The Basic Story

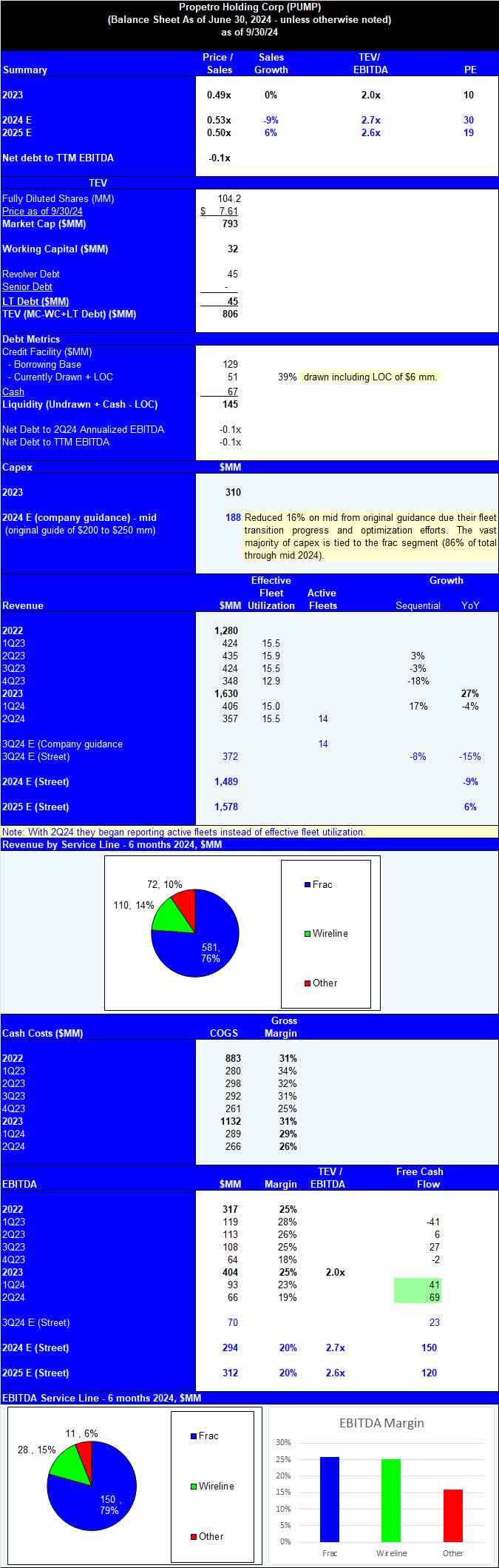

ProPetro Holding Corp. (NYSE:PUMP) is a small-cap Permian-focused pressure pumping name with recent acquisitions in completion-related services of cementing, wireline, and wet sand broadening their offering for a more integrated solution. Like others in the frac space, they are transitioning their frac fleet to dual fuel and electric fleets (their Force fleets). The balance sheet has more cash than debt, and they are generating free cash flow and buying back shares in 2024 with the potential for meaningful further share repurchases. We covered the 2Q24 results on our site, and although they came up slightly short on revenue and EBITDA (something that was common for their group in 2Q24) we were impressed with their performance in a weak North American oil service market. Others, it seems, were less impressed and the shares are down 15% since the 2Q report and are off 9% on the year. ProPetro is all in on the Permian and is viewed as a high-quality provider with a strong customer base. We view the Permian as the most resilient oily basin in the U.S. and see continuous takeaway capacity adds keeping it that way given its scale and proximity to Gulf Coast refining and export markets. Given their solid margins, investment discipline, cash-rich balance sheet, a significant buyback, and their customer base that is unlikely to get a lot less active anytime soon we view ProPetro, which trades well under 3x EBITDA (this year and next) as overly cheap.

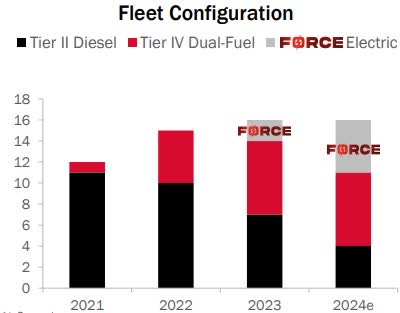

Frac Fleet Portfolio

They have 16 active frac fleets in their portfolio, of which 14 were expected to be working this quarter. ProPetro has been continuously upgrading the fleet, but not expanding it. On the whole, the newer fleets are cheaper to run, cleaner, more efficient, more reliable, and require lower maintenance capex. The dramatic shift to dual fuel and efrac fleets can be seen here:

ProPetro Holding Corp.

The newer fleets command a premium over older fleets.

- ProPetro has seven Tier IV DGB fleets and over the last year and a half, they’ve been able to increase gas substitution for diesel from around 50% to just over 60% (cleaner, less cost).

- They have four Force fleets under contract with upstream players now (the fourth went to work this month) and they have an order placed for a fifth fleet that is expected to go into service before year-end. This fifth Force fleet will likely not be additive to horsepower, but will replace one of the remaining Tier II fleets.

- They lease the Force fleets for three-year extendable terms. Leases appear to run about $2.3 per quarter per fleet (+/- depending on the level of use) and each fleet has initial additional costs of about $5.5 mm (one-time setup costs). The lease portion of their costs is included in the cheat sheet segment EBITDA margins below. They don’t lease fleets without solid customer demand and have a deal in place with Exxon for fleets #3 and #4 along with associated services.

- While many are making the shift to newer fleets, ProPetro currently has one of the youngest average fleet lives with 70% of their fleets less than 2.5 years old.

Balance Sheet

Net cash positive, Credit facility with $45 mm, cash balance of $67 mm. They generated over $100 mm in FCF through mid-year and liquidity appears more than ample.

Return of Capital: Meaningful buyback in progress

They do not pay a dividend at present. Instead, management is focused on their active repurchase program. They bought back 2.5 mm shares in the second quarter and 5.5 mm through mid-year or about 5% of the outstanding count. At mid-year they had $103 mm (13% of the current cap) authorized for additional repurchases and planned to continue to opportunistically reduce the share count. Given the current valuation discount, our view is that they were likely to have been active again in 3Q24.

Valuation: Inexpensive

ProPetro trades at TEV to Street EBITDA of 2.7x and 2.6x for 2024 and 2025 respectively. The clean balance sheet and solid EBITDA margins during a weak phase of the cycle for frac and their ability to generate positive free cash flow during this period suggest this is too cheap. We also note it’s trading cheaper than more basin-diversified, larger peers Patterson-UTI Energy, Inc. (PTEN) and Liberty Energy Inc. (LBRT) both of which are trading near 3x next year’s consensus. And yet, despite the cheapness, the name is still 11% short. Our view is that the Street is missing the shift in FCF generation during the current tougher times and the name is now easily overly discounted.

Z4 Energy Research

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.