Introduction

When JPMorgan (JPM) reports earnings, it is like the opening bell of the earnings season. This is why, no matter if you are invested in it or in similar banks, its report should always be considered, as it both wraps up the year behind us, but also – and most importantly – sets the tone for what’s going to come. This is why I consider it the first note of the earnings waltz.

I have never directly dealt with the largest bank in the market, but after having shared my outlook for this year, it is finally time I initiate my JPMorgan coverage.

JPMorgan Chase: A Quick Overview

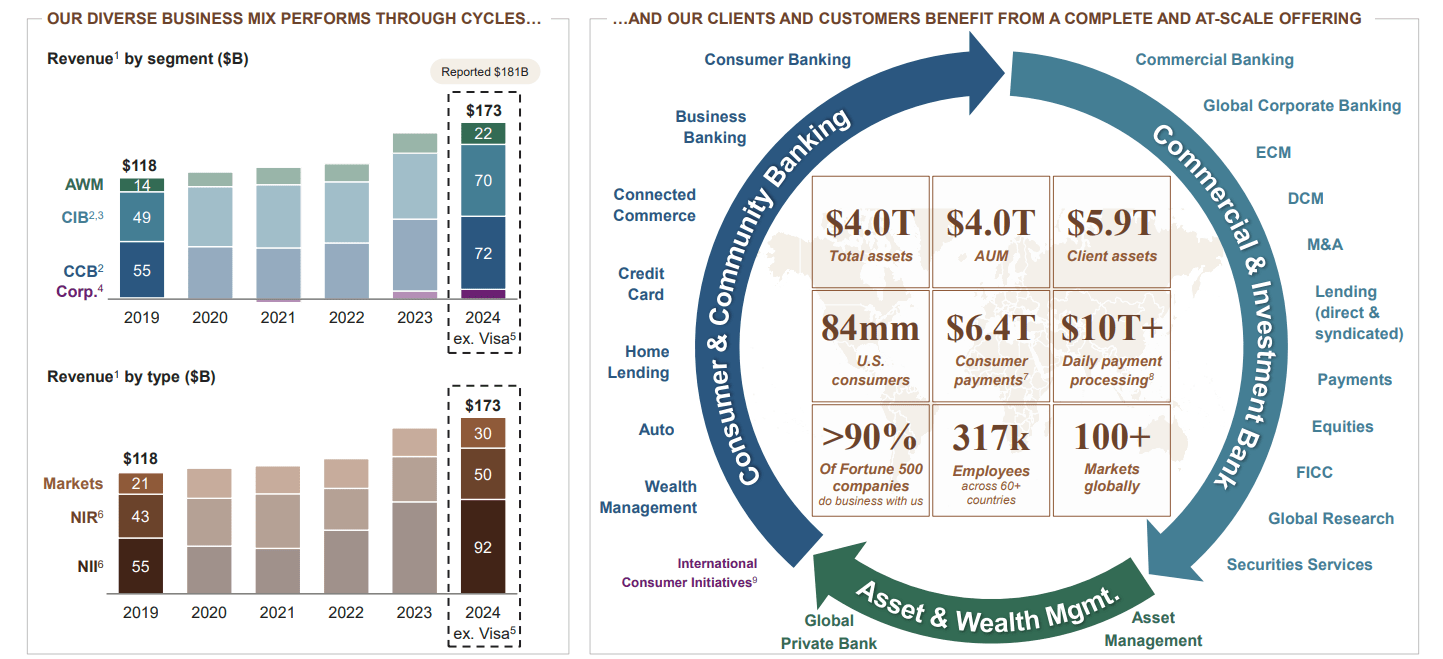

This bank is a giant that will likely reach $1T in market cap soon. However, we have to be aware at least of its main internal structure. You can see below that JPMorgan has three main segments: Consumer and Community Banking (CCB), Commercial and Investment Banking (CIB), and Asset and Wealth Management (AWM). At the end of FY24, the bank reported revenues of $173B, with CIB and CCB being roughly even since they reported $70B and $72B, respectively. AWM is smaller and generated $22B. Overall, we are talking about a bank with client assets just shy of $6T, with over 84M U.S. customers. In Q3 alone, the bank added 400k new checking accounts.

The two main segments are internally divided into multiple businesses: CCB, for example, includes consumer banking, home lending, and credit cards; CIB has commercial banking, corporate banking, payments, lending, and global research, among others. At the end of Q3, CCB reported quarterly revenues of $19.47B, while CIB took the lead with $19.88B. AWM broke just above the $6B landmark. When we look at the net income of each segment, we see that CCB reported net income of $5B (+24% YoY), CIB reached $6.9B (+21% YoY), and AWM $1.7B (+23% YoY). There is no way to hide the fact that JPMorgan is simply thriving. What drove these results? In CIB, it was mainly M&A activity and the Equity Capital Markets division (ECM), which works with companies that need to raise capital either through IPOs or private placements.

JPM 2025 Investor Presentation

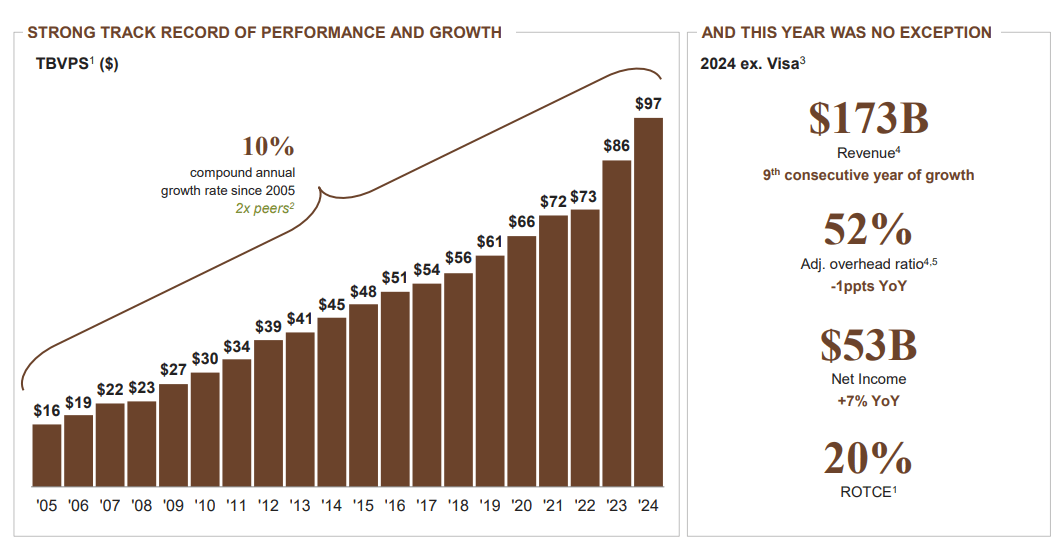

This is a consequence of its scale: in U.S. retail deposits, the bank has a market share of 11.3%. Moreover, we can see below that JPMorgan has been able to keep growing its tangible book value per share (TBVPS) even during the GFC, achieving a 10% CAGR since 2005.

JPM 2025 Investor Presentation

Now, banks have done really well after the pandemic for two reasons. The first one is linked to high interest rates, which made their NII explode. The second was that, after the GFC, banks traded at a discount for a long period of time, betraying investors’ lack of confidence in these assets. However, after the pandemic, it became obvious that most banks are now well capitalized. In addition, now that interest rates have started to come down, we are seeing that a bank such as JPM is still expanding its profitability, showing that, even though NII is past its peak, the scenario is not that of a free fall but one of a glide. In the meantime, its balance sheet is solid as a rock, with capital levels well above regulatory requirements. Finally, JPMorgan’s ROTCE is incredibly high and often comes above 20%, which is way above its cost of equity.

All of this makes JPMorgan able to return capital to its shareholders, both through dividends and big buybacks. In short, JPMorgan is a story about continued balance sheet compounding.

As its Q4 earnings approach, let’s then see how we could prepare ourselves both for the results that matter for the bank’s valuation and for the data that we will learn about the general economy.

JPMorgan’s Q4 Earnings Preview

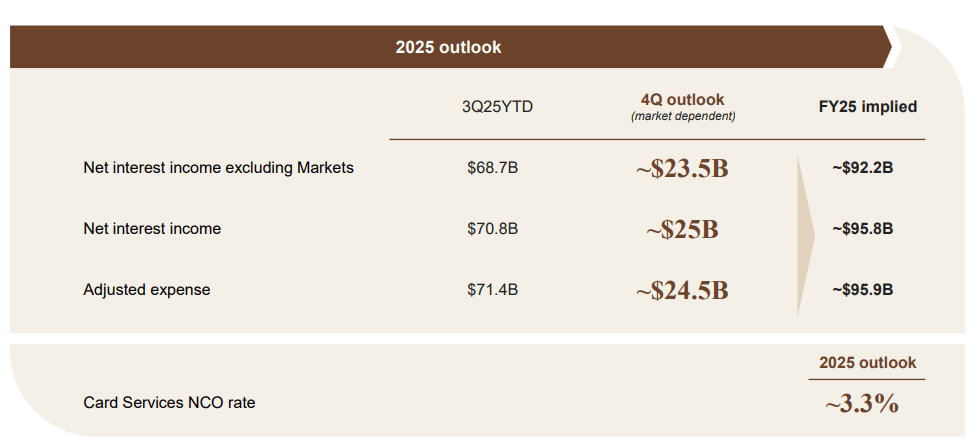

First of all, what are investors expecting? All eyes will be on NII, which should be stable or slightly decreasing. Since we are hearing that some consumers are indeed being pressured by persistent inflation, investors will also look at the bank’s credit provisions, which have been moving up in recent quarters. If they suddenly spike, it would be a terrible macroeconomic indicator.

JPM Q3 2025 Earnings Presentation

Surely, I also expect market revenues to be strong. After all, market conditions have been favorable because volatility is usually helpful for a bank such as JPMorgan. This could be the real area where we find a positive surprise that could push the stock higher. Talks about future capital return policies will also attract attention.

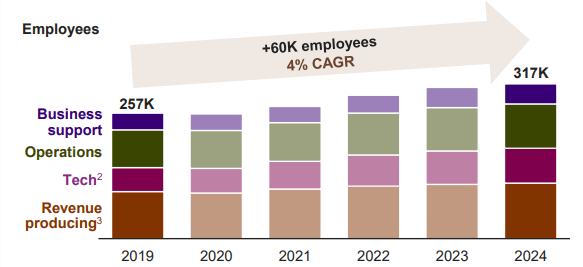

But I would like to point out something that might not immediately come to mind. Look at the slide below. It shows that from 2019 to 2024, JPMorgan hired 60k employees, increasing its headcount by 4% annually. This makes its overall cost structure higher. Now, on one side, JPMorgan wanted to capitalize and invest in its growth. But, on the other side, this hiring policy started before a major revolution was released. I am talking about AI. As a matter of fact, this year, JPMorgan has hired fewer than 1,000 employees (for a total of 318k). It has also repeatedly stated that it wants to manage its cost structure effectively and that it is about to release more than 100 programs where AI is involved. What does this mean? JPMorgan is moving in the direction of using AI to enhance its productivity and count less on new workers. As far as I see it, big banks are going to be among the first beneficiaries of AI because they are entirely built on data. This is a truly favorable environment for AI to be effectively deployed.

So, I think that one major area of interest will be headcount management and productivity increases. If JPMorgan is able to show the benefit of AI, it could be another major catalyst in favor of this revolution.

JPM 2025 Investor Presentation

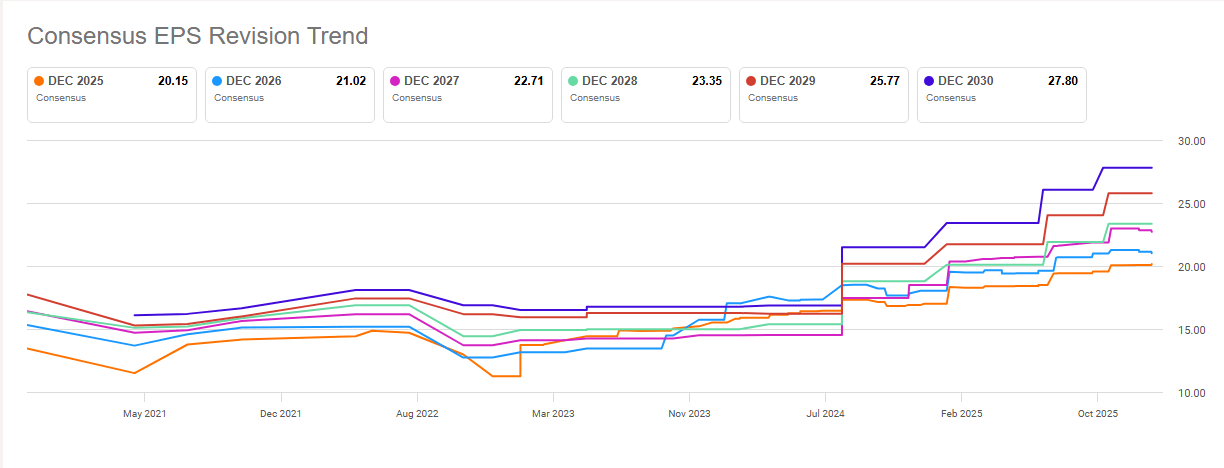

It seems that some analysts are realizing this, as we see that JPMorgan’s consensus EPS revision trend has been moving upwards since last year at a much faster pace compared to the past.

Seeking Alpha

I think it will almost be a non-event that JPMorgan will beat its revenue estimates of $46.25B, and that it will probably come in above quarterly EPS of $5.00.

Right now, the stock trades at a P/B of 2.6, which is a bit expensive for a bank. But since JPMorgan usually trades at a premium, it can be understood why the bank is given this multiple. It is not cheap, but it is not even extremely expensive. Its FWD P/E is also 16, which is a bit to the high end of its usual range. But an EPS beat and a strong 2026 guidance could immediately bring this multiple to 13 or 14. This would make the bank trade within a fair range. I am not saying that JPMorgan is a screaming buy, but I am not of the opinion that the stock is done growing. In fact, the bank is flourishing. However, part of how the stock will react will depend on what we discuss in the next paragraph. Investors will react depending on the outlook that JPMorgan will give on the overall economy.

JPMorgan Could Give Us 3 Macroeconomic Signals

In this earnings call, besides what we discussed about the bank, we could receive a sample of the economy’s health. Usually Jamie Dimon is quite cautious in his takes, but here I am not talking about the CEO’s direct words. We will have to understand from the data and the earnings call how the consumer is doing. In particular, while we know that some consumers are slowing, we need to find evidence that they are not breaking. Here, the most important number could come from card spending and delinquencies. The second signal will be about credit conditions. We need to see how different books are doing and if they improve or worsen. For example, if cards perform poorly, we could think about consumer stress. If Commercial Real Estate does badly, we could understand that there is still a rate shock effect. If provisioning appears gradual, then we might talk about a cooling economy, but within the narrative frame of a normalization, rather than a recession. Third, NII – its guidance, in particular, coupled with deposit pricing, will show what’s happening in monetary transmission. If NII remains stable despite moderately high rates, it will mean that the economy is actually absorbing the Fed’s policy. If we see sudden pressure on JPMorgan’s NII, well, it means that the Fed’s bite has finally arrived.

Conclusion

With a market that has started January in bull mode, JPMorgan’s earnings could hold the fate of how the market will behave for the rest of the month. In a few days, I doubt that the question will be whether JPMorgan beat earnings or not. This is almost a certainty. But investors will ponder the report and the earnings call to detect if this could be an earnings season where dispersion matters more than de-risking. In the first case, we will see some companies miss, while the majority will keep beating. There will be sector rotation, and an equal-weighted index, such as RSP could do well. There won’t be panic. If, on the other hand, JPMorgan suggests it is time to de-risk, then a sell-off could be triggered that would not leave behind good companies as well as bad ones.

I believe that JPMorgan will do well and that it will confirm that the economy, though with some sectors that are struggling, is generally doing well and set to grow in 2026, too. This is why I think JPMorgan is a buy before earnings.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.