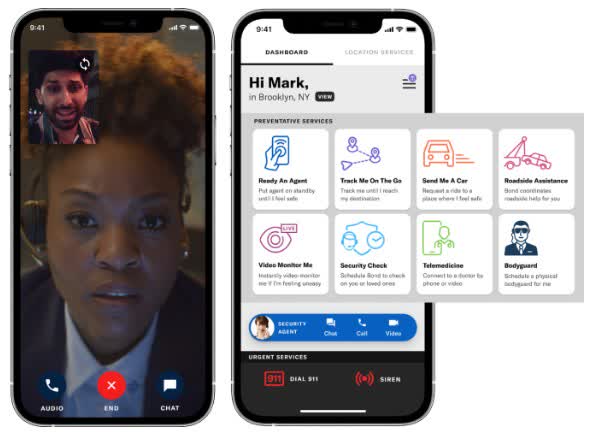

Our Bond (OBAI), also known by its official corporate moniker TG-17, Inc., provides preventative personal security products and services delivered via a proprietary mobile application and backed up by live agents. Called the Bond Preventative Personal Security Platform, the application is accessed on a mobile device like a phone or tablet to engage a remote agent when the user is worried about their situation. The user can ask the agent to stand by until they feel safe again or track the user until a safe location is reached. The user can also ask the agent to monitor the situation on video and even warn off suspicious characters through the user’s mobile device microphone. If necessary, the agent can summon police or an ambulance using the 911 system.

The platform is not just for emergency situations. Users can also plan ahead for a bodyguard or secure car service. Medical or roadside assistance can also be summoned.

The company boasts over 1.4 million cases handled since its inception in 2020, including over 10,000 emergencies where lives were at stake.

ourbond.com

Source: Our Bond Corporate Website at ourbond.com

- Spot-on market timing for new security services as global tensions rise and local communities experience rising theft and assault rates

- Proprietary suite of personal security services using a mobile application branded the Bond Preventative Personal Security Platform

- Early entrance to the security market allows time to capture market share and establish a deep moat around the Our Bond brand and the platform’s robust suite of features and options

- Integrated artificial intelligence technology drives platform differentiation and effective service execution

- Ubiquitous availability of smartphones and cellular networks affords a widespread addressable market around the world

- Proven product marketability and user satisfaction through zero subscription cancellations since inception

- Efficient product marketing and delivery through cost-effective B2B sales channel

AI Implementation: Here’s the beef!

Our Bond is using AI in several ways to enhance its platform performance. The company has developed a rule-based system based on historic data to detect anomalies in user-shared video. Third-party AI tools are being used to support agent decision making. Importantly, Our Bond relies on third-party AI applications to automate translation in the various countries where it provides services.

The use of AI is expected to deepen as Our Bond completes development of its own technology. A top priority for the company is work on machine learning models that will use historic anomaly data to improve threat detection in user-provided or public video. In simple terms, the AI-based process will use intelligence built on historic observations to supplement rule-based and human threat detection.

Investors may come across the acronym AI RAG (Retrieval-Augmented Generation) bandied about to impress. It simply references AI-driven output referencing knowledge beyond the training data used by a large language AI model. Bond plans its own RAG to incorporate its proprietary processes and content into third-party data.

Bond is also relying on AI technology in behind-the-scenes administrative functions. The company is already using third-party AI-driven interview and candidate assessment tools. Plans are underway to use AI-driven virtual agents for live-agent training and evaluation. The result should be a more effective and efficient live-agent force, delivering better results for users and improved profit margins.

Details on Our Bond’s platform and its technology development plans are described in the company’s registration statement at sec.gov. The company’s corporate website also provides illustrations of its Bond Platform and business model

Fast Growing Security Services Market

Depending upon whether investors see the world through a ‘half empty’ or ‘half full’ prism, the world is either sadly becoming more precarious or a new, exciting market is building for personal security services. Industry research firm, Real Time Data Stats estimates the personal security market will be valued at approximately $112.2 billion in 2025. Of course, the impressive market size numbers include conventional on-site security personnel and monitoring systems.

Urbanization, rising crime rates, and consumer interest in proactive security measures are driving demand for creative security solutions. Real Time estimates the market could grow at a compound annual growth rate near 10.5% to reach $250.5 billion by 2033. Another industry research firm, Verified Market Reports, also finds a significant market opportunity characterized by strong growth. Verified estimated the global personal security market was valued at $144.6 billion in 2025 and growing at a compound annual rate of 8.1% to reach $284.5 billion by 2033.

A more compelling point for investors is that the fast pace is being driven by a shift in interest towards on-demand personal protection services such as the Bond Platform. On-demand services delivered through mobile apps and cellular networks can be as effective as conventional solutions, yet flexible and economical compared to the long-term contracts required by full-term in-person or on-site security arrangements.

Customers: Large, Loyal, and Global

In addition to economy, Our Bond’s platform has the advantage of versatility that makes it suitable in a variety of situations, such as employees who work alone, individuals in remote locations, and high traffic situations such as apartment complexes. Rather than focusing on vertical markets by industry, the company’s marketing and sales team appeals to users in such situations.

For the corporate prospect, the sales pitch can be based less on emotion and more on the reality of employee insecurity. The business consulting firm, McKinsey estimates workplace violence costs businesses an estimated $130 billion globally each year for absenteeism, lost productivity, medical compensation, and lawsuits, among other costs. The use case for the Bond Platform could be compelling for a risk averse employer.

The Bond Platform is now available in twenty-eight countries around the world. Potential customers can seek advice from Our Bond’s stable of security advisors hailing from high profile positions in law enforcement and security across the U.S. and Europe.

Our Bond leadership has been somewhat circumspect about its customer base, simply claiming ‘two of the three largest corporations in the world’ among its subscribers. The company has also described a large private equity fund and a family investment office as significant customers. Additionally, a ‘top smartphone vendor’ and a leading credit-card company have been mentioned. Most recently, Our Bond disclosed the successful completion of a pilot deployment of the Bond Platform by a major municipality, which has indicated it will offer Bond services to all city employees.

Importantly, Our Bond boasts a 100% customer retention rate in the first years of operation. It may not be possible to maintain a perfect record indefinitely, especially since the company’s annual subscription model is only moderately ‘sticky.’

Competition: Threat or Validation?

The company’s management team downplays direct competition. Nonetheless, it is notable that several other mobile apps for security services have been developed in recent years. For example, the StaySafe Lone Worker App is also marketed to corporate subscribers by Ecoonline. Similarly, Panic Guard provides a personal security app for solitary workers and travelers. While these players may not have the same feature-rich service platform or business model as Our Bond, their entrance onto the playing field helps validate the use of mobile applications to provide on-demand security services.

It is not likely that Our Bond is experiencing any immediate rivalry for customers from these services, as the Bond Platform should fare well in a side-by-side comparison. The company may experience more competition from providers of conventional on-site security personnel or installed video monitoring systems, where entrenched business relationships dominate purchase decisions.

Financial Resources

To stay ahead of the competition, Our Bond must make capital investments in marketing and customer acquisition programs as well as new technology development. Does the company have deep enough pockets to achieve its goals?

In a direct offering of common stock in early February 2026, a significant portion of company’s capital stock was registered for public trading. Only previously issued common stock was registered for sale by current owners. Additionally, non-voting shares of common stock, originally issued in conversion of certain preferred shares, were switched to voting and are now registered common stock. No new capital was raised by the company with the ‘going public’ step.

Fortunately, Our Bond is not without access to the capital market should it need more cash resources. Concurrent with the registration of common stock, the company consummated an equity line of credit. Over the next three years, Our Bond can put up to the creditor shares of common stock valued at up to $300 million. Importantly, the company is not obligated to use the line of credit should the stock price drift to an unacceptably undervalued level.

In the meantime, the company is relying on existing cash resources. Our Bond reported $925,000 on its balance sheet at the end of September 2025, the most recent figures disclosed in the company’s registration statement with the Securities and Exchange Commission. However, subsequent to the quarter close, the company raised an estimated $2.9 million in new capital through the sale of preferred stock and warrants. An agreement was also reached to sell additional preferred stock for $2.1 million at the time of Our Bond’s direct offering. Based on recent cash usage rates, we estimate the company has approximately $2.7 million in cash resources in the first week of February 2026.

Expectations for Internal Cash Flow Generation

Since Our Bond is still scaling operations, the company has yet to turn a profit. In the year ending December 2024, Our Bond turned $9.7 million in sales, representing 35% growth over the previous year. Entrance into new markets and strong customer retention helped drive subscriptions.

Despite the top-line expansion, Our Bond experienced a deeper operating loss of $9.6 million in the full year 2024 compared to the year before. While less was spent on research and development in 2024, the effort to enter new markets required increased sales and marketing activity. Consequently, the company used $8.2 million in cash resources to support operations in the full year 2024.

In more recent months, growth appeared to slow to 1% year-over-year, with sales totaling $7.3 million in the first nine months of 2025. The more measured pace appeared despite a 57% year-over-year increase in sales and marketing expenditures. In the same period, operations used $5.1 million in cash resources to support operations, representing a 17% slower pace in the use of cash resources.

Subscriptions drive Our Bond’s top-line, ramping with the addition of new customers and aided by successful retention. Capacity to serve new customers is augmented with new computing equipment, engineering staff, and response personnel. Once subscriptions deliver sufficient contribution margin, the company should be able to self-finance new growth.

Management is somewhat circumspect about the number of users required to reach financial milestones. Nonetheless, investors may not have long to wait for a report of positive cash flow. Based on the recent pace in growth, management has hinted that late 2026 or early 2027 is pivotal in the company’s path to at least breaking even on a quarterly basis.

Capitalization

Our Bond has been financed by a combination of the founder’s initial equity capital, loans, and sales of common and preferred stock to a wide audience of professional and retail investors. The company’s founder, Doron Kempel, invested a total of $44.7 million in the company through his initial investment and subsequent participation in a series of capital raises through the sales of preferred stock. Kempel’s investment represents 35.5% of equity capital raised.

At the end of September 2025, the company reported capital composed of $8.1 million in long-term liabilities and a stockholder deficit of $20.0 million. Investors might find Our Bond’s capital picture somewhat murky. In addition to 3.2 million shares of common stock, the company reported at the end of September 2025, seven different series of convertible preferred stock totaling 29.1 million shares. Each series has a particular conversion price and dividend rate.

Details on Our Bond’s historic financial performance can be found in the company’s registration statement at SEC.gov.

Risks to New Investors

The investment case is easily made for a company with an innovative and comparatively feature-rich product that has already been proven through impressive customer adoption. Still, investors need to look at operational vulnerabilities as well as obstacles to full valuation of its stock.

Customer concentration. Since the company has focused on the B2B channel to get started, its customer base is populated by a few large corporate subscribers. One customer, a large private equity firm, accounted for 63.6% of total revenue in the full year 2024 and 51.9% of total revenue in the first nine months of 2025. Cash flow is also at risk, as 69.5% of accounts receivable at the end of December 2024, was attributed to a single customer. Loss of a customer or the inability to collect on historic billings could have a significant impact on future earnings and therefore stock value.

Corporate control. Kempel’s significant investment in Our Bond has resulted in ownership of an overwhelming 98.2% of the company outstanding voting common stock. Consequently, Kempel has a vice grip of control over all matters before the shareholders. Conversion of outstanding preferred stock and sales of new common stock through the equity line of credit could ultimately dilute Kempel’s ownership percentage. Nonetheless, the company will remain closely held until Kempel divests part or all of his common stock position.

Unseasoned stock. Our Bond’s common stock was registered for public trading under the symbol OBAI and listed on the Nasdaq National Market in early February 2026. Consequently, at the time of this article, the stock had limited trading history. The first few days of trading were characterized by low volumes and a relatively wide spread between bid and ask prices. In such circumstances buyers experience an immediate drop in value, and sellers may need an extended time to exit from long positions.

Limited exposure. The company chose a direct offering alternative to public registration, foregoing the usual investment bank sponsorship and roadshow introduction that accompanies an initial public offering of new shares. In its favor, Our Bond has a lengthy list of enthusiastic investors who participated in various rounds of preferred and common stock sales. We believe this group is likely to remain interested in Our Bond’s future, helping to make up for the low-key nature of its ‘going public’ step.

Nominal flotation. Our Bond’s direct offering provided for the registration of 3.8 million shares of voting common stock, composed of 180,241 shares of common stock already outstanding and 3.6 million shares of non-voting common stock converted at the time of registration to voting shares. It is estimated these shares will represent the greater portion of shares available for active trading.

The company’s registration statement also applies to an additional 30.3 million shares of common stock underlying previously issued convertible preferred shares and warrants. Should OBAI continue to trade with strength, these securities would be ‘in-the-money,’ and holders could be highly motivated to convert or exercise.

Traders should not expect the founder’s shares to help expand the trading float any time soon. Kempel had to agree to an extended lock-up agreement with the providers of the company’s new equity line of credit. Kempel’s shares remained on the sidelines until at least 95% of the recently issued Series D preferred stock were redeemed or converted.

Dilution. Traders might like to see the flotation expanded in order to facilitate ease of movement in and out of positions, but new shares of common stock also dilute financial results per share. The company has 48 million shares of convertible preferred stock and warrants outstanding with various conversion or exercise prices. Approximately 30.3 million shares of these securities have rights of piggyback registration of the underlying common stock, providing more incentive to take action.

Traders can also expect dilution from Our Bond’s use of its new equity line of credit. Initiated concurrent with the registration action, the line allows the company to sell common stock valued at a total of $300 million. The number of shares will ultimately depend upon future share prices. A future registration statement is planned to include shares issued for the equity line.

Summary

Much has been made of the potential in artificial intelligence ((AI)) technology, driving exceptional interest in the required computing devices and network infrastructure. Unfortunately, investors have had few opportunities to grab successful applications that creatively use AI in a product or service.

Investors hungry for applied AI should look closely at Our Bond, which has successfully applied AI technology to an innovative personal security service platform. Perfect subscriber retention speaks volumes about product performance and service quality.

Our Bond’s common stock recently began trading on the Nasdaq National Market under the symbol OBAI. There are risks associated with an early-stage operation that has only recently offered a publicly traded stock. For this reason, investors should consider OBAI a speculative security suitable for the patient investor prepared to hold the course to successful implementation of the company’s business objectives.

Neither the author of the Small Cap Strategist web log, Crystal Equity Research nor its affiliates have a beneficial interest in the companies mentioned herein.

Underwriters of the Prime series may have a beneficial interest in, serve as agents of, or act as advisors to the companies mentioned herein.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.