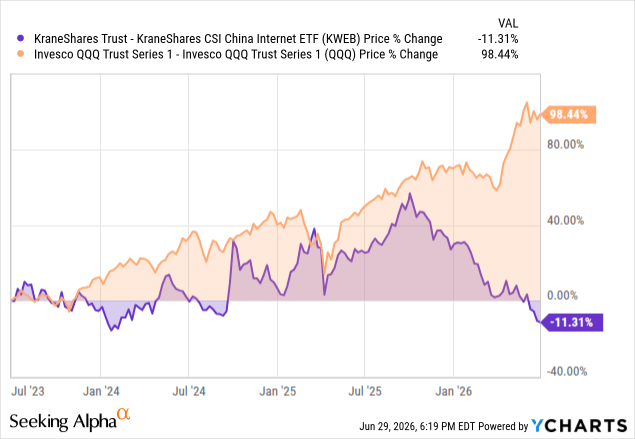

The KraneShares CSI China Internet ETF (KWEB) offers a focused, passive investment strategy in Chinese companies that mainly operate in the internet space and related technologies and are listed mainly on the Hong Kong Stock Exchange, NASDAQ, and NYSE. KWEB is managing $4.76 billion of net assets with an annual expense ratio of 0.70%. The index-tracking fund utilizes a modified free float market capitalization-weighting approach to track the performance of the CSI Overseas China Internet Index. KWEB is a concentrated ETF where the ten most significant positions consist of market leaders like PDD Holdings Inc. (PDD), Tencent Holdings Limited (TCEHY), Alibaba Group Holding Limited (BABA), Meituan (MPNGF), and NetEase, Inc. (NTES) represent about 64% of the portfolio. In terms of the sector allocations, KWEB is heavily weighted towards consumer cyclical (46%) and communication (39%). Therefore, KWEB is vulnerable to the developments in the domestic consumers’ sentiment and regulatory changes. Currently trading close to its 52-week low, the ETF has been facing a lot of challenges, generating a negative total year-to-date return of about -28%.

The Fund

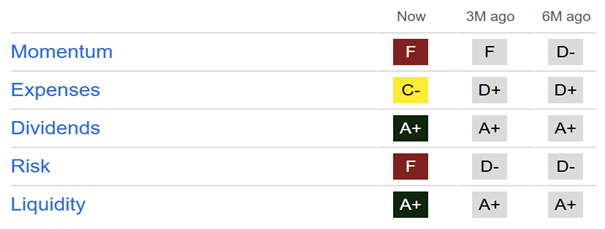

Regarding the fund itself, the expense ratio is 70 basis points, and it earns a Seeking Alpha C- Expense Grade. Liquidity is excellent, with an average daily dollar volume on a 3-month basis around $722 million and an AUM of $4.76 billion, earning it a Seeking Alpha A+ Grade. In terms of the Dividend Grade, it earns a Seeking Alpha A+ Grade, with a high trailing dividend yield of 8.76% and a rather excellent track record of 43.73% CAGR over a 10-year period.

Seeking Alpha

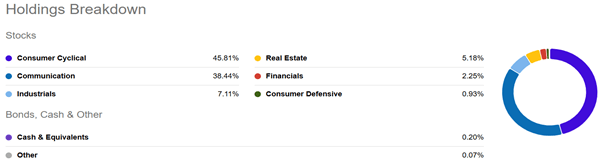

Regarding fund holdings, the fund is fully invested in equities. The bulk of the fund is formed by the Consumer cyclical and Communication sectors, with 45.81% and 38.44%, respectively.

Seeking Alpha

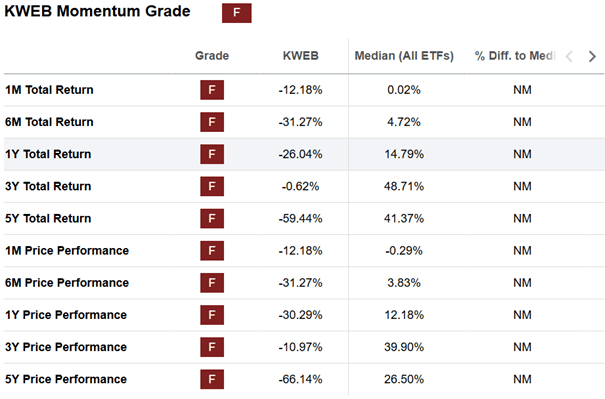

In terms of performance, well, it hasn’t been going well for the fund. The fund has underperformed the median ETF largely on every time scale, with a specifically awful period being the last 6 months, making this a rather contrarian play at this point.

Seeking Alpha

In the past I did a piece on Invesco China Technology ETF (CQQQ), and I recommend you check it out if you are interested in this theme. I will shortly go over some of the potential catalysts already reviewed in that article since the two are peer funds covering largely the same investment space. Given that the fund encompasses growth companies, we will go over the long-term perspective also.

Increasing AI Investments And Strong Earnings

China has an ever-expanding AI space, showcased by financial results from Alibaba Cloud, growing 36% year over year and sales of AI-related products growing triple digits in ten consecutive quarters. Tencent is spending RMB 18 billion on AI in 2025, and the plan is that figure to double in 2026. Baidu’s AI segment revenues are growing and make up around 43% of its total revenues, compared to 26% the past year. Continued monetization of AI services and products, therefore improving earnings results, will surely be a powerful catalyst in the period ahead, especially for companies such as Tencent or Alibaba.

Government Support

The Chinese government, realizing the potential and national importance of next frontier technologies, is stepping in with fiscal aid and support. Specifically, 1.3 trillion yuan of fiscal spending is directed towards science and technology development, with the goal of the technology space reaching over 10 trillion yuan in AI industry valuation by the end of the 15th Five-Year Plan. Short-term fiscal aid of $51 billion is directed to promote consumption and investment with initiatives such as swapping old for new devices and appliances, benefitting companies such as Alibaba, JD.com, and Meituan.

China In The AI Race

The most structurally compelling long-term driver for KWEB will be the China AI race. KWEB has the most actively used AI companies by the user base globally: Alibaba, Baidu, and Tencent own one of the ten most-used AI applications on a monthly active user basis as of January 2026. Qwen, the large language model owned by Alibaba, surpassed 700 million downloads and became the most downloaded AI system in the world. Baidu’s ERNIE Bot, Tencent’s Hunyuan, and K-ling AI owned by Kuaishou are making cloud technology popular among Chinese enterprises. Revenues related to cloud and AI increased by 12% in 2025 for KWEB constituents. The data advantage is huge here, as China had an increase in annual data volume with a CAGR of 26% from 2022 to 2026, being the first place worldwide. In the long run, once the monetization of AI becomes more prominent than investments, margins are expected to expand.

Valuation

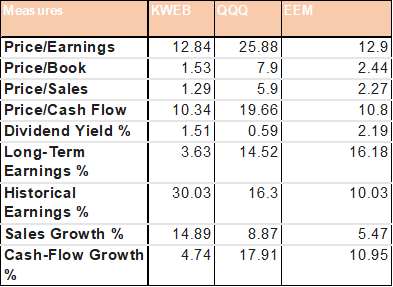

Valuation is particularly attractive, given its enormous discount to the Nasdaq and trading at par with Emerging markets as a whole on a P/E basis. The fund looks cheap on a P/B and P/S basis also, while historical earnings and projected sales growth are strong.

Morningstar

We have to pair the valuation case to the VIE structure, which means that investors own economic interests and not actual equity in Chinese companies.

Risks

KWEB is faced with various risks, which include regulatory uncertainty, geopolitical factors, macroeconomic weakness, and market dynamics. The biggest risk is China’s regulatory action since internet platform companies continue to be exposed to sudden changes of policies implemented by the Chinese government. This was evident through past regulatory actions against internet-based companies like Alibaba Group and Tencent when the companies’ earnings and valuation multiples were affected. Another important risk is geopolitics between the U.S. and China, which includes sanctions, tariffs, risks of ADR delistings, and export control on semiconductors. Though KWEB does not hold chip companies, the major portfolio holdings need AI and cloud computing capabilities, which might be hindered by the inability to access high-performing chips from NVIDIA.

Furthermore, the legal risks associated with KWEB come from the extensive use of Variable Interest Entity (VIE), in which the ownership by foreign investors is via contractual claim of offshore vehicles, instead of equity ownership of Chinese companies, hence raising doubts on shareholders’ rights under worst-case scenarios. From a macro standpoint, KWEB will always be very much susceptible to the performance of consumer demand in China, especially with the negative influences of the weak property market, deflationary environment, slow credit growth, and low consumer confidence on the sector. Lastly, there are valuation and sentiment risks attached to KWEB, as although it may look cheap compared to the technology stocks in the US, the fund could still be a value trap as long as international investors are giving a permanent valuation discount to Chinese stocks.

Conclusion

KWEB presents an interesting theme: world-class tech generating real earnings trading at half the valuation of its western peers, with structural tailwinds arising from AI commercialization, a supportive policy environment, and hundreds of millions of AI users, which are undermonetized. However, KWEB has been an underperforming theme for the past five years; the VIE structure and ADR delisting risk are still present, and U.S.-China relations have been at a low point for the past period. Given the risks, even though long-term perspectives remain compelling, I rate the fund a HOLD.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Enjoyed this article? Sign up for our newsletter to receive regular insights and stay connected.