Feverpitched

Thesis Summary

The economy has proven resilient in recent weeks, and equities have rallied.

The Fed is now nearing a pause, and this has traditionally been very good for equities.

However, recessions have always followed hiking cycles, and this has been a very aggressive one.

Can we time the recession?

The Pain Is Yet To Come

When it comes to

economy, we can make both bullish and bearish arguments for the future.

In the past few months, we have seen an immaculate witnessed an immaculate disinflation take hold, while at the same time, the economic data kept surprising analysts with its resilience. Expectations for a soft landing or even no-landing at all have risen in recent months, but I fear that the worst is yet to come.

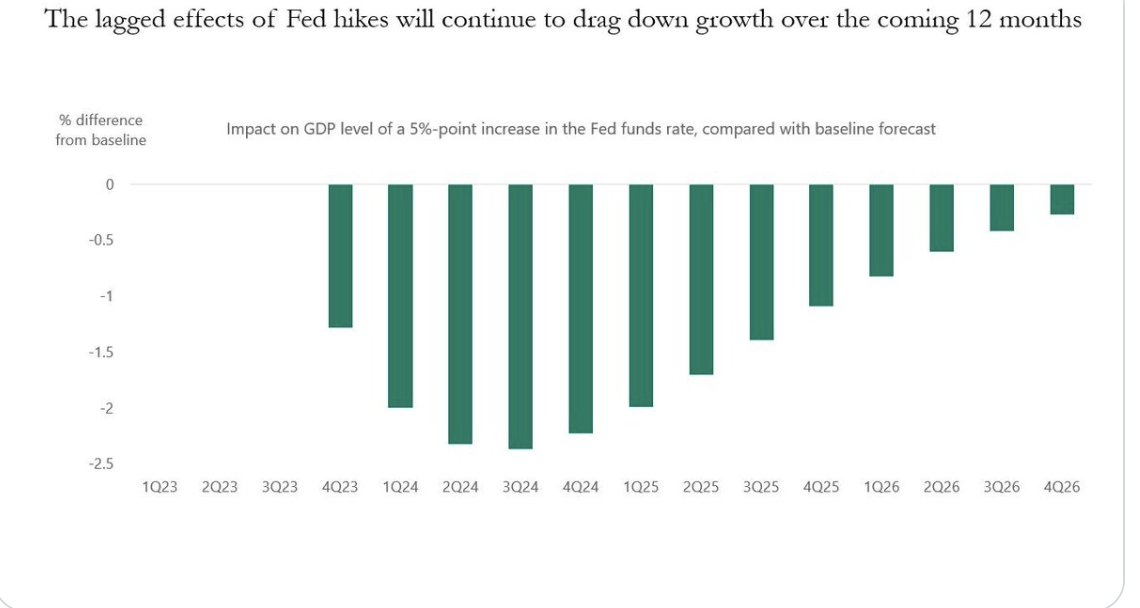

Effects of monetary policy on GDP (Twitter)

According to this chart, the current rate cuts will have the most impact on GDP as we approach Q2 and Q3 of 2024.

With that said, as the economy remains strong, for now, and commodities begin to creep up, inflation might actually prove more resilient than once thought.

Moving forward, the prospect of higher inflation could cause a re-valuation of stocks as the market digests the possibility of more rate hikes.

On the other hand, if the economy does begin to weaken, leading to disinflation, this could accelerate the outlook for rate cuts, which should be bullish for equities.

When Will The Recession Hit Stocks?

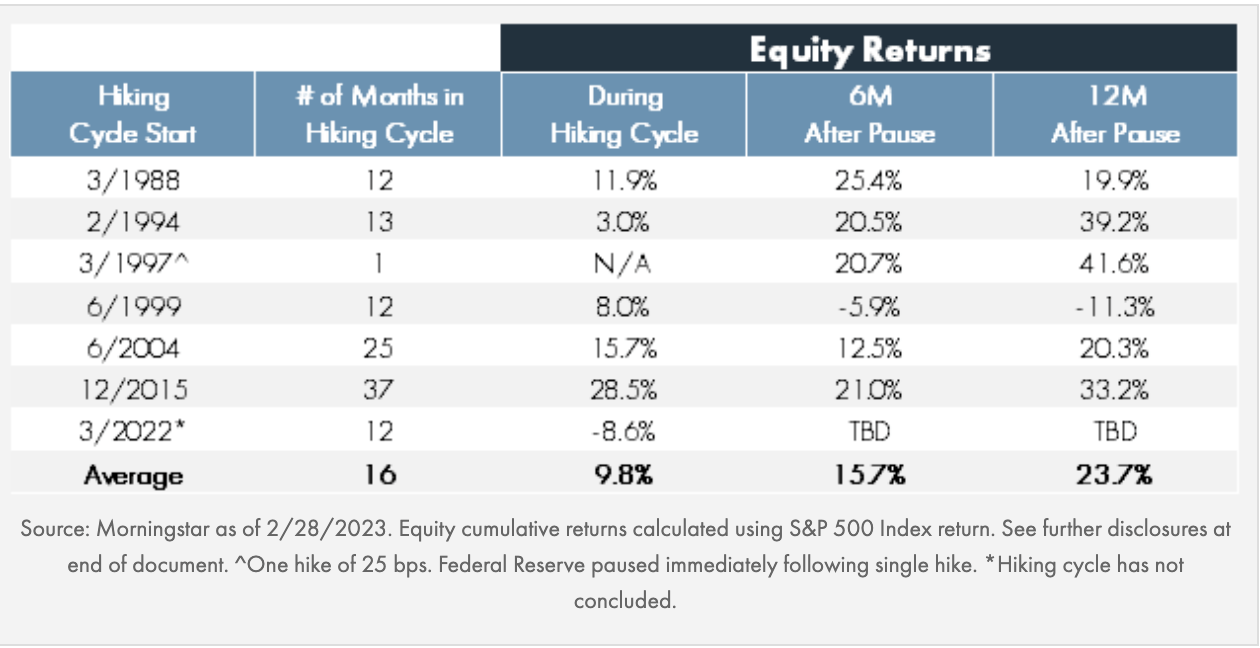

Based on history, we can try to assess how the market and economy will react to a Fed pause.

Equity returns after a pause (Morningstar)

We can see how, historically, equities tend to perform well after the pause. But what about a possible recession?

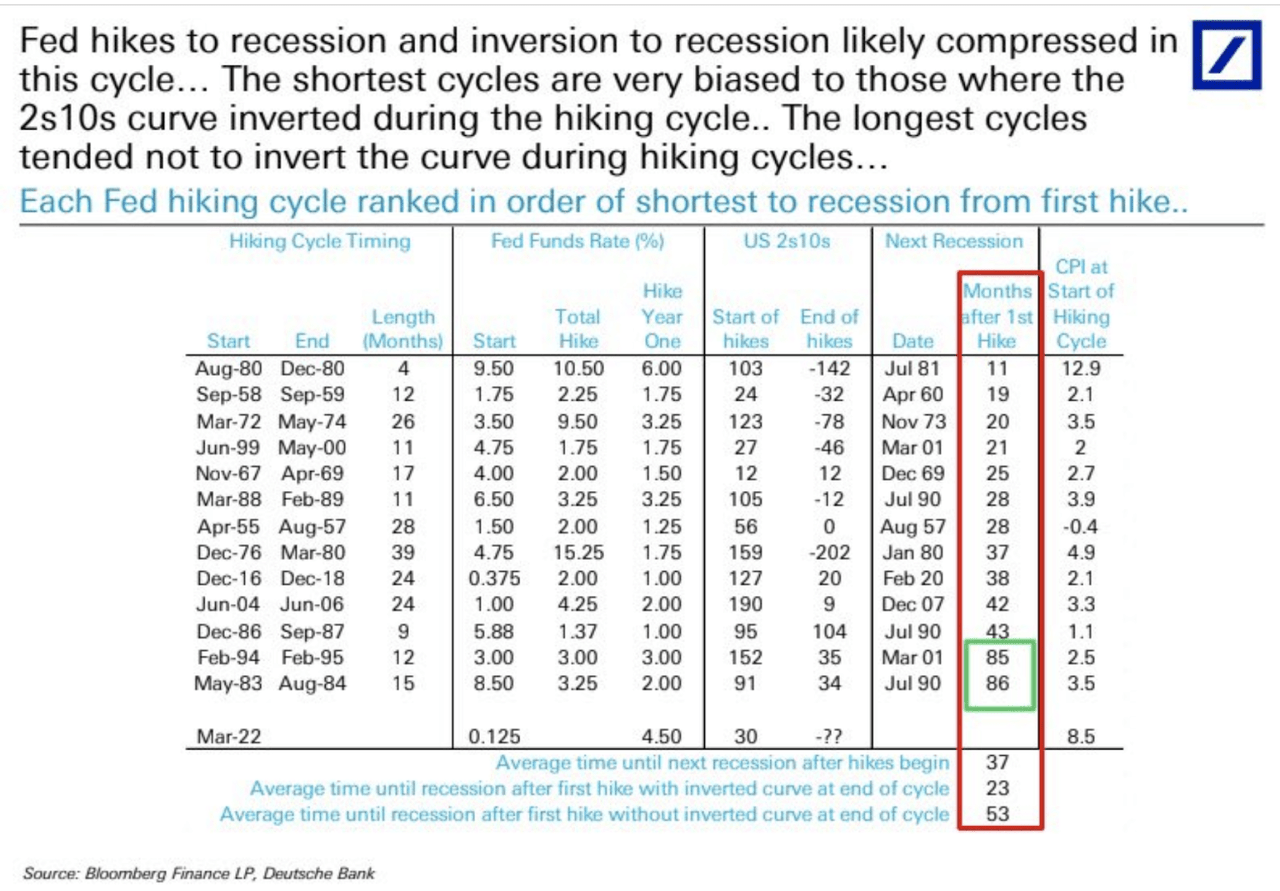

This table from Deutsche Bank tells the story of how equities have reacted in the past to rate hikes.

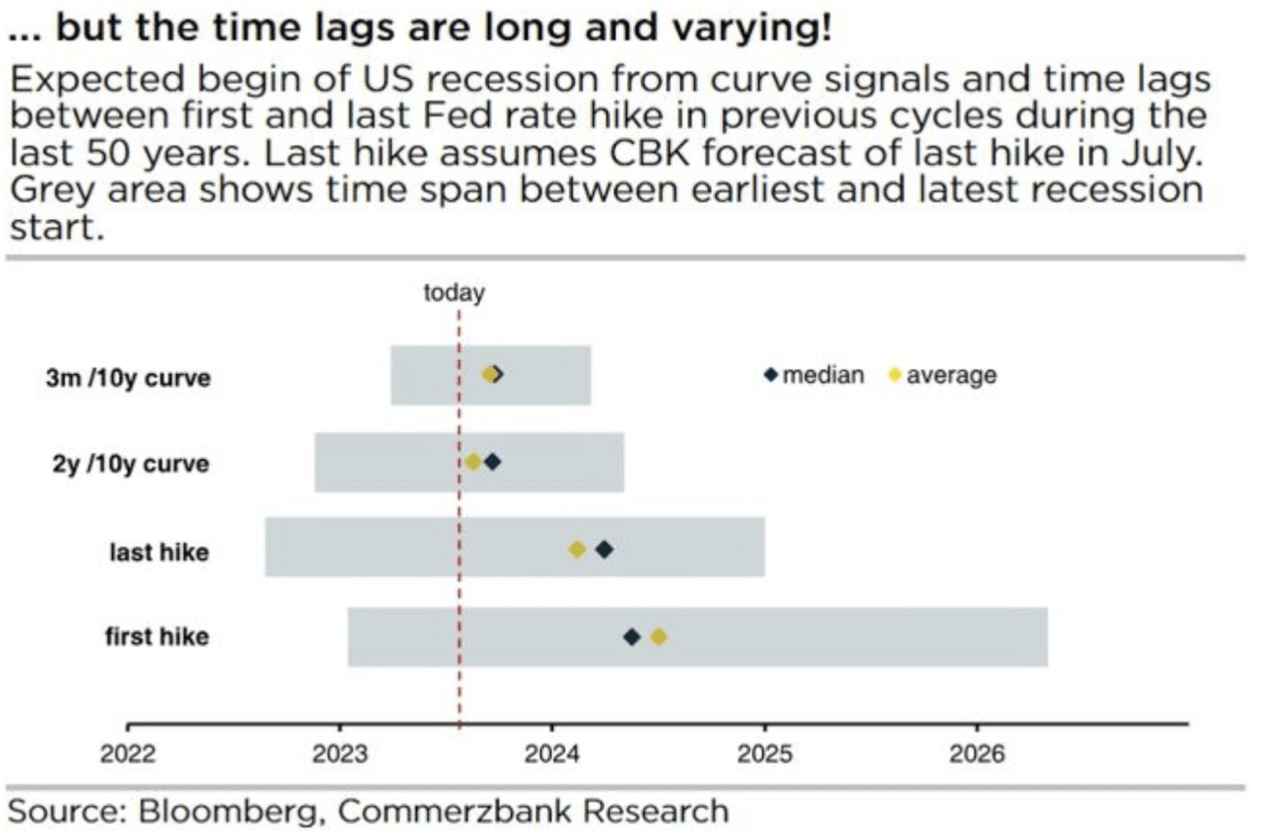

Recession after hikes (Bloomberg)

The column in red shows the months that it took for the economy to enter a recession in previous hiking cycles. We also have data on how quick these rate hikes were and whether the 2-10yr spread was inverted at the beginning and end of the hikes.

This analysis precinct that a recession could hit the economy in 23 months, which would imply it begins in February 2024.

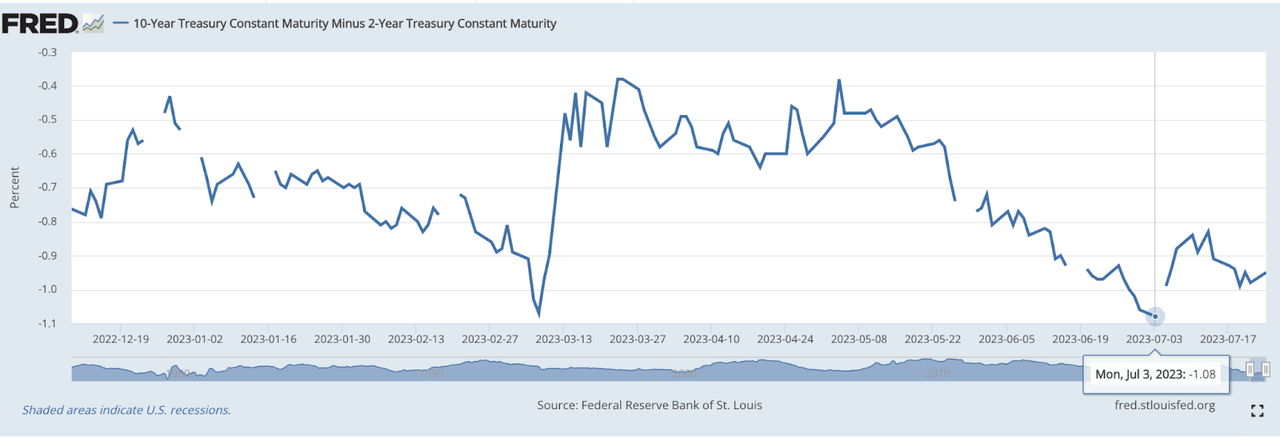

2-10yr spread (FRED)

Now, we can see some similar information presented in a different way in the table below.

Recession following yield inversion (Bloomberg)

If we look at the timing of previous recessions based on the yield curve inversion, then we could expect the economic downturn to begin late this year, 2024, but I have my suspicions it could take longer.

This Time Is (A Bit) Different

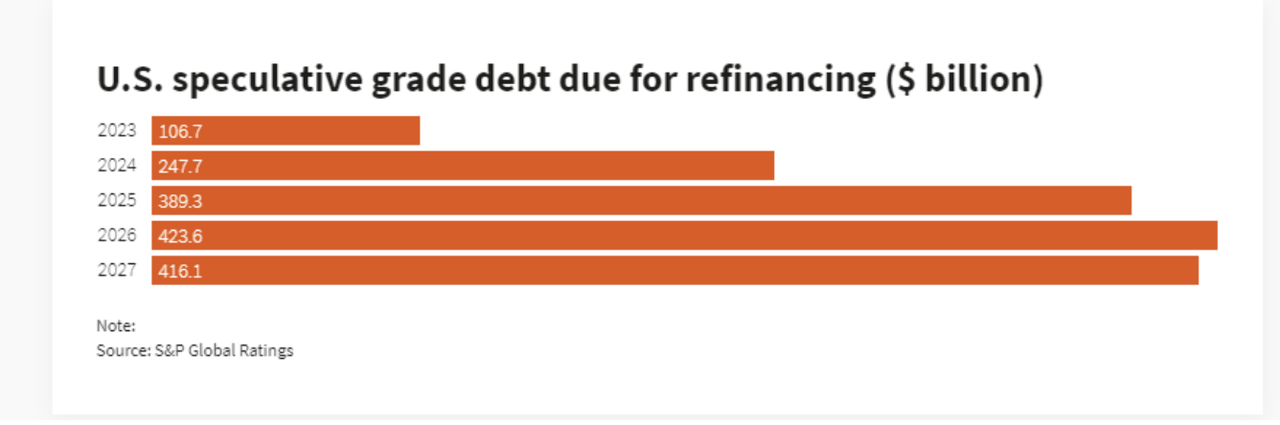

This is an unprecedented time, which follows massive economic and monetary stimulus, which will take a lot longer to unwind. Corporate bond maturities are longer than they have ever been.

Investment grade corporate debt (FT)

These much longer maturities are making the economy seem a lot more resilient in the face of the recent rate hikes.

As I mentioned in my last macro article, we have significant debt maturing in 2024 and 2025.

S&P Global (US corporate debt maturities)

And in a similar way, mortgages are a lot more resilient this time around due to the fact that a large part of existing maturities are locked at low 30-year mortgage rates. However, it’s just a matter of time before the effective.

Technical Outlook

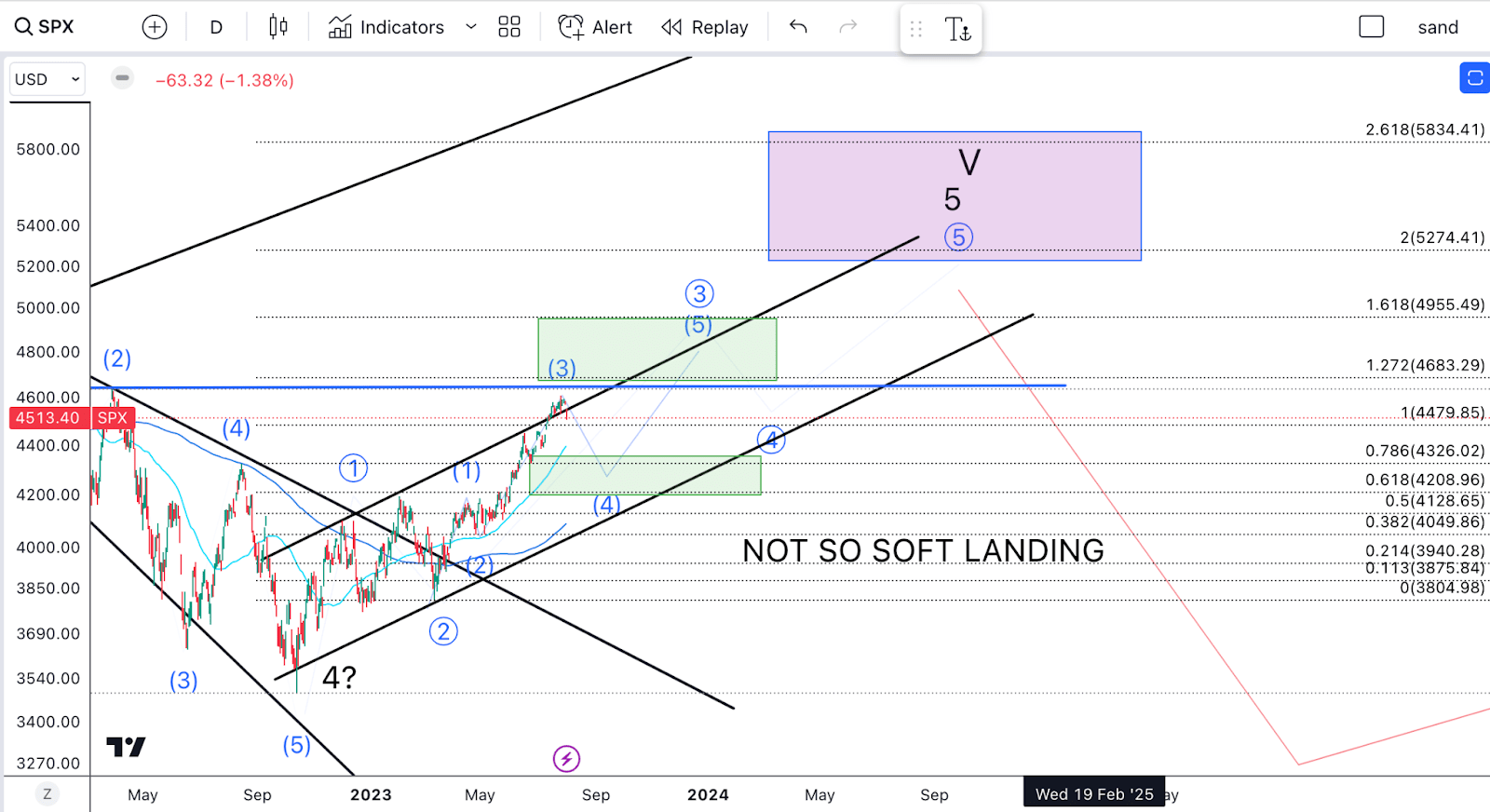

Based on the technical outlook, I think we are still en route for a blow-off top, but the recent price action makes it clear that a correction is due in the more immediate term.

SPX TA (Author’s work)

The way I see it, we are still completing an impulse from the lows in 2022. Based on the initial rally of the lows, this could take the SPX into the 5200-point region.

However, we have now fallen back below the top of the trendline of this rally, and that is a strong indication that we could have begun a pull-back in a wave (4). The way I see it, if we can reach 4200, that will be an ideal place to load up.

Takeaway

Ultimately, we still need to go higher before we go lower, and the timing of the recession/equity sell-off will also depend on when we reach my targets for the SPX. For now, I think a renewal of inflation fears and perhaps even another hike could send markets tumbling. However, I’d say we still have close to a year before a full-blown recession sets in, and in that time, I expect us to rally much higher. Analysts will claim the soft landing has been achieved, but what I see is a delayed hard landing.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.