Investment Thesis

iShares U.S. Telecommunications ETF (IYZ) is a buy due to the strength of its top-weighted holdings and their durable cash flow profiles. While these established telecommunications companies will likely see less impressive growth than some top holdings of peer funds, the networks of IYZ’s top holdings are mature with stable customer bases. Additionally, these same networks are capitalizing on growth in hyperscaler demand and AI infrastructure, driving IYZ to offer a blend between capital appreciation and dividend income potential.

iShares U.S. Telecommunications ETF: Overview and Compared ETFs

IYZ is a passive ETF that tracks an index that provides investors exposure to U.S. phone, internet, and communication services companies. With its inception in 2000, the fund has 21 holdings and $1.1B in AUM. Within the communications sector, IYZ captures communications equipment (47.6% weight), integrated telecommunications services (25.4% weight), and alternative carriers (11.6% weight).

For comparison purposes, other funds examined are Vanguard Communication Services Index Fund ETF (VOX) and State Street SPDR S&P Telecom ETF (XTL). VOX is a passive fund that captures holdings focused on telephone, data transmission, cellular, and wireless communications services. I wrote on VOX over a year ago and rated the fund a buy. XTL seeks to track a modified equal weight index focusing mostly communications equipment (57% weight) and alternative carriers (20% weight). Due to its index construction, the fund has the most diversified blend of large, mid, and small-cap holdings.

IYZ Compared: Performance, Expense Ratio, and Dividend Yield

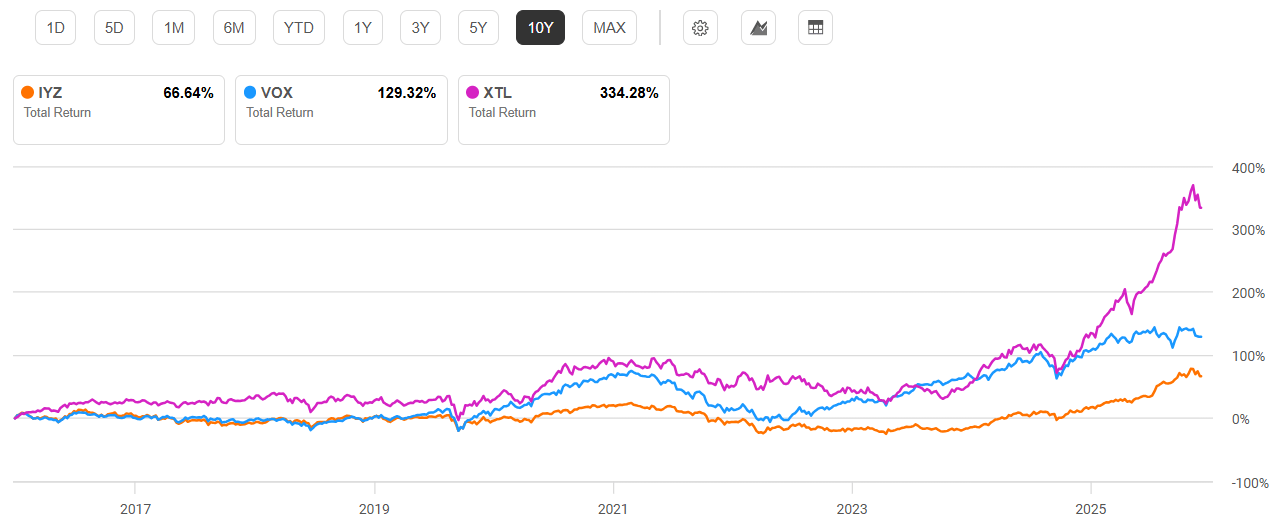

IYZ has a 10-year average annual return of 5.05%. As a result, the iShares fund has significantly underperformed both VOX and XTL with 10-year average annual returns of 9.55% and 16.54%, respectively. This underperformance can largely be attributed to the fact that IYZ has maintained heavy concentration on large, established telecommunications providers that have seen slow growth. However, for reasons I discuss in this article I believe that these top holdings are positioned for a solid rebound.

10-Year Total Return: IYZ and Compared Telecommunications Funds (Seeking Alpha)

Beyond performance, a key drawback for IYZ is its fees. With an expense ratio of 0.38%, IYZ has the highest fees compared to peer funds. However, a redeeming quality is its dividend yield, which is the highest at 1.69%. While IYZ’s 5-year dividend CAGR has been the lowest, its top holdings demonstrate income growth potential which I believe will reverse this declining dividend trend.

Expense Ratio, AUM, and Dividend Yield Comparison

| IYZ | VOX | XTL | |

| Expense Ratio | 0.38% | 0.09% | 0.35% |

| AUM | $1.13B | $5.98B | $833.73M |

| Dividend Yield TTM | 1.69% | 1.02% | 0.90% |

| Dividend Growth 5 YR CAGR | -3.70% | 16.14% | 20.06% |

Source: Seeking Alpha, 20 Jun 26

IYZ Holdings and Its Competitive Advantages

Due to the differences in each fund’s tracked index, top holdings differ significantly. IYZ’s top holdings are Cisco (CSCO), Verizon (VZ), AT&T (T), Iridium (IRDM), and Arista Networks (ANET). VOX’s top holdings are Meta Platforms (META), Alphabet Class A (GOOGL), Alphabet Class C (GOOG), and Walt Disney (DIS). XTL unique top holdings are Extreme Networks (EXTR), Viavi Solutions (VIAV), and Viasat (VSAT).

Top 5 Holdings for IYZ and Peer Communications Funds

| IYZ – 21 holdings | VOX – 112 holdings | XTL – 41 holdings |

| CSCO – 27.88% | META – 22.19% | EXTR – 5.96% |

| VZ – 11.50% | GOOGL – 14.15% | IRDM – 5.24% |

| T – 9.22% | GOOG – 7.54% | VIAV – 4.67% |

| IRDM – 5.69% | VZ – 4.43% | CSCO – 4.33% |

| ANET – 5.21% | DIS – 4.40% | VSAT – 4.01% |

Source: Multiple, compiled by author on 20 Jun 26

IYZ’s top three holdings comprise almost 50% weight for the fund. Additionally, given the fund’s track index, these top companies are likely to maintain top positions for the foreseeable future. Each of these top holdings have distinct strengths driving a positive outlook for IYZ overall.

Cisco: Capitalizing on Massive Hyperscaler Growth

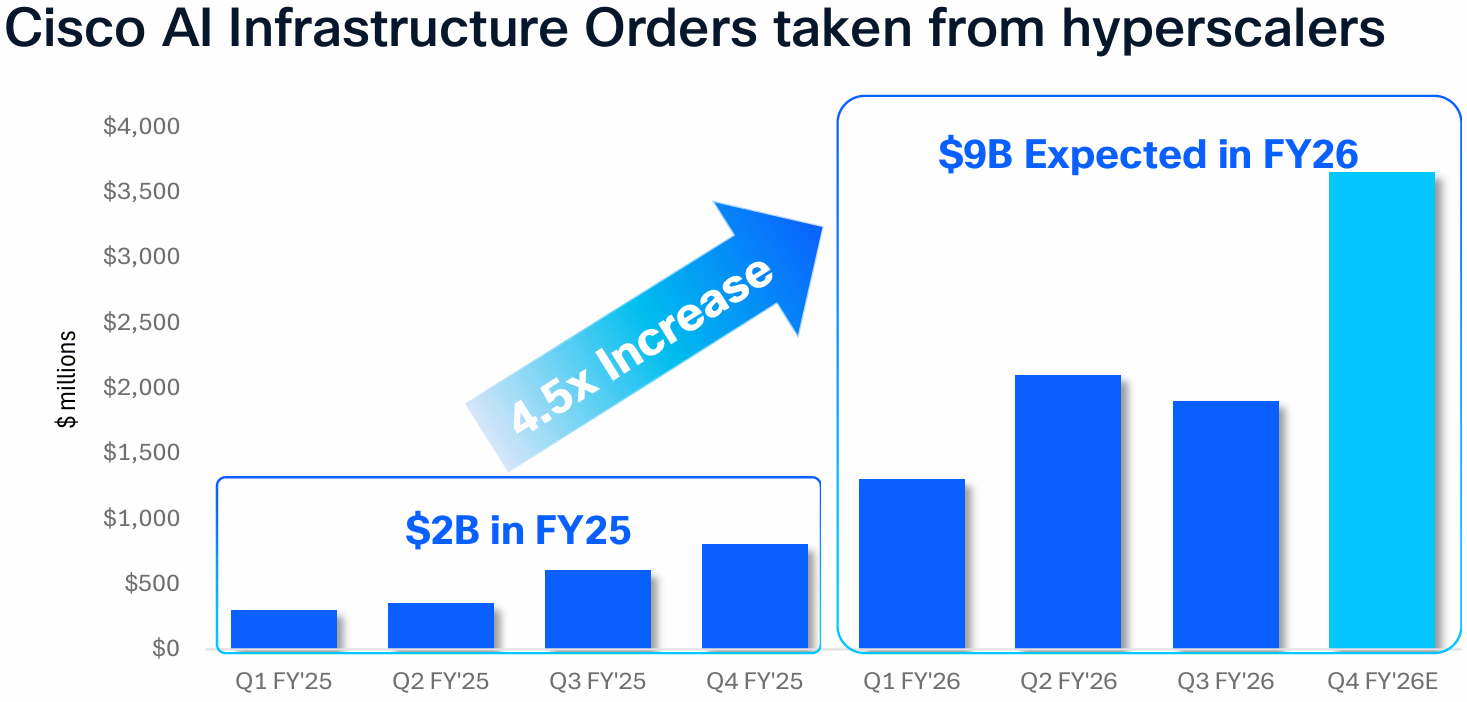

The first key holding for IYZ is Cisco Systems, an infrastructure company that strives to unify automation, AI, and security. Cisco has positioned itself as a key provider in hyperscaler AI infrastructure and AI connectivity. For instance, Cisco generated nearly $2B in hyperscaler AI orders late last year and is expecting to see $4B in hyperscaler-related revenue in FY26. These hyperscalers are experiencing strong growth driven by large-scale data center expansion required by companies like Google and Amazon (AMZN).

Cisco Growing Hyperscaler Infrastructure Orders (Cisco May 2026 Presentation)

This data center growth has driven an overall 9.2% YoY revenue growth for Cisco. The company has also been profitable with 19.7% net income margin. As a result of its growth in supplying hyperscalers and AI connectivity, Cisco has seen a one-year share price rise of 81%. CSCO’s valuation is a bit stretched with a forward P/E of 28.0x. Looking forward, hyperscaler-owned data capacity and infrastructure is expected to reach about 60% of total critical worldwide IT load by 2030. This is up significantly from just 10% in 2018. However, Cisco reduces risk through diversification in other products and services. Its total product order, excluding hyperscalers, rose 19% YoY last quarter. Therefore, Cisco represents the first strong holding for IYZ.

Verizon: Expanding Fiber Network and Healthy Dividend Yield

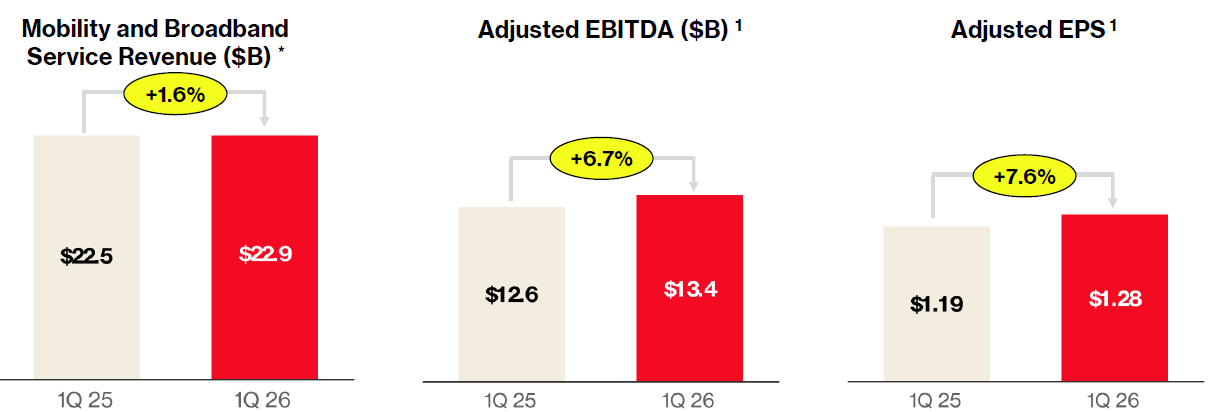

The second strong factor for IYZ is Verizon, an integrated telecommunications company that has traditionally seen muted growth over the past decade. This has been seen by its YoY revenue growth of just 2.85%. However, the carrier is seeing strong recent returns including the highest-ever adjusted EBITDA last quarter. Verizon also has been able to achieve solid profitability with a 12.5% net income margin. Over the past five years, Verizon’s share price has declined 18.7%. Verizon’s valuation is also attractive compared to the rest of the communications sector with a forward P/E of just 9.2x.

Verizon Stable Mobility and Broadband Revenue Growth (Verizon 1Q 2026 Earnings Presentation)

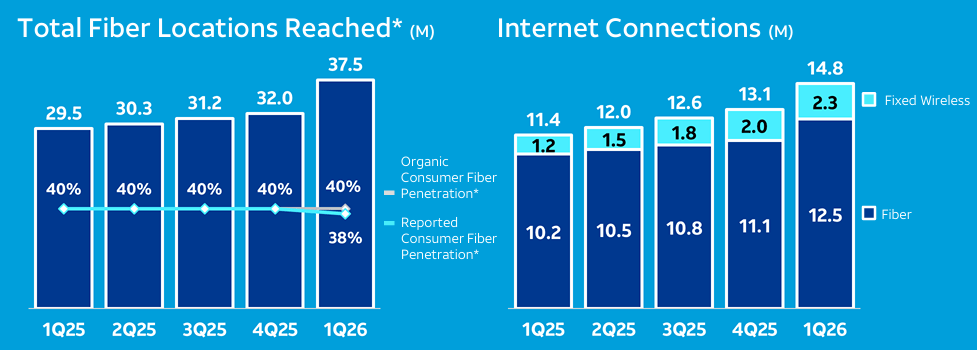

Looking forward, Verizon will maintain its competitiveness against peers like AT&T and T-Mobile US (TMUS) through its strategic acquisitions and expanding fiber internet network. This expansion includes its acquisition of Frontier Communications in February, expanding its fiber network to 31 states. Verizon also provides a solid income component to IYZ through its high 6.2% forward dividend yield. Given its profitability and healthy 57.6% dividend payout ratio, Verizon will remain a key factor for IYZ’s overall dividend yield.

AT&T: Beat Down and Ready for Rebound

The third difference is AT&T, another telecommunications provider. AT&T, like Verizon, has seen a string of unimpressive fundamental metrics. These include a YoY revenue growth of just 2.9%. Additionally, AT&T’s free cash flow has declined for three consecutive quarters while the company’s net debt has reached a recent high. As a result, AT&T’s share price has dropped by over 20% in the last year. However, there is room for optimism. AT&T has increased its convergence rate, which is the percentage of customers that subscribe to both AT&T wireless and broadband home internet services. This metric has slowly increased in recent years up to 42%. Furthermore, AT&T hit 30 million fiber locations last year, halfway to its goal of 60 million fiber locations by 2030.

AT&T Advanced Connectivity Growth (AT&T 1Q 2026 Presentation)

As a result of its share price decline, AT&T is also attractively valued. With a forward P/E of 9.5x, AT&T’s valuation is 56% lower than the communication sector’s median P/E ratio. With its growing fiber network, the company expects free cash flow to steadily rebound, hitting over $18B in 2026 and $21B in 2028. While AT&T faces fierce competition with other providers like Verizon, AT&T’s competitive advantage lies in its more affordable service plans and more widespread 5G coverage. These factors will likely perpetuate AT&T’s strong dividend yield which currently stands at over 5%.

Current Valuation and Performance Outlook

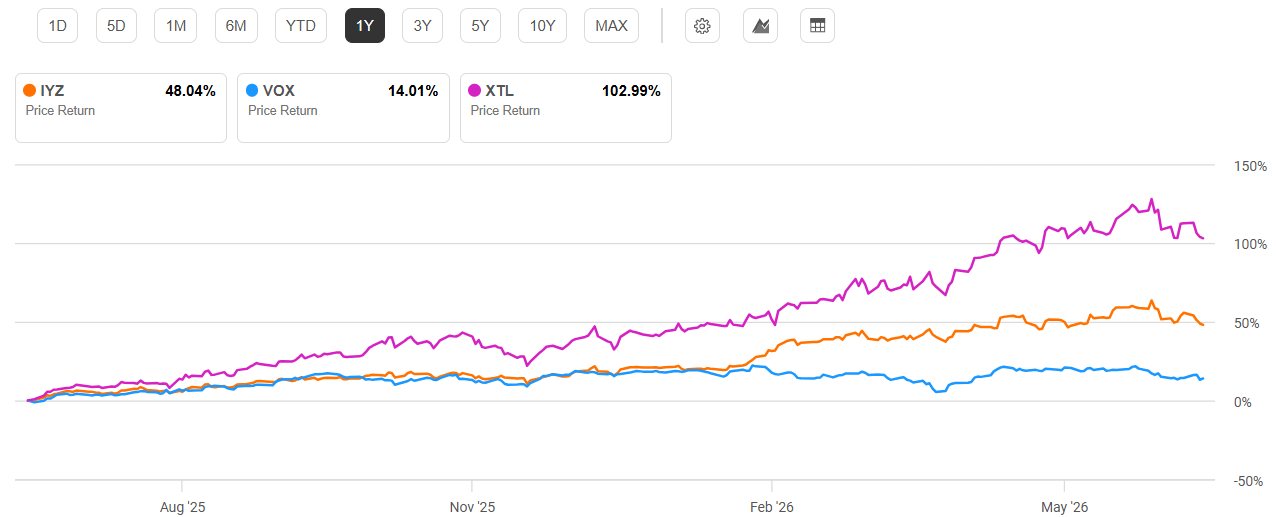

Over the past year, XTL has seen significant outperformance compared to IYZ due to its diversified blend of holdings that include amplified exposure to AI infrastructure and data centers. As a result, XTL includes companies like VIAVI Solutions and Extreme Networks that have seen one-year returns of 405% and 89%, respectively. However, these same holdings have negative or low net income margins and rely on significant earnings growth. Should these companies disappoint in future earnings, they will likely see steep declines.

One-Year Price Return: IYZ and Compared Telecommunications ETFs (Seeking Alpha)

In contrast, IYZ’s top holdings demonstrate stable cash flows with steady growth. IYZ’s overall valuation is roughly on par with peers with a P/E ratio of 18.2x. All funds examined in the communications sector are more attractively valued than the broader U.S. market as measured by the S&P 500 Index’s P/E ratio of 32x. While peer funds like XTL may see explosive returns compared to IYZ, I believe the iShares fund still warrants an overall buy ratio due to its stable income streams from subscription plans and growing networks. For this reason, I believe IYZ may underperform XTL and VOX in the short term but offer stronger and more stable returns in the long term.

Valuation Metrics for IYZ and Peer Communications ETFs

| IYZ | VOX | XTL | |

| P/E ratio | 18.24x | 18.00x | 21.46 |

| P/B ratio | 2.62x | 3.50x | 2.49 |

Source: Compiled by Author from Multiple Sources, 20 Jun 26

Risks to Investors

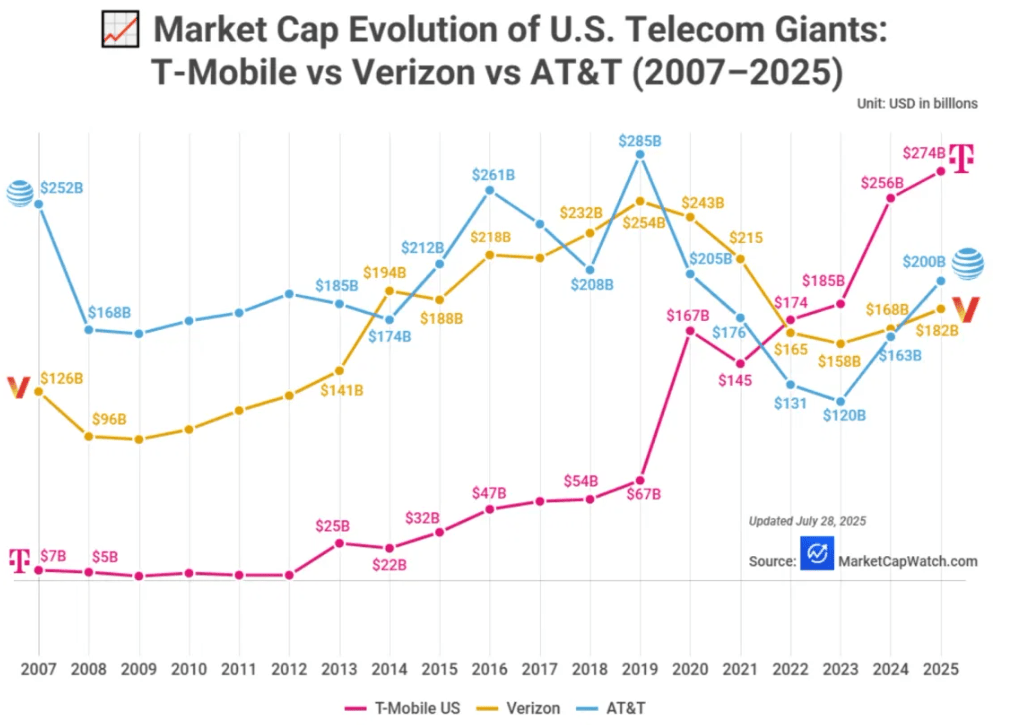

IYZ has inherent risk by being concentrated in the communications sector. IYZ’s holdings like Cisco are benefiting from growth in other sectors such as information technology. Another key risk is competitive pressure within residential and commercial telecommunications providers. After T-Mobile acquired Mint Mobile in 2023, T-Mobile’s market share surpassed both Verizon and AT&T.

Market Cap Evolution of Largest U.S. Telcom Providers (MarketCapWatch)

Given a U.S. population growth of only 0.5% annually over the past few years, these telecommunications companies must compete for roughly the same consumer base, at least within the United States. The competitive environment will perpetuate the slow, but steady growth for top holdings like Verizon and AT&T. As a result of these risk factors, investors in IYZ may face short-term opportunity costs compared to both peer funds and the broader U.S. market.

Concluding Summary

IYZ has traditionally underperformed multiple peer funds due to its concentration on established telecommunications providers. However, these top holdings offer stable cash flows while investing in growing networks. Therefore, while IYZ may see less impressive short-term returns, I believe IYZ offers investors a balanced mix of capital appreciation and income potential over the long run.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.