Tencent (OTCPK:TCEHY) faces present difficulties from a slowdown in the Chinese economy, but full-year fiscal 2023 results look to close the book on a promising year, indicating the slow return of continued future growth after a troubling 2022. I believe that the stock is presently significantly undervalued based on a long-term horizon, but investors shouldn’t expect exceptional growth.

Overview & Future Direction

Tencent Holdings is a Chinese multinational conglomerate focusing on various sectors, including entertainment and AI. It is known as the world’s largest video game vendor, as well as having a crucial stake in social media, venture capital and investment. It operates Tencent QQ and WeChat and owns Tencent Music, among other assets.

Recently, it has begun to focus on a term called “Immersive Convergence.” A white paper produced with Accenture (ACN) outlines the intention of further deepening the synthesis of the digital economy with the real world. The white paper suggests the advancement of five critical technologies to this end: digital twin, remote interaction, ubiquitous intelligence, trusted platform modules, and infinite computing power. By 2040, it anticipates the evolution of remote interaction to full sensory experiences by harnessing IoT, Real-Time Communication, Extended Reality, multi-sensory interaction, and multi-modal fusion sensing technology.

Q4 Earnings Preview

For Q4 earnings, expected to be announced post-market on 3/20/2024, analysts are expecting normalized earnings per share of $0.60, which is a significant improvement from last year’s $0.44. The full-year normalized EPS estimate for Tencent is $2.25, indicating 30.85% growth for the year. Tencent’s fiscal 2022 struggle has considerably reversed in fiscal 2023, and this marks a year where Tencent has regained some of its growth momentum.

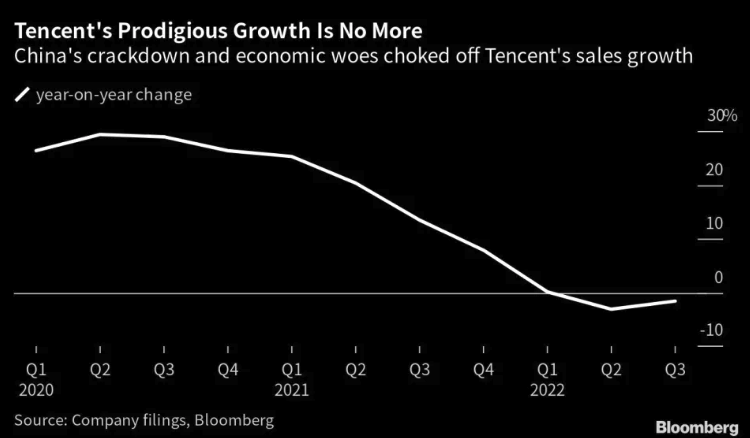

Tencent Historical Sales Growth Chart (Bloomberg)

Throughout 2023, its growth has been driven by a combination of gaming, advertising sales, and fintech services. In Q1, the firm saw an 11% jump in revenue as the Chinese economy began to recover. International gaming revenue saw a 25% rise.

By the third quarter, Tencent marked its third consecutive quarter of revenue growth. The firm rebounded after a regulatory crackdown on China’s tech sector, and Tencent’s online advertising business saw a 20% jump in revenue.

There is a significant value opportunity at this time that I will elucidate in my ‘Value Analysis’ section below, in part driven by a rebound in the Chinese economy that is likely to unfold but also by strong future earnings estimates indicating high growth likely to resume. I estimate an EPS CAGR of 15% is reasonable over the next 10 years, helped by a general growth trend I expect to resume in China’s economy overall, but also significantly bolstered by growing trends in technology and high levels of digitalization, which Tencent has a significant role in.

Long-Term Outlook

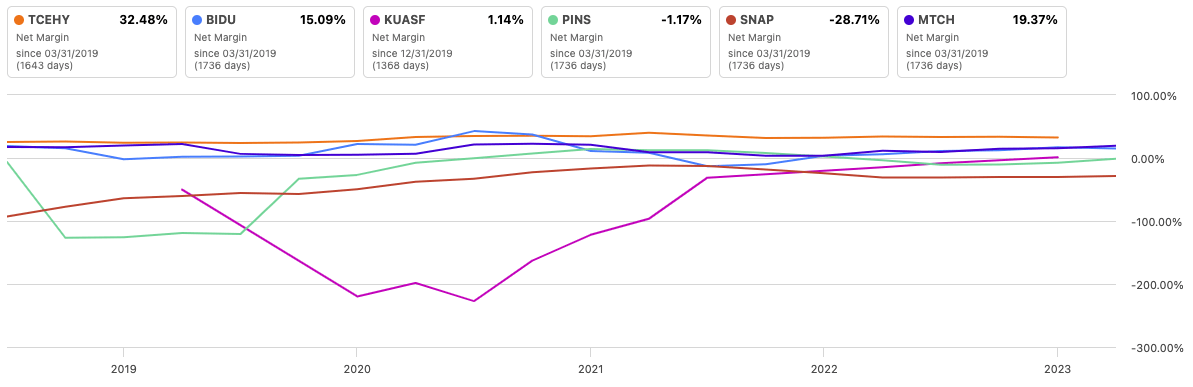

One of Tencent’s strongest elements is its high-grade profitability. Consider a net income margin of 32.48% at the time of this writing compared to the sector median of 3.07%. Compared to peers, it is right at the top of the pack, but it is also way larger than most companies of a similar nature, and hence, it commands a much richer moat in terms of operational scope.

Net Income Margin (Seeking Alpha)

Market Cap (Seeking Alpha)

Its high level of net income compared to its peers places it in a good position to continue to excel in the field of technology and entertainment throughout the next decade, which I believe could see long-term growth resume for the firm following what has been a challenging period from around 2021. An improvement in the Chinese economy could largely drive this, but the

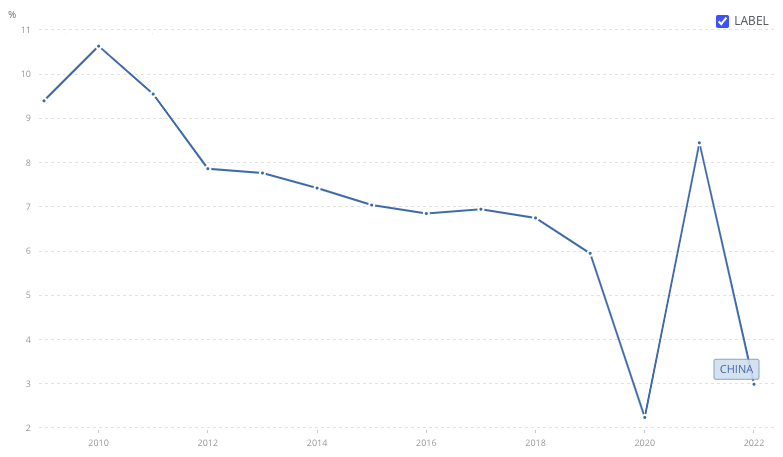

Peterson Institute of International Economics (PIIE) suggests several long-term problems facing China, including slumps in productivity, an aging labor force, and restrictions on technology transfer from abroad. However, it also mentioned that long-term severe contraction for the economy is unlikely, and domestic demand may now be strengthening, as seen in the slight growth of import volumes and household consumption in urban areas. If the Chinese economy includes measures to support the increase in household consumption, like government-funded consumer vouchers, tax cuts, faster wage growth, and improvements in the social safety net, deflationary pressures could be addressed. Tencent could benefit from an improvement in technology and entertainment consumption as a result.

GDP Growth (Annual %) – China (The World Bank Open Data)

However, I believe investors should be cautious because there is some degree of uncertainty about how China will manage its economic condition at this time. There is significant evidence for China’s continued success, and given the size of Tencent, I believe the two conditions are largely correlated. I believe that it may be a prudent bet on a Chinese economic rebound and a decent valuation at this time, but I also believe there are better investments in China. Additionally, there are smaller but higher-reward companies at only slightly more risk.

However, Tencent is well-positioned in its financial health to succeed over the long term as economic conditions improve. Consider a balance sheet with an equity-to-asset ratio of 0.74. Compare this to some of the companies I have used in my peer analysis, which reveals that Tencent has formidable management of liabilities:

- Baidu (BIDU): Equity-to-asset ratio of 0.6.

- Kuaishou (OTCPK:KUASF): Equity-to-asset ratio of 0.47.

- Pinterest (PINS): Equity-to-asset ratio of 0.86.

- Snap (SNAP): Equity-to-asset ratio of 0.3.

Tencent’s strong balance sheet is evidenced by a heavy focus on the repayment of its long-term debt, which, indeed, it does issue frequently, but it manages it with care. Additionally, its repurchase of common stock, which far exceeds its issuance of said stock, is admirable, in my opinion, and has significantly bolstered shareholder value over time. Evidence reveals to me that this is a well-run company, and I estimate that it will indeed outperform the S&P 500 over the next decade, especially if bought now, largely a result of high growth prospects at an attractive valuation at the time of this writing.

Seeking Alpha

Value Analysis

For my value analysis, I have used a typical discounted cash flow model, as opposed to the P/E multiple analysis that I sometimes use for companies with a very high price premium, which is common in elite tech companies from America. In this instance, I do not believe Tencent has such a premium.

I have considered the following metrics for my DCF analysis:

- Diluted EPS growth 3-year average of 16.9%, 5-year average of 17.61%, and 10-year average of 28.67%.

- Fiscal 2023 full-year normalized EPS of $2.25.

- My estimated next-10-year normalized EPS growth of 15% as an annual average.

- A 4% normalized EPS growth rate as an annual average for the decade following my 10-year growth stage.

- An 11% discount rate.

From the above elements placed into my discounted cash flow calculation, my fair value estimate is $42.01, indicating a 17.85% margin of safety on the stock price of $34.51.

Risk Analysis

The largest risk I can identify with my thesis on the long-term opportunity related to good growth and a significant undervaluation in the shares at this time is issues that China encounters economically, particularly geopolitically. I believe that investors would be wise at this time to attempt to diversify holdings away from China, the US, and other world powers. My present portfolio is heavily weighted toward the US, but I believe there are exceptional investments, particularly in small caps from other parts of the world, that offer durable competitive advantages and compelling valuations and may protect against present economic tensions.

I also believe that Tencent will face significant difficulty in maintaining high growth and may be at a competitive disadvantage when compared to the capabilities of Western technology companies, with Nvidia’s CEO mentioning China being 10 years behind America in some areas on this front.

Both of these concerns lead me to caveat my value analysis with the potential for more moderate growth for Tencent over the next decade, a result of what could be a significant upset from escalations in global military conflict, causing high volatility in the technology sector temporarily, particularly in China and America.

Conclusion

This is one of the lower-risk opportunities in China that I consider a good value investment. However, I believe investors would be wise to consider some of the risks that are inherent in the wider Chinese economy’s present stagnation. I believe that there are also geopolitical risks not priced into the shares at this time, but due to the exceptional value and high long-term growth for the company that I expect, I rate Tencent stock a Buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.