Investment Thesis

GARP (Growth At a Reasonable Price) is by far my preferred strategy, strictly speaking about stocks, because options are much more complex and versatile. And while my stock portfolio is mostly focused on IT (hardware and software), I also look at other industries for diversification. For example, in biotech I look for the following traits:

- Either a company with a portfolio of products in an incipient phase to give it very high-growth potential and free cash flow positive. However, these are difficult to find; there are mostly some niche companies here.

- Or a company with a recently launched product with blockbuster potential, with a cash position large enough to last until they become free cash flow profitable, and preferably debt-free.

- Or a company with a product in an advanced phase and with high chances of approval. I sometimes close these positions immediately after approval, or even just before approval if the stock advanced enough, depending on factors like fair value estimate, cash position, etc.

Therefore, I look for very high growth ahead, although I acknowledge that these profiles come with a high risk too. That’s why I usually initiate small positions in about 10 names. Even if one of them crashes, my biotech sub-portfolio (which is just a small part of my entire portfolio) should still be good enough.

One of the companies that fits well in the second category is CRISPR Therapeutics AG (CRSP). It has a newly launched product in the gene-editing area, CASGEVY, which clearly has blockbuster potential. With ~$1.97B in cash & equivalents and no debt, they have a cash runway of at least 2-3 years. Then, for this category, I usually look for companies with 2-3 products in their pipeline, just enough to offer them some sales continuity but not too many to deplete their cash reserves too fast. However, since it’s difficult to find this combination, I sometimes look at companies with one launched product and no pipeline and other times at companies with one product and a more extended pipeline. CRISPR is in this last group, but I am content with their cash position (for now).

The next question is, of course, is the current price appealing enough to initiate a position? I will try to answer below.

Business Analysis and Market Estimates

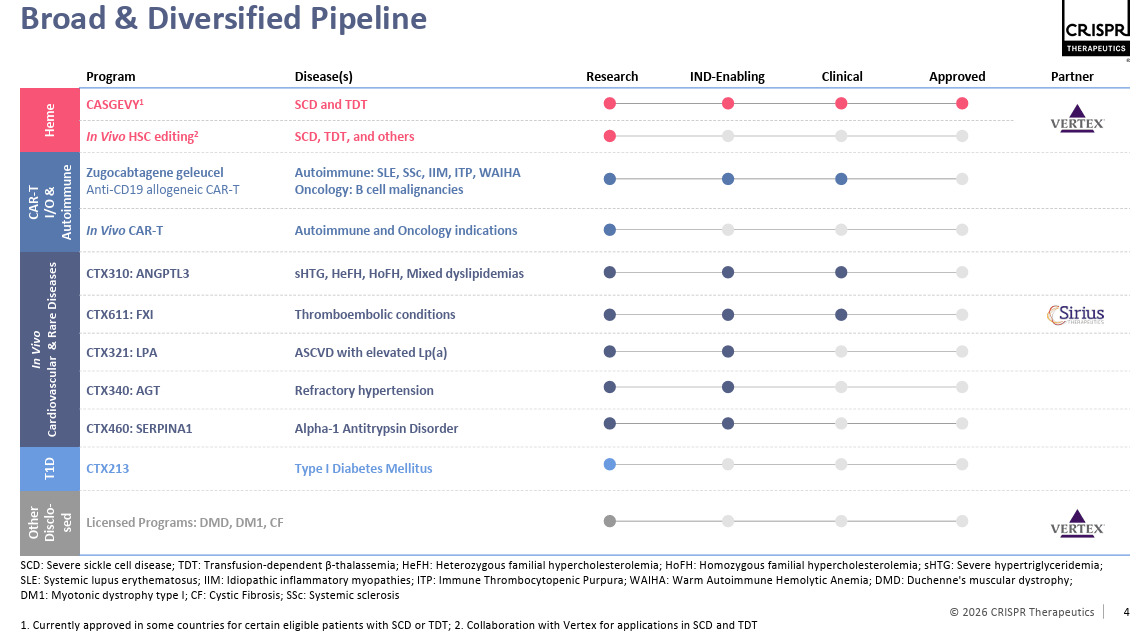

CRISPR Therapeutics is a Swiss-based company focused on developing gene-based medicines for serious human diseases. Like mentioned in the introduction, they have a broad and diversified pipeline, which I usually don’t find a good idea for non-profitable companies relying on a single product. I generally prefer them to focus on 2-3 pipeline drugs until they become free cash flow positive, and then they can diversify. But let’s see in more detail:

Figure 1: CRISPR Therapeutics Pipeline (Investor Presentation)

CASGEVY

CASGEVY is an ex vivo gene-editing therapy designed as a one-time treatment for patients aged 12 and older with severe SCD (sickle cell disease) or TDT (transfusion-dependent beta-thalassemia) by using the CRISPR-Cas9 technology. It is jointly owned by Vertex Pharmaceuticals (VRTX) and CRISPR Therapeutics, with Vertex recording 100% of the revenue and costs and subsequently sharing 40% of the net profits or losses with CRISPR.

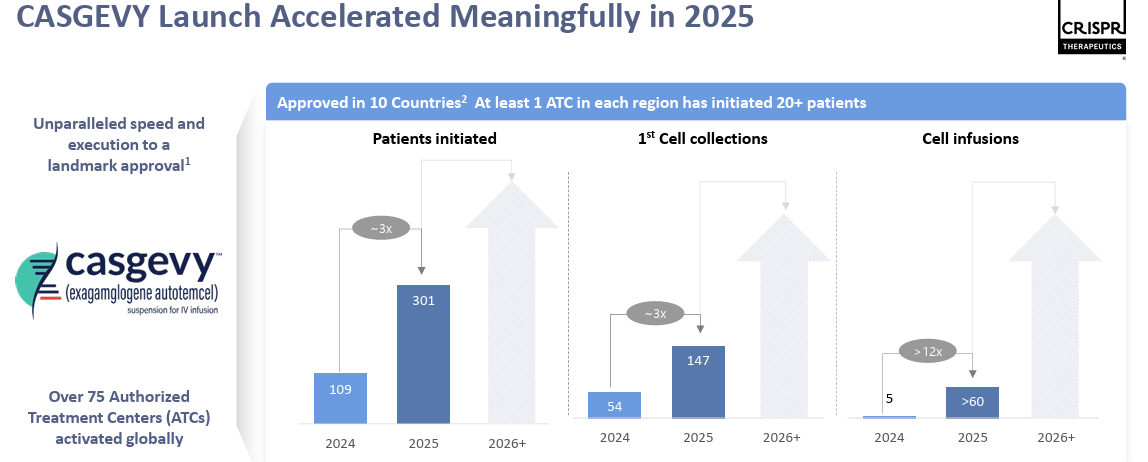

Launched in 2024, CASGEVY accelerated meaningfully in 2025, with infusions occurring in all regions (US, EU, UK, Middle East) for both SCD and TDT:

Figure 2: CASGEVY Number of Patients (Investor Presentation)

The biggest hurdles for CASGEVY are its logistical complexity, safety concerns, and high cost. The process involves extracting patient cells, shipping them to a specialized facility, editing them, and re-infusing them. The safety concerns are mostly related to a pre-conditioning chemotherapy phase, used to clear existing blood-forming stem cells from the bone marrow. However, the benefits of CASGEVY are generally considered to outweigh the risks of the associated chemotherapy, with 100% of SCD patients and 98% of TDT patients achieving 12 consecutive months of freedom from hospital (with a mean duration of 36 months and 40 months, respectively) and with ~95% of patients free of vaso-occlusive crises for at least 12 months.

The list price is $2.2M in the US, which triggered some discussion about its “equitable access”. There is a close price in Canada, C$2.8M (~$1.9M), with some requests to reduce it to C$1.7M. In the UK, the list price is GBP1.65M (~$2.1M), although there are some discounts. The official EU-wide pricing is not public, with confidential negotiated discounts applied in different European nations, but it’s also expected to be close to $2M. With some normal discounts, I’ll model an average of $1.5M per patient.

In the next step, I look at their potential market:

- There are about 35000 plus 23000 patients considered immediately eligible (with severe forms of SCD and TDT).

- There is potential for expansion into pediatric severe SCD and TDT, with good results presented in 2025 and regulatory submission expected in H1 2026.

- TAM is significantly larger with in vivo and non-chemo conditioning (and I must say that this is a main reason for my interest), with CRISPR’s LNP (lipid nanoparticles) technology and Vertex actively working on a gentler conditioning, although just in research for now.

CASGEVY’s main competitors are:

- bluebird bio/Genetix: Lyfgenia (for SCD), although with a black box (and curiously enough, with a higher list price than that of CASGEVY), and Zynteglo (for TDT).

- Beam Therapeutics: Risto-Cel (in development for SCD).

In conclusion, I model a total of 58,000 potential patients (I ignore the expansion potential because it’s too far away in time) x 50% market share for gene therapies (due to chemo risks and insurance coverage) x 1/3 for CASGEVY x $1.5M average price x 40% for CRISPR = ~$5.8B for 2030.

However, CASGEVY has orphan drug exclusivity until 2031 in the US and about the same in the EU. Other emergent players could enter the market in 2031, so I model halved revenues for 2031, followed by other modest decreases.

Pipeline

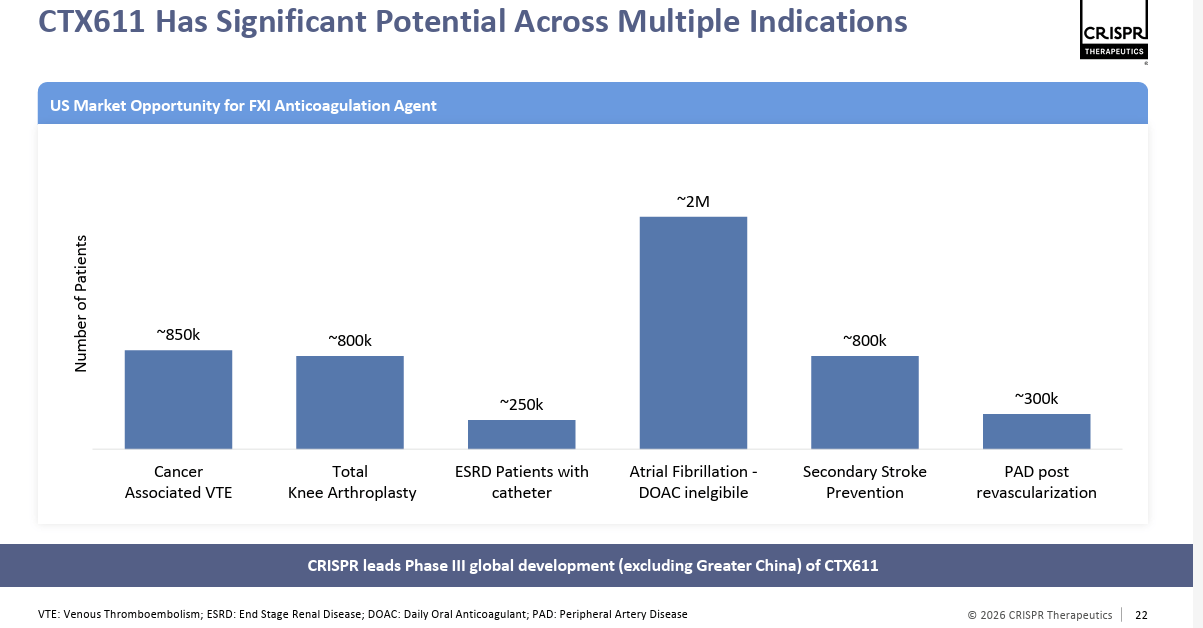

CTX611 is their most advanced candidate. This is a factor XI siRNA, a long-acting anticoagulant that uses small interfering RNA to knock down the production of clotting Factor XI in the liver, aiming to prevent thrombosis without causing significant bleeding risks. It is in an ongoing Phase 2 clinical trial in patients undergoing TKA (total knee arthroplasty), but with multiple indications seen as possible:

Figure 3: CTX611 Potential (Investor Presentation)

The thrombosis market size is estimated to reach ~$40B in 2031. Factor XI is a small piece of pie in 2025 but is estimated to have ~8% CAGR. With intense competition either from other Factor XI or from diverse oral inhibitors, I see maybe between $500M and $2B potential peak sales x 30%-40% probability of success (potential launch in 2029) x 50%-50% with Sirius Therapeutics, for $150M peak sales.

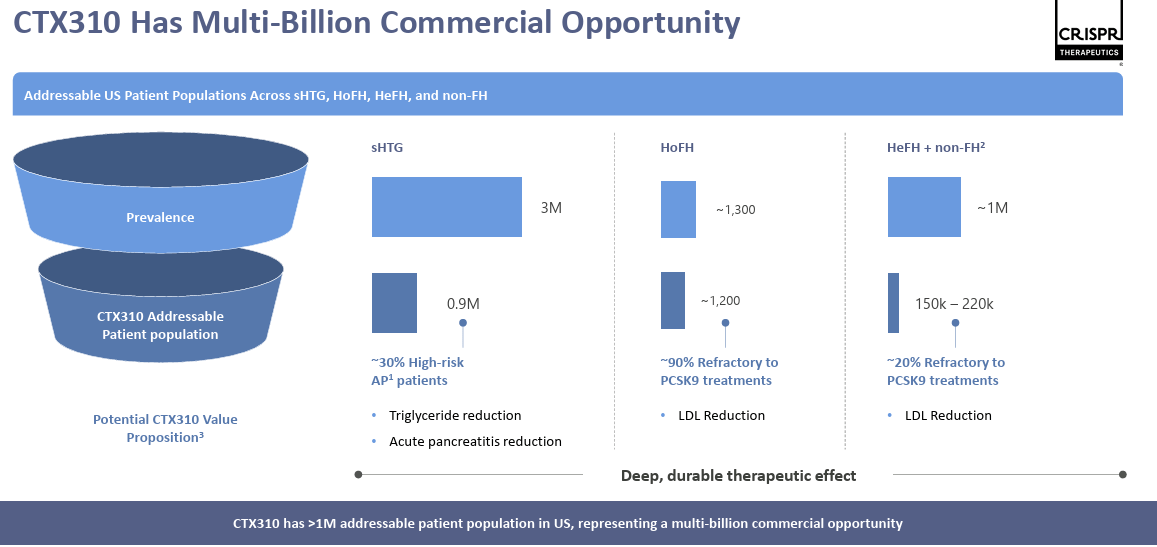

CTX310 is an in vivo CRISPR/Cas9 gene-editing therapy designed to knock out the ANGPTL3 gene in the liver. Using LNPs (lipid nanoparticles) for delivery, it aims to durably lower triglycerides and LDL cholesterol to treat severe cardiovascular diseases:

Figure 4: CTX310 Opportunity (Investor Presentation)

It reached ~50% mean LDL and ~55% mean triglyceride reductions with a well-tolerated safety profile in a Phase I basket study. The company sees a “multi-billion commercial opportunity”, but with competition from Eli Lilly, which acquired Verve Therapeutics‘ similar program, let’s round it to $1B. With a 15% probability of success for a Phase 1 program (and potential launch in 2031), I model $150M peak sales.

Zugo-cel is an allogeneic CAR-T, which uses immune cells from healthy donors, in Phase 1 for SLE (Systemic Lupus Erythematosus) and other autoimmune diseases and Phase 1/2 in B-cell malignancies.

SLE has a ~$2.2B market size, but this is a very competitive market. B-cell malignancies is an ~$3B market today but also with very intense competition. With other risks like unclear long-term effects (allogeneic therapies have historically struggled) and severe side effects for ~17% of patients for its highest dosage, I pass; I don’t model anything.

Fair Value

I find a relative valuation not suitable for CRSP because it just started to generate sales from CASGEVY and because it’s a unique, gene-editing company.

For an absolute valuation, I use a 10-year DCF (Discounted Cash Flow) model, and I start with my peak sales estimates described in the above section:

| (million USD) | 2026 | …2030 | …2035 |

| CASGEVY | $43M | $5800M | $2200M |

| CTX611 | $40M | $150M | |

| CTX310 | $150M | ||

| Total Revenue | $43M | $5840M | $2500M |

Table 1: CRSP’s Revenue Estimates (Author)

The other assumptions in my model are:

- I model a local maximum of $350M for R&D expenses in 2028, one year before the estimated launch of CTX611; a local minimum of $325M in 2031, after the estimated launch of CTX310; and then 6%-10% growth per year, with still a healthy pipeline, for a 16.5% margin in 2035.

- For “Collaboration” expenses, I model a CAGR of 30% through 2029 for the CASGEVY launch (and CTX611, but with 30%-40% probability), followed by modest growth for about ~29% margin in 2035. However, for CTX310, I will model Cost of Revenues because this is only internally developed, with a 20% terminal margin in 2035, in line with other biotech companies.

- G&A expenses grew only marginally last year, but I do model a healthy 7% growth rate with more products in advanced phases.

- Terminal tax rate in 2035: 24%, but this is just an estimate; it can vary with multiple jurisdictions and unclear fiscal policies.

- Growth in perpetuity: I usually model 0% for small biotech companies, but here I will model 1.5%, coming either from in vivo or non-chemo conditioning for CASGEVY or from other candidates in pre-clinical stages.

- Discount Rate: I usually model 12%-13% for a company relying on a single product, ~12% with an already launched product, and ~13% with a product waiting for approval, so I will model 12.25% in this case.

Resulting Fair Value is $91.95, about 73% potential upside from the current price ($53.07). For an analysis of sensitivity, let’s further vary growth in perpetuity and discount rate:

| Fair Value | Rate = 13.5% | Rate = 12.25% | Rate = 11% |

| Growth = 0% | $80.25 | $88.08 | $97.62 |

| Growth = 1.5% | $83.09 | $91.95 | $103 |

| Growth = 3% | $86.75 | $97.06 | $110.39 |

Table 2: CRSP Fair Value Estimate (Author)

We can observe the stock undervalued even with more modest assumptions: a discount rate of 13.5% and zero growth in perpetuity.

However, I think that revenue is the variable with the biggest uncertainty in the model, so I want to do another exercise, a reverse DCF: what revenue inputs would be necessary to justify the current price? If I model a more modest growth to CASGEVY peak sales of $3B in 2030 (accompanied by slightly lower growth for “Collaboration” expenses), followed by a constant $1.6B from 2031 to 2035, then Fair Value would be $52.59, around the current price. This is not such an unlikely scenario (more about risks later).

Short-Term Signals

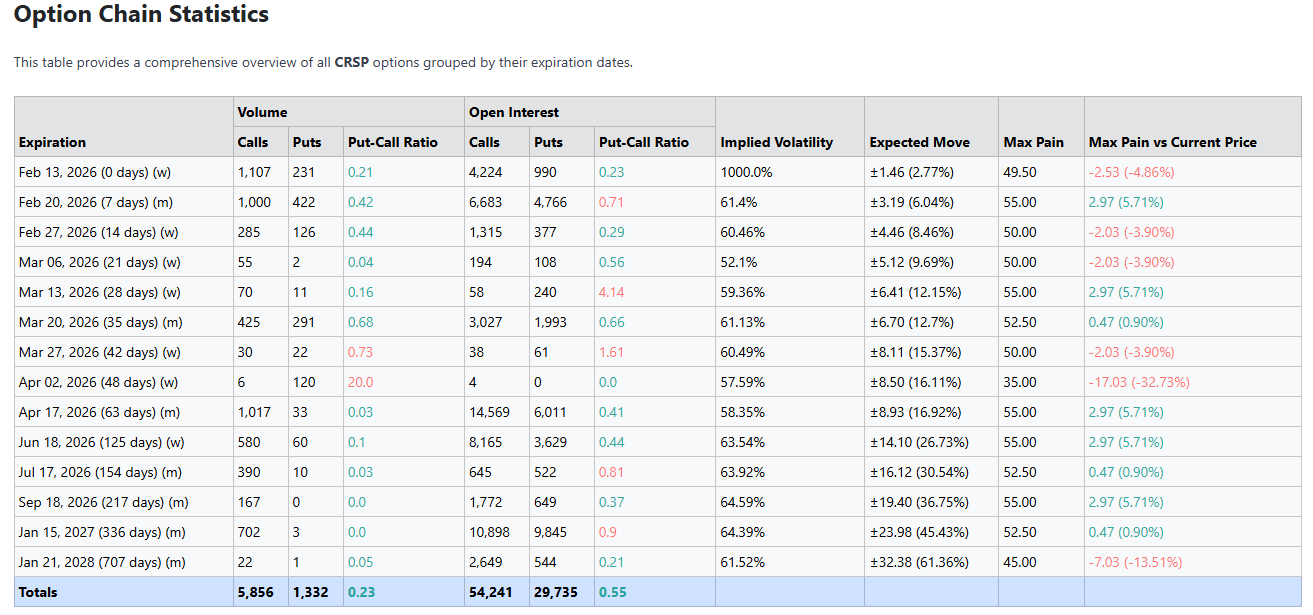

The options market can give us many interesting hints. For example, an Open Interest Put-Call Ratio of 0.55 is considered bullish because there are more Call options than Put options:

Figure 5: CRSP Put-Call Ratio (OptionCharts)

This is truly a bullish signal, because the Call options are spread over multiple expiration dates and strike prices and are especially OTM (Out-of-The-Money). Even more, let’s look under the hood at the Jan ’27 expiration, where there are apparently many Put options too. But there are 2102 Puts for the $55 strike and 2239 for the $52.5 strike, so it’s clear that this is, in fact, a Put Spread. If we ignore them, the Open Interest Put-Call ratio is ~0.46. And if we also consider the bullish Volume Put-Call Ratio of 0.23 (although these transactions came immediately after the last earnings report, so it’s less likely to be from insiders), I consider this signal strong.

For a second signal, if we look at insider transactions, there are two purchases in July and August last year at $52.03 and $57.03, so around the current price, and especially the first one had a very large value. I consider this signal moderate; for a strong signal, I would like to see more recent insider purchases.

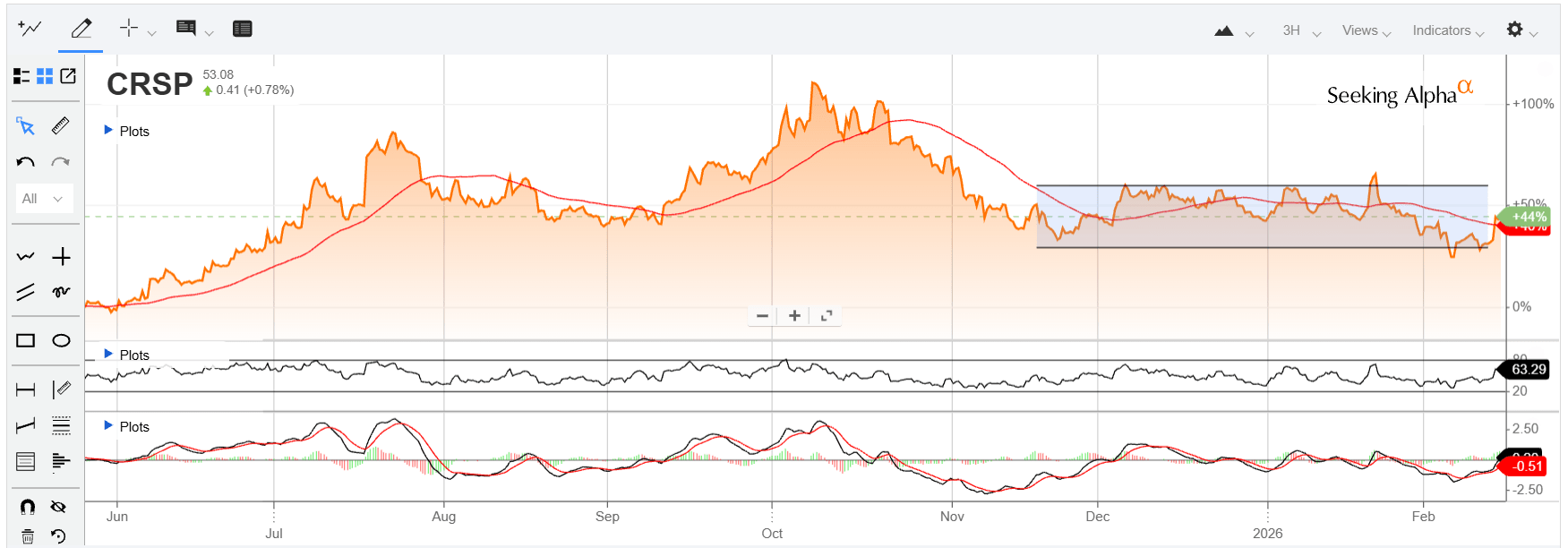

Then, if we look at technical analysis, we can see the stock crossing its 50-day moving average upwards, which can sometimes be bullish, like it was in June-July or in September-October:

Figure 6: CRSP Technical Analysis (Seeking Alpha)

However, the stock has been in a consolidation pattern since December, so this signal is not so clear; I consider it neutral.

Finally, CRSP’s short interest is very high, with ~25% of the float shorted. However, please notice that this is a decreasing trend since July 2025; therefore, I consider that these two signals offset each other. There is also a possibility of a short squeeze, but this is difficult to predict; we can see the stock going down from October until December despite a decreasing short interest. Therefore, I consider this signal neutral.

Risks

With this very high price, CASGEVY is dependent on insurance coverage. It seems that ~90% of US patients have reimbursed insurance access to treatment, and likely about the same in the EU, but things can change, especially in the US, after the expiration of its NTAP (New Technology Add-On Payment) status, while in other countries there are usually multi-year agreements. If we add that some patients might be reluctant to undergo chemotherapy, that’s why I included in my model only 50% of eligible patients for 2030.

I also talked about the price pressure, and not only in the US. While I modeled an average price of $1.5M, things can change until 2030; for example, a multi-year contract can be negotiated, but at a lower price. The combination of these two factors (possibly even less than 50% of eligible patients treated plus a lower price) made me say that the reverse DCF (with $3B revenue in 2030 instead of $5.8B and $52.59 Fair Value) is not such an unlikely scenario.

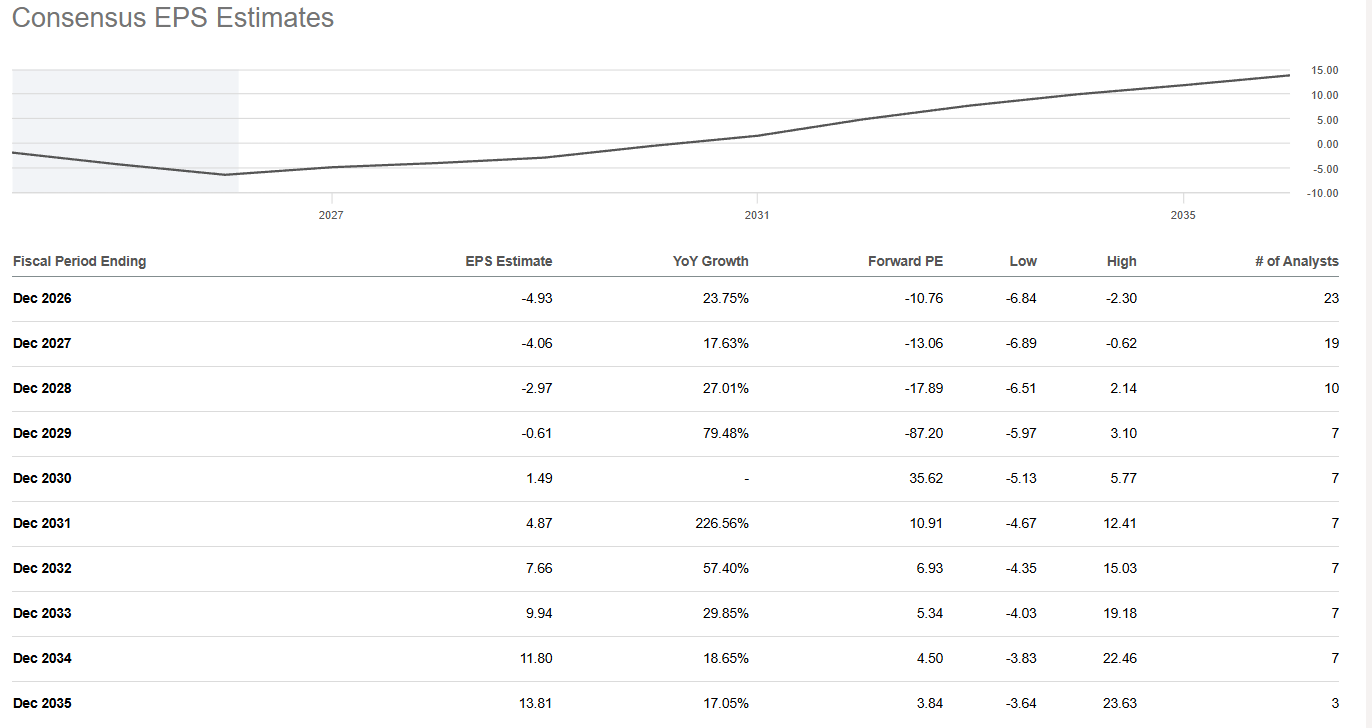

Their cash reserves of about $1.97B should easily last for about two to three years. For example, I modeled about $600M cash burn for 2026 and profitability by 2029. With higher sales in 2028, cash burn should be lower; therefore, they have chances for enough cash runway without needing to raise more capital. However, I acknowledge that both R&D and Collaboration expenses could come higher, so they might need more capital somewhere in 2028-2029. Especially if we look at consensus, they are estimated to become profitable only by 2030:

Figure 7: CRSP Consensus EPS Estimates (Seeking Alpha)

Finally, there are several risks related to their dependence on a single product. For example, Intellia Therapeutics (NTLA) suffered a severe crash after a patient died after receiving its gene-editing treatment. While they use different approaches (Intellia’s treatment is in vivo) for different diseases, and while no death or secondary cancer has been associated with CASGEVY or its chemotherapy yet, this is a very serious risk, even if unlikely.

Then, like I said, I hope they could advance to an in vivo or non-chemo gentler conditioning, but what if some competitors could come up with such a solution first? Some good results even in a more incipient phase, combined with a lack of results for VRTX/CRSP, could also dramatically affect CASGEVY. And if we add the eventuality of failure in CTX611 and CTX310, that could dramatically affect the company.

Strategy

For a GARP (Growth At a Reasonable Price) stock, I usually initiate a position when the sum Undervaluation + Revenue growth + Free Cash Flow yield is greater than Uncertainty Threshold.

For a company in such an incipient phase, it’s more difficult to choose revenue growth because they start from a very low base (basically zero). Therefore, I will use my CAGR estimate only after 2026, which is ~57% through 2035.

For Uncertainty Threshold, I use the following values:

- About 35% for a medium uncertainty

- About 50% for a high uncertainty

- About 75% for a very high uncertainty

I generally use a very high+ uncertainty for a company relying on a single product, or even extreme if that product is not approved yet. In this case, there is a rich pipeline, but this is more than offset by the risks associated with CASGEVY, especially since I noticed that reverse DCF scenario with not-shy chances. Therefore, I will use an uncertainty threshold of 90%.

With the sum 73% (undervaluation) + 57% (estimated revenue CAGR) – 12% (free cash flow yield, estimated for 2026) = 118%, CRSP is above my uncertainty threshold; therefore, I rate it as “Buy.”

However, with so many risks mentioned above, some of them severe, some with not-shy probability, I limit my position to ¼ or 1/3 maximum. But then, why am I still getting involved? Because, while I see very high risk, I see even higher potential reward. If they could come first with in vivo/non-chemo conditioning, or if they report good results for their pipeline candidates, the stock could easily fly above $100 (perhaps helped by a short squeeze in such scenarios), and my initially small position will simply grow due to price appreciation.

In my personal portfolio, I opened a tiny ~0.12-0.13x position in spring 2024 (which grew to ~0.2x today due to price appreciation), and I am adding another 0.12-0.13x today. For my Seeking Alpha portfolio, since this is my first article about CRSP, I will just model 0.25x at today’s price.

Takeaway

CASGEVY’s gene-editing therapy targets severe SCD and TDT, and I model 2030 peak sales of $5.8B, based on market size, market share, and price estimates. However, with orphan drug exclusivity only until 2031, I model $2.5B in sales in 2035, with minor aid from pipeline candidates CTX611 and CTX310.

CRSP trades at ~$53, while my DCF-based fair value is $91.95, reflecting 73% potential upside, with undervaluation even under more conservative assumptions for cost of equity and growth in perpetuity. However, more conservative CASGEVY scenarios suggest CRSP might be just fairly valued.

There are multiple risks, like CASGEVY’s insurance coverage, pricing pressure, potential adverse CASGEVY effects, especially related to chemotherapy, dependence on a single product, pipeline execution, and possible competitive threats.

I limit my position to 1/4-1/3, with very high+ uncertainty, but asymmetric reward if the pipeline advances.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.