Merck & Co., Inc. (NYSE: MRK) has had a fantastic six months, seeing its share price go up nearly 50%. The company has a valuable portfolio of assets that will enable strong shareholder returns, making it a valuable investment.

Merck Results

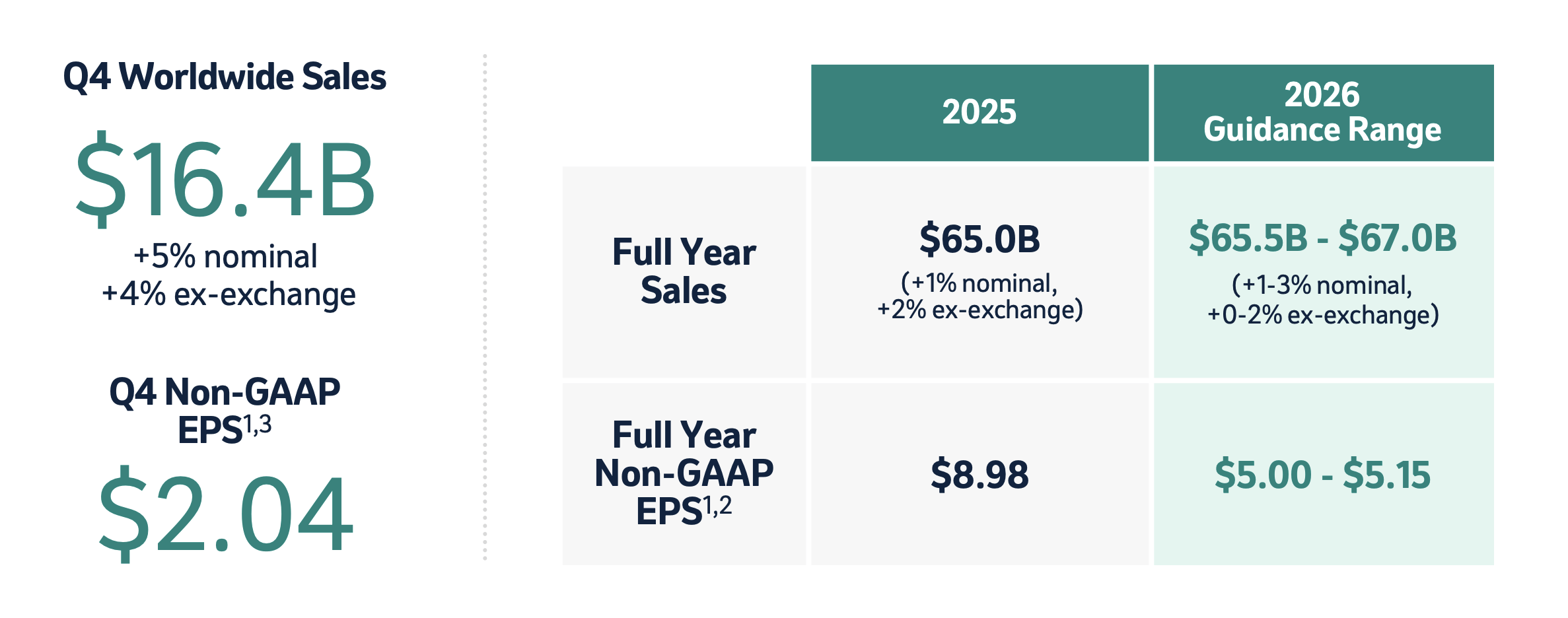

Merck had $16.4 billion in sales for the quarter, driving $2/share in EPS and mid-single-digit top-line growth.

Merck Investor Presentation

The company’s fiscal year guidance is ~$66.5 billion in revenue, just a hair below inflation, and the company’s 2026 guidance is in the same range. The company’s FY non-GAAP EPS is just under $9/share, a low double-digit P/E ratio, quite respectable. The company’s 2026 guidance is ~$5.1/share, mostly impacted by its $9.2 billion acquisition of Cidara.

Merck Investor Presentation

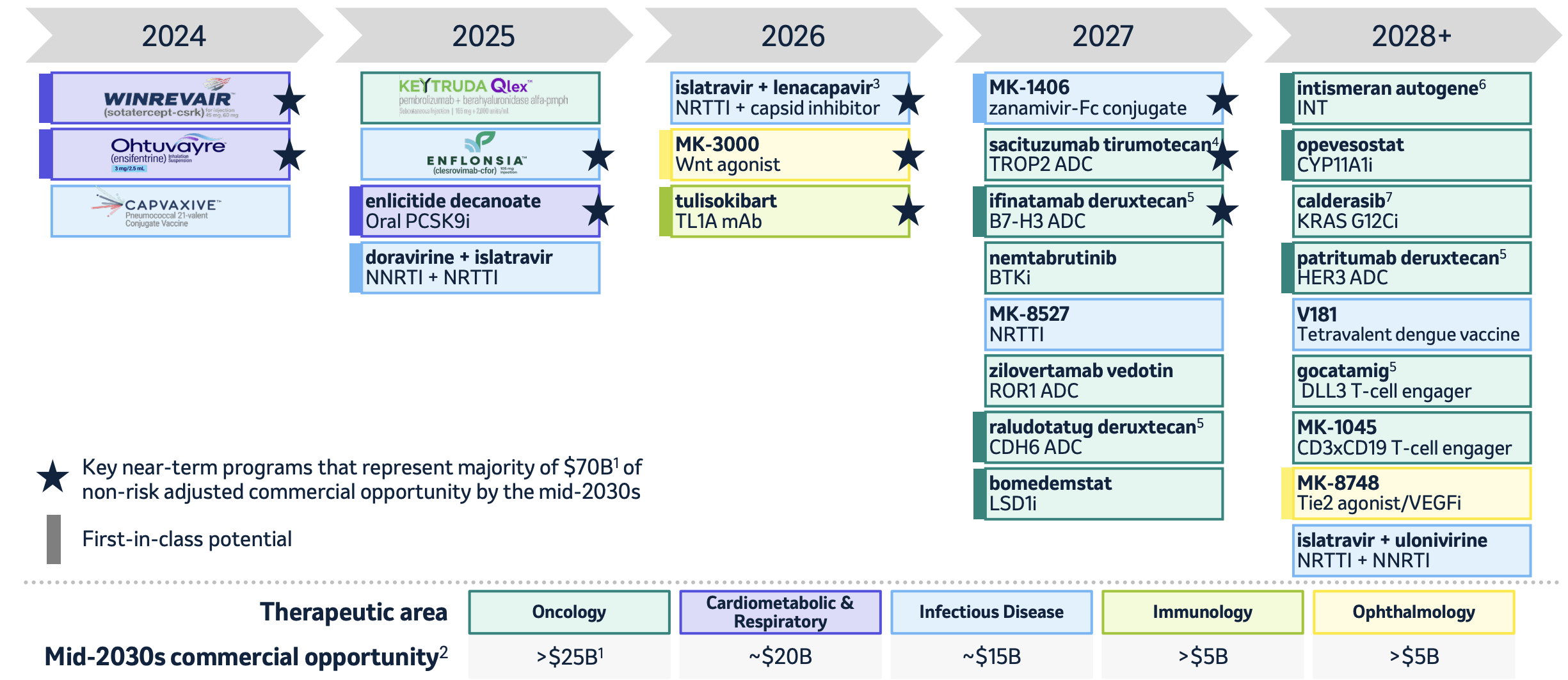

Looking at Merck’s multi-year outlook, the company has a number of interesting commercial opportunities. The company sees the total commercial opportunity to be ~$70 billion, more than enough to replace its existing revenue and enable strong shareholder returns to continue.

Merck Keytruda

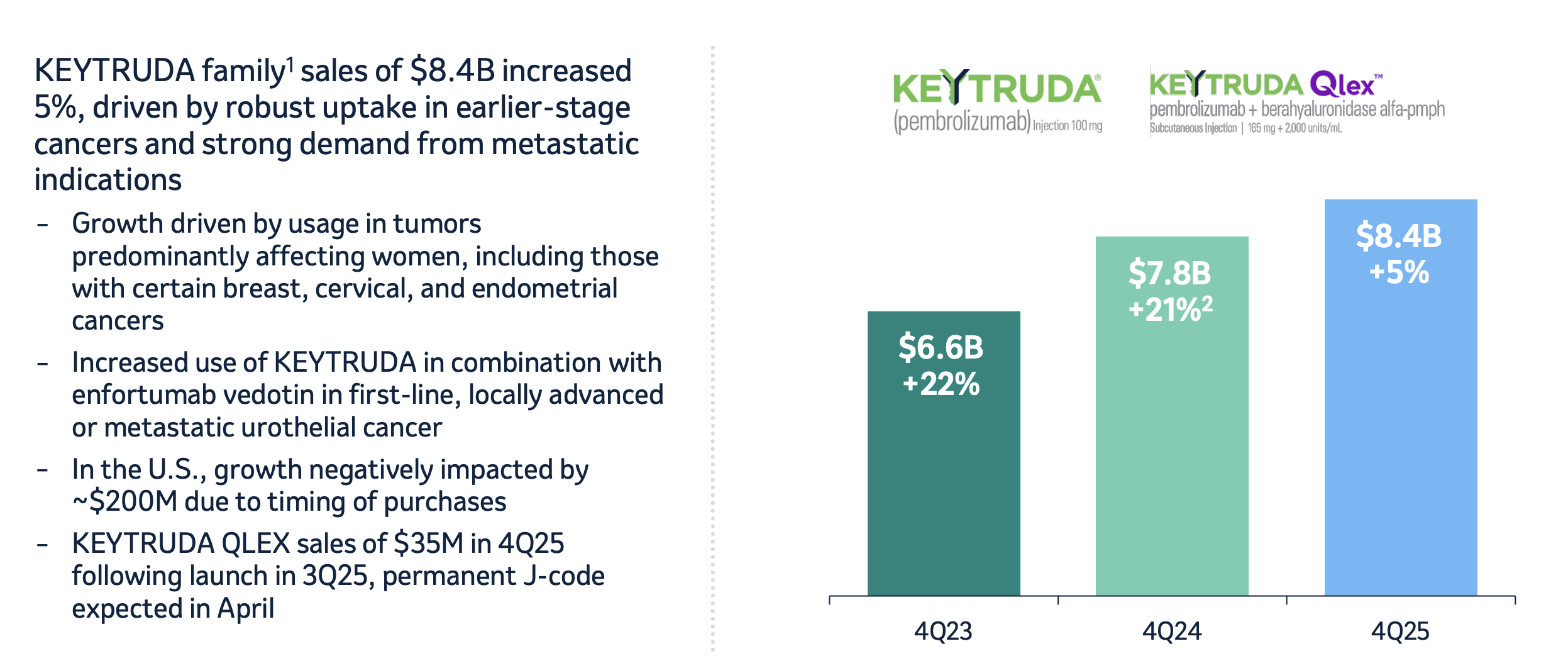

Merck’s most important drug is Keytruda, at more than $32 billion in annual sales, with a concerning 2028 patent cliff.

Merck Investor Presentation

The drug has continued to see lofty annual sales growth, with 22% going into 2023 and 21% going into 2024. The company’s 2025 guidance is another 5% sales growth to $8.4 billion in quarterly revenue. Keytruda has seen its growth as it’s become a premier front-line cancer treatment across a variety of cancers, changing lives.

Keytruda Qlex has been approved, which can help with the patent cliff, but after 2028, the sales of the drug are expected to decline substantially. Tracking Keytruda Qlex and the patent risk is worth paying close attention to.

Merck Vaccines

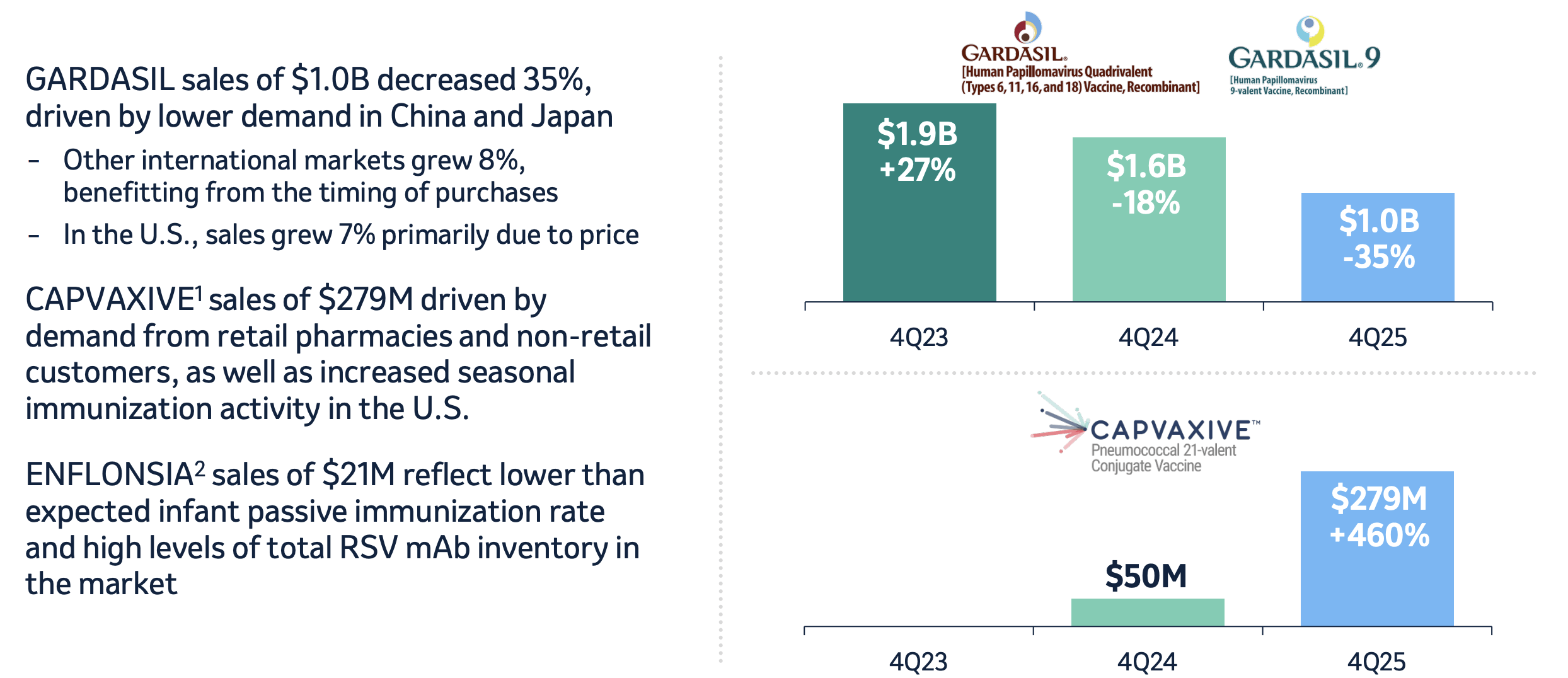

Among Merck’s largest businesses is its vaccine business, where Gardasil is the leading drug.

Merck Investor Presentation

Gardasil saw $1.9 billion in 4Q 2023 sales, a double-digit percentage of the company’s revenue. However, since then, revenue has declined nearly in half, primarily due to competition in markets like China and Japan. Capvaxive is a valuable new entry, though, that has seen sales grow 460% to more than $1 billion annualized, and the company’s vaccine portfolio remains strong.

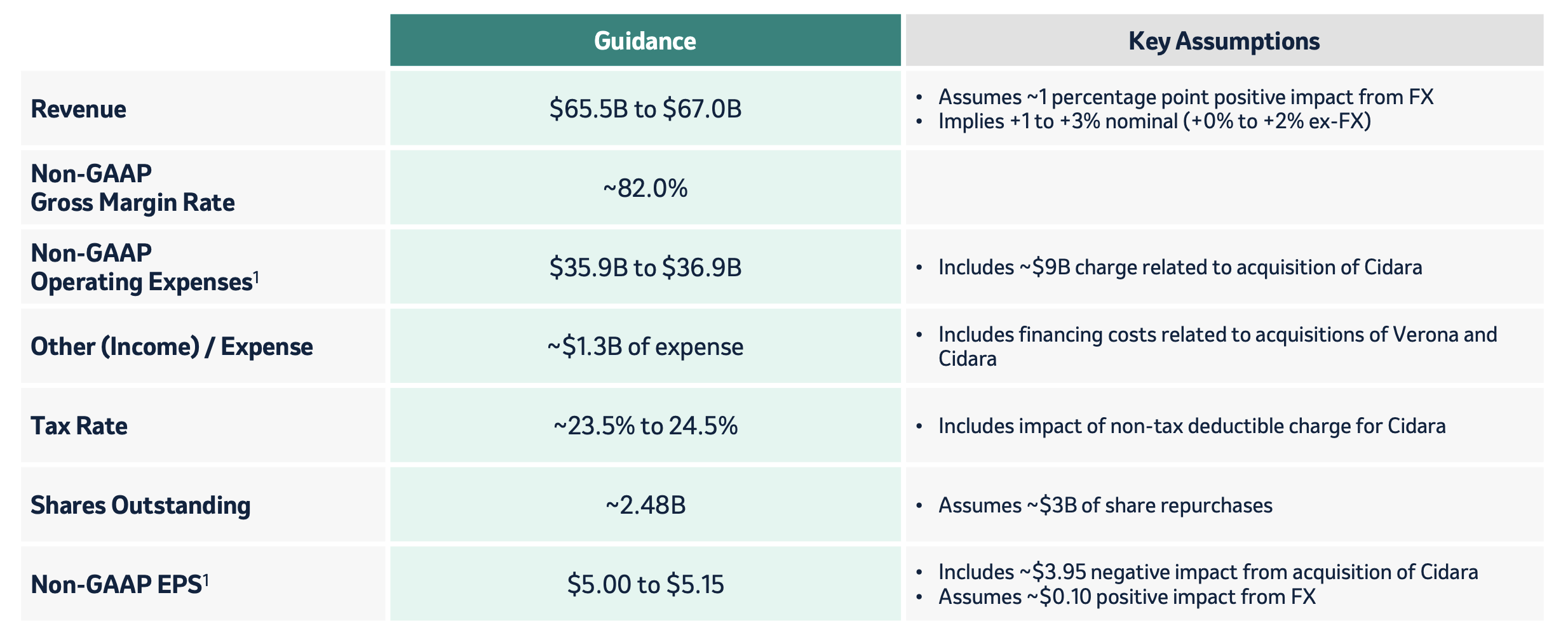

Merck 2026 Guidance

Looking into 2026, Merck is guiding for strong shareholder returns with an almost 2.8% dividend yield.

Merck Investor Presentation

Merck’s revenue guidance, as we already discussed, is ~$66 billion at the midpoint with ~2% nominal growth. Margins are expected to remain strong, while operating expenses are going up due to a $9 billion charge of Cidara. The company’s tax rates are expected to remain more than manageable, and profits will remain high.

Merck’s outstanding share count of ~2.48 billion assumes ~$3 billion of share repurchases, or ~1% of its float, which it can comfortably afford. Removing the negative impact of the Cidara acquisition, non-GAAP EPS of $9/share, is expected to lead to $22.3 billion in profit, enough to afford a wide variety of shareholder returns.

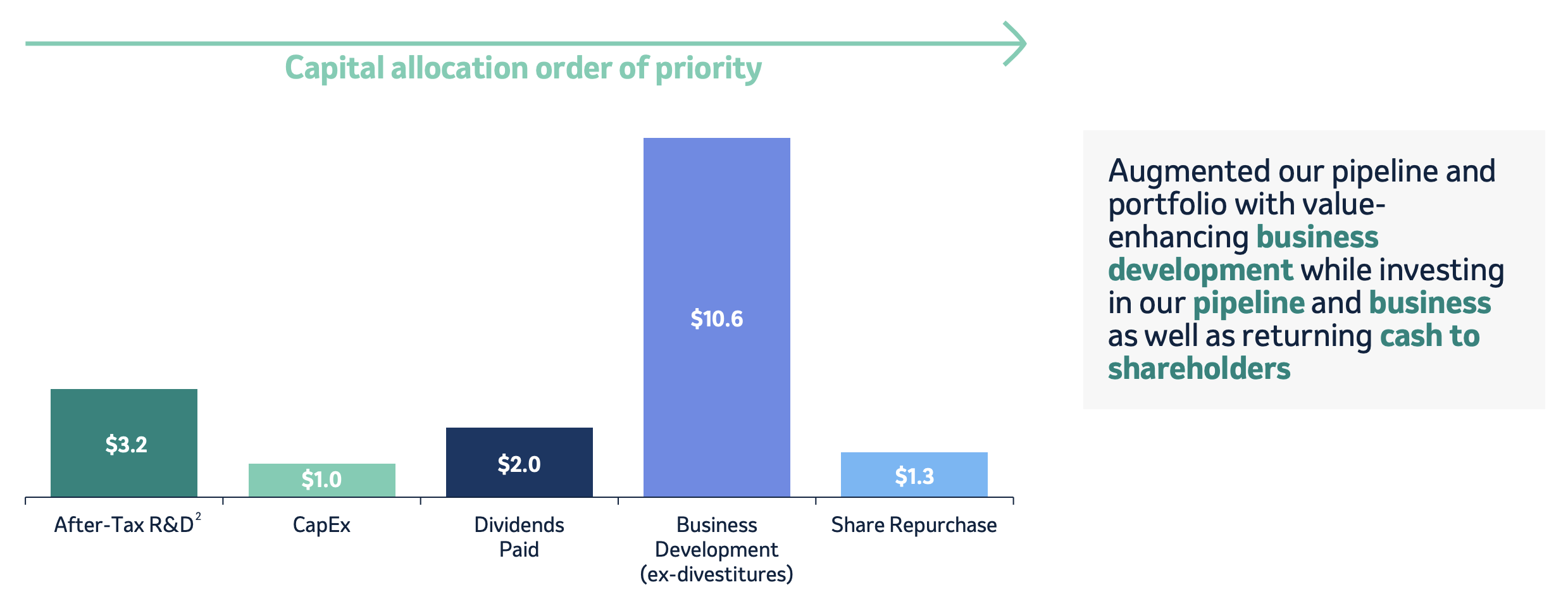

Merck Capital Spending

Merck’s capital spending involves a wide variety of shareholder returns.

Merck Investor Presentation

The company’s Q4 2025 spend had substantial continued R&D and capex ($4.2 billion), along with $3.3 billion in shareholder returns and its acquisition. Merck’s share repurchases enable close to 4% annualized shareholder returns, while the company continues to invest in its business and future growth.

The company has substantial capital plans as it works to bring new assets online and handle the Keytruda patent cliff, but we expect it to comfortably handle that.

Thesis Risk

The largest risk to our thesis is Merck’s patent cliff. Keytruda makes up more than half of the company’s revenue, something that will need to be handled going forward. The company has a plan to handle that, but whether it pans out remains to be seen, and if it doesn’t, that can hurt Merck’s ability to drive future returns.

Conclusion

Merck has an impressive portfolio of assets and a commitment to shareholder returns. The company continues to see revenue growth driven by the best-seller and game-changing Keytruda drug. At the same time, the company is looking at multi-billion dollar acquisitions that can position Merck to drive future shareholder results.

Merck’s 2026 EPS is expected to decline, impacted by the company’s Cidara acquisition. However, the company will be able to maintain a strong dividend yield and share repurchases. That makes Merck a valuable long-term investment.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.