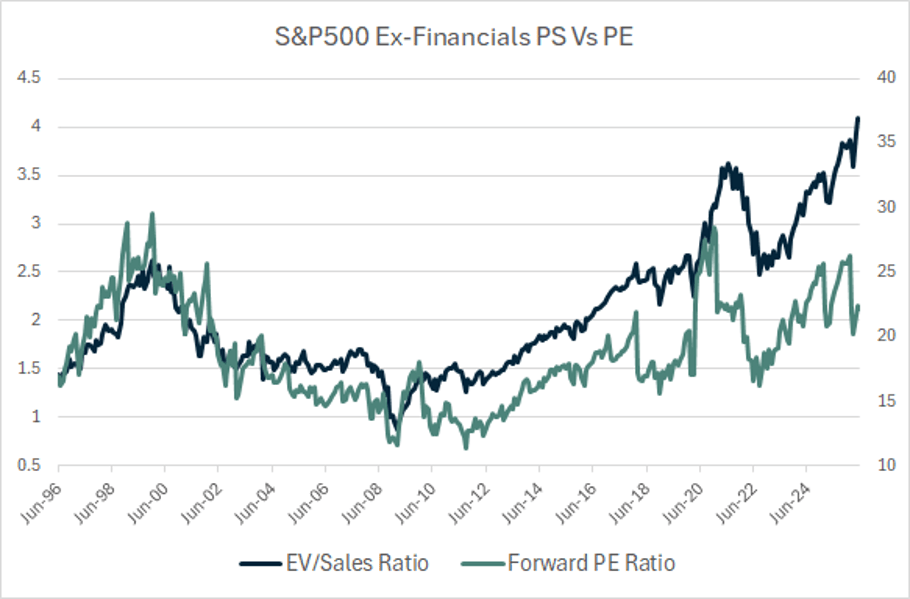

The S&P 500 (SPX) now trades at a price-to-sales ratio of 3.5x. This figure rises to 3.9x if we take into account net debt by using enterprise value rather than market cap. If we strip out financial companies, it rises further to over 4.0x, which is fully 60% above the 2.5x multiple seen at the peak of the 2000 bubble. This multiple is being justified in the minds of investors by astonishingly high expectations for profit growth driven by the AI boom, which has suppressed forward earnings multiple on the SPX to reasonable levels.

Bloomberg

The earnings boom required to justify current sales multiples would be unprecedented. Unfortunately for investors, history shows that the benefits of ‘new economy’ technological advancements overwhelmingly accrue to consumers rather than producers. There will of course be some major winners, but the market is already priced for the absolute best-case scenario. Almost half of the market’s capitalization is now represented by companies trading at over 10x sales, and 20% of the market is expected to generate negative owners earnings over the next 12 months. When sentiment eventually turns, the ferociousness of the selling is likely to shock even those who witnessed the dot-com bust.

At 4x Sales, Investors Require Unprecedented And Sustained Margin Expansion

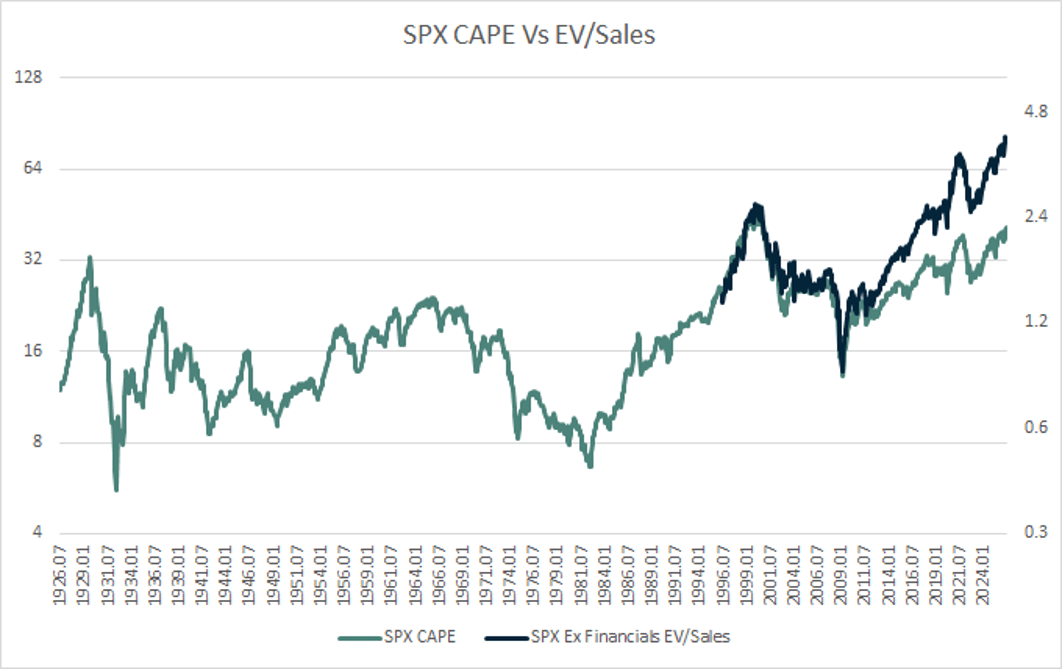

To see just how extreme 4x sales are for the S&P 500, take a look at the chart below, which compares the P/S ratio to the CAPE ratio. The CAPE ratio was designed to smooth out the impact of cyclical profit margins by taking a 10-year average, but margins have moved relentlessly higher over the past 15 years, causing the 10-year average of earnings to rise significantly relative to sales. From the mid-1990s to the early 2010s, the two valuation metrics moved in lockstep. Since then, the P/S ratio has decoupled to the upside significantly.

Bloomberg, Robert Shiller

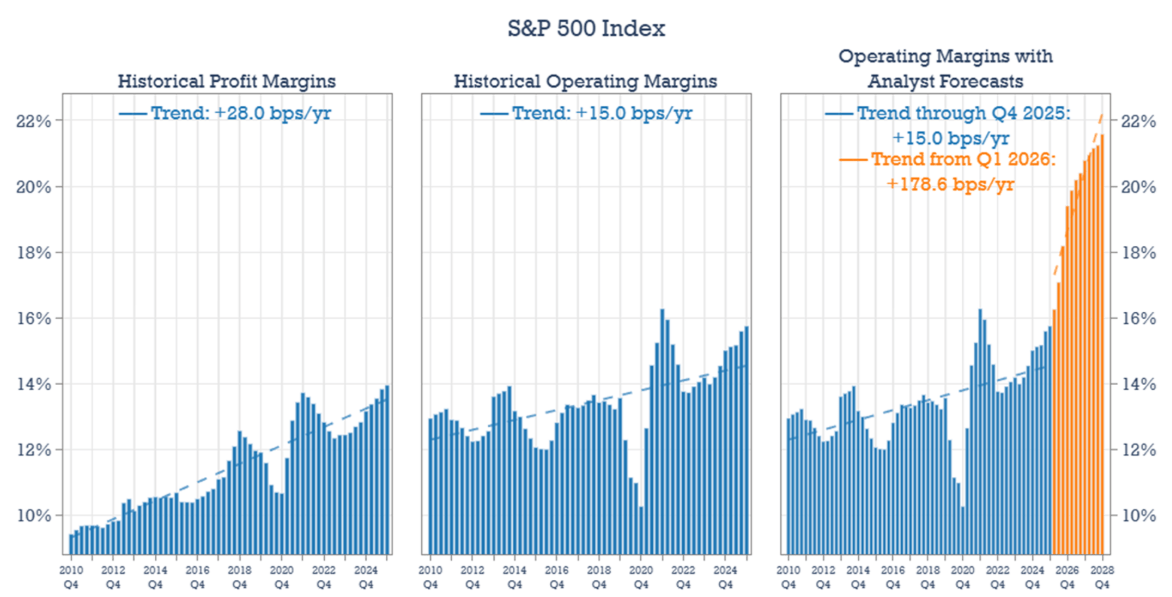

Rather than anticipating mean reversion in profit margins, investors are expecting them to rise even further, and by a lot. The following chart from Bill Hester captures the extent to which profit margins are expected to rise. According to his research, Wall Street analysts now see operating margins rising to almost 22% by the end of 2028 from 16% at present, implying net profit margins will rise to 20% from 14%.

Bill Hester, Hussman Advisors

If analysts are right, then it would mean that the SPX will grow into its current extreme P/S ratio to some degree, as it would put the index below 20x earnings by the end of 2028. To be clear, this would not make stocks cheap by any means, but it would suggest that the market is just fully priced rather than in one of the biggest bubbles in world stock market history.

Capex Explosion Will Drive Down Owners’ Earnings Margins

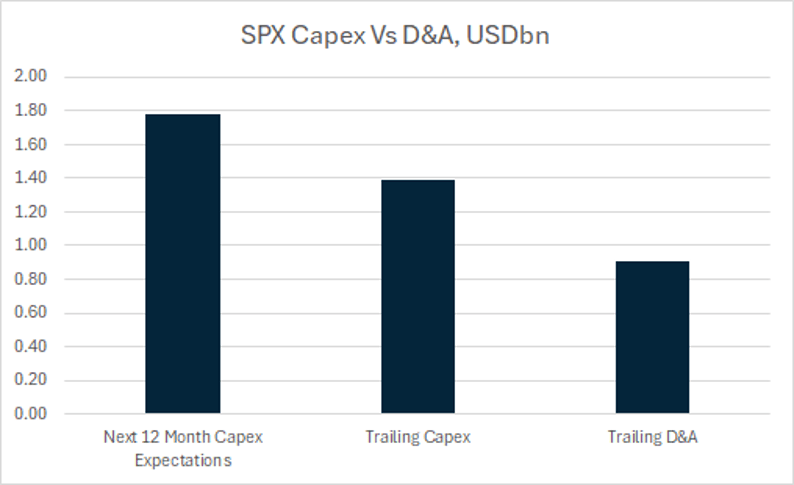

In my view, margin pressures are more likely to face downward than upward pressure. To explain this, it is important firstly to distinguish between reported earnings and actual owners earnings, with the crucial difference being reported earnings use depreciation and amortization while owners’ earnings use capital expenditure, and this difference is crucial.

D&A expenses over the past 12 months have been the equivalent of 5.6% of sales, while capex has been equivalent to 8.5%. The latter is expected to rise to over 10% next year, meaning actual owners earnings margins are likely to be around 4.5 pp lower than reported earnings even if analysts bullish estimates are correct.

Bloomberg

Bulls will argue that surging capex over the coming years is just a small price to pay, as winning the AI race will allow companies to continue expanding their operating margins. However, this is not how the benefits of technological advancements have typically been distributed. Competition tends to result in the benefits of technology accruing largely to consumers in the form of lower prices.

In this paper from 2004, William Nordhaus examines “Schumpeterian profits” – the rewards innovators capture from technological advances. Analyzing the US non-farm business economy from 1948 to 2001, Nordhaus reveals that innovators retained a mere 2.2% of the total social surplus from innovation, while consumers captured 97.8% through lower prices and improved goods.

Intense competition and AI capex spending among hyperscalers is likely to result in significant benefits to consumers at the expense of profit margins. Meta’s record capex spending aimed at undermining the monopoly position of its competitors is a good example of Nordhaus’s findings. Meta is using its massive ad revenues to subsidize a free product, capturing user engagement while destroying competitors’ pricing power. Consumer value is maximized instantly as Meta transfers the technology’s massive social surplus directly to the public.

A great example of how incredible technological advancement failing to translate into significant producer surpluses is the airline industry. One may have expected that when businesses harnessed the ability to save people countless travel hours via commercial air travel, they would have reaped the rewards in terms of extremely high profits. However, intense competition and capital investment meant that the vast majority of the benefit accrued to consumers. This is nicely captured in the following Warren Buffett quote: “I like to think that if I’d been at Kitty Hawk in 1903 when Orville Wright took off, I would have been farsighted enough, and public-spirited enough—I owed this to future capitalists—to shoot him down. I mean, Karl Marx couldn’t have done as much damage to capitalists as Orville did.”

Why A Crash Is Now Inevitable

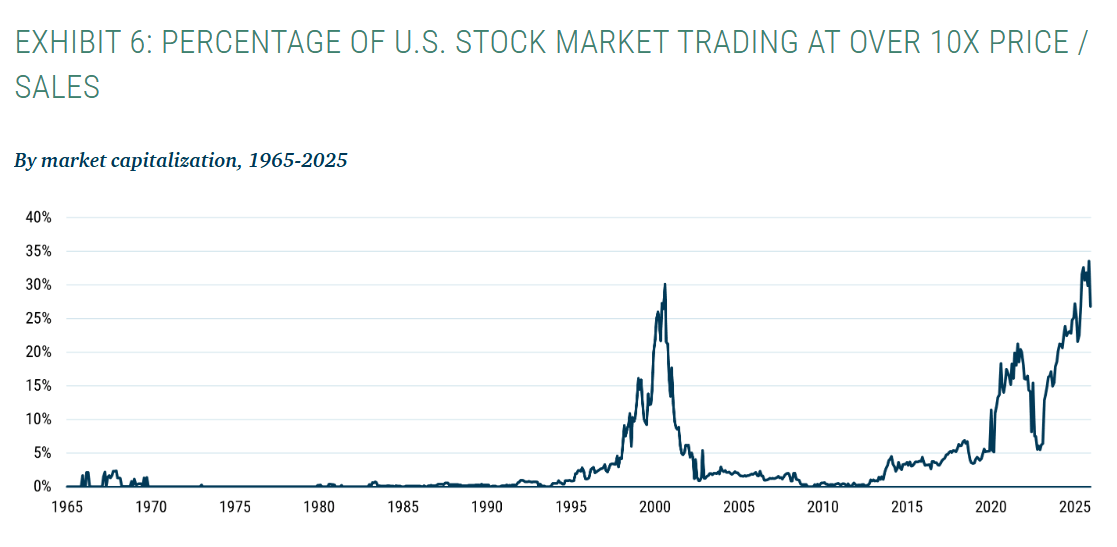

With SPX valuations at their most extreme level in history, if AI profit growth expectations do not fully materialize, we are unlikely to see stocks drift steadily lower in an orderly fashion. Certain segments of the market have become intensely speculative. For example, almost 40% of the SPX is now represented by companies that trade in excess of 10x sales, a figure that rises to almost 50% when we strip out financials.

GMO

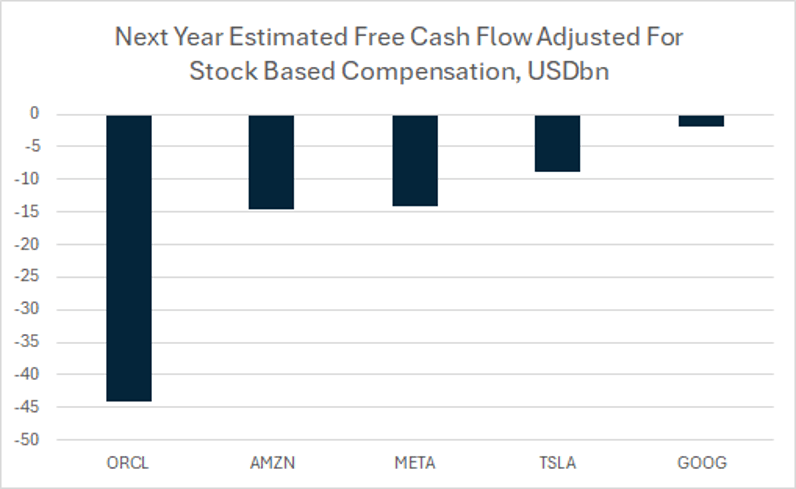

Even more concerning is the fact that 20% of the market by capitalization is expected to generate negative owners earnings over the next 12 months, including Alphabet (GOOG)(GOOGL), Amazon (AMZN), Meta (META), Tesla (TSLA), and Oracle (ORCL), due to their colossal capex plans.

Bloomberg

Such market dynamics almost guarantee systemic malinvestment. To justify such extreme valuations, these companies must grow exponentially for decades. This manic expectation forces corporate management to aggressively burn capital on unproven projects. Value investor Jeremy Grantham warns that Big Tech is locked in a historic, multi-trillion-dollar AI arms race that mirrors the 1990s Dot-com bubble and the railway mania of the 1840s. Because no company can afford to lose, they are collectively overinvesting in infrastructure far ahead of actual commercial demand that will inevitably crash. He predicts this brutal capital destruction will trigger a major financial bust for tech investors, even as the broader public reaps the technological benefits. If GMO’s latest 7-year asset class forecast turns out to be accurate, it would leave the SPX 25-40% lower than current levels in 2034.

GMO 7-Year Asset Class Forecast (GMO)

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.