Some different portfolios for a comfortable retirement

$100,000 is a good target in retirement with the current state of inflation. Where a married couple might have been able to live on less, much less, just 10 years ago, times have changed:

visualcapitalist.com

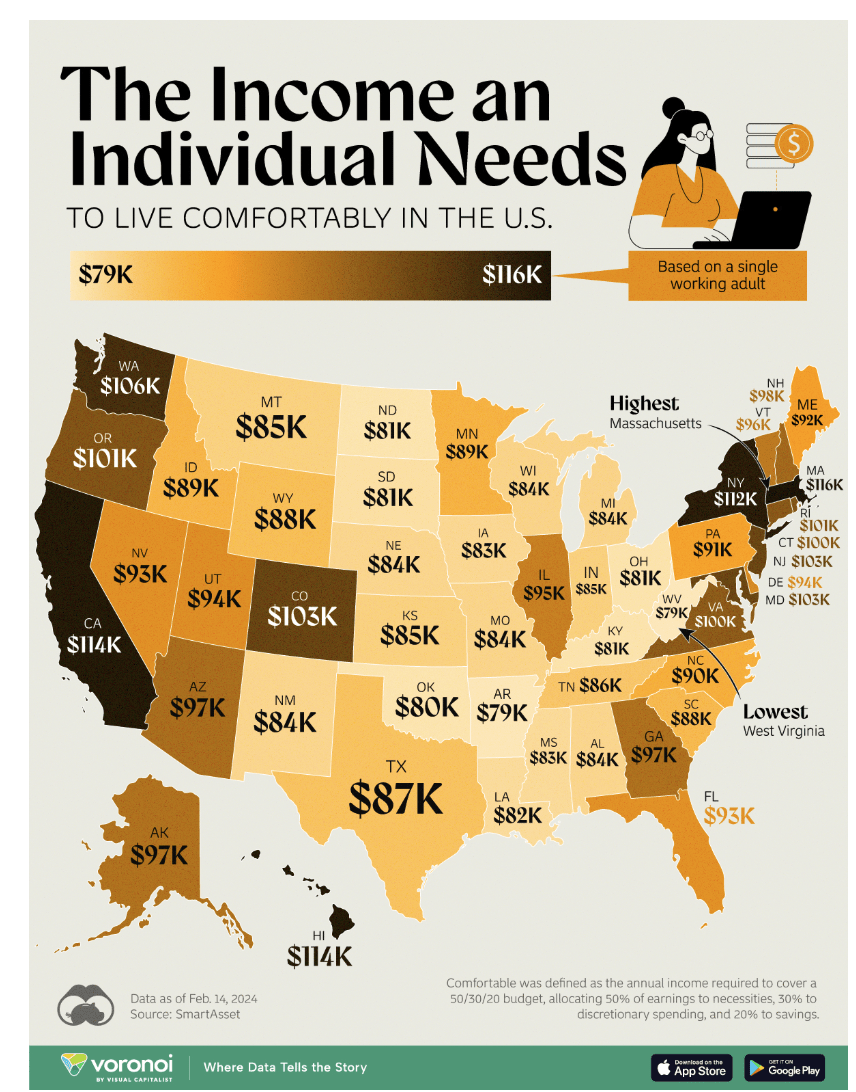

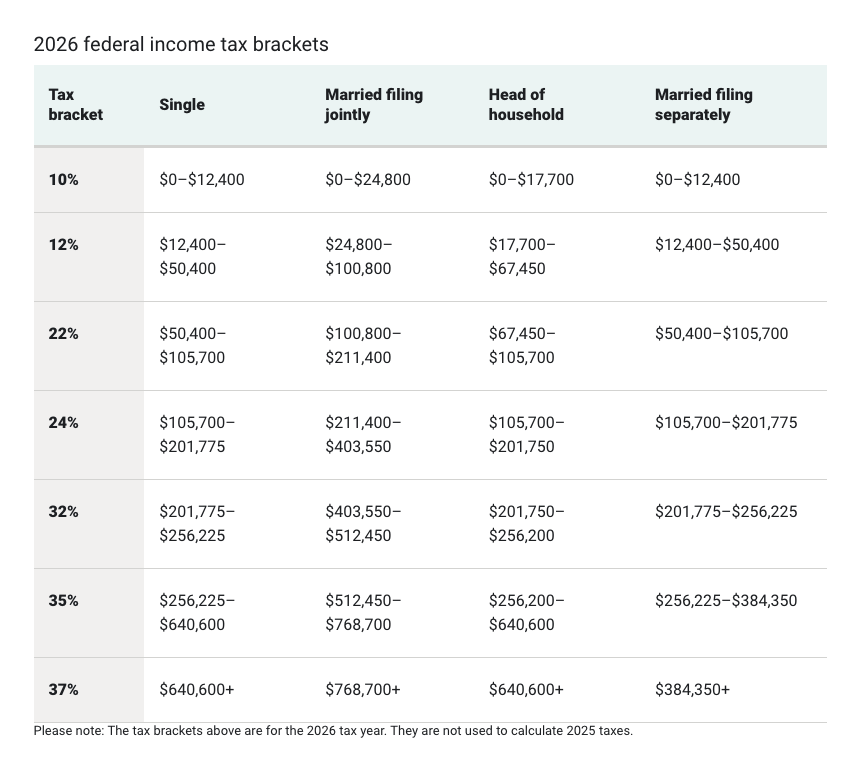

Now, this data that comes from a SmartAsset survey encompasses a single earner in the accumulation phase, not preservation or distribution. Why are the numbers so extreme for an individual? First, the individual has a compressed tax bracket due to being single. The US punishes those not married by making them hit higher tax brackets faster than a married filing jointly couple. Let’s take a look at the brackets for 2026:

ameriprise.com

We can see that for single earners, they hit the next bracket almost twice as fast a married couple with their earning ranges for each bracket roughly 50% less than a married filer.

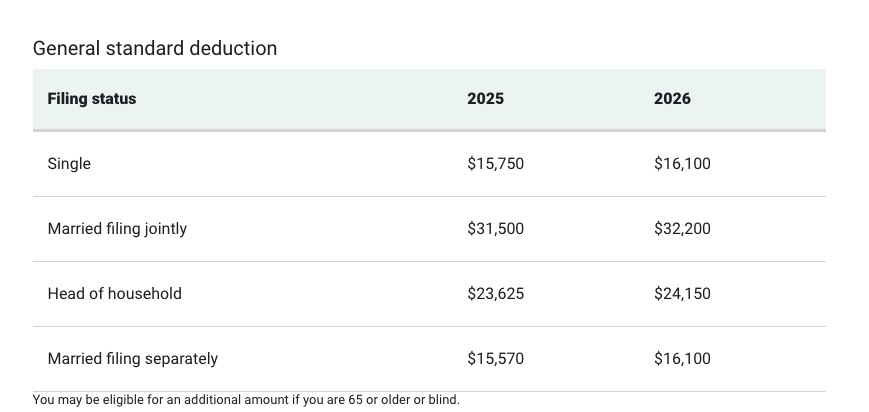

Then we get to the standard deduction:

ameriprise.com

As a double whammy, the standard deduction is also roughly 50% less for a single vs. a married filer. No wonder all the Silicon Valley bachelor tech engineers have loaded their 401Ks and tax-deferred accounts. They make as much as an entire married household but get taxed twice as hard unless they contribute as much as possible to above-the-line deductions. The story here, going into retirement, is that it also pays to be married.

Other things to be considered

After the tax considerations related to cost of living, just narrowing the focus down to retirees and early retirees, the 20% allocated to the saving number [in the survey footnotes] is now curbed downward or stopped altogether. Thus, life just got 20% cheaper with this in mind once you’ve reached financial independence.

Next, you are generating portfolio income in this hypothetical scenario [although you may also have other cash-flowing assets like rental properties and partnerships or small semi-passive businesses]. This type of income, which is not active income, is not subject to FICA tax and Social Security.

As an employee in the United States in a W2 income scenario, you are subject to 1/2 the FICA taxes, which includes Social Security [OSADI] of 6.2% for the employee, and Medicare of 1.45% for the employee portion. If that individual makes more than $200,000, there’s another .9% additional Medicare tax, and this threshold is met at $250,000 for a married couple. Just for the sake of simplicity, we’ll say those are not breached, and the now-retired individual saves another 7.65% here.

So what is the actual burden in retirement?

Now let’s use Texas as an example. The survey says a single individual needs $87k to live. Multiply this by two for a married filing jointly couple in this situation, and we get $174,000 to meet the model budget in the scenario. Now let’s chip away at this for a retired couple.

First, let’s reduce this number by 20% to cut off the new savings. We’ll also reduce it by the employee payroll taxes that go away at 7.65% for a combined total reduction of 27.65%. That puts us at $174,000 X (1-.2765)= $125,000.

Then we can also model the married filing jointly vs single standard deduction:

| Filing Status | Income | Standard Deduction 2025 | Taxable Income | Tax Savings |

|---|---|---|---|---|

| Single | $174,000 | $15,750 | $158,250 | NA |

| Married MFJ | $174,000 | $31,500 | $142,500 | $3,780 |

So now, for a married couple, we’ve whittled this down to $121,000. Also, there’s more. The goal in retirement is to get to as low a tax bracket as possible. In some cases, you can get to 0% by using only the standard deduction amount from your pre-tax accounts, only long-term capital gains and qualified dividends up to the 0% range from taxable accounts [LT cap gains and qualified dividends have a 0% bracket for taxable accounts], and then top it off with Roth withdrawals at the very end which are tax free.

Depending on the state taxes, this could shave off another $14-$20,000 in taxes. Now we’re hitting our $100,000 number. If you have a paid-off mortgage, which is normally 30% or so of a couple’s gross income, then you really get into the safety zone at $100,000.

So when we look at safe withdrawal rates or yields, let’s see what kind of nest egg we need to hit these numbers before Social Security kicks in.

The typical 4-5% portfolio

Bill Bengen recently updated his 4% rule and put the safe withdrawal rate in the last 30 years closer to 5% [4.7% to be precise]. We’ll use 5% as a nice round number. This would mean a portfolio of around $2million.

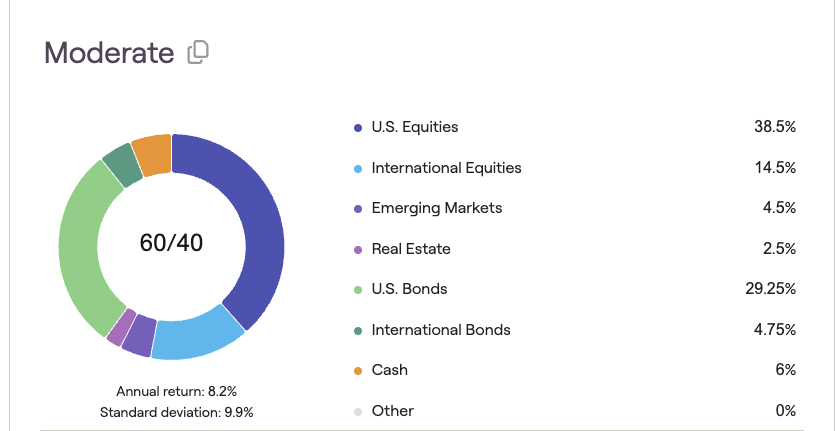

We’ll use a typical moderate 60/40 portfolio here, all adjusted for a cost-of-living increase annually of 2%.

Right Capital

To match these standard allocations, I’ll use the following ETFs:

- Vanguard S&P 500 ETF (VOO)-US

- Vanguard Total International Stock Index Fund ETF Shares (VXUS)-International

- Vanguard FTSE Emerging Markets Index Fund ETF Shares (VWO)-Emerging markets

- Vanguard Real Estate Index Fund ETF Shares (VNQ)-Real estate

- Vanguard Total Bond Market Index Fund ETF Shares (BND)-US bonds

- Vanguard Total International Bond ETF (BNDX)-Int’l bonds

- SPDR® Bloomberg 1-3 Month T-Bill ETF (BIL)- Cash

This will be rebalanced quarterly to maintain the diversification. A 30 year horizon will be used.

Portfolio Visualizer

With inflation adjustment set to a max of 2% [so an investor would need self-control to not increase their budget more than 2% per year], this conservative rebalanced annually portfolio had a 86.68% chance of success over 30 years, with the worst 10% drawing it down to zero at or near the end of retirement.

However, by making one adjustment, not doing rebalancing, the success rate improved to 93.21%

Portfolio Visualizer

This is the adage of letting your winners run and ‘don’t pick your flowers to water your weeds‘. Zero rebalancing is extreme, but allowing for selective, possibly less than annual rebalancing can improve Monte Carlo simulation outcomes if you want to run a conservative 60/40 allocation and a 5% withdrawal rate.

The high-yield portfolio

If now we get into ‘high yield’ investments, more in the 6-7% range, we would need the following nest eggs:

6%- $1.6 million

7%- $1.4 million

In this case, sloughing off parts of one’s portfolio at these rates unless using a sophisticated guardrails method might be best left to closed-end funds and other high dividend funds to send you dividend and distribution checks rather than selling shares.

We’ll use 6% on this portfolio, also 60/40 bonds to stocks, but using larger yielding allocations.

Portfolio Visualizer

Using the above allocation still starts 60% equities and 40% bonds. This is also done without ramping up the bond ETF yield to more junk-like holdings. This is also not rebalanced to let the winners run, and cash is eliminated to increase and lock in the yield on longer-duration BND in this instance. I would still recommend at least a 1 year cash bucket in retirement, but this, for the sake of the Monte Carlo simulation, is convenient.

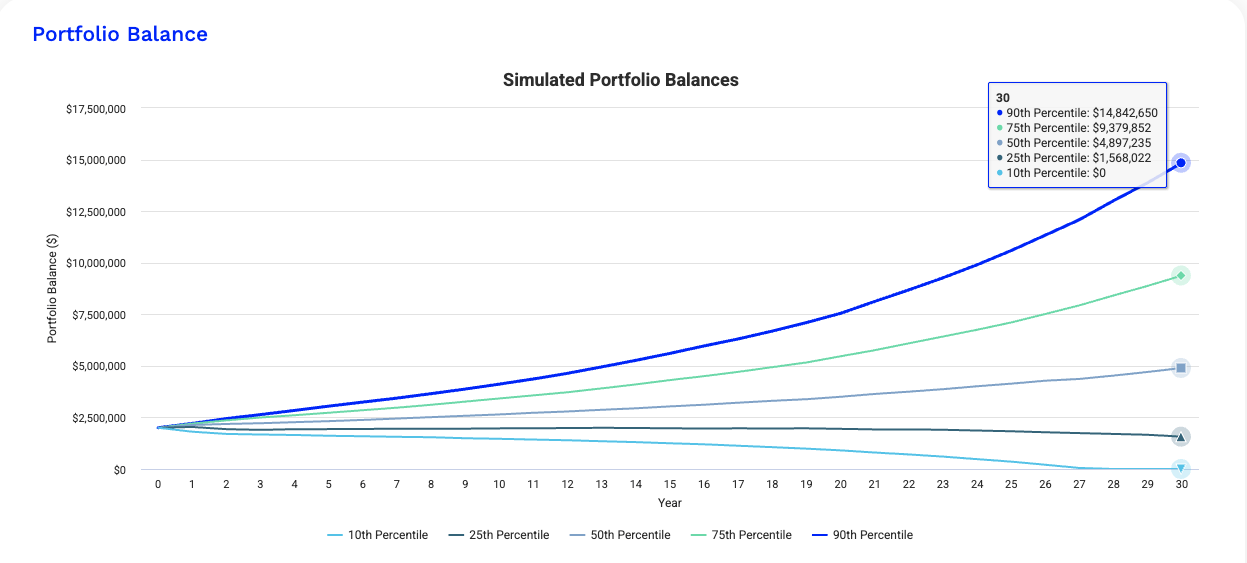

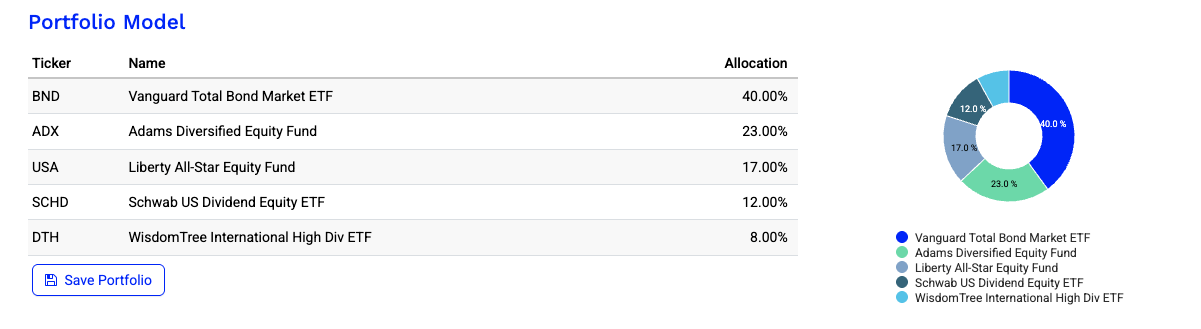

Here we have two excellent equity blend closed-end funds in Adams Diversified Equity Fund (ADX) and Liberty All-Star Equity (USA), and two dividend growth ETFs, Schwab U.S. Dividend Equity ETF (SCHD) and WisdomTree International High Dividend Fund ETF (DTH). The goal is to get the inflation adjustment bump from the dividend growth funds and assume the other yields are static. Income is received and used in this case rather than shares being sold.

This combination in this allocation had a combined yield of roughly 6% on a TTM basis.

Portfolio Visualizer

Again, with no rebalancing, the 30-year $100,000 withdrawal rate bumped up 2% per year for 30 years had a 90.6% success rate. This is pretty solid for starting out at only 60/40 [less aggressive] with a 6% withdrawal rate.

The max distribution portfolio

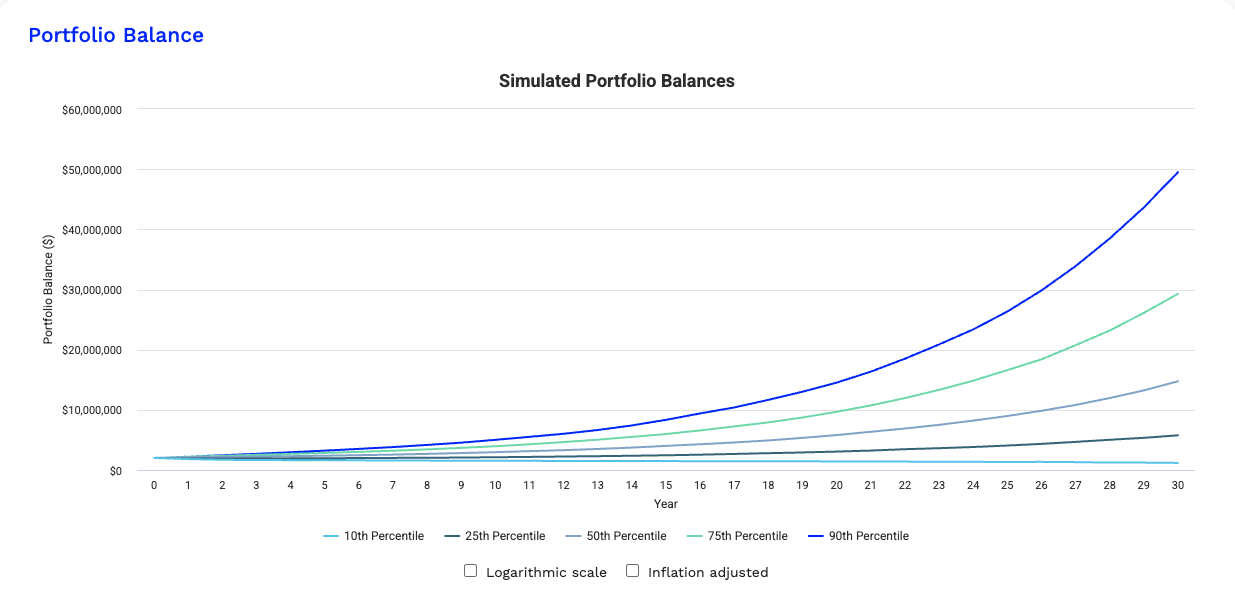

Finally, if we want to squeeze this out of an 8% yield, this would need to be more aggressive, with at least a 70/30 equity to bond portfolio in my opinion and possibly split the bonds into both high-quality US bonds and high-yield bond funds. Here’s how much we’d need at an 8% withdrawal rate:

8%- $1.25 million

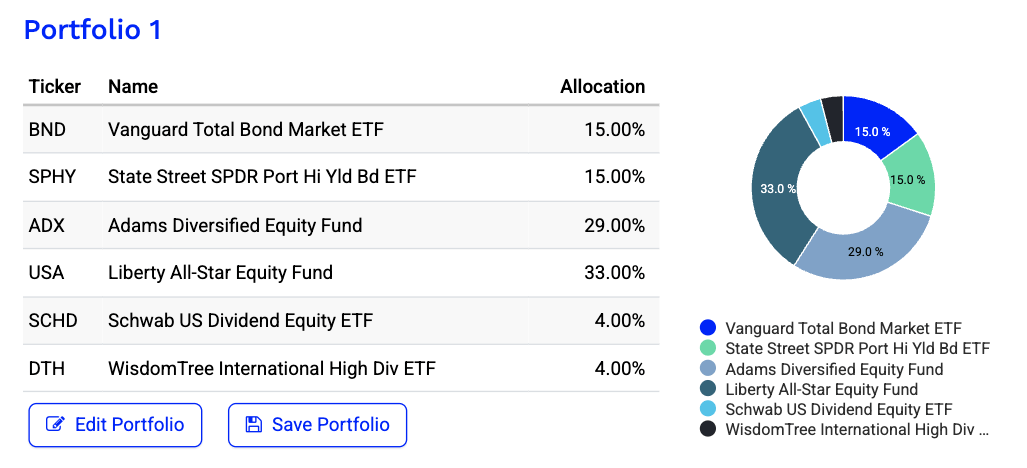

Here is the proposed mix that currently has a roughly 8% yield at current:

Portfolio Visualizer

Here, the allocations were changed to increase allocations to distribution based closed end funds and The SPDR Portfolio High Yield Bond ETF (SPHY) used for half of the bond position.

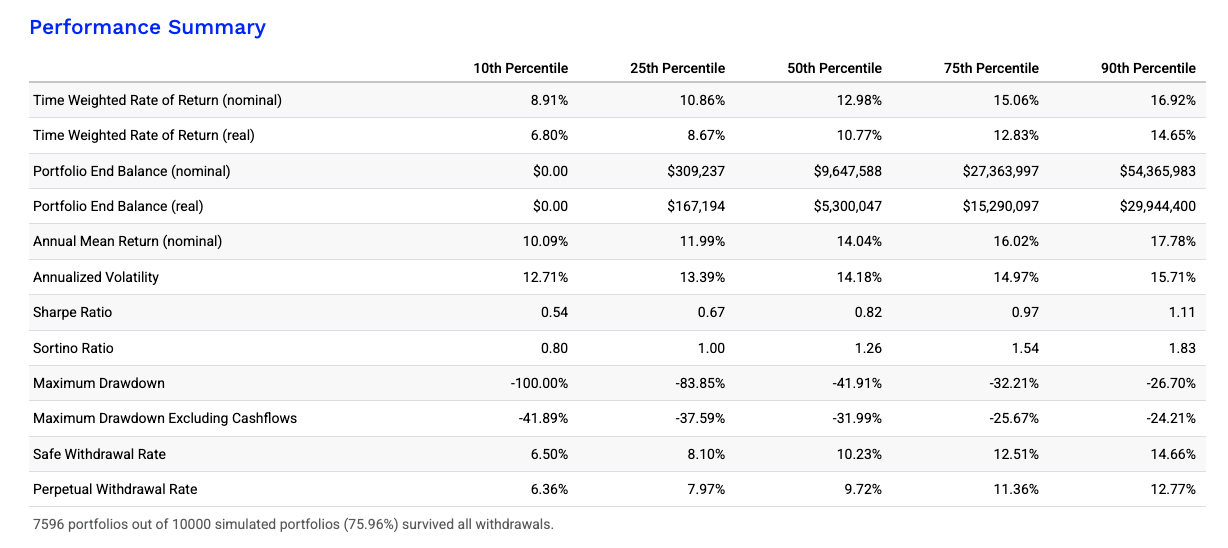

Here were the outcomes:

Portfolio Visualizer

At this high a withdrawal rate over 30 years, the results were not all that bad, as this is also adjusted for inflation. At a 75.96% success rate, the investor who has a paid off home and low fixed expenses [paid off car, etc.], this seems feasible, especially assuming social security kicks in 5-10 years into retirement and then supplements the portfolio. Social Security also has its own cost-of-living adjustments and should track this inflation adjustment well. Let’s say someone retires early on this 8% portfolio and then gets $30,000 in today’s dollars at 65 in social security. Let’s also lengthen this retirement to 40 years.

| Age | Portfolio Withdrawal | Social Security | Net Portfolio Draw | Effective Rate |

|---|---|---|---|---|

| 55 to 64 | $100,000 | $0 | $100,000 | 8.0% |

| 65 over | $100,000 | $30,000 | $70,000 | 5.6% |

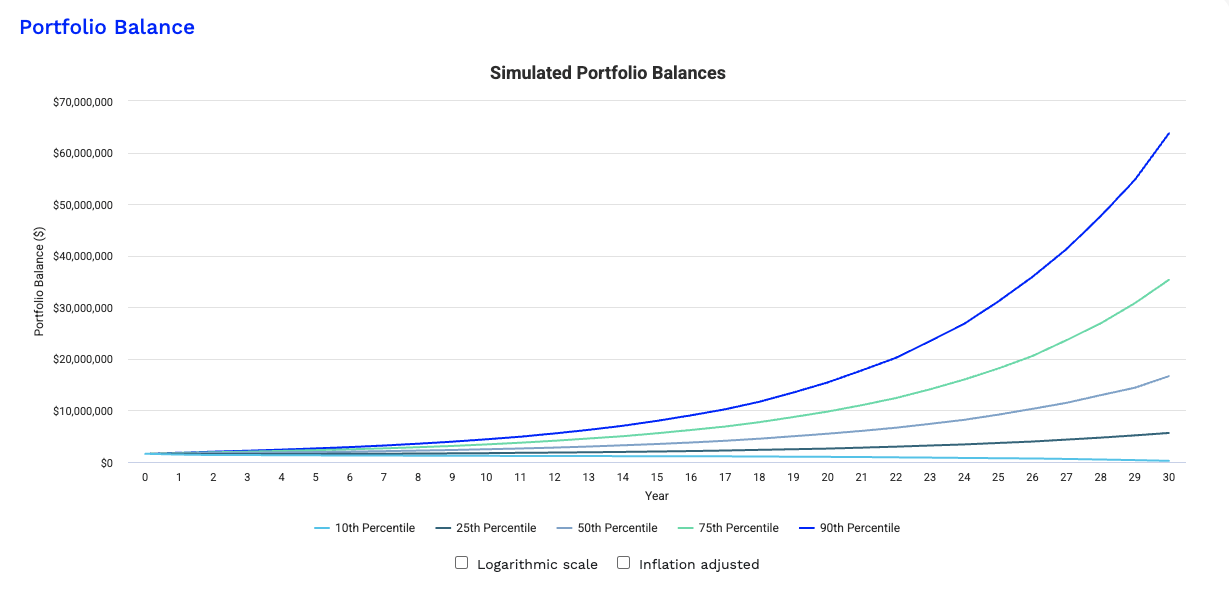

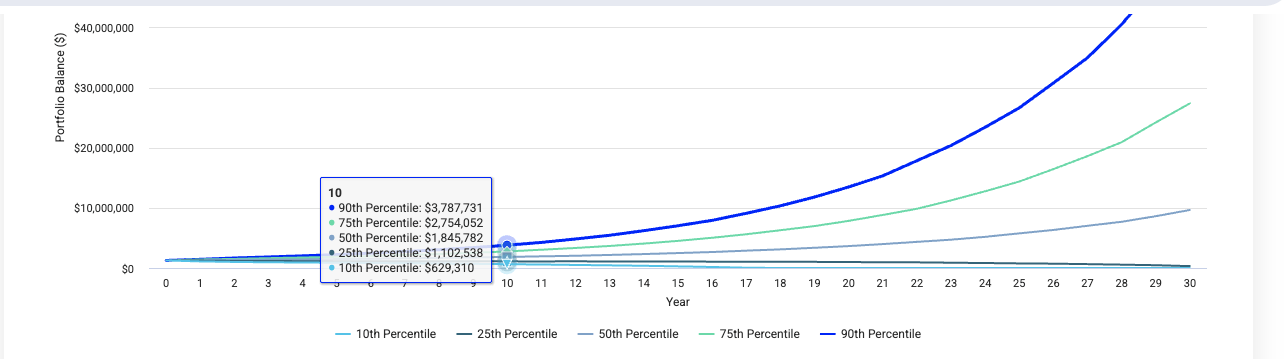

Again, with this reduction in portfolio draw kicking it down to 5.6% after the first 10 years, we’ll run this again using the 25th percentile [ a pretty poor performance] and then resetting the simulation from then for another 30 years:

Portfolio Visualizer

The 25th percentile had $1,102,538 million by year 10.

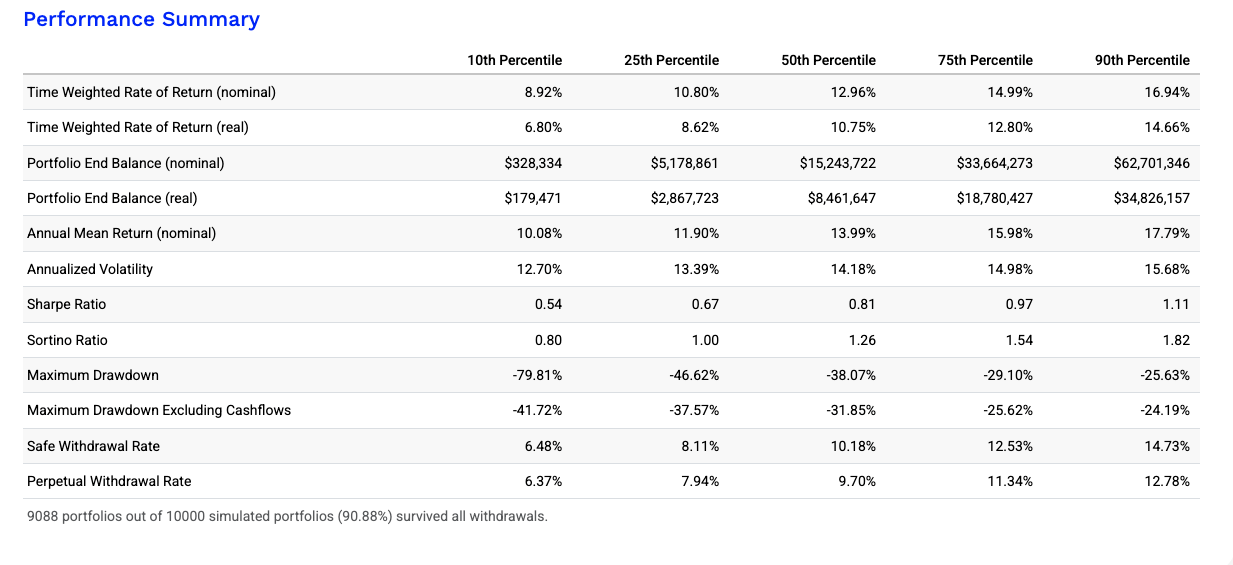

Portfolio Visualizer

In this scenario [another 30 years now starting at $1,102,538 million and $70,000 a year adjusted for inflation], the success rate is up to 90.88%. Social security is a big factor that still allows for smaller portfolios to plan for early retirement at still very comfortable incomes adjusted annually for inflation. Not that $1.25 million is small, this is a huge achievement, but this is now your own personal income factory.

Summary

There are many ways to design a portfolio for early or on-time retirement. If one is on the cusp of being able to withdraw a comfortable income at an early retirement age [say 55], don’t forget about social security stepping in to assist in the years to come [along with Medicare].

One shouldn’t be dissuaded from enjoying their retirement life earlier than normal as long as they’re comfortable with a more aggressive or income-oriented portfolio to start. Once social security kicks in, they may even be able to selectively de-risk the portfolio by reducing equity allocations and going into funds with lower dividends to enhance tax control once that social security kicks in and modified adjusted gross income becomes a factor regarding the taxation of that SS check.

Correct withdrawal strategies are also key. Having the right mix of pre-tax, taxable and tax free Roth accounts is almost as important as the right asset allocations. Nothing is impossible when everything is considered.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.