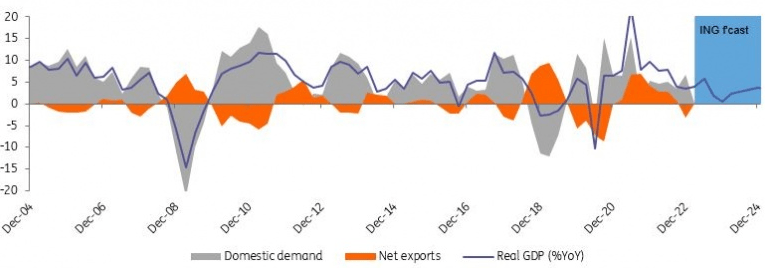

- GDP growth is likely to improve in the second quarter of the year thanks to the impact of reconstruction efforts after this year’s earthquake, though the risks are on the downside for the second half of 2023 given higher FX volatility and the signalling of a gradual tightening in the policy stance.

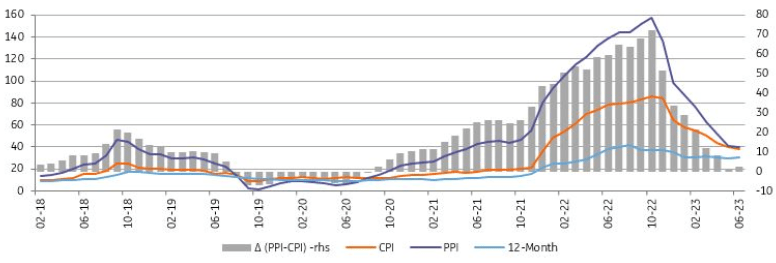

- Annual inflation dropped in June with a better-than-expected monthly reading, while the downtrend continuing since last October seems to have come to an end.

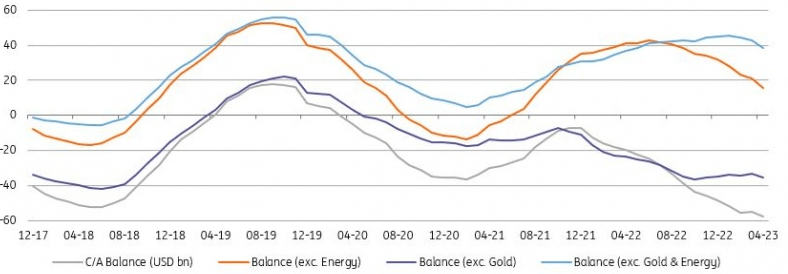

- The current account deficit has been on an expansionary path, implying the need for rebalancing. It is likely to narrow in the second half of the year mainly due to softer energy prices, although still-elevated demand, energy and gold imports remain a concern.

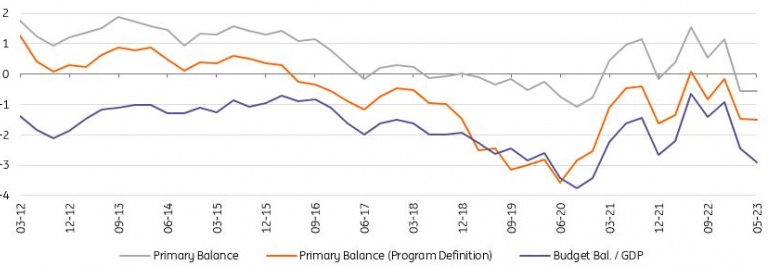

- Given the current pace of fiscal spending, pulling the 12M rolling budget deficit close to 3% of GDP in May, the government prepared a draft law forseeing an increase in revenues and control widening in the deficit.

Quarterly forecasts

Various sources, ING

Risks are on the downside

While April industrial production reflected a weak start to the second quarter, recent data releases hint at strength in economic activity:

- The manufacturing PMI has remained strong at 51.5 in the last three months to June implying a solid expansion in production despite currency volatility in the aftermath of the elections.

- After returning to pre-earthquake levels in April, capacity utilisation continued to increase in the remainder of the second quarter.

- Real sector confidence has maintained its recovery since the beginning of this year. However, according to sector PMIs in manufacturing, the data portrays a challenging picture as TRY weakness has adversely affected some sectors (although five out of ten sectors recorded PMIs above the 50 threshold in June).

All in all, the recovery is likely attributable to the impact of reconstruction efforts, though the risks are on the downside for the second half of this year given higher FX volatility and a gradual tightening in the policy stance.

Real GDP (%YoY) and contributions (PPT)

TurkStat, ING

Weak start to the second quarter

In April, calendar-adjusted industrial production (IP) recorded a 1.2% year-on-year decline, while the seasonally adjusted IP dropped by 0.9% month-on-month, indicating a loss of strength in the recovery following February’s earthquake in southern Turkey.

According to the main economic activities, intermediate goods and nondurable consumer goods were two major drivers of the sequential decline attributable to foreign demand conditions and the earthquake impact. Durable consumer goods and capital goods were other drags, while energy production pulled the (adjusted) headline rate up in April.

Among the sub-groups of the manufacturing industry, the sectors with a strong presence in the earthquake region were the drivers of the drop in the adjusted IP. Among 24 sub-sectors, 17 recorded sequential declines. This suggests that the loss of production was relatively widespread.

IP vs PMI

Markit, TurkStat, ING

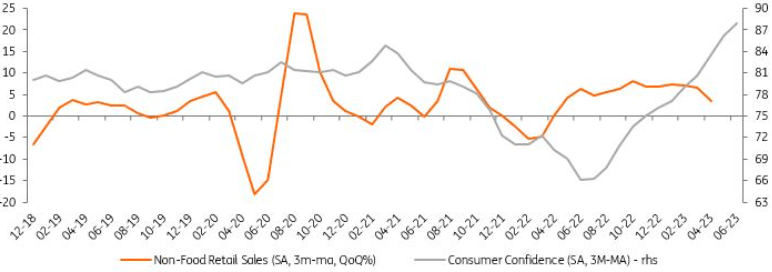

Momentum loss in April retail sales

Retail turnover, which plunged in February by more than 6% month-on-month because of the earthquake impact, returned to its long-term growth trajectory that has continued since early 2022 with a 7% MoM increase in March, and reached an all-time high in April with a further 0.9% sequential growth. However, the latest figure shows a significant loss of pace on the back of a 1.5% MoM contraction in energy. Year-on-year performance on the other hand, remained high at 27.5%, driven mainly by the non-food component.

In the labour market, TurkStat conducted a Household Labour Force Survey across the whole country in April for the first time since the earthquake, while retrospectively reflecting the earthquake effect in the indicators in February and March data with an additional survey. Accordingly, after a jump in February to 10.2% from 9.8% in the previous month, the seasonally adjusted unemployment rate stood at this level in April.

Retail sales vs consumer confidence

TurkStat, ING

Inflation still down, despite FX developments

With a better-than-expected June figure of 3.92% MoM (vs the consensus at 4.84%), annual inflation maintained its downtrend and fell further to 38.2% from 39.6% in the previous month, attributable to lower price increases in non-food groups than last year. Additionally, after mild PPI readings in recent months, we saw an acceleration to 6.5% MoM reflecting the impact of exchange rate volatility, although annual inflation dropped slightly to 40.4% due to large base effects.

The data imply that cost pressures have started to gain strength again and will likely continue in the near term given recent minimum wage adjustments and the hike in civil servant salaries. The inflation data show that the downtrend continuing since last October seems to have come to an end as we will likely see an increase in the headline figure ahead given the FX pass-through from recent lira weakness, continuing strength in demand conditions allowing companies to pass their cost increases to consumers, and potential adjustments in administered prices.

Inflation outlook (%)

TurkStat, ING

Capital flows remained weak in April

With a wider-than-expected April deficit of US$5.4bn, the current account has remained on a widening track and reached $57.8bn (translating into 6.0% of GDP) on a 12-month rolling basis, the highest since 2013. The key drivers on the monthly reading over the same month of the previous year was a continuing increase in the net gold deficit ($-1.1bn vs $-0.4bn last year), while core trade that was at a $2.4bn surplus last year turned into a $2.1bn deficit this year.

Among other variables was the net energy deficit which showed improvement to -$3.8bn from -$6.3bn in April 2022, and services income including tourism revenues was practically unchanged. The capital account was weak with a mere $0.9bn of inflows. With the monthly current account deficit and outflows via net errors and omissions at $3.7bn, official reserves recorded a sharp $8.2bn drop (financing roughly 75% of the cumulative deficit in the first four months of the year).

Current account (12M rolling, US$bn)

CBT, ING

Actions to support budget revenues

In May, the budget posted a surplus of TRY118.9bn, showing a 17.4% YoY decrease, while the deficit for the last 12 months rose to TRY527.3bn (2.9% of GDP). According to the programme (IMF) defined primary balance realisation, which excludes one-off revenues, the 12-month rolling primary deficit was 1.5% of GDP. The May budget results reflected that despite the increase in direct and indirect taxes, non-interest expenditures deteriorated compared to the same month of the previous year due to the increase in current transfers and transfers to SEEs. Interest expenditures, on the other hand, surged (recording close to a sixfold increase) due to the redemption of CPI-indexed bonds.

Given that recent moves have increased pressure on the budget side including above-inflation wage adjustments, regulation on early retirement, the increase in the lowest pension along with a continuation of various subsidies, the government prepared a draft law envisaging the increase of revenues and control of the widening in the deficit, by:

- Hiking the corporate tax rate to 25% from 20%, starting with 2023 revenues. This rate will be applied as 30% for financial institutions.

- A one-off additional motor vehicle tax, equal to the amount of the tax accrued in 2023. Thus, the tax to be paid by vehicle owners will be doubled in 2023.

- Transferring the Treasury-run part of the FX-protected deposit scheme to the CBT. Exchange rate differential expenses were TRY92.5bn in the 2022 budget and remained at TRY4.4bn in the first five months of this year due to the flat course of exchange rates. However, following the rapid lira adjustment after the elections, the burden is expected to increase significantly. With the legislation, all FX-protected deposit scheme-related exchange rate risk will be borne by the CBT.

- Temporarily expanding the authority of the president this year in determining the borrowing limit of the Treasury.

- Introducing a five percentage point corporate tax discount for companies’ export income in order to support foreign trade.

Budget performance (% of GDP)

Ministry of Treasury and Finance, ING

Gradual tightening

Amid rising expectations of a rate hike and monetary policy normalisation, Turkey’s new central bank governor, Gaye Erkan, raised interest rates less than expected to 15% from 8.5%. The decision and the accompanying statement show that the switch to orthodoxy will be gradual, but more so than envisaged earlier.

Despite the under-delivery vs the consensus expectation, the CBT’s statement recognised the deterioration in the inflation outlook by pointing to the increase in the underlying trend as well as the “strong course of domestic demand, cost pressures and the stickiness of services inflation” as major drivers. Its guidance also noted that “monetary tightening will be further strengthened as much as needed in a timely and gradual manner until a significant improvement in the inflation outlook is achieved”.

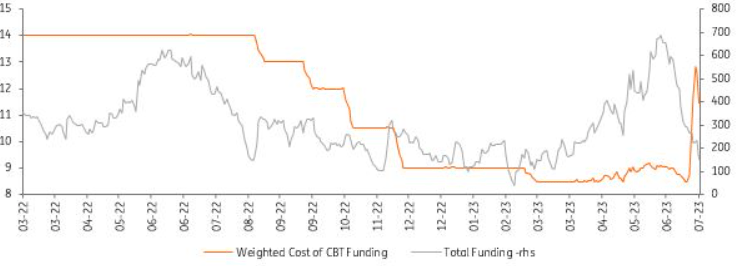

In line with expectations, the CBT signalled that it would “simplify and improve the existing micro and macro-prudential framework”. Again, the approach here will be gradual as the bank stated that it would be ”guided by impact analyses” and “the simplification process will be gradual”. Accordingly, alternative instruments, i.e the long list of regulatory measures as well as the FX-protected deposit scheme, will likely continue for a while, though to a lesser extent than before.

Central bank funding

CBT, ING

Pressure on rates and currency recently

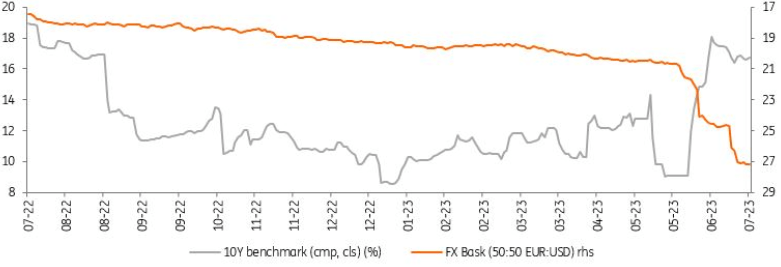

Reserves have been under pressure since the beginning of this year as a result of growing external imbalances and noticeable FX intervention measures. While FX reserve levels are quite low and require efforts to build up, there has been a rapid increase in recent weeks with less involvement of the central bank in the currency market. Since the elections, TRY fell close to 24% against the US dollar, now trading around 26. The low USD demand in the summer months and tourism revenues should be supportive of efforts to gradually return to a more conventional policy.

Given the gradual normalisation in the policy rate, deep negative real rates and hence alternative policy instruments, i.e the long list of regulatory measures as well as the FX-protected deposit scheme will likely continue for longer. Going forward, market participants will be focusing on the government’s new medium-term programme which is expected to be announced in September. In this regard, the normalisation process and related policy signals will also be closely followed ahead of the local elections in March 2024. Given the fiscal performance so far, local bond issuance will likely remain high in the near term.

10Y local bond vs FX basket

Refinitiv, ING

External debt markets calm after wild ride

Spreads on Turkey’s dollar sovereign bonds have gone full circle in recent months, with a sharp sell-off following the first-round presidential election, before a recovery as signs of a policy shift emerged. With spreads now at the tight end of their range for recent years, and around 100bp tight to the single-B sovereign average, there remains a risk of further disappointment for investors in the pace of policy adjustment, especially with pressure on the inflation rate likely to re-emerge due to the effect of FX pass through.

On the positive side, shorter-dated maturities should continue to be well supported by local demand, while signs of further financial commitments from peers in the Gulf could offer an upside surprise. That being said, it is difficult to expect further significant spread tightening for Turkish Eurobonds until investors have been convinced of the durability of the new economic team’s policy shift, while the potential for further new issuance is another risk given the rally seen in recent weeks.

ICE US$ Bond Sub-Index Spreads vs USTs

Refinitiv, ING

Content Disclaimer:

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.