As I write this, Nvidia Corp. (NVDA) sits at about $192, down from its May high above $235 and leaving investors perplexed at the market’s unwillingness to support such low valuation multiples—12 times forward sales and 22 times adjusted forward earnings. I myself did not expect such a rapid erosion of capital because my thesis has always had a much longer horizon, and it has never rested on any sort of deteriorating fundamentals or business missteps.

Indeed, despite my Strong Sell rating, which I reiterate with this piece, I assessed this as a solid business with fine fundamentals and a robust TAM that it is proactively expanding.

Unfortunately, even the most ‘accurate’ financial models are seldom, if ever, in line with real-world market sentiment. When the market has spoken and what one hears does not appear to match the numbers on one’s ticket, one should put everything down and listen.

To encapsulate the development of my thesis to date, my bearish stance on NVDA has never been about the business; it has always used the fair fulcrum of market reality. Reality as I see it, admittedly, but one can only rely on one’s own reality to make any sense of it. Therefore, it is only one of many opinions that you may treat as treasure or trash as you see fit, and as you see it fitting into your own reality paradigm.

This is the Reality I See for NVDA

Having reiterated that there is absolutely nothing significantly wrong with the business model or how efficiently things are executed therein, I should like to point out in a very strong manner that several of the risks that underscore my bearish thesis have further intensified, and my view is that the market collectively recognizes this and is pricing the stock accordingly.

There are several well-worn arguments against NVDA’s incumbent position as the dominant force in data center AI GPUs, but my view is that one should only focus on the high-momentum risks that are almost exponentially building up against this dominance. What are they, and how will they affect NVDA? That is my quest(-ion) for today.

Risk #1: Key Customers Are Transforming into Potentially Fierce Competitors

I see this as the highest-momentum risk threatening to disrupt NVDA’s data center GPU dominance in AI training workloads, but I should like to make it clear that high-momentum does not equate to imminent. That said, material developments in the last six months—particularly in the two and a half months since the “Nvidia And AMD: Trim Your Hare, Buy A Tortoise” article that I last wrote on the name—have elevated the risk to new levels, which I believe the market is now beginning to price in.

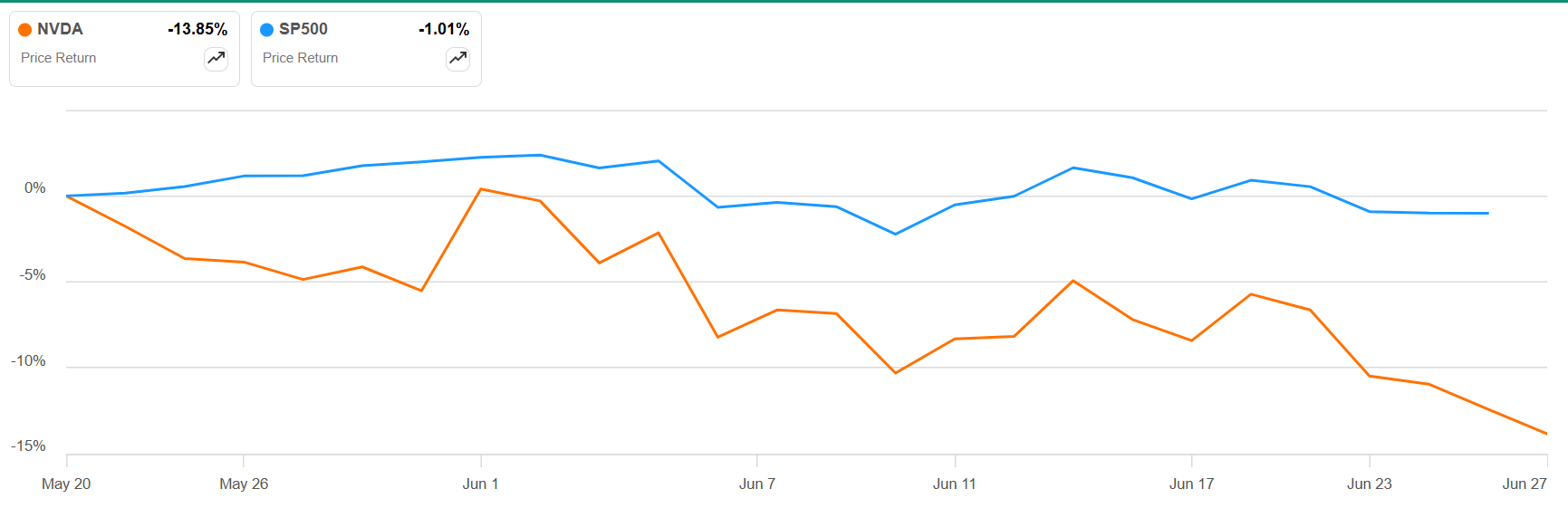

The Q1 2027 report released last month clearly indicated that NVDA’s biggest customers are still generating significant demand that allowed the company to report an 85 percent revenue spike year-on-year, driven primarily by a 92 percent increase in data center revenues.

Indeed, if management guidance is accurate, one can expect a 95 percent year-on-year growth rate from the $46.75 billion for Q2 2026 (July 2026 quarter). If the actuals come in above that, one could witness a return to the triple-digit quarterly revenue growth not seen since the July 2024 quarter, or NVDA’s Q2 2025, at which time the company reported 122 percent growth at the top.

Seeking Alpha

Unfortunately, despite the promise of this return to triple digits, the stock is down 13 percent since Q1 2027 earnings, creating a drag on the S&P 500’s (SP500) otherwise positive momentum since the trough in March.

Seeking Alpha

There is a tremendous amount of market pressure to send NVDA further down from the $190s, and the risk of its key customers simultaneously taking up their positions as competitors in the actual AI compute workload volume has further escalated in the nearly three months since my ‘Trim Your Hare’ article.

When Microsoft (MSFT), a lead player in NVDA’s court of key hyperscaler customers, initially announced in January that it had jumped to the 3nm node with its Maia 200 AI accelerator, it was a thinly veiled shot across NVDA’s bow. Of Maia, MSFT said that it (text bolded for emphasis by author):

gives developers fine-grained control when needed while enabling easy model porting across heterogeneous hardware accelerators.

One need not be a cryptographer to decipher the thrust behind MSFT’s announcement, and the ‘shot’ in question was not limited to NVDA:

This makes Maia 200 the most performant, first-party silicon from any hyperscaler, with three times the FP4 performance of the third generation Amazon Trainium, and FP8 performance above Google’s seventh generation TPU.

Of course, one should recognize that Microsoft is relatively new to custom silicon, despite having launched the Maia family as far back as 2023.

By comparison, Amazon’s (AMZN) Trainium family was announced in 2020 and available on AWS from October 2022, and Google’s (Alphabet’s) (GOOG) TPUs are more than a decade old now.

Amazon’s homebrew silicon is now operating at a run-rate of $20 billion, with total commitments as of Q1 amounting to “over $225 billion in revenue commitments for Trainium”. As a standalone business, CEO Jassy estimates its custom silicon unit’s “annual revenue run rate would be $50 billion”, and more recent corroboration comes from what is quite possibly the most credible source in the world (in-quote link from TechCrunch report):

Amazon’s AI chief Peter DeSantis told Bloomberg that AWS is in talks to sell its AI chip Trainium to other companies for use in data centers. DeSantis declined to specify which companies could be the buyers of these chips.

This narrative has now transformed from a remote possibility to an imminent threat. One could make the argument that it is not a direct threat to NVDA’s chips because of their superior performance, but yet another development, discussed as Risk #2, looms on the horizon.

Meanwhile, further amplifying that risk to NVDA’s dominance is Alphabet confirming deliveries of TPUs to third parties a little over a month ago.

The risk that this collective development poses to NVDA may not be a direct one, as I said, but the second risk is closely related to how AI compute is increasingly shifting away from high-cost GPUs. This development has also posted recent milestones, and it runs parallel to another transition in the form of a shift from compute-intensive AI training to the rapidly expanding AI inferencing and agentic AI markets.

Risk #2: Parallel Transitions – Away from GPUs, Away from Training

These parallel transitions are marked by the emergence of ASICs and CPUs as being more suited to AI inferencing workloads, which now make up “two-thirds of total AI compute demand, up from about one-third in 2023, and is expected to reach 70%–85% by 2028–2030.”

The magnitude of this risk is double for NVDA because it dominates the AI datacenter GPU space for training large frontier models, so these transitions present a dual challenge to future revenues and thereby the cash flows that currently support a forward multiple of 22.5 times.

We have just seen how ASICs from the hyperscalers are making inroads into the custom silicon market, and a more recent threat has come from CPUs.

Inference, especially for agentic AI, involves task orchestration, tool invocation, multi-step logical reasoning, and sequential decision-making. These workloads rely heavily on complex logic control and serial processing, areas where CPUs shine.

It is the shift to inferencing over training one sees with AI workloads that has been instrumental in enabling this relatively new risk to emerge against the NVDA bull narrative. So much so that it prompted NVDA to counter it with a recent announcement that “the world’s technology leaders are planning to adopt NVIDIA Vera, the first CPU built for AI agents.”

The company clearly recognizes this, albeit as a market to capture demand, but my view of it is as a hedge against AMD’s EPYC. A more detailed review of these competing products can be found in my May article on Advanced Micro Devices (AMD), titled “3 Things Favor This Nvidia Competitor.”

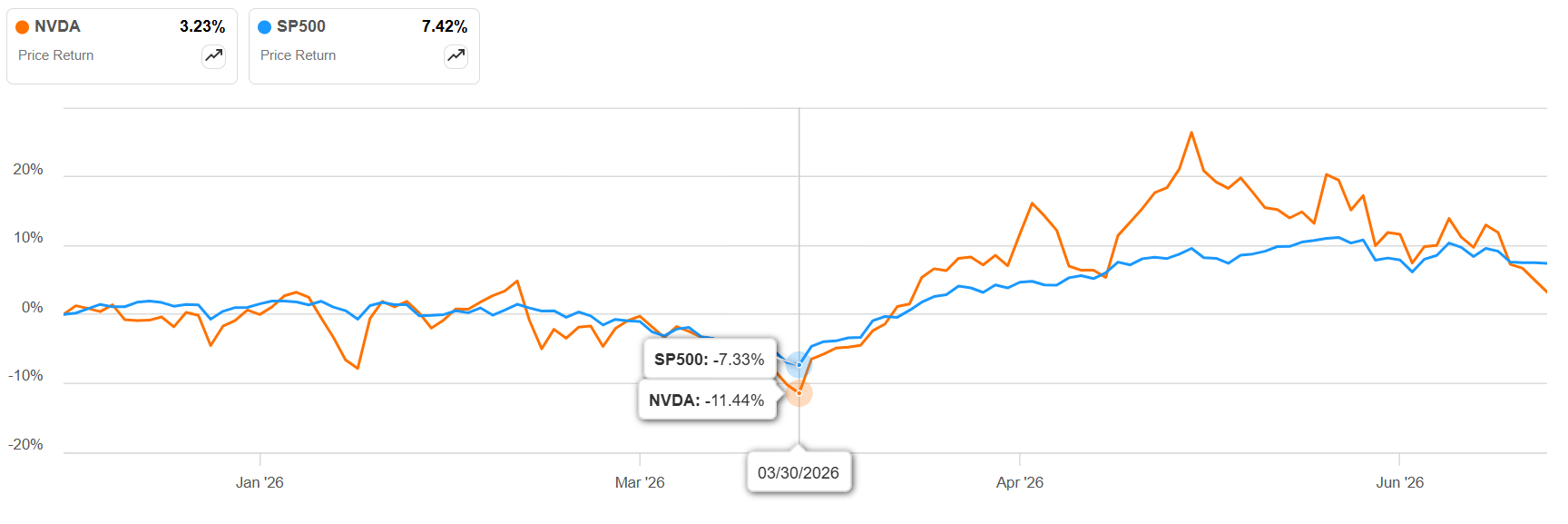

This dual risk is clearly gaining momentum against NVDA even as Risk #1 is now in motion. But there is a third risk that essentially forms the basis for my Strong Sell rating on NVDA. I believe it is worth reiterating this risk because it is increasingly becoming more material with the stock down again, significantly below the $200 that it initially breached in late October 2025 and again in April of this year.

Risk #3: The Opportunity Cost Deepens

If you have not followed my work on NVDA, I should like to make it amply clear that my Strong Sell does not imply a recommendation to sell off completely. My recommendation has always been to trim the fat if NVDA has grown into a large component of one’s portfolio. It does not make sense to stay away from the stock, but it does seem prudent to limit one’s exposure to an equity that has been ranging since October 2025 despite large moves to the upside and downside.

The opportunity cost of holding a large allocation of NVDA is yet another downside catalyst that has transitioned from possible to probable to likely as one continues to maintain one’s position. A simple back-test is sufficient to highlight this risk.

Portfolio Visualizer

If NVDA continues to decline, the opportunity cost will deepen over that time-window, so if one does not use capital appreciation in other QQQ equities, for example, as a hedge against this opportunity cost, one could be paying a heavy price without being aware of it.

A Thought (or Three) in Parting

Three key risks now pressure NVDA stock, so while its fundamentals get stronger by the quarter, until the market is willing to pay for that strength, the opportunity cost risk will persist. The other risks are significantly more material and are progressively weakening the bull case foundation.

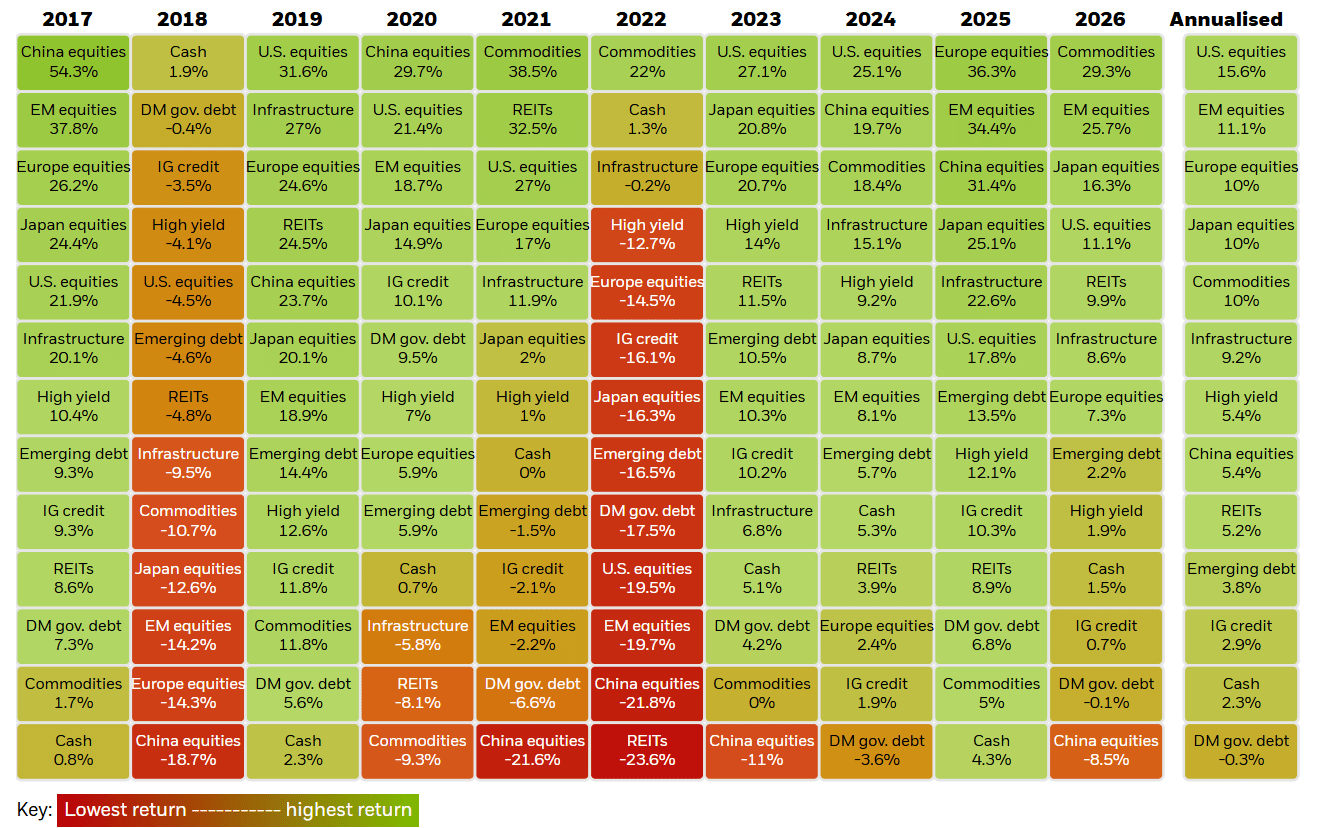

The gist of my NVDA Strong Sell is to avoid keeping all one’s eggs in the same basket. Diversification is essential, and per BlackRock’s Asset Return Map, one sees opportunities in both the broader U.S. equity market as well as commodities, emerging markets, and other asset classes. For clarity’s sake, the 2026 column is the year-to-date return, with full-year projections in the Annualized column.

BlackRock

Thank you for reading; I truly appreciate the patronage.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.